Generative AI in the Enterprise Market By Technology (Deep Learning, Generative Adversarial Networks, Cloud Computing, and Others), By Deployment Mode (Cloud-Based and On-Premises), By Application (Content Generation, Design & Creativity), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2024-2033

-

37867

-

April 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

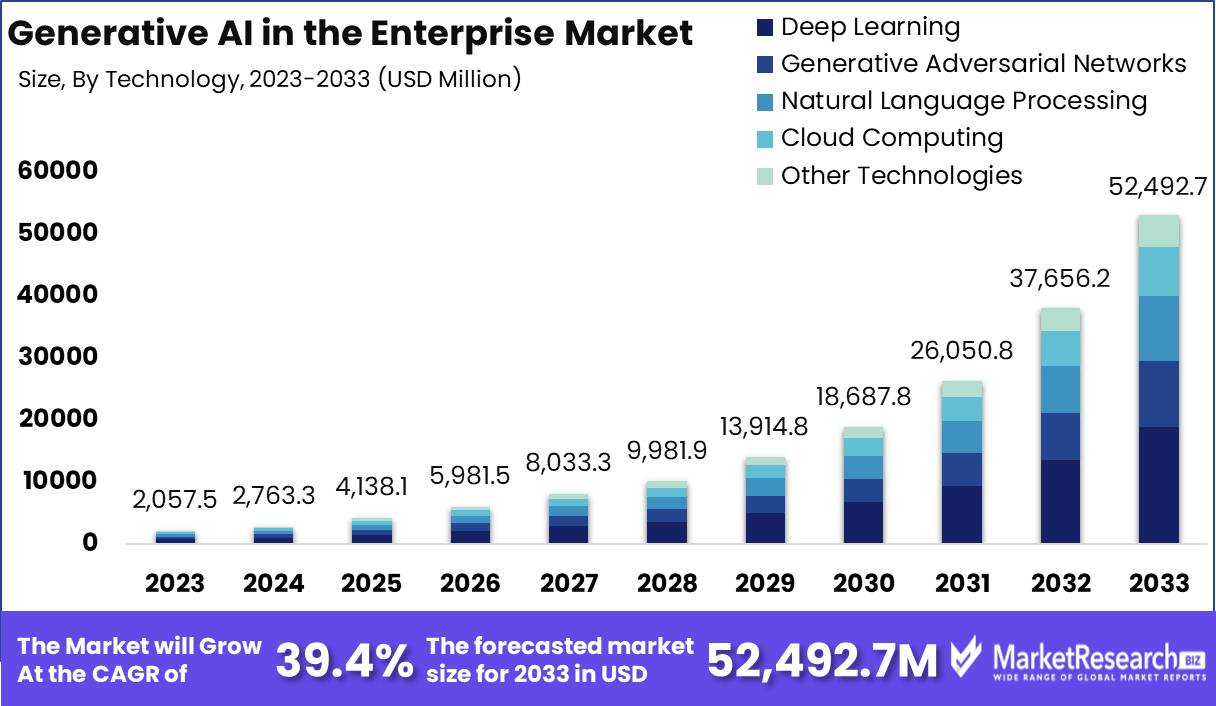

The Generative AI in the Enterprise Market size is expected to be worth around USD 52,492.7 Mn by 2033 from USD 2,057.5 Mn in 2023, growing at a CAGR of 39.4% during the forecast period from 2024 to 2033.

The surge in demand for advanced technologies and the rise in several market industries are some of the main key driving factors for generative AI in the enterprise. Generative AI in the enterprise refers to the applications of artificial intelligence technologies to automate and improve different business methods starting from customer services and sales to product development and decision making. It uses advanced algorithms and machine learning methods to produce new insights, content, and solutions.

In an enterprise context, the generative AI Model makes enterprise organizations simplify operations, enhance productivity, and propel new innovation by automating monotonous tasks, augmenting resource allocations, and identifying novel opportunities. By analyzing large datasets and learning from patterns, generative AI systems can develop customized experiences for customers, forecast market trends, and facilitate data-driven decision-making. It has the potential to extend all across diverse domains that comprise of natural language processing, computer vision, and forecasting analysis and offers a versatile accessory for solving difficult business challenges and getting a competitive edge in a rapidly growing market.

According to Study in October 2023, highlights that by 2026, more than 80% of enterprises will implement generative artificial intelligence application programming interfaces models, and deploy GenAI-enabled applications in production environments, up from less than 5% in 2023. By 2026, organizations that operationalize AI transparency, trust, and security will see their AI models achieve a 50% improvement in terms of adoption, business goals, and user acceptance.

Moreover, an article published by Oreilly in November 2023, highlights that 67% of those surveyed report that their companies are currently using generative AI, and over a third of this group (38%) report that their companies have been working with AI for less than a year. Data analysis (70%) and customer-facing applications (65%) round out the top three use cases for generative AI in the enterprise right now, with additional nods to the technology’s help in generating marketing (47%) and other forms of copy (56%).

Generative AI in enterprises enhances workflows, automates tasks, and improves decision-making methods. It nurtures new innovation by producing novel solutions and insights. Moreover, it customizes customer engagements, forecasts market trends, and enhances efficacy, ultimately propelling growth and competitiveness in vigorous business Models. The demand for generative AI in enterprises will increase due to its requirement in several verticals of industries that will help in market expansion in the coming years.

Key Takeaways

- Market Value: Generative AI in the Enterprise Market size is expected to be worth around USD 52,492.7 Mn by 2033 from USD 2,057.5 Mn in 2023, growing at a CAGR of 39.4% during the forecast period from 2024 to 2033.

- Based on Technology: Generative AI drives 30% enterprise market growth via adversarial networks

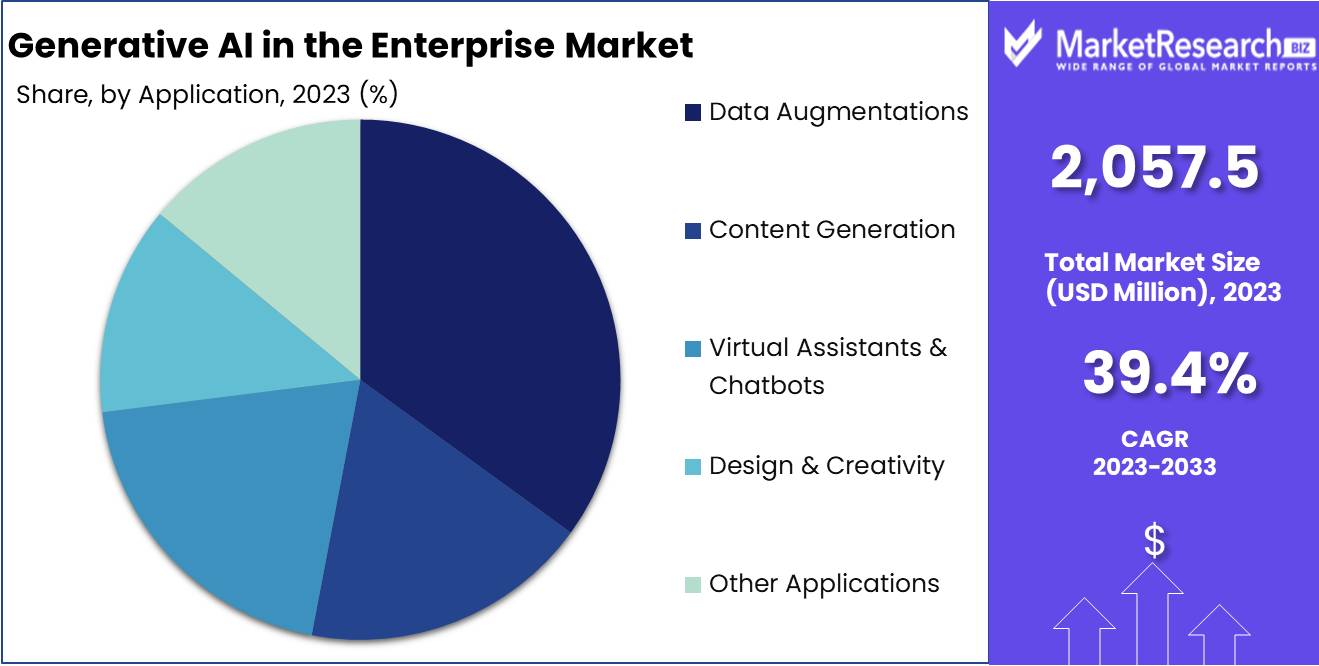

- Based on Application: Data augmentation applications lead, holding 35% of the generative AI market.

- Based on Deployment Mode: Cloud deployment dominates with 58% in the enterprise generative AI market.

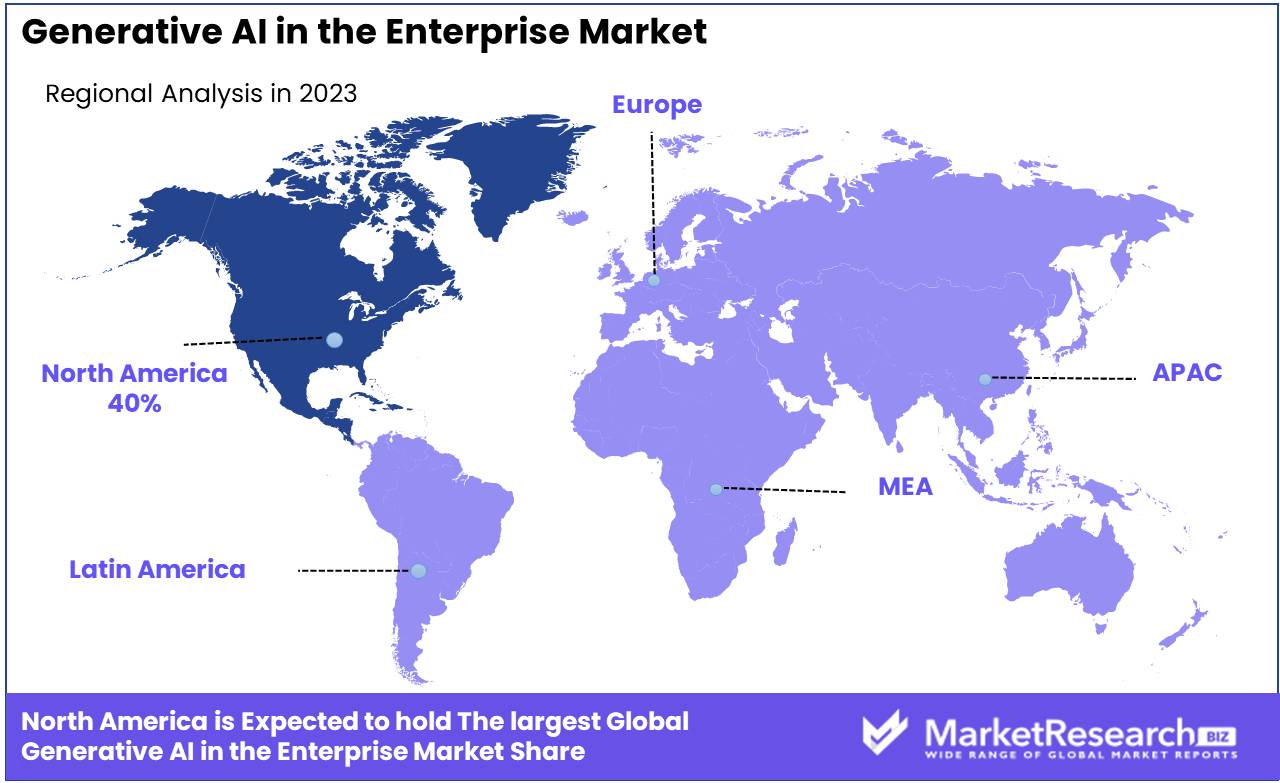

- Regional Analysis: North America holds 40% of the enterprise generative AI market.

- Growth Opportunity: In 2023, the global generative AI market is poised to revolutionize creative sectors by enhancing design and creativity, while also improving data analysis and decision-making, thereby enabling enterprises to optimize operations, innovate, and maintain a competitive edge.

Driving factors

Enhanced Customer Interaction through AI Integration

The deployment of AI-powered chatbots and virtual assistants is revolutionizing customer engagement across various sectors. These tools enable real-time, personalized interaction, significantly enhancing user experience and satisfaction. By automating routine inquiries, companies can allocate human resources to more complex issues, thus increasing efficiency and effectiveness. For instance, a chatbot capable of handling thousands of interactions simultaneously not only reduces operational costs but also improves customer response times. The impact on the market is substantial, as businesses that adopt these AI solutions often see increased customer loyalty and a boost in sales due to improved service quality.

Strengthening Fraud Detection Capabilities

AI-driven analytics are pivotal in the realm of fraud detection, offering companies a robust defense against financial and data breaches. By utilizing advanced machine learning algorithms, these systems can analyze patterns and anomalies that would be difficult for human auditors to detect. This capability is increasingly important as businesses expand digital operations and face more sophisticated threats. The adoption of these AI systems not only protects companies from potential financial losses but also safeguards their reputation, which is crucial in maintaining customer trust and confidence. The market growth driven by this need for enhanced security measures is significant, as enterprises invest heavily in AI to ensure regulatory compliance and risk management.

Automation in Content Generation

Generative AI's ability to automate content creation represents a transformative shift in how businesses produce and manage their digital content. This technology can generate written articles, marketing materials, and comprehensive reports with efficiency and scale, freeing human talent to focus on strategic and creative tasks. As generative AI tools continues to evolve, it promises not only to enhance the quality of content but also to reduce the time and resources spent on content production. This capability is especially valuable in marketing and communications, sectors where content is critical for engagement and brand positioning. Consequently, the demand for generative AI in the enterprise sector is growing as companies seek to leverage these efficiencies to gain a competitive edge.

Restraining Factors

Navigating the Challenges of Technical Complexity in Generative AI

Generative AI systems, particularly those designed for enterprise applications, often encompass complex architectures involving billions or even trillions of parameters. This complexity translates into significant challenges for enterprise organizations, not only in terms of the technical expertise required to develop and maintain such systems but also in the substantial financial investment necessary for their implementation.

The technical barriers include the need for advanced computing infrastructure and skilled personnel capable of managing and optimizing these sophisticated AI models. As a result, the growth of the generative AI market may be tempered by the readiness and capability of enterprises to handle these complexities. Small to mid-sized businesses, in particular, may find the cost-prohibitive nature of these technologies a major hurdle, thereby slowing market penetration and potentially widening the technology gap between large and smaller firms.

Ensuring Data Quality for Effective AI Deployment

The success of AI-driven solutions in the enterprise sector heavily relies on the quality and diversity of the datasets used to train these systems. High-quality, diverse data is essential for AI models to perform accurately and deliver reliable outputs. However, access to such data can be a significant constraint, particularly for industries where data may be fragmented, sensitive, or subject to stringent regulatory protections.

This issue not only affects the performance and reliability of AI applications but also restricts the scope of their deployment, particularly in critical areas such as healthcare, finance, and legal services. The lack of comprehensive, unbiased datasets can impede AI training processes, leading to models that are either ineffective or biased, which could potentially limit market growth and acceptance of generative AI technologies in sensitive sectors.

By Technology Analysis

Generative Adversarial Networks drive 30% growth in the Generative AI enterprise market, revolutionizing industry applications.

In 2023, Generative Adversarial Networks (GANs) held a dominant market position in the "Based on Technology" segment of the Generative AI in the Enterprise Market, capturing more than a 49.2% share. This prominence underscores the critical role GANs play in the broader ecosystem of AI technologies, which includes Deep Learning, Natural Language Processing (NLP), Cloud Computing, and other emerging technologies.

Generative Adversarial Networks are particularly valued for their ability to generate new, synthetic data instances that are virtually indistinguishable from real data. This capability is instrumental in various applications such as content generation, image processing, and more sophisticated simulation tasks, which are increasingly demanded across industries. The finance and healthcare sectors, for example, leverage GANs for fraud detection and drug discovery, respectively, highlighting the technology's versatility and broad market applicability.

Deep Learning, another significant technology in this segment, supports a variety of AI functions with its ability to process and learn from large data sets, thus enhancing the accuracy and efficiency of AI systems. NLP technologies facilitate human-computer interactions, and their integration into enterprise applications is expanding as businesses seek to improve customer experience and streamline operations.

Cloud Computing also plays a pivotal role by providing the necessary infrastructure and scalability for deploying these complex AI models, enabling enterprises to access AI tools and services efficiently and cost-effectively.

By Deployment Mode Analysis

Cloud deployment dominates, holding 58% of enterprise generative AI market adoption and scalability.

In 2023, Cloud held a dominant market position in the "Based on the Deployment Mode" segment of Generative AI in the Enterprise Market, capturing more than a 58% share. This significant market share underscores the pivotal role that cloud-based solutions play in facilitating the adoption and scalability of AI technologies across various industries.

The preference for cloud deployment can be attributed to several key advantages. Primarily, it offers enterprises the flexibility to scale their AI capabilities without the substantial upfront capital expenditure associated with on-premises installations. Furthermore, cloud environments provide seamless updates and maintenance of AI applications, ensuring that businesses can leverage the latest advancements without enduring downtime or additional costs.

The cloud's dominance is also driven by its capacity to democratize access to cutting-edge technologies. Small to medium-sized enterprises (SMEs), which may lack the resources to invest heavily in their own IT infrastructure, particularly benefit from cloud software. They can access sophisticated AI tools that were previously attainable only by large corporations, enabling them to compete more effectively in their respective markets.

On-premises deployment, while offering higher control over data and security, has seen slower growth due to its higher costs and complexity. However, certain sectors such as government and healthcare, where data sensitivity is paramount, continue to rely on on-premises solutions to meet stringent regulatory compliance standards.

By Application Analysis

Data augmentation applications lead, capturing 58% of the generative AI enterprise market segment.

In 2023, Data Augmentations held a dominant market position in the "Based on Application" segment of Generative AI in the Enterprise Market, capturing more than a 35% share. This substantial market share illustrates the critical importance of data augmentations in leveraging artificial intelligence to enhance the quality and effectiveness of data sets across various industries.

Data Augmentations primarily involve techniques used to expand or enhance data through methods that generate synthetic data or transform existing data. This capability is crucial for industries where large, comprehensive datasets are necessary but difficult to obtain due to constraints such as privacy issues, limited access to data, or the need for balanced datasets in training AI models. Industries such as healthcare, financial services, and automotive particularly benefit from these applications, using augmented data to improve predictive models and decision-making processes without compromising on data privacy and security.

The impact of Data augmentation extends beyond just enhancing data quality. It also enables more robust AI training processes and improved model accuracy, making AI deployments more effective and efficient. This is especially valuable in AI-driven fields like anomaly detection, risk management, and personalized customer experiences.

While Data Augmentations lead this application segment, other applications such as Content Generation, Design & Creativity, and Virtual Assistants & Chatbots also play significant roles. Content Generation, for instance, leverages generative AI to produce unique textual, visual, or audio content, whereas Design & Creativity uses AI to generate innovative design prototypes and creative materials.

Key Market Segments

Based on Technology

- Deep Learning

- Generative Adversarial Networks

- Natural Language Processing

- Cloud Computing

- Other Technologies

Based on the Deployment Mode

- Cloud

- On-premises

Based on Application

- Content Generation

- Design & Creativity

- Virtual Assistants & Chatbots

- Data Augmentations

- Other Applications

Growth Opportunity

Driving Innovation in Design and Creativity

The global generative AI market presents substantial opportunities for enterprises in 2023, particularly in enhancing creativity and design capabilities. AI-driven generative models are revolutionizing the creative sectors by assisting in complex tasks such as graphic design, generating innovative artwork, and formulating fresh ideas for product development. These capabilities enable businesses to drastically cut down on design time and explore new creative possibilities that were previously unattainable. Companies that harness these advanced tools can differentiate their products in the market, provide superior customer experiences, and maintain a competitive edge.

Enhancing Data Analysis and Decision-Making

Another significant opportunity for generative AI lies in its ability to process and analyze vast datasets to generate actionable insights. This aspect is particularly crucial as enterprises seek to leverage data-driven strategies to optimize operations and forecast market trends. By integrating generative AI technologies, companies can enhance their analytical capabilities, leading to more informed decision-making and innovative business strategies. The ability to quickly interpret complex data and provide strategic insights can significantly improve efficiency and effectiveness, driving business growth and sustainability.

Latest Trends

Revolutionizing Software Development: Code Generation, Documentation, and Quality Assurance

In 2023, one of the most impactful trends in the global generative AI market is its application in software development, specifically in code generation, documentation, and quality assurance. Generative AI technologies are becoming indispensable generative tools for developers, enabling them to write and complete sophisticated software codes more efficiently. These AI systems can also vet code for errors, handle bug fixes, automate test generation, and produce various types of technical documentation. This not only accelerates the development process but also enhances the quality and reliability of software products. Enterprises adopting these AI capabilities are likely to see significant improvements in productivity and a reduction in the time-to-market for new software solutions.

Enhancing Accuracy with Retrieval-Augmented Generation (RAG)

Another leading trend is the adoption of Retrieval-Augmented Generation (RAG). This advanced technique combines the capabilities of large language models (LLMs) with retrieval-augmented generation, enhancing the accuracy of generated outputs while minimizing errors known as "hallucinations." By integrating external information during the generation process, RAG enables LLMs to provide more precise and contextually relevant answers. This trend is particularly transformative for industries relying heavily on data accuracy and detail, such as legal, medical, and technical fields. As businesses increasingly rely on accurate and reliable data, RAG presents a compelling solution to improve the trustworthiness and utility of generative AI applications.

Regional Analysis

North America dominates 40% of the generative AI enterprise market, leading in adoption and innovation.

The enterprise market for generative AI is experiencing a dynamic expansion across various global regions, each displaying unique growth characteristics and adoption rates. North America is the dominant force, holding approximately 40% of the market. This leadership is attributed to robust technological infrastructure, significant investments in AI by major corporations, and a concentrated presence of pioneering AI firms. The U.S. leads in both the development and application of generative AI technologies, driving innovations primarily in sectors such as finance, healthcare, and retail.

In Europe, the market is driven by a strong emphasis on data privacy and ethical AI, supported by stringent regulations such as GDPR. Countries like Germany, the UK, and France are at the forefront, integrating AI into manufacturing and automotive industries. The European market is also witnessing a surge in AI startups, bolstered by favorable government policies and funding.

The Asia Pacific region is rapidly catching up, with China, Japan, and South Korea making significant advancements in AI technology. The region benefits from government backing in technology, a thriving tech startup ecosystem, and extensive manufacturing capabilities. AI adoption is particularly noticeable in consumer electronics, e-commerce, and automotive sectors.

Meanwhile, the Middle East & Africa, and Latin America are emerging as potential growth areas. The Middle East, with its strategic investments in smart cities and digital transformation, and Africa, with its untapped potential and increasing mobile penetration, are beginning to leverage AI for economic and social development. Latin America shows promise with its growing tech-savvy workforce and increasing digitalization across businesses, particularly in Brazil and Mexico.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the rapidly evolving landscape of generative AI in the enterprise market, key players are shaping the trajectory through strategic innovations and expansive ecosystems. As of 2024, OpenAI stands out with its trailblazing language models, which have set the standard for generative AI capabilities. Their offerings not only enhance business efficiency but also foster new avenues for user interaction and content creation, placing them at the forefront of AI-driven transformation.

NVIDIA Corp. is instrumental in providing the hardware backbone necessary for running sophisticated AI algorithms. Their advanced GPU technologies and AI platforms not only power other enterprises’ AI applications but also democratize AI accessibility, enabling faster and more efficient AI deployments across various sectors.

IBM Corp. leverages its long-standing expertise in enterprise IT solutions by integrating generative AI into its portfolio, focusing on sectors such as healthcare and finance where data sensitivity and security are paramount. IBM’s emphasis on trust and transparency in AI aligns with the growing demand for ethical AI solutions.

Microsoft Corp. and Google LLC are pivotal in shaping the generative AI landscape through comprehensive cloud and AI solutions that cater to a wide range of business needs. Microsoft’s Azure AI and Google Cloud AI services provide robust, scalable platforms that support enterprise AI initiatives, driving innovation and operational agility.

Amazon Web Services, Inc. and Salesforce, Inc. enhance their cloud offerings with generative AI capabilities, focusing on personalizing customer experiences and optimizing business processes, which are crucial for competitive differentiation in today’s digital marketplace.

Adobe Inc. transforms creative industries by integrating AI into its software suites, thus streamlining content creation and enabling new forms of artistic expression, thereby reshaping creative workflows.

Top Key Players in Generative AI in the Enterprise Market

- OpenAI

- NVIDIA Corp.

- IBM Corp.

- Microsoft Corp.

- Google LLC

- Amazon Web Services, Inc.

- Adobe Inc.

- Salesforce, Inc.

- Other Key Players

Recent Development

- In April 2024, Nvidia reported a significant surge in net income for fiscal year 2024, driven by the demand for AI technologies like those enhancing ERP systems with generative AI capabilities, which are poised to transform enterprise resource planning by enabling more intuitive interactions and predictive analytics.

- In April 2024, Kore.ai, an enterprise conversational and generative AI platform, appointed Paul Rilstone as its new vice president for Australia and New Zealand to drive regional growth and expand its presence in the GenAI market, following a US$150 million funding round aimed at supporting its international expansion.

- In April 2024, Generative AI (GenAI) is revolutionizing enterprise operations by transforming tacit knowledge into actionable insights, thus enabling businesses to drive innovation, enhance decision-making, and achieve significant competitive advantages, as detailed in the report by McKinsey & Company and S&P Global Market Intelligence.

- In March 2024, Investor interest in Hewlett Packard Enterprise was reinvigorated due to a significant backlog in orders for AI servers using Nvidia GPUs, prompting a reassessment of the stock's value amidst its broader corporate transformation and upcoming acquisition of Juniper Networks, as reported by Barron’s.

Report Scope

Report Features Description Forecast Revenue (2033) USD 52,492.7 Mn CAGR (2024-2033) 39.4% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology (Deep Learning, Generative Adversarial Networks, Natural Language Processing, Cloud Computing, and Others), By Deployment Mode (Cloud-Based and On-Premises), By Application(Content Generation, Design & Creativity, Virtual Assistants & Chatbots, Data Augmentations, Others) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape OpenAI, NVIDIA Corp., IBM Corp., Microsoft Corp., Google LLC, Amazon Web Services, Inc., Adobe Inc., Salesforce, Inc., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- OpenAI

- NVIDIA Corp.

- IBM Corp.

- Microsoft Corp.

- Google LLC

- Amazon Web Services, Inc.

- Adobe Inc.

- Salesforce, Inc.

- Other Key Players

Our Clients

View Our Licence Options