Generative AI in Defense Market By Component (Software, Services), By Deployment Mode (Cloud-based, On-premises), By Application (Target Recognition, Decision Support Systems, Others), By End-User, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2023-2032

-

37835

-

April 2024

-

137

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

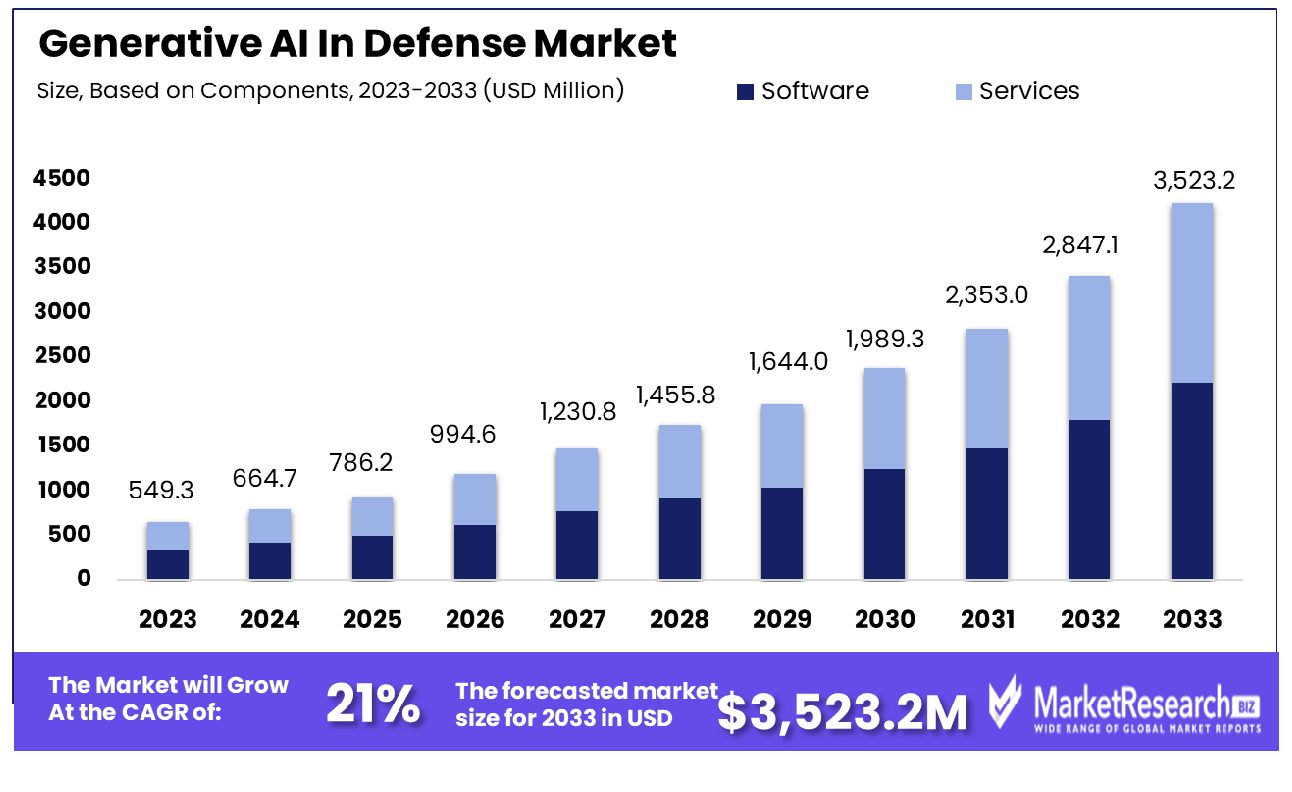

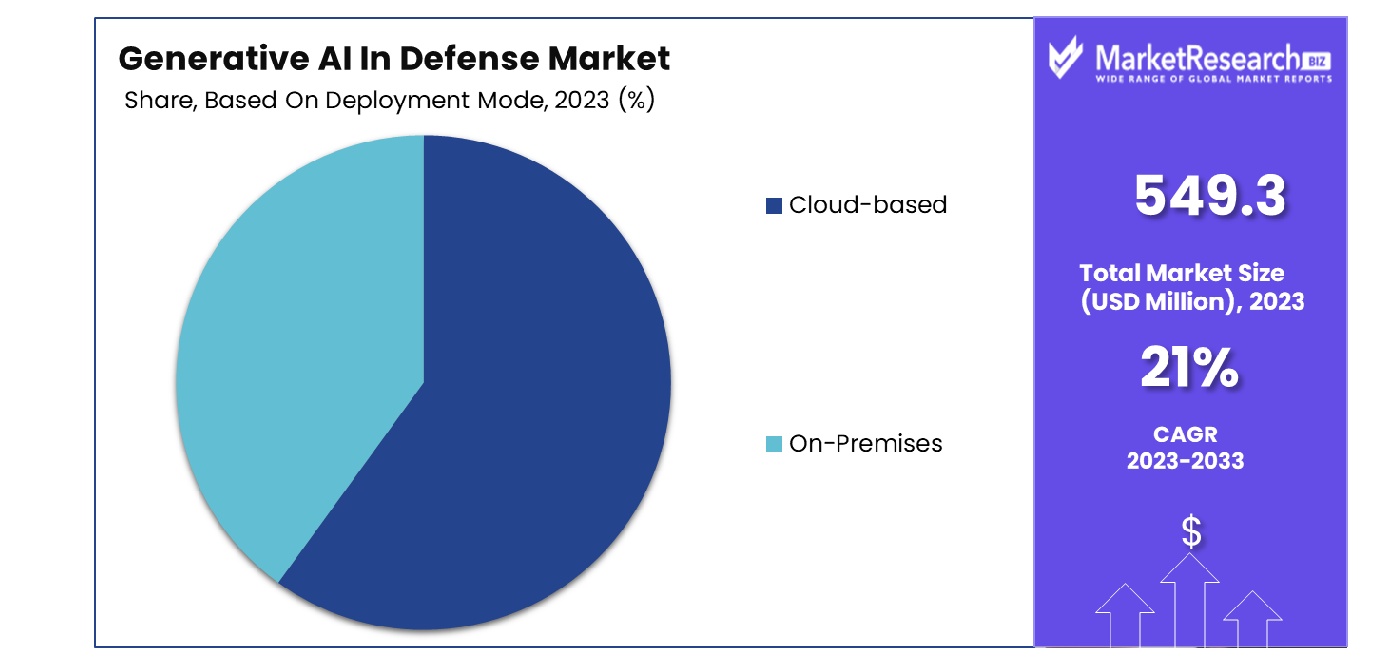

The Generative AI In Defense Market was valued at USD 549.3 Million in 2023. It is expected to reach USD 3,523.2 Million by 2033, with a CAGR of 21% during the forecast period from 2024 to 2033.

The surge in demand for new advanced technology and extensive use in the military sector are the main keys driving factors for the generative AI in defence market. The high-end usage of AI-based technology in the defense industry comprises different functions and chances like training, investigation, logistics, cybersecurity, and the latest military weaponry such as combat vehicles, automatic robots, and LAWS. Such types of applications make sure to enhance the defense sector in modern war tactics.

GenAI is one of the most important technological tools in modern times. Its combination with other related advanced technologies mainly the IoT and robotics has tremendous usage in the defence sector. The main capability of GenAI is present in all segments of defense such as cyberspace, and intelligence, and comprises political, tactical, and operational warfare. The defense sector mainly depends upon basic and highly confidential data on people, areas, monetary securities, nations, the cyber world, and many more.

This huge amount of information, when used will regulate the readiness of the defense sector to warfare. Analyzing and examining the industry’s willingness affects the whole process of military decision-making starting from the strategic operations, and force structure to monetary budgets. GenAI enables management and handling readiness by using the information extracted from different sources and enriches the industry by offering futuristic war systems that are primarily dominated by intelligent robots, data processing, intelligence assessment, information analyzing, training, and much more.

In the defense sector, GenAI and machine learning with geospatial analysis help in acquiring precious and confidential intelligence from different sources and connected tools such as radars, cyberspace, automatic identification systems, etc. The automated robots that are power-driven with AI and computer vision and integration with IoT have the potential to interpret visuals for target identifications and categorization. Governments that use AI in their defense mechanism get an edge in war situations with insights from intelligence and investigation.

According to a report published by the government of India in February 2023, stated that the Indian armed forces are ready to meet any war situation in the coming future. The union budget for FY2023 to 2024 predicts a total amount of sum of Rs 45,03,097 crore. Out of this, the Military Organizations of defence has also allotted a total budget of Rs 5,93,537.64 crore, which is 13.18 % of the total budget.

In 2022, the Russian defense military has said to use the GenAI-based drones in their recent war with Ukraine. Similarly, Ukraine utilized the power of GenAI to battle misinformation at the time of war with Russia. The demand for generative AI in defense market is important due to its high requirement for GenAI technology in defense sector that will help in market expansion in the coming years.

Key Takeaways

- Market Growth: The Generative AI In Defense Market was valued at USD 549.3 Million in 2023. It is expected to reach USD 3,523.2 Million by 2033, with a CAGR of 21% during the forecast period from 2024 to 2033.

- Based on Components: Software component ensures precision in operations, enhancing efficiency across various sectors.

- Based On Deployment Mode: Cloud-based deployment offers scalability, accessibility, and cost-effectiveness for diverse applications.

- Based on Application: Target recognition applications streamline identification processes, improving security and surveillance measures significantly.

- Based on End-Users: Government and military end-users benefit from advanced capabilities, ensuring national security.

- Regional Dominance: North America dominates 44% of the global Generative AI in Defense Market share.

- Growth Opportunity: Generative AI is revolutionizing the global defense market by developing innovative technologies and enhancing defense operations through predictive analytics, simulation, and automated systems, significantly improving strategic capabilities and operational efficiency.

Driving factors

Quantum Computing: Enhancing Security and Decision-Making Efficiency

Quantum computing holds transformative potential for Generative AI in Defense Market, primarily through its profound implications for encryption and security. The technology's ability to process complex calculations at unprecedented speeds is anticipated to revolutionize AI-driven defense systems, enabling the creation of ultra-secure communications and the decryption of previously impenetrable data.

This advancement is crucial in defense, where securing sensitive information and communication lines from adversarial interception is paramount. Moreover, quantum computing can significantly enhance the decision-making capabilities of AI in defense applications by analyzing vast datasets more efficiently than traditional computing methods. This increased computational power will facilitate the development of more sophisticated, autonomous defense systems, thereby driving market growth.

Ethical and Legal Concerns: Navigating the Complex Landscape

The integration of AI into defense mechanisms brings to the forefront a range of ethical and legal considerations that must be meticulously addressed. Concerns over the responsible use of autonomous systems in combat scenarios, including adherence to international humanitarian laws and the avoidance of unintended collateral damage, are paramount.

These ethical and legal challenges are not merely regulatory hurdles but also drive innovation and the development of AI systems that are not only capable but also compliant with global standards. As such, these considerations stimulate investment in research and development aimed at creating AI solutions that can navigate the complex moral and legal terrain of modern warfare, further propelling the market's growth.

Data Fusion and Analysis: Realizing Enhanced Situational Awareness

AI-driven data fusion and analysis tools are critical in harnessing the power of generative AI within the defense sector, offering unparalleled real-time situational awareness and decision-making capabilities. By integrating and analyzing data from diverse sources — including satellites, drones, sensors, and intelligence reports — AI systems can provide defense operatives with a comprehensive understanding of the battlefield. This capability is instrumental in making informed decisions swiftly, significantly reducing response times to threats and enhancing operational efficiency.

The ability to analyze and synthesize large volumes of data in real time not only improves strategic planning but also the execution of defense operations, thereby contributing significantly to market growth. Together, these factors demonstrate the vital role data fusion and analysis play in strengthening defense forces' strategic capabilities, driving demand for advanced AI solutions in this sector.

Restraining Factors

Regulatory and Compliance Issues: Navigating the Complex Framework

The deployment of Generative AI in the defense market is significantly influenced by regulatory and compliance issues, which present both challenges and catalysts for growth. These systems are subject to stringent regulations and standards designed to ensure their safe and ethical application. Compliance with these frameworks may prove to be challenging due to the fluid nature of AI technology and defense operations. However, this stringent regulatory environment also drives innovation and improvements in AI systems.

To meet these standards, organizations are compelled to invest in advanced research, development, and testing, ensuring that their AI solutions are not only effective but also compliant. This necessity for high compliance standards propels the market forward by fostering a competitive environment where only the most sophisticated and reliable AI technologies thrive. While the need to navigate regulatory complexities might initially seem like a restraint, it ultimately enhances the quality and reliability of AI applications in defense, contributing to market growth.

Ethical Concerns: The Imperative for Responsible AI Development

Ethical concerns regarding the use of generative AI in defense, particularly relating to autonomous weapons systems and potential misuse, represent a significant restraint. The fear of creating autonomous systems capable of making life-or-death decisions without human intervention has sparked a global debate on the moral implications of such technologies. These ethical challenges necessitate a cautious approach to the development and deployment of AI in defense contexts, emphasizing the need for systems that are not only technologically advanced but also ethically responsible.

The focus on ethical AI fosters a culture of transparency, accountability, and human oversight, which, in turn, can enhance trust in AI technologies among defense entities and the public. Although these ethical considerations may slow down the pace of adoption, they also drive the development of more sophisticated, ethically conscious AI solutions. By ensuring that generative AI systems in defense are developed with a strong ethical foundation, the market is positioned to grow in a manner that is sustainable and aligned with societal values, ultimately contributing to the long-term viability of AI technologies in defense applications.

Based on components

Based on components, software dominates with its extensive capabilities in data processing and algorithm optimization.

In 2023, software emerged as a pivotal component in the Generative AI in Defense market, asserting a dominant position within the "Based on Components" segment, which also encompasses services. This ascendancy can be attributed to the software's integral role in facilitating advanced AI capabilities, such as predictive analytics, threat simulation, and autonomous decision-making processes. The utilization of generative AI software in defense mechanisms significantly enhances operational efficiency, strategic planning, and security measures, thereby driving the segment's growth.

The market's inclination towards software solutions is further reinforced by continuous innovations and the development of bespoke AI models tailored to specific defense applications. These advancements enable more accurate data analysis, simulation of complex scenarios, and the generation of predictive insights, which are crucial for national security and defense strategy formulation. Consequently, the demand for such software solutions has seen a notable increase, underscored by their capability to provide a competitive edge through technological superiority.

Moreover, the services segment, complementing the software, contributes to the market's dynamics by offering expert implementation, maintenance, and training services. These services ensure that defense organizations can maximize the potential of generative AI technologies, thereby fostering a symbiotic relationship between the software and service components.

Integrating these segments underscores a comprehensive approach to adopting generative AI in defense applications, underlining both innovative software solutions and professional services' key role in realizing AI's full potential in defense applications.

Based On Deployment Mode

In deployment mode, cloud-based solutions offer unparalleled scalability and accessibility, facilitating real-time data analysis.

In 2023, cloud-based solutions held a dominant market position in the "Based on Deployment Mode" segment of the Generative AI in Defense Market, juxtaposed with on-premises solutions. This prominence is attributed to the cloud-based deployment model's unparalleled scalability, flexibility, and cost-efficiency, which are critical in managing the voluminous data and compute-intensive tasks characteristic of generative AI applications in defense.

Cloud-based generative AI solutions in the defense sector allow organizations to leverage the advanced computational power and storage capacity required for training complex AI models. These models are instrumental in simulating complex security scenarios, enhancing situational awareness, and facilitating rapid decision-making processes. The cloud's agility in deploying and updating AI functionalities aligns with the dynamic nature of defense needs, ensuring that defense entities remain at the forefront of technological advancements.

Furthermore, cloud-based AI platform models offer significant cost advantages by eliminating the need for substantial upfront investments in hardware and infrastructure, which is often a limiting factor for on-premises deployment. The pay-as-you-go model inherent in cloud services allows defense organizations to optimize their budgets, focusing resources on innovation and strategic initiatives.

Despite the advantages, the choice between cloud-based and on-premises deployment continues to be influenced by considerations of data security and operational control. However, the evolving landscape of cybersecurity measures in cloud services, coupled with regulatory compliance and data sovereignty solutions, progressively mitigates these concerns.

Based on Application

Regarding application, target recognition technology advances significantly, enhancing precision in both civilian and military operations.

In 2023, Target Recognition emerged as the leading application within the "Based on Application" segment of the Generative AI in Defense Market, amid other critical applications such as Decision Support Systems, Autonomous Systems, Cybersecurity, and Other Applications. This dominance is primarily attributed to the escalating need for precision and efficiency in identifying and neutralizing threats, a requirement that generative AI excels in addressing through advanced pattern recognition and data analysis capabilities.

The application of generative AI in target recognition encompasses the use of sophisticated algorithms capable of analyzing vast datasets to identify potential threats accurately. This capability is pivotal in modern defense strategies, where the rapid and accurate identification of targets can significantly enhance operational effectiveness and ensure national security. Generative AI technologies facilitate the processing of real-time data from various sources, including satellites, drones, and ground sensors, thereby enabling defense forces to make informed decisions swiftly.

Moreover, the integration of generative AI into target recognition systems has been instrumental in automating surveillance and reconnaissance tasks, reducing the reliance on human intervention and minimizing the margin of error. This automation not only increases the speed and accuracy of target identification but also enhances the safety of military personnel by reducing their exposure to hazardous environments.

While Target Recognition holds the dominant position, the importance of other applications like Decision Support Systems, Autonomous Systems, and Cybersecurity continues to grow. These applications collectively contribute to the development of an integrated defense ecosystem where generative AI plays a central role in augmenting defense capabilities across multiple fronts.

Based on End-Users

Among end-users, government and military sectors prioritize these technologies for security and strategic superiority.

In 2023, the Government/Military segment held a dominant market position in the "Based on End-Users" segment of the Generative AI in Defense Market, alongside other key stakeholders such as Defense Contractors and Research Institutions. This preeminence is primarily attributed to the substantial investments and strategic initiatives undertaken by governmental and military bodies worldwide, aimed at integrating generative AI technologies into their defense mechanisms.

The government and military sectors have recognized the transformative potential of generative AI in revolutionizing defense strategies, enhancing operational capabilities, and ensuring national security. The application of generative AI in these sectors spans across various dimensions, including but not limited to, autonomous systems, cybersecurity, target recognition, and decision support systems. These applications facilitate the processing and analysis of complex datasets, enabling the prediction and neutralization of threats with unprecedented accuracy and efficiency.

Moreover, the government and military's commitment to adopting generative AI is further evidenced by the increasing allocation of budgets towards research and development in AI technologies, collaborative projects with defense contractors, and partnerships with research institutions. These efforts are aimed at fostering innovation and developing cutting-edge AI solutions tailored to defense requirements.

While the Government/Military segment remains at the forefront, Defense Contractors and Research Institutions also play pivotal roles in the ecosystem. Defense Contractors are instrumental in translating AI research into practical solutions, whereas Research Institutions contribute through foundational research and innovation.

Key Market Segments

Based on components

- Software

- Services

Based On Deployment Mode

- Cloud-based

- On-Premises

Based on Application

- Target recognition

- Decision Support Systems

- Autonomous Systems

- Cybersecurity

- Other Applications

Based on End-Users

- Government/Military

- Defense Contractors

- Research Institutions

Growth Opportunity

Development of Innovative Defense Technologies

Defense sector transformation is underway globally as Artificial Intelligence (AI), specifically Generative AI, becomes a central factor in developing innovative defense technologies. The capabilities of generative AI to simulate, predict, and automate complex tasks have opened new vistas for military applications, including but not limited to, cyber defense mechanisms, simulation of tactical scenarios, and the autonomous operation of unmanned systems.

The adoption of these technologies can be seen as a strategic endeavor to enhance operational efficiency, decision-making speed, and the precision of defense mechanisms. It is evident that the exploration of generative AI in developing innovative defense technologies not only promises a significant enhancement in strategic capabilities but also paves the way for a new era in warfare technology.

Integration of Generative AI in Defense Operations

The integration of generative AI into defense operations marks a revolutionary step in military strategy and operations. This technology's inherent ability to process and analyze vast amounts of data in real time enables the generation of predictive analytics, which can be crucial for tactical planning and threat assessment. Furthermore, generative AI's role in creating realistic training simulations enhances the preparedness and response capabilities of military personnel, ensuring they are better equipped to face contemporary challenges.

The application of generative AI in logistics and supply chain management within the defense sector also signifies substantial improvements in efficiency and cost-effectiveness. Consequently, the comprehensive integration of generative AI across various facets of defense operations not only augments operational capabilities but also significantly contributes to the strategic superiority and security resilience of nations.

Latest Trends

Biometrics and Identity Verification

In 2023, the global defense market has witnessed a remarkable surge in the adoption of generative AI for biometrics and identity verification. The integration of AI-based biometric technologies is revolutionizing secure access control and personnel authentication processes. These advanced systems, leveraging facial recognition, iris scans, and fingerprint analysis, offer unparalleled accuracy and security.

The implementation of such technologies ensures the safeguarding of sensitive military installations and information, thereby significantly enhancing national security measures. Moreover, generative AI's capability to continuously learn and adapt to new security threats positions biometrics as a critical component in the defense sector's evolving security architecture.

AI-Powered Weapons Systems

The advent of AI-powered weapons systems represents a transformative trend in the global defense industry. 2023 has seen a substantial advancement in the development of autonomous combat vehicles and AI-assisted targeting systems, marking a new era in military capabilities. These systems, characterized by their precision, rapid response times, and ability to operate in complex environments, offer strategic advantages previously unattainable.

The utilization of generative AI in weapons systems not only enhances operational effectiveness but also redefines the parameters of engagement, emphasizing the importance of technological superiority in modern warfare. This trend towards AI-powered military technology underscores a significant shift towards automation and smart weaponry, setting new standards for efficiency and combat readiness in the defense sector.

Regional Analysis

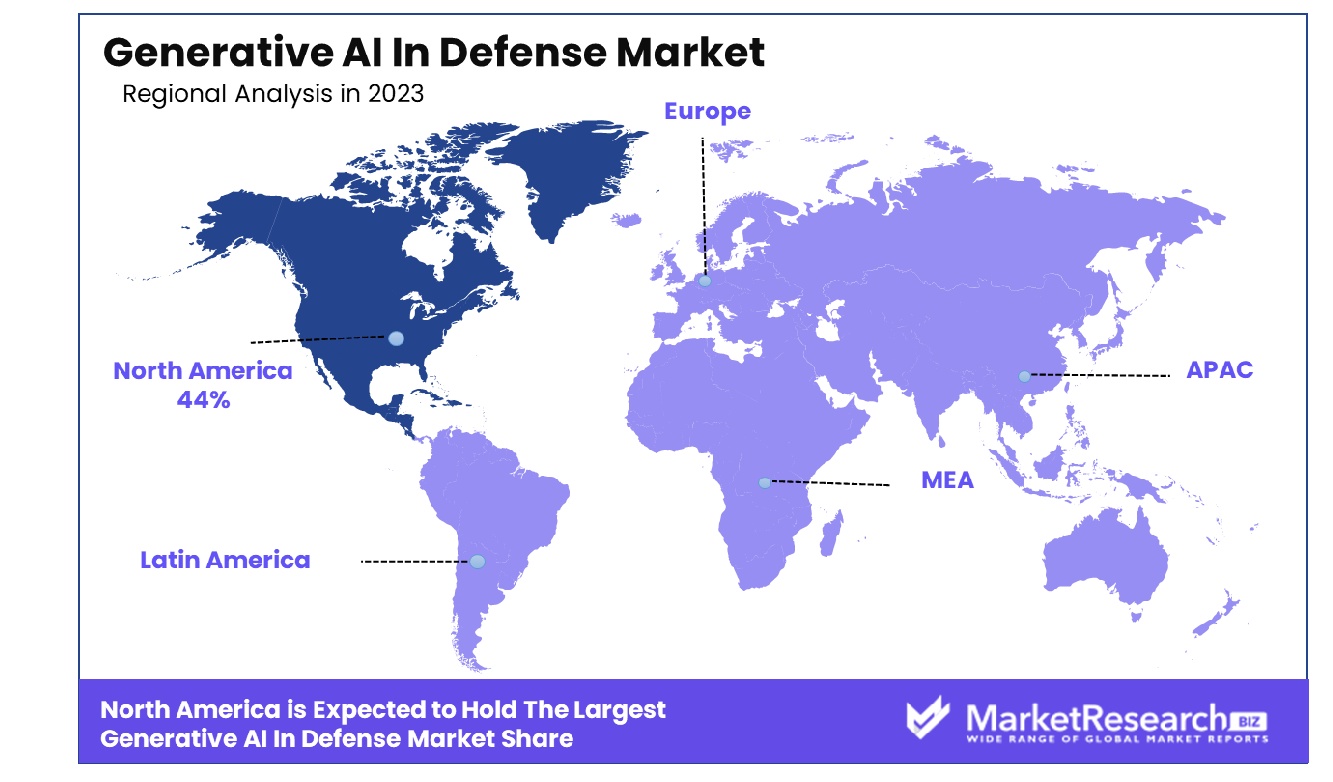

North America dominates the Generative AI in Defense Market with a substantial 44% market share.

The integration of Generative AI in the defense sector marks a pivotal evolution across various regions, reflecting diverse technological adoption rates, strategic priorities, and investment landscapes. North America emerges as the dominant player, accounting for 44% of the global market. This can be attributed to substantial investments in defense innovation, a robust technological infrastructure, and the presence of leading AI firms collaborating with defense agencies to develop advanced military solutions.

In Europe, the market is characterized by a strong emphasis on enhancing defense capabilities through innovation and collaboration among EU member states. Initiatives aimed at integrating AI in defense mechanisms are receiving significant funding, underscoring Europe's strategic focus on technological sovereignty and security.

The Asia Pacific region exhibits rapid growth, driven by escalating defense budgets and a keen focus on adopting next-generation technologies. Countries like China, South Korea, and India are spearheading AI development, leveraging generative AI for cybersecurity, autonomous systems, and simulation-based training, thus bolstering their defense capabilities.

The Middle East & Africa region is witnessing an increasing incorporation of AI technologies in defense, primarily to enhance surveillance, intelligence operations, and unmanned systems. Investments in AI research centers and partnerships with tech companies are instrumental in this growth, despite challenges related to technological infrastructure and expertise.

Latin America, while still in the nascent stages of generative AI adoption in defense, shows potential for growth. Efforts are being made to modernize military capabilities and incorporate AI, albeit at a slower pace compared to other regions, due to budgetary constraints and focus on other immediate concerns.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In the rapidly evolving landscape of the Generative AI in Defense Market, several key players are at the forefront of innovation, shaping the future of military technologies and strategic capabilities globally. IBM Corporation, with its extensive research and development in AI, is pioneering solutions that enhance cybersecurity and cognitive warfare, positioning itself as a critical enabler of smarter defense mechanisms. Lockheed Martin Corporation leverages generative AI to revolutionize design processes, predictive maintenance, and simulation training, ensuring superior operational readiness and efficiency.

BAE Systems plc stands out for its commitment to integrating AI in national security and defense, with a focus on ethical AI deployment and advanced analytics to support military operations. Northrop Grumman Corporation, known for its cutting-edge aerospace and defense technologies, is actively incorporating AI to bolster its autonomous systems and cyber defense capabilities, demonstrating a forward-thinking approach to warfare.

Raytheon Technologies Corporation, through its expertise in missiles and air defense systems, is utilizing AI to enhance decision-making processes and situational awareness, thereby reinforcing its position as a leader in defense innovation. General Dynamics Corporation’s focus on AI-driven communication systems and cybersecurity solutions is pivotal in ensuring secure and efficient military operations.

Thales Group, with its global footprint, is pioneering AI applications in defense to enhance operational effectiveness and safety, particularly in critical systems and digital security. Leidos Holdings, Inc., excels in leveraging AI for intelligence analysis, reconnaissance, and surveillance, highlighting the strategic importance of data in modern warfare.

The collective efforts of these key players, along with other significant participants in the market, underscore a strategic shift towards AI-driven defense solutions. Their contributions not only enhance national and global security but also set the pace for innovation and ethical considerations in the deployment of generative AI in defense, marking a transformative era in military capabilities.

Market Key Players

- IBM Corporation

- Lockheed Martin Corporation

- BAE System plc.

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- General Dynamics Corporation

- Thales Group

- Leidos Holdings, Inc.

- Other Key Players

Recent Development

- In April 2024, Dell Technologies emphasizes responsible GenAI adoption in Ireland, addressing security risks. They advocate robust security measures, continuous monitoring, and flexibility in data privacy and ethics, promoting optimism in AI-cybersecurity synergy.

- In April 2024, Denodo partnered with Google Cloud, integrating Denodo Platform with Vertex AI for innovative data virtualization and generative AI solutions. Enables transformative insights across industries, fostering ethical considerations.

- In March 2024, Deloitte's report highlights government agility through tech adoption, focusing on 10x performance gains. Generative AI and efficient processes drive service improvements. Recommendations include breaking silos and leveraging data for faster response times.

Report Scope

Report Features Description Market Value (2023) USD 549.3 Million Forecast Revenue (2033) USD 3,523.2 Million CAGR (2024-2032) 21% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered Based on components(Software, Services), Based On Deployment Mode(Cloud-based, On-Premises), Based on Application(Target recognition, Decision Support Systems, Autonomous Systems, Cybersecurity, Other Applications), Based on End Users(Government/Military, Defense Contractors, Research Institutions) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape IBM Corporation, Lockheed Martin Corporation, BAE System plc., Northrop Grumman Corporation, Raytheon Technologies Corporation, General Dynamics Corporation, Thales Group, Leidos Holdings, Inc., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- IBM Corporation

- Lockheed Martin Corporation

- BAE System plc.

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- General Dynamics Corporation

- Thales Group

- Leidos Holdings, Inc.

- Other Key Players

Our Clients

View Our Licence Options