Generative AI Market By Component (Services, Software), By Technology (Generative Adversarial Networks (GANs), Transformer, Diffusion Networks), By End-User (Media & Entertainment, BFSI, IT & Telecommunication, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

38301

-

Aug 2024

-

137

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

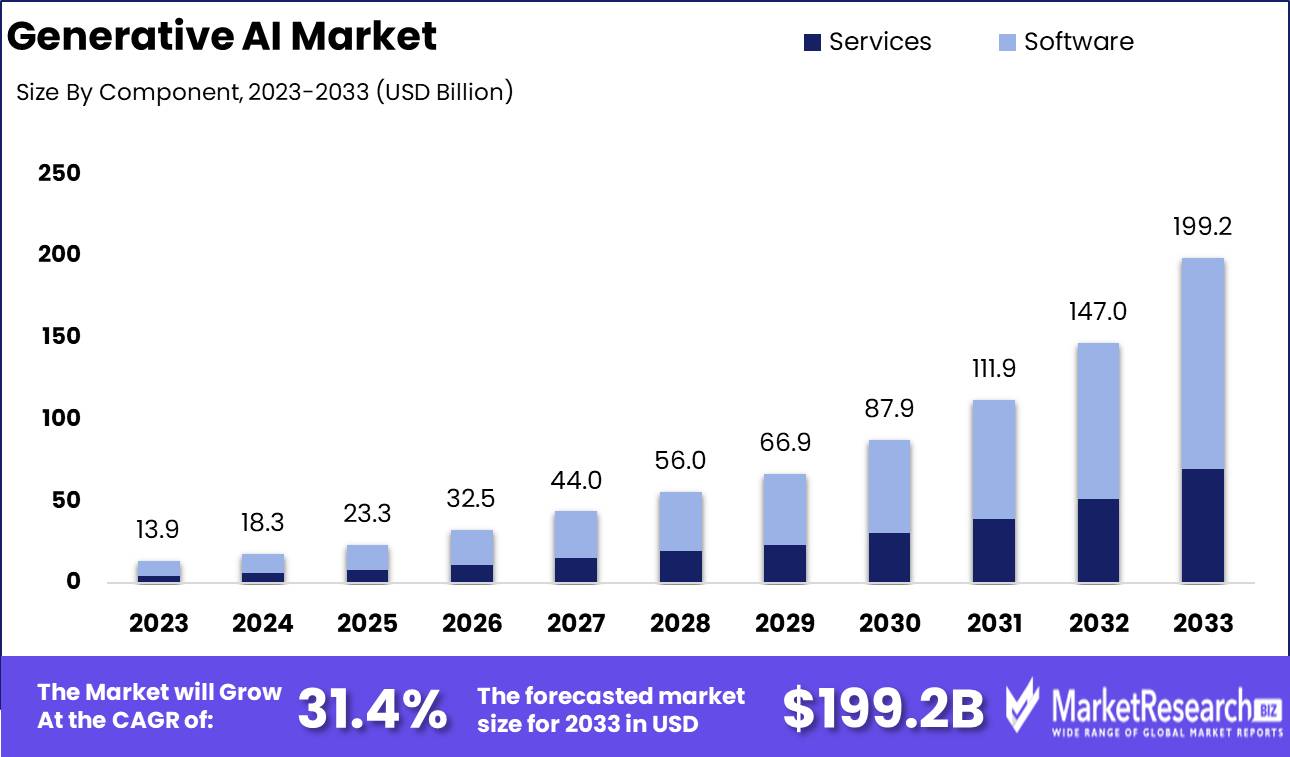

The Global Generative AI Market was valued at USD 13.9 Bn in 2023. It is expected to reach USD 199.2 Bn by 2033, with a CAGR of 31.4% during the forecast period from 2024 to 2033.

The Generative AI Market encompasses technologies that leverage artificial intelligence to create new content, designs, and solutions autonomously. This includes applications across various industries such as healthcare, pharmaceuticals, media, and entertainment, where AI models generate text, images, music, and molecular structures. The market is propelled by advancements in deep learning algorithms, increasing computational power, and growing demand for automation and innovation.

The Generative AI Market is experiencing transformative growth, driven by technological advancements and the increasing need for innovative and efficient solutions across various industries. Generative AI, with its capability to autonomously create new content and solutions, is redefining traditional workflows and opening new avenues for creativity and productivity. In the healthcare sector, AI-driven documentation tools have proven to be highly effective, saving physicians up to 2 hours per day and improving documentation accuracy by 35%. This not only enhances operational efficiency but also allows healthcare professionals to focus more on patient care, ultimately improving healthcare outcomes.

The Generative AI Market is experiencing transformative growth, driven by technological advancements and the increasing need for innovative and efficient solutions across various industries. Generative AI, with its capability to autonomously create new content and solutions, is redefining traditional workflows and opening new avenues for creativity and productivity. In the healthcare sector, AI-driven documentation tools have proven to be highly effective, saving physicians up to 2 hours per day and improving documentation accuracy by 35%. This not only enhances operational efficiency but also allows healthcare professionals to focus more on patient care, ultimately improving healthcare outcomes.A notable example in the pharmaceutical industry is Insilico Medicine's use of generative AI to accelerate drug discovery. Their AI model generated over 6,000 potential molecules, leading to the identification of ISM6331, a promising treatment for advanced solid tumors. This exemplifies the profound impact of generative AI on speeding up the drug development process and reducing associated costs. Such advancements demonstrate the potential of generative AI to revolutionize research and development, enabling faster and more accurate discovery of therapeutic solutions.

The market is also witnessing significant interest from the media and entertainment sectors, where AI-generated content is enhancing creativity and efficiency. Companies are leveraging AI to produce high-quality graphics, music, and scripts, thus reducing production time and costs. As generative AI continues to evolve, it is expected to drive substantial value creation across multiple industries by enhancing innovation, reducing time-to-market, and improving overall productivity. Key market players are likely to focus on further refining AI algorithms and expanding their application areas, ensuring sustained growth and adoption of generative AI technologies.

Key Takeaways

- Market Value: The Global Generative AI Market was valued at USD 13.9 Bn in 2023. It is expected to reach USD 199.2 Bn by 2033, with a CAGR of 31.4% during the forecast period from 2024 to 2033.

- By Component: Software dominates, representing 65% of the market, essential for developing and deploying AI models.

- By Technology: Generative Adversarial Networks (GANs) constitute 40%, crucial for creating realistic data simulations and enhancements.

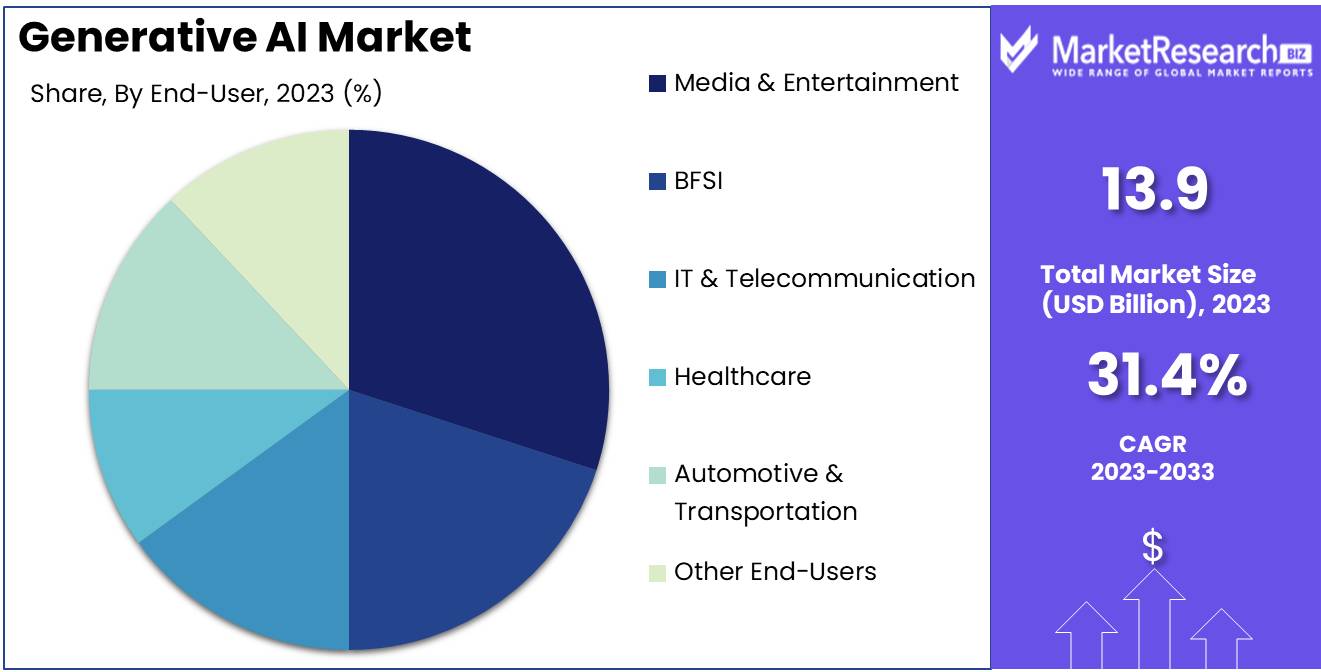

- By End-User: Media & Entertainment utilizes 30%, leveraging AI for content creation and enhancement.

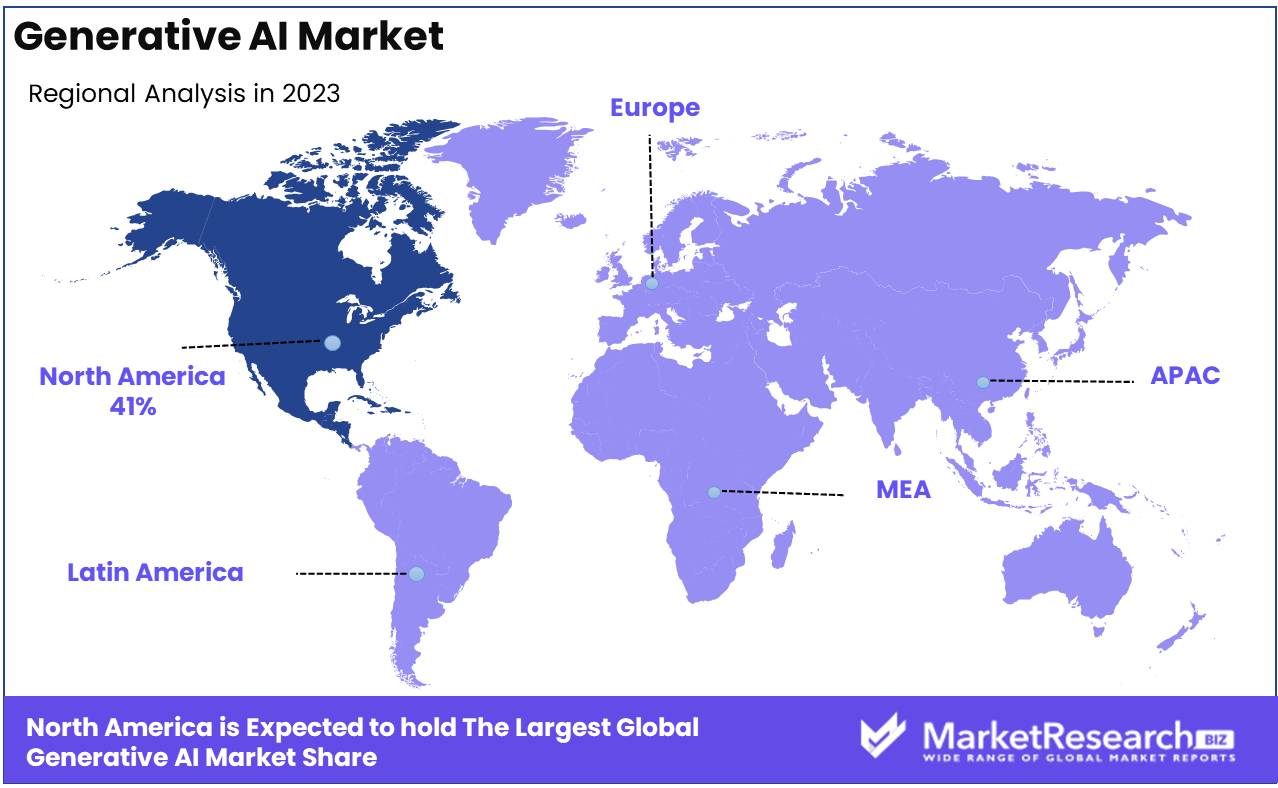

- Regional Dominance: North America holds a 41% market share, driven by high innovation rates and advanced technological infrastructure.

- Growth Opportunity: Expanding AI applications into new sectors like healthcare and finance can drive significant growth in the generative AI market.

Driving factors

Advancements in AI and Deep Learning Technologies

The advancements in AI and deep learning technologies are pivotal in driving the growth of the generative AI market. Cutting-edge algorithms and neural networks have significantly enhanced the capabilities of generative AI, enabling machines to create complex content autonomously.

These technological breakthroughs have broadened the scope of applications for generative AI, from natural language processing and image synthesis to advanced data analytics and predictive modeling. As AI and deep learning continue to evolve, they enhance the performance, reliability, and versatility of generative AI solutions, thereby accelerating their adoption across various industries.

Increasing Demand for Automation and Efficiency

The growing demand for automation and efficiency is another crucial factor contributing to the expansion of the generative AI market. Businesses across sectors are increasingly seeking ways to streamline operations, reduce costs, and improve productivity. Generative AI provides a powerful tool for achieving these goals by automating complex tasks such as data analysis, content creation, and customer interactions.

By implementing generative AI solutions, organizations can enhance operational efficiency, free up human resources for higher-value activities, and achieve greater accuracy and consistency in their processes. This drive for automation not only fuels market growth but also stimulates continuous innovation and improvement in generative AI technologies.

Growth in Personalized Content Creation

The surge in personalized content creation is a significant driver of growth for the generative AI market. In an era where consumers increasingly expect tailored experiences, generative AI offers the ability to produce customized content at scale. This includes personalized marketing materials, individualized customer support interactions, and bespoke product recommendations.

The capability of generative AI to analyze user data and generate content that aligns with individual preferences enhances customer engagement and satisfaction. As businesses strive to meet these rising expectations, the demand for generative AI solutions in content creation is set to grow, further propelling market expansion.

Restraining Factors

High Computational Costs

The high computational costs associated with generative AI pose a significant restraint on market growth. Developing and deploying generative AI models require substantial computational resources, which translate into increased operational expenses. These costs can be prohibitive for smaller organizations or startups, limiting their ability to adopt and integrate generative AI solutions.

The ongoing expenses related to maintaining and scaling these systems can deter potential users from investing in generative AI technology. Consequently, the market growth is somewhat constrained as only well-funded enterprises can afford the high costs associated with advanced AI computations.

Ethical Concerns and Intellectual Property Issues

Ethical concerns and intellectual property (IP) issues present another substantial challenge to the generative AI market. The ability of generative AI to create content that is indistinguishable from human-generated content raises significant ethical questions, including the potential for misuse in generating deepfakes, spreading misinformation, or infringing on privacy.

The ownership of content generated by AI models can lead to complex IP disputes, as it is often unclear who holds the rights to AI-generated works. These ethical and legal challenges can create a cautious approach among businesses and regulators, potentially slowing down the adoption and development of generative AI technologies.

By Component Analysis

Software held a dominant market position in the By Component segment of the Generative AI Market, capturing more than a 65% share.

In 2023, Software held a dominant market position in the By Component segment of the Generative AI Market, capturing more than a 65% share. This dominance is driven by the rapid development and deployment of generative AI software solutions across various industries. These software solutions are critical for creating, training, and deploying generative AI models, enabling businesses to harness the power of AI for diverse applications such as content creation, data augmentation, and predictive analytics. The scalability, flexibility, and continuous updates offered by generative AI software make it a preferred choice for organizations looking to integrate AI into their operations.

Services associated with generative AI, such as consulting, implementation, and support, also play a significant role. However, their market share is smaller compared to software due to the high reliance on robust and versatile software platforms to drive AI functionalities. As the market matures, the demand for specialized services is expected to grow, but currently, software remains the primary driver of the generative AI market.

By Technology Analysis

Generative Adversarial Networks (GANs) held a dominant market position in the By Technology segment of the Generative AI Market, capturing more than a 40% share.

In 2023, Generative Adversarial Networks (GANs) held a dominant market position in the By Technology segment of the Generative AI Market, capturing more than a 40% share. GANs are widely recognized for their ability to generate high-quality, realistic data, which is invaluable in applications such as image and video synthesis, data augmentation, and even generating synthetic datasets for training other AI models. The innovative architecture of GANs, which involves two neural networks contesting with each other, has proven highly effective in producing superior generative outcomes, driving their popularity and adoption.

Transformers and Variational Auto-encoders (VAEs) are also significant technologies within the generative AI landscape. Transformers, known for their effectiveness in natural language processing and understanding, are gaining traction but currently hold a smaller share compared to GANs. VAEs, which are valuable for their ability to learn efficient data representations, contribute to the market but are less prominent due to their more specialized applications.

Diffusion Networks and other emerging generative AI technologies are gaining attention for their unique capabilities and potential applications. While their market share is currently smaller, ongoing research and development are expected to enhance their adoption in the future.

By End-User Analysis

Media & Entertainment held a dominant market position in the By End-User segment of the Generative AI Market, capturing more than a 30% share.

In 2023, Media & Entertainment held a dominant market position in the By End-User segment of the Generative AI Market, capturing more than a 30% share. The media and entertainment industry leverages generative AI for a wide range of applications, including content creation, special effects, video game development, and personalized media experiences. The ability of generative AI to produce high-quality visual and audio content, automate editing processes, and enhance user engagement makes it highly valuable in this sector.

The BFSI (Banking, Financial Services, and Insurance) sector is also a significant adopter of generative AI, using it for fraud detection, risk management, and customer service automation. However, its market share is smaller compared to media and entertainment due to the more specialized nature of its applications.

IT & Telecommunication sectors utilize generative AI for network optimization, predictive maintenance, and customer experience enhancement. The market share in this sector is growing as companies increasingly adopt AI to improve operational efficiencies and service delivery.

Healthcare leverages generative AI for medical imaging, drug discovery services, and personalized treatment plans. The potential to revolutionize healthcare practices with AI-driven insights is significant, although the market share is currently less than that of media and entertainment.

Automotive & Transportation industries use generative AI for design optimization, autonomous driving, and predictive maintenance. The adoption of generative AI in these sectors is driven by the need for innovation and efficiency, but their market share remains smaller.

Other End-Users, including manufacturing, retail, and education, also benefit from generative AI applications tailored to their specific needs, contributing to the overall growth of the market.

Key Market Segments

By Component

- Services

- Software

By Technology

- Generative Adversarial Networks (GANs)

- Transformer

- Variational Auto-encoder (VAE)

- Diffusion Networks

By End-User

- Media & Entertainment

- BFSI

- IT & Telecommunication

- Healthcare

- Automotive & Transportation

- Other End-Users

Growth Opportunity

Development of Industry-Specific Generative AI Solutions

The development of industry-specific generative AI solutions represents a significant opportunity for market growth in 2024. Tailoring generative AI to meet the unique needs and challenges of different industries allows for more effective and specialized applications. For instance, in healthcare, generative AI can assist in creating synthetic medical data for research, while in finance, it can generate predictive models for market analysis.

This targeted approach enhances the relevance and value of generative AI solutions, driving adoption across various sectors. By focusing on industry-specific needs, AI developers can create more efficient, reliable, and impactful tools, thereby expanding the market and fostering innovation.

Expansion in Creative Industries like Art and Entertainment

The expansion of generative AI in creative industries, such as art and entertainment, offers substantial growth opportunities. Generative AI's ability to create music, art, scripts, and even entire virtual worlds is transforming how content is produced and consumed. In the entertainment industry, AI-generated content can streamline production processes, reduce costs, and enable new forms of creative expression.

Artists and creators are leveraging AI to push the boundaries of traditional art forms, exploring new aesthetic possibilities and enhancing productivity. This fusion of technology and creativity not only attracts a diverse audience but also drives investment in AI tools tailored for creative applications, significantly contributing to market growth.

Latest Trends

Use of Generative AI for Automated Content Creation

One of the key trends driving the generative AI market in 2024 is the use of AI for automated content creation. Businesses are increasingly leveraging generative AI to produce a wide array of content, from marketing materials and social media posts to news articles and technical documentation. This automation significantly reduces the time and cost associated with content production, allowing organizations to scale their output without compromising quality.

AI's ability to generate personalized content tailored to specific audiences enhances engagement and effectiveness. As demand for high-volume, high-quality content continues to grow, the adoption of generative AI for automated content creation is set to expand, driving market growth.

Integration with AR/VR for Immersive Experiences

The integration of generative AI with augmented reality (AR) and virtual reality (VR) is another transformative trend shaping the market in 2024. Combining AI with AR/VR technologies creates immersive, interactive experiences that are revolutionizing industries such as gaming, entertainment, education, and retail. Generative AI can produce realistic virtual environments, characters, and scenarios, enhancing the depth and realism of AR/VR experiences.

In gaming, AI can generate dynamic content and adaptive storylines, while in retail, it can create personalized virtual shopping experiences. This synergy between AI and AR/VR not only attracts a broad user base but also drives innovation and investment in immersive technologies.

Regional Analysis

North America held a dominant market position in the Generative AI Market, capturing more than a 41% share.

The North America region dominated the Generative AI Market in 2023, capturing more than a 41% share. This dominance is driven by the region's advanced technological infrastructure, high adoption rates of AI technologies, and significant investments in research and development. The U.S. is a major contributor, with numerous tech companies and startups leading the development of innovative generative AI applications. The increasing demand for AI-driven solutions across various industries, including healthcare, finance, and marketing, further drives market growth.

Europe follows closely, with a strong focus on AI research and development. Countries like Germany, the UK, and France are investing heavily in AI technologies to enhance their competitive edge. The market growth in Europe is supported by government initiatives and public-private partnerships aimed at fostering AI innovation.

The Asia Pacific region is experiencing rapid growth in the generative AI market, driven by significant investments in AI research and development. Countries like China, Japan, and India are leading the adoption of generative AI technologies across various sectors. The rising number of AI startups and the increasing integration of AI in business processes contribute to market growth in the region.

In the Middle East & Africa, the generative AI market is emerging, with growing interest in AI technologies. Countries in the Middle East, such as the UAE and Saudi Arabia, are making significant investments in AI to drive economic growth and innovation. The market growth is supported by government initiatives aimed at building robust AI ecosystems.

Latin America is steadily adopting generative AI technologies, with countries like Brazil and Mexico leading the market. The increasing digitalization and the growing demand for AI-driven solutions across various industries are driving market growth in the region.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

IBM leads in AI innovation with its Watson platform, offering comprehensive generative AI solutions across various industries. Its robust AI infrastructure ensures IBM's prominent position in the market.

Google’s extensive AI research and development, particularly through DeepMind and Google AI, positions it as a frontrunner in generative AI. Its advancements in AI technology significantly impact the market.

Microsoft leverages its Azure cloud platform and AI services to deliver scalable generative AI solutions. Its integration of AI across products like Microsoft 365 further strengthens its market presence.

Intel's AI hardware accelerates the performance of generative AI applications. Its innovations in processors and AI software contribute to the market's growth and development.

AWS provides robust cloud-based AI services, facilitating the deployment and scalability of generative AI solutions. Its comprehensive AI tools position it as a key market player.

NVIDIA’s GPUs are essential for training and deploying generative AI models. Its hardware accelerates AI processing, making it a critical player in the generative AI market.

OpenAI’s breakthroughs in generative models, such as GPT-3, drive significant advancements in the AI field. Its research and development efforts position it at the forefront of generative AI innovation.

Companies like Alphabet Inc., Salesforce.com, Inc., and Adobe Inc. also contribute significantly to the generative AI market. Their diverse AI solutions and continuous innovation drive the market's evolution and expansion.

Market Key Players

- IBM Corporation

- Google LLC

- Microsoft Corporation

- Intel Corporation

- Amazon Web Services, Inc.

- NVIDIA Corporation

- OpenAI

- Alphabet Inc.

- Salesforce.com, Inc.

- Adobe Inc.

- Other Key Players

Recent Development

- In April 2024, Microsoft Corporation launched an AI-powered creative suite that utilizes generative algorithms for content creation. This suite is expected to enhance productivity by 20%.

- In February 2024, Google LLC introduced a new generative AI model for natural language processing applications. This model aims to improve text generation accuracy by 35%.

Report Scope

Report Features Description Market Value (2023) USD 13.9 Bn Forecast Revenue (2033) USD 199.2 Bn CAGR (2024-2033) 31.4% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Services, Software, By Technology (Generative Adversarial Networks (GANs), Transformer, Variational Auto-encoder (VAE), Diffusion Networks), By End-User (Media & Entertainment, BFSI, IT & Telecommunication, Healthcare, Automotive & Transportation, Other End-Users) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape IBM Corporation, Google LLC, Microsoft Corporation, Intel Corporation, Amazon Web Services, Inc., NVIDIA Corporation, OpenAI, Alphabet Inc., Salesforce.com, Inc., Adobe Inc., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- IBM Corporation

- Google LLC

- Microsoft Corporation

- Intel Corporation

- Amazon Web Services, Inc.

- NVIDIA Corporation

- OpenAI

- Alphabet Inc.

- Salesforce.com, Inc.

- Adobe Inc.

- Other Key Players

Our Clients

View Our Licence Options