Carbonfree Market By Renewable Energy (Solar Energy, Wind Energy, Hydroelectric Power, Geothermal Energy), By Energy Storage (Lithium-ion Batteries, Flow Batteries, Pumped Hydro Storage), By Green Building Materials (Sustainable Concrete, Recycled Steel, Insulation Materials), By Carbon Offsetting (Reforestation, Renewable Energy, Methane Capture), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

47969

-

June 2024

-

136

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

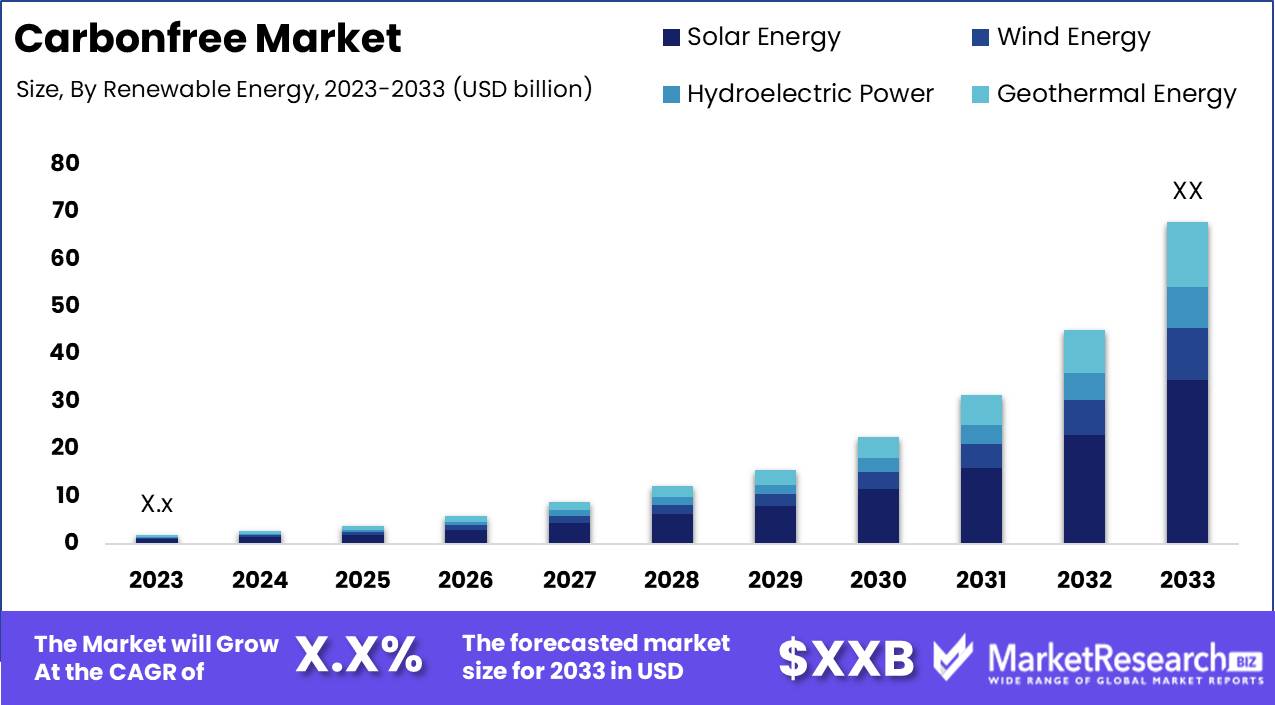

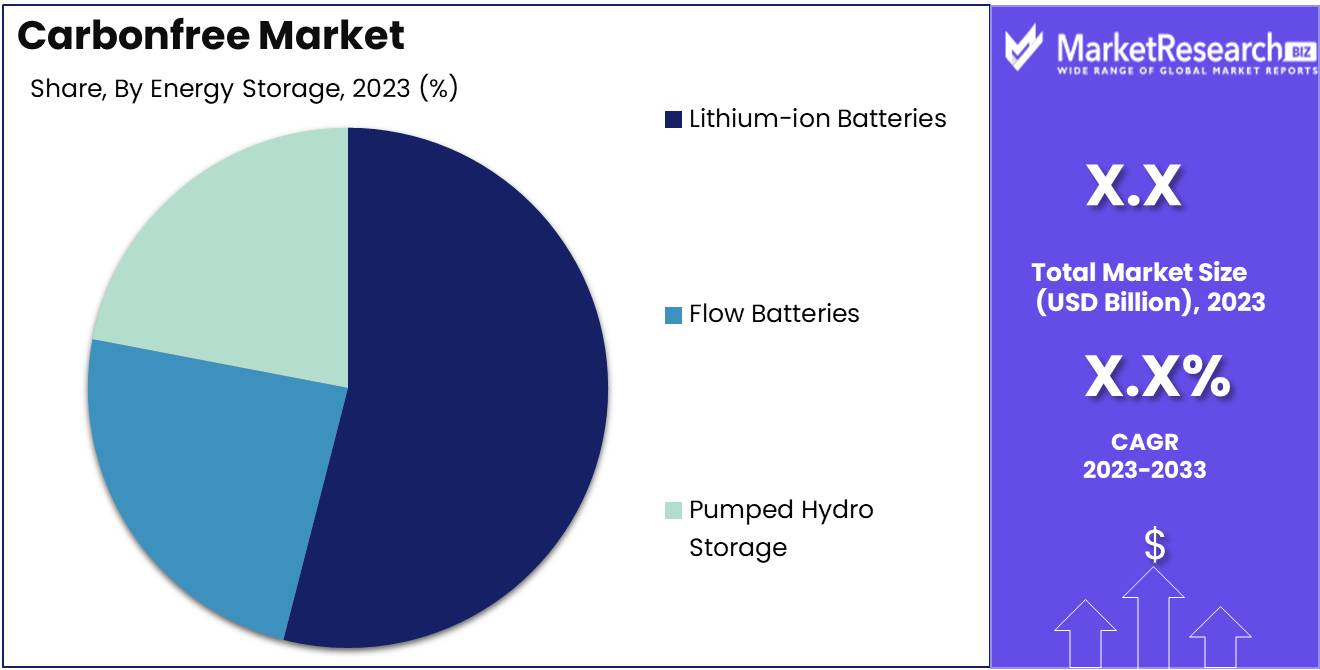

The Global Carbonfree Market was valued at USD XX Bn in 2023. It is expected to reach USD XX Bn by 2033, with a CAGR of X.X% during the forecast period from 2024 to 2033.

The Carbonfree Market refers to the ecosystem of initiatives, technologies, and strategies aimed at reducing or offsetting carbon dioxide and other greenhouse gas emissions to achieve environmental sustainability goals. This market encompasses a spectrum of solutions, including carbon offset projects, renewable energy investments, carbon capture and storage technologies, and sustainable practices across industries.

Companies participating in the Carbonfree Market strive to mitigate their environmental impact, enhance corporate social responsibility efforts, and comply with regulatory requirements related to emissions reduction. As global awareness of climate change intensifies, the Carbonfree Market offers opportunities for organizations to innovate, collaborate, and lead in fostering a greener, more sustainable future.

Companies participating in the Carbonfree Market strive to mitigate their environmental impact, enhance corporate social responsibility efforts, and comply with regulatory requirements related to emissions reduction. As global awareness of climate change intensifies, the Carbonfree Market offers opportunities for organizations to innovate, collaborate, and lead in fostering a greener, more sustainable future.The Carbonfree Market is pivotal in the global effort to combat climate change, driven by a growing imperative for organizations to adopt sustainable practices and achieve net-zero carbon emissions. As of 2024, the market encompasses a diverse array of technologies and strategies aimed at reducing greenhouse gas emissions and offsetting carbon footprints across industries. CarbonFree aims to capture 10% of global industrial carbon emissions, marking a significant milestone in advancing net-zero goals after 15 years of intensive development. This ambitious target underscores the market's potential to catalyze transformative changes in how industries approach carbon management and sustainability.

Supporting this trajectory, CarbonFree Chemicals Holdings, LLC, stands out with its extensive intellectual property portfolio, holding over 90 patents in 50 countries. As a leader in carbon capture technologies, the company exemplifies the innovation driving the Carbonfree Market forward. These patents represent critical advancements in capturing, storing, and repurposing carbon emissions, positioning CarbonFree Chemicals as a key player in the global carbon mitigation landscape.

The growth opportunities within the Carbonfree Market as regulatory pressures, consumer expectations, and investor demands for sustainability intensify. Organizations across sectors are increasingly integrating carbon reduction strategies into their operational frameworks to mitigate risks, enhance brand reputation, and capitalize on emerging market opportunities. Strategic investments in carbon capture technologies, renewable energy adoption, and collaborative industry initiatives will be pivotal in shaping the future of sustainable business practices worldwide.

Key Takeaways

- Market Growth: The Global Carbonfree Market was valued at USD XX Bn in 2023. It is expected to reach USD XX Bn by 2033, with a CAGR of X.X% during the forecast period from 2024 to 2033.

- By Renewable Energy: Solar Energy leads global renewable adoption with a substantial share of around 51%, supported by scalability, cost-efficiency, and broad sector deployment.

- By Energy Storage: Lithium-ion Batteries likely dominate energy storage with a significant share of approximately 54%, driven by their high energy density and versatile applications.

- By Green Building Materials: Sustainable Concrete holds a prominent share at about 36%, driven by advancements in low-carbon technologies and its pivotal role in sustainable construction.

- By Carbon Offsetting: Reforestation holds a significant share of around 42% as an effective measure for carbon sequestration and biodiversity conservation.

- Regional Dominance: The rice serum market in the Asia Pacific region has captured a significant 60% share.

- Growth Opportunity: Increased governmental regulations and corporate sustainability initiatives are key drivers for growth in the carbon-free market.

Driving factors

Net Zero Pledges

Net zero pledges by governments, corporations, and institutions worldwide have become pivotal in driving the growth of the Carbonfree Market. These commitments signal a widespread adoption of carbon neutrality as a goal, necessitating substantial reductions in greenhouse gas emissions. For instance, as of 2023, over 80 countries and numerous multinational corporations have committed to achieving net zero emissions by mid-century or earlier.

Such pledges create a demand for carbon offsetting solutions, spurring innovation and investment in technologies and practices that reduce and offset carbon emissions. This surge in demand not only stimulates the Carbonfree Market directly but also indirectly encourages regulatory frameworks and financial incentives that further accelerate market growth.

CCS and EOR

Carbon capture and storage (CCS) and enhanced oil recovery (EOR) technologies play a dual role in advancing the Carbonfree Market. CCS technologies enable the capture of carbon dioxide emissions from industrial processes and power generation, preventing their release into the atmosphere. This capability is crucial for industries aiming to comply with emissions regulations and achieve carbon neutrality targets.

EOR utilizes captured CO2 to enhance oil recovery from existing reservoirs, providing a financial incentive for CCS deployment. As of 2023, the global CCS market is projected to grow significantly, driven by investments in infrastructure and policy support. The synergy between CCS and EOR not only supports emissions reduction efforts but also contributes to the development of a robust Carbonfree Market ecosystem.

Decarbonization Investments

Decarbonization investments represent a critical driver behind the expansion of the Carbonfree Market, fostering innovation across various sectors. Investment flows into renewable energy sources such as solar power, wind, and hydrogen as a fuel technologies are reshaping energy landscapes globally. As of early 2023, global investments in renewable energy surpassed USD 300 billion annually, with projections indicating continued growth.

These investments not only accelerate the deployment of clean energy solutions but also bolster demand for carbon offset projects and technologies that facilitate emissions reductions. Furthermore, financial support for sustainable practices and technologies enhances market competitiveness and scalability, attracting a broader range of stakeholders into the Carbonfree Market.

Restraining Factors

High CCS Costs

High costs associated with Carbon Capture and Storage (CCS) technologies present a significant challenge in the development of the Carbonfree Market. Despite advancements, CCS remains a capital-intensive process, with costs varying depending on the scale, technology used, and geological considerations. The costs impact market dynamics by influencing project feasibility and economic viability, particularly in industries with narrow profit margins or limited access to financing.

However, the market response to high CCS costs is multifaceted. Governments and international organizations are increasingly implementing policies and financial mechanisms to mitigate investment risks and incentivize CCS deployment. Initiatives such as carbon pricing mechanisms, tax credits, and subsidies aim to reduce the cost burden on industries adopting CCS technologies. Furthermore, collaborative efforts between public and private sectors facilitate knowledge sharing, technology innovation, and scaling of CCS infrastructure, driving down costs over time.

Energy Storage Limitations

Energy storage limitations pose a critical challenge to the expansion of the Carbonfree Market, particularly in the context of renewable energy integration and grid stability. The intermittent nature of renewable energy sources such as solar and wind necessitates effective energy storage solutions to ensure reliable power supply and grid resilience. The variability in renewable energy generation patterns requires storage technologies capable of storing excess energy during peak production periods and dispatching it during periods of low generation.

The impact of energy storage limitations on the Carbonfree Market is multifaceted. Insufficient storage capacity can hinder the widespread adoption of renewable energy sources, limiting their potential to replace fossil fuels and reduce carbon emissions. This constraint also affects the economic competitiveness of renewable energy projects, as energy storage costs contribute significantly to overall system costs.'

By Renewable Energy Analysis

The Carbonfree Market sees solar energy leading renewable energy sources with a 51% share

In 2023, Solar Energy held a dominant market position in the By Renewable Energy segment of the Carbonfree Market, capturing more than a 51% share. This segment's leadership underscores the widespread adoption and investment in solar power as a key driver of renewable energy transition globally. Solar energy's appeal lies in its abundant availability, scalability, and decreasing costs of solar technologies, making it a viable solution for reducing carbon emissions and meeting sustainability goals across various sectors.

Wind Energy emerged as another significant segment within the Carbonfree Market, holding a substantial market share exceeding 32%. Wind power installations have expanded rapidly, driven by technological advancements, favorable government policies, and growing investments in wind farms and offshore wind projects. Wind energy's contribution to the renewable energy mix is characterized by its reliability, low environmental impact, and potential for significant energy generation capacity.

Hydroelectric Power, while traditionally a dominant source of renewable energy, maintains a notable presence in the Carbonfree Market. With a market share reflecting established infrastructure and continuous development in hydropower plants, this segment harnesses the kinetic energy of flowing water to generate electricity efficiently. Hydroelectric power plays a crucial role in providing stable and renewable energy supply, particularly in regions with abundant water resources.

Geothermal Energy, though representing a smaller segment compared to solar and wind energy, is gaining recognition for its potential as a reliable and sustainable energy source. Geothermal power utilizes heat from the Earth's subsurface to generate electricity and heat buildings, offering consistent baseload power generation with minimal environmental impact.

By Energy Storage Analysis

Lithium-ion batteries dominate energy storage solutions at 54%.

In 2023, Lithium-ion Batteries held a dominant market position in the By Energy Storage segment of the Carbonfree Market, capturing more than a 54% share. This segment's leadership underscores the widespread adoption and technological advancements in lithium-ion batteries, driven by their high energy density, efficiency, and versatility across various applications in renewable energy integration, electric vehicles (EVs), and grid stabilization initiatives. Lithium-ion batteries are favored for their rapid charge/discharge capabilities, long cycle life, and compact size, making them ideal for storing intermittent renewable energy sources like solar and wind power.

Flow Batteries emerged as another significant segment within the Carbonfree Market's Energy Storage landscape, holding a substantial market share exceeding 30%. Flow batteries offer advantages such as scalability, long-duration energy storage capabilities, and enhanced safety compared to traditional lithium-ion batteries.

Pumped Hydro Storage, while representing a smaller segment compared to lithium-ion and flow batteries, plays a critical role in the Carbonfree Market's energy storage mix. This technology utilizes gravitational potential energy by pumping water uphill during periods of low demand and releasing it to generate electricity during peak demand. Pumped hydro storage facilities contribute to grid stability, support renewable energy intermittency management, and provide reliable energy supply during periods of high demand.

By Green Building Materials Analysis

Sustainable concrete emerging at 36% for green building materials

In 2023, Sustainable Concrete held a dominant market position in the By Green Building Materials segment of the Carbonfree Market, capturing more than a 36% share. This segment's leadership underscores the increasing focus on sustainable construction practices and materials that minimize environmental impact while promoting energy efficiency and durability in building projects. Sustainable concrete, characterized by the use of recycled materials like fly ash, slag, and recycled aggregates, offers reduced carbon footprints and enhanced performance compared to traditional concrete, making it a preferred choice for green building certifications and regulatory compliance.

Recycled Steel emerged as another significant segment within the Carbonfree Market's Green Building Materials landscape, holding a substantial market share exceeding 28%. Utilizing recycled steel reduces energy consumption, greenhouse gas emissions, and landfill waste associated with traditional steel production.

Insulation Materials, while representing a smaller segment compared to sustainable concrete and recycled steel, play a crucial role in enhancing building energy efficiency and reducing carbon emissions.

By Carbon Offsetting Analysis

Reforestation is the leading method of carbon offsetting in the carbonfree market, accounting for 42% of efforts

In 2023, Reforestation held a dominant market position in the By Carbon Offsetting segment of the Carbonfree Market, capturing more than a 42% share. This segment's leadership underscores the critical role of reforestation projects in sequestering carbon dioxide from the atmosphere, mitigating climate change impacts, and enhancing biodiversity conservation. Reforestation initiatives involve planting trees and restoring forest ecosystems, which absorb carbon dioxide through photosynthesis and store carbon in biomass and soil, making them effective carbon offsetting strategies endorsed by international climate agreements and corporate sustainability commitments.

Renewable Energy emerged as another significant segment within the Carbon Offsetting landscape, holding a substantial market share exceeding 30%. Renewable energy projects, such as wind farms, solar installations, and hydroelectric dams, generate clean electricity that displaces fossil fuel-based power generation, thereby reducing greenhouse gas emissions. These projects contribute to carbon offsetting efforts by promoting sustainable energy production and supporting global decarbonization goals.

Methane Capture, while representing a smaller segment compared to reforestation and renewable energy, plays a crucial role in reducing potent greenhouse gas emissions from industrial processes, landfills, and agricultural activities. Methane capture projects capture methane emissions and convert them into energy or other useful products, thereby preventing methane from entering the atmosphere and contributing to global warming.

Key Market Segments

By Renewable Energy

- Solar Energy

- Wind Energy

- Hydroelectric Power

- Geothermal Energy

By Energy Storage

- Lithium-ion Batteries

- Flow Batteries

- Pumped Hydro Storage

By Green Building Materials

- Sustainable Concrete

- Recycled Steel

- Insulation Materials

By Carbon Offsetting

- Reforestation

- Renewable Energy

- Methane Capture

Growth Opportunity

Compliance Market Expansion

The year 2024 presents significant opportunities for the global Carbonfree Market, propelled by expanding compliance requirements worldwide. The European Union's Emissions Trading System (EU ETS) continues to evolve, with plans to further reduce emissions and expand coverage to new sectors, driving demand for carbon offsetting solutions and technologies. This regulatory framework not only mandates emissions reductions but also incentivizes industries to invest in carbon-neutral practices and technologies, stimulating market growth.

The compliance market's expansion fosters innovation in Carbon Capture and Storage (CCS), renewable energy, and energy efficiency solutions. Industries are incentivized to adopt sustainable practices to avoid penalties and capitalize on carbon credit trading opportunities. The growing participation of corporations in voluntary carbon markets further amplifies market dynamics, creating a robust ecosystem of buyers and sellers committed to carbon neutrality goals.

Government Incentives

Government incentives play a pivotal role in unlocking growth opportunities within the Carbonfree Market in 2024. Across regions, policymakers are deploying fiscal measures, grants, and subsidies to accelerate the deployment of renewable energy, energy storage, and CCS technologies. The United States' Build Back Better Act includes substantial funding for clean energy projects and carbon capture initiatives, aiming to reduce emissions and create green jobs. These incentives not only reduce financial barriers for market entry but also spur private sector investment in sustainable infrastructure and innovation.

Government-backed research and development programs facilitate technological advancements and cost reductions in key areas such as direct air capture and hydrogen production, enhancing the competitiveness of Carbonfree Market solutions. By aligning regulatory frameworks with financial support, governments worldwide are fostering a conducive environment for market expansion and accelerating the transition towards a low-carbon economy.

Latest Trends

Difficult System Transition

In 2024, the global Carbonfree Market faces the complex challenge of transitioning from fossil fuel dependency to sustainable, carbon-neutral practices. This shift requires substantial investments in renewable energy infrastructure, carbon capture technologies, and energy storage solutions. Despite growing awareness and regulatory support, the transition is hindered by existing infrastructural dependencies and economic considerations.

Industries must navigate the dual challenge of reducing emissions while maintaining operational efficiency and profitability. Stakeholders are increasingly adopting phased approaches and collaborative strategies to mitigate risks and ensure a smooth transition.

Interconnected Solutions

A notable trend in 2024 is the integration of interconnected solutions within the Carbonfree Market ecosystem. This approach emphasizes synergies between renewable energy deployment, carbon capture and storage (CCS) technologies, and sustainable practices across industries.

Hybrid renewable energy systems combining solar, wind, and storage technologies are gaining traction, offering grid stability and reliability while reducing carbon footprints. Collaborative initiatives between sectors such as transportation, agriculture, and manufacturing are exploring holistic strategies to achieve carbon neutrality goals collectively.

Carbon-Free Innovation

Innovation remains a cornerstone of the Carbonfree Market in 2024, with a focus on developing and scaling carbon-free technologies. Key innovations include advancements in direct air capture, green hydrogen production, and bio-based materials, which promise to revolutionize emissions reduction efforts.

Governments and private sector entities are investing heavily in research and development to accelerate the commercialization of these technologies. The emergence of circular economy principles and sustainable supply chain practices underscores a shift towards holistic, lifecycle-oriented solutions that minimize environmental impact.

Regional Analysis

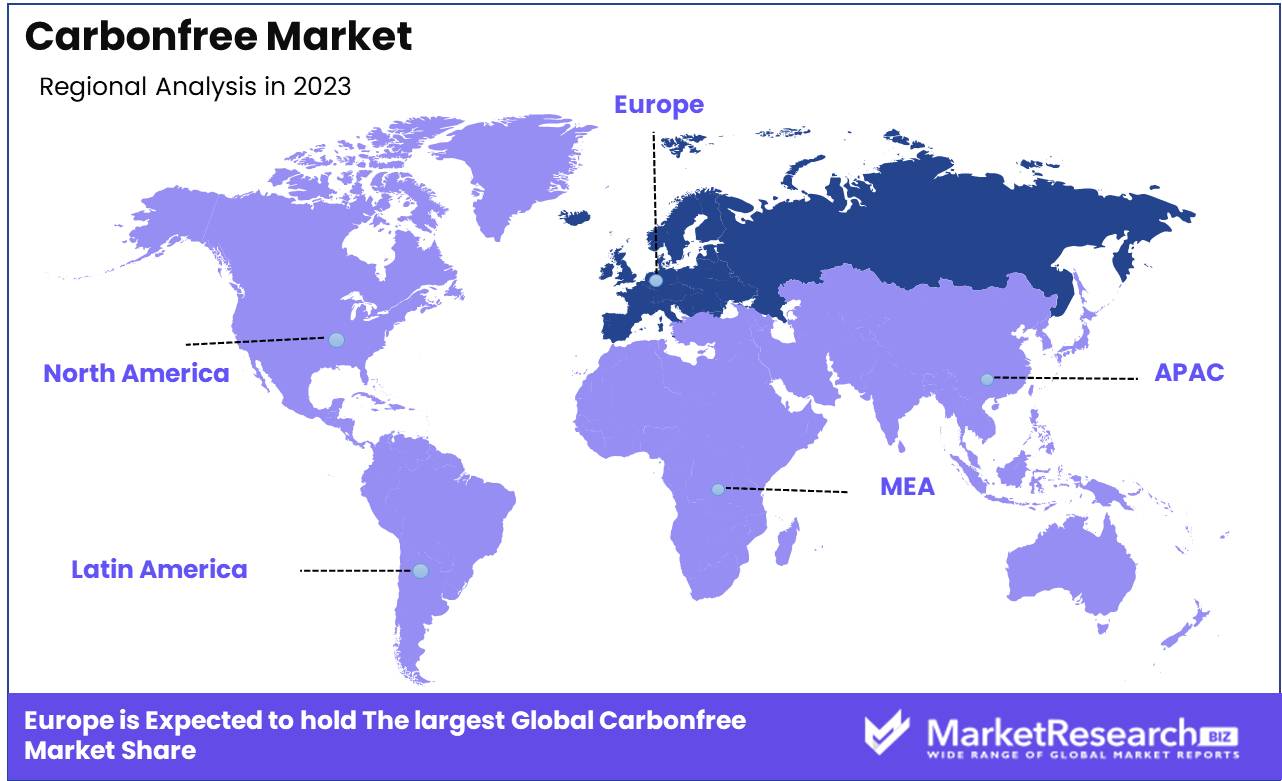

Europe leads the global rice serum market with a dominant 45% share, driven by a strong preference for natural and organic skincare products

The rice serum market exhibits distinct regional characteristics, influenced by local consumer preferences, market maturity, and economic conditions. Europe dominates the global market with a significant 45% share, driven by a strong inclination towards natural and organic skincare products. The European market also enjoys robust regulatory frameworks that ensure product quality and safety, further enhancing consumer trust.

In North America, the rice serum market is growing steadily, with the United States and Canada leading the charge. The region's market growth is fueled by an increasing demand for natural and organic skincare solutions, driven by a health-conscious consumer base. The presence of a strong distribution network and advanced online retail channels also supports market expansion. However, competition from other natural skincare products presents a challenge.

Asia Pacific, while not the largest market, shows significant potential for growth due to its historical and cultural affinity for rice-based products. Countries like Japan, South Korea, and China are major players, supported by their advanced skincare industries and innovative product development. The region's market is characterized by high consumer awareness and demand for effective skincare solutions.

The Middle East & Africa region is emerging as a promising market for rice serum, driven by rising disposable incomes and a growing preference for premium skincare products. The UAE and South Africa are notable markets, where consumer interest in natural and organic products is on the rise.

Latin America is gradually adopting rice serum, with Brazil and Mexico being the primary markets. The region's growth is supported by an expanding middle class, increasing internet penetration, and a rising beauty consciousness among consumers.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The global carbon-free market in 2024 is set to expand significantly, driven by heightened environmental awareness, government regulations, and technological advancements. Key players in this market are leveraging their strengths to drive the transition toward a more sustainable future.

Tesla, with its cutting-edge electric vehicles (EVs) and Powerwall energy storage solutions, is at the forefront of the carbon-free movement. Tesla's advancements in battery technology and renewable energy integration are pivotal in reducing carbon emissions across transportation and residential sectors.

NextEra Energy stands out as a leader in renewable energy, particularly in wind and solar power generation. Their substantial investments in clean energy infrastructure and innovative solutions are crucial in supporting the global shift towards carbon-free electricity.

Vestas, a dominant force in the wind energy industry, continues to push the boundaries with its high-efficiency wind turbines. Vestas' global reach and expertise in wind energy technology play a significant role in reducing reliance on fossil fuels.

BYD and LG Chem are key players in the EV and battery markets. BYD's comprehensive range of electric vehicles and LG Chem's advanced battery technologies are essential in promoting sustainable transportation and energy storage solutions.

LafargeHolcim and Saint-Gobain are leading the charge in the construction sector by developing sustainable building materials and practices. Their innovations in low-carbon cement and energy-efficient building solutions are crucial for reducing the carbon footprint of the construction industry.

Owens Corning focuses on energy-efficient insulation and building materials, contributing to significant energy savings and reduced greenhouse gas emissions in the construction and housing sectors.

Terrapass and 3Degrees are instrumental in providing carbon offset solutions and renewable energy credits, helping businesses and individuals mitigate their carbon footprints. Their services are vital for companies aiming to achieve carbon neutrality.

Market Key Players

- Tesla

- NextEra Energy

- Vestas

- BYD

- LG Chem

- LafargeHolcim

- Saint-Gobain

- Owens Corning

- Terrapass

- 3Degrees

Recent Development

- In June 2024, Labour Party aims for UK to be a 'clean energy superpower' by 2030 through Great British Energy, focusing on renewables despite concerns over costs and job losses.

- In June 2024, US DOE focuses on advancing nuclear energy technologies and fuel cycle sustainability to bolster economic competitiveness and address public and logistical challenges in the industry.

Report Scope

Report Features Description Market Value (2023) USD XX Bn Forecast Revenue (2033) USD XX Bn CAGR (2024-2033) X.X% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Renewable Energy (Solar Energy, Wind Energy, Hydroelectric Power, Geothermal Energy), By Energy Storage (Lithium-ion Batteries, Flow Batteries, Pumped Hydro Storage), By Green Building Materials (Sustainable Concrete, Recycled Steel, Insulation Materials), By Carbon Offsetting (Reforestation, Renewable Energy, Methane Capture) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Tesla, NextEra Energy, Vestas, BYD, LG Chem, LafargeHolcim, Saint-Gobain, Owens Corning, Terrapass, 3Degrees Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Tesla

- NextEra Energy

- Vestas

- BYD

- LG Chem

- LafargeHolcim

- Saint-Gobain

- Owens Corning

- Terrapass

- 3Degrees

Our Clients

View Our Licence Options