Solar Power Market By Application (Residential, Commercial, Industrial),By Technology (Photovoltaic Systems and Concentrated Solar Power Systems), By End Use (Electricity Generation, Lighting, Heating, Charging), By Solar Module (Monocrystalline, Polycrystalline, Cadmium Telluride, Amorphous Silicon Cells, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

1471

-

July 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

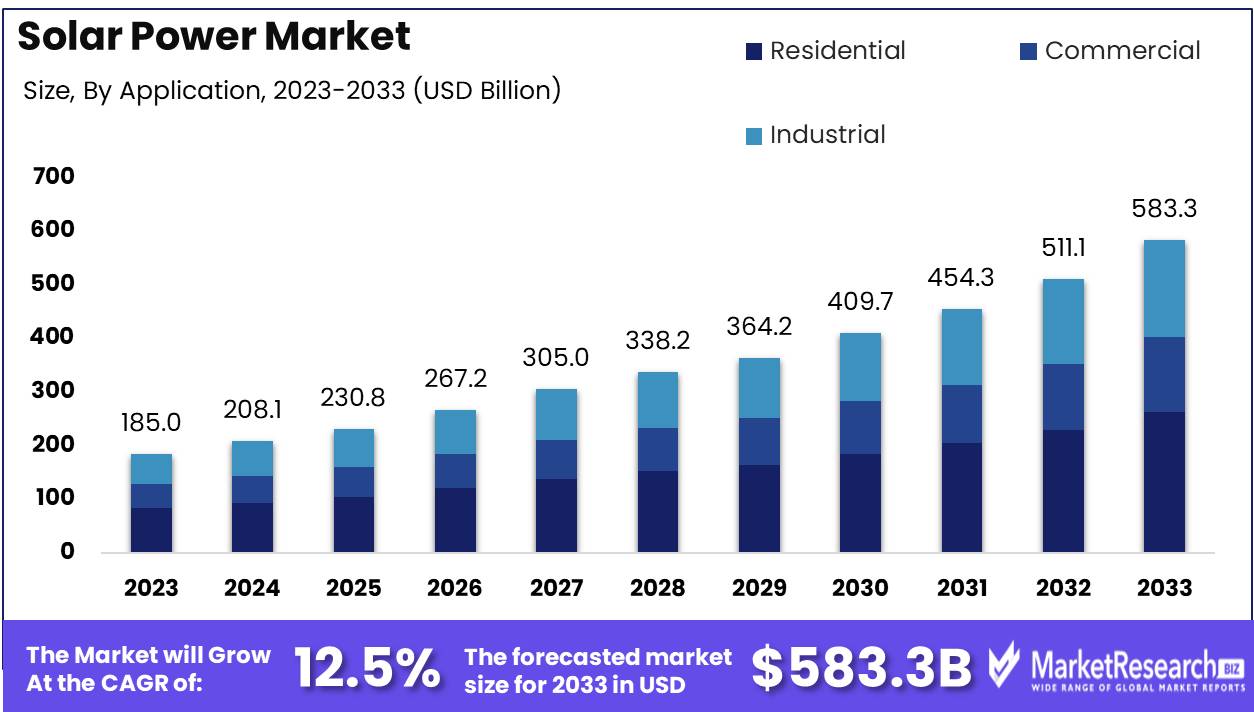

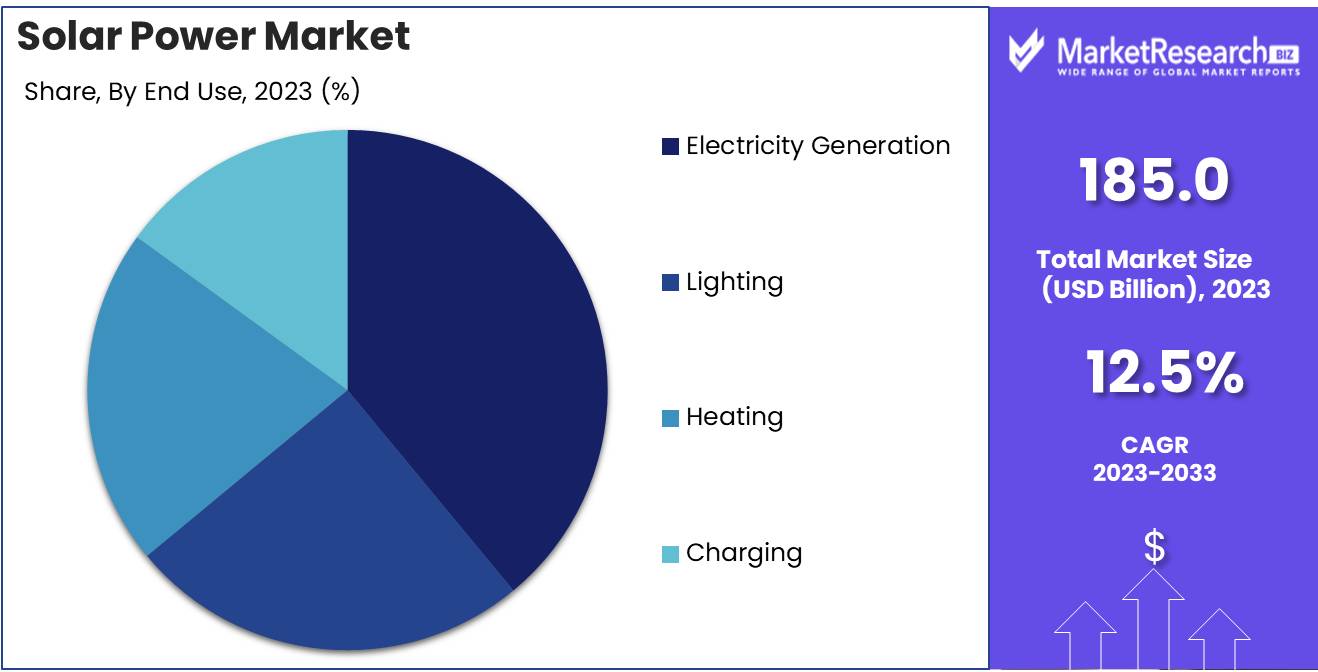

The Solar Power Market was valued at USD 185.0 billion in 2023. It is expected to reach USD 583.3 billion by 2033, with a CAGR of 12.5% during the forecast period from 2024 to 2033.

The Solar Power Market encompasses the global industry involved in the production, distribution, and consumption of energy harnessed from solar radiation. It includes various technologies such as photovoltaic (PV) systems, concentrated solar power (CSP), and solar thermal applications. The market is driven by increasing demand for renewable energy sources, advancements in solar technology, and supportive government policies promoting sustainable energy. It covers residential, commercial, and utility-scale sectors, providing solutions for reducing carbon footprints and ensuring energy security.

The Solar Power Market has shown remarkable growth over the past decade, driven by a confluence of factors that have collectively enhanced its attractiveness and viability as a renewable energy source. Declining costs of solar panels have been pivotal, significantly lowering the barrier to entry and making solar energy a more economically feasible option for both residential and commercial consumers. This trend is further bolstered by robust government initiatives and policies aimed at promoting renewable energy adoption. For instance, subsidies, tax incentives, and favorable regulatory frameworks have played crucial roles in accelerating solar power deployment.

However, the market is not without its challenges. The high initial capital investment required for solar power installations remains a significant hurdle, particularly for small and medium enterprises and residential users. Despite this, the overall market outlook remains positive, supported by ongoing advancements in solar technologies.

Continued innovations, particularly in perovskite solar cells and bifacial panels, are expected to drive further market growth by enhancing efficiency and reducing costs. These technological advancements are poised to address some of the current limitations of traditional silicon-based solar panels, offering higher energy yields and better performance in diverse environmental conditions. The integration of these advanced technologies could significantly improve the return on investment for solar power systems, making them more attractive to a broader range of consumers. Moreover, as global efforts to combat climate change intensify, the emphasis on renewable energy sources like solar power is expected to increase, providing a robust impetus for market expansion.

Key Takeaways

- Market Growth: The Solar Power Market was valued at USD 185.0 billion in 2023. It is expected to reach USD 583.3 billion by 2033, with a CAGR of 12.5% during the forecast period from 2024 to 2033.

- By Application: The Residential sector dominated the Solar Power Market.

- By Technology: Photovoltaic Systems dominated the Solar Power Market technology segment.

- By End Use: Electricity Generation dominated the solar power market end-use in 2023.

- By Solar Module: Monocrystalline modules dominated the Solar Power Market segment.

- Regional Dominance: Asia Pacific dominates the global solar power market with a 55% largest share.

- Growth Opportunity: The convergence of supportive government policies and the declining costs of solar technology presents a robust growth opportunity for the global solar power market.

Driving factors

Growing Need for Clean, Renewable Energy Sources

The demand for clean, renewable energy sources is a primary driving factor for the growth of the solar power market. With increasing concerns over climate change, greenhouse gas emissions, and the depletion of fossil fuels, there is a significant shift towards sustainable energy solutions. Governments worldwide are implementing stringent regulations and offering incentives to promote renewable energy adoption. For instance, the European Union's Renewable Energy Directive aims for at least 32% of energy consumption to come from renewable sources by 2030. This regulatory push, combined with rising public awareness and corporate sustainability initiatives, significantly boosts the solar power market.

Falling Prices of Solar Photovoltaic (PV) Systems

Technological improvements, economies of scale, and better manufacturing techniques have led to a dramatic decrease in the prices of solar photovoltaic (PV) systems. The cost of solar PV modules has fallen by approximately 80% over the past decade. This reduction makes solar energy more competitive with traditional energy sources and increases its attractiveness to consumers and businesses. As installation costs decrease, the return on investment for solar power systems improves, further driving market growth. Additionally, financing options such as solar leases and power purchase agreements (PPAs) have made it easier for consumers to adopt solar energy without significant upfront costs.

Advancements in Solar Technology

Advancements in solar technology play a crucial role in the market's expansion. Innovations such as bifacial solar panels, which capture sunlight from both sides and perovskite solar cells, known for their high efficiency and lower production costs, are enhancing the performance and affordability of solar power systems. These technological breakthroughs increase the efficiency of solar energy conversion and expand the potential applications of solar power. For instance, improvements in energy storage solutions, such as lithium-ion batteries, enable more efficient storage and use of solar energy, addressing the intermittency issue associated with solar power. As a result, these advancements make solar power a more viable and reliable energy source, encouraging broader adoption.

Restraining Factors

Adverse Effects of Extreme Heat on Solar Panel Efficiency and Longevity

Heat waves pose a significant challenge to the solar power market, primarily due to their detrimental impact on the efficiency and longevity of solar panels. Solar photovoltaic (PV) systems are designed to perform optimally within a specific temperature range, usually between 25°C to 30°C (77°F to 86°F). When temperatures exceed this range, the efficiency of solar panels drops, as excessive heat increases the resistance in photovoltaic cells, thereby reducing their ability to convert sunlight into electricity. This phenomenon is quantified by the temperature coefficient of a solar panel, typically around -0.3% to -0.5% per degree Celsius rise above the optimal temperature. For instance, if a solar panel has a temperature coefficient of -0.4%/°C and the temperature rises by 10°C above the ideal range, the panel’s efficiency would decrease by 4%.

Moreover, prolonged exposure to high temperatures can accelerate the degradation of solar panels, shortening their lifespan and increasing maintenance costs. This is particularly concerning in regions prone to frequent and intense heat waves, which are becoming more common due to climate change. The increased degradation rate leads to higher operational costs over the panel's lifetime, thereby making solar investments less attractive compared to other renewable energy sources or traditional fossil fuels.

Financial Hurdles Stemming from Prolonged Payback Periods for Solar Investments

One of the most significant restraining factors for the solar power market is the extended return on investment (ROI) period. Solar power projects typically require substantial upfront capital investment, including costs for purchasing and installing solar panels, inverters, batteries, and other necessary infrastructure. Despite the declining cost of solar technology over recent years, the initial expenditure remains a barrier for many potential investors and consumers.

The payback period for solar investments, which is the time taken to recover the initial costs from energy savings, can be lengthy, often ranging from 7 to 12 years, depending on factors such as geographic location, local energy prices, and available financial incentives. This extended ROI period can deter both individual consumers and large-scale investors, as the financial returns are not immediately realized. In comparison, investments in other forms of energy generation, such as natural gas or coal, often have shorter payback periods due to established infrastructure and market stability.

By Application Analysis

In 2023, The Residential sector dominated the Solar Power Market.

In 2023, The Residential sector held a dominant market position in the By Application segment of the Solar Power Market. This dominance is attributed to increasing consumer awareness about renewable energy sources and supportive government policies, such as tax incentives and rebates, which have significantly driven the adoption of residential solar power systems. The rise in electricity prices has also incentivized homeowners to switch to solar energy as a cost-effective alternative. The Residential segment's market share was further bolstered by advancements in solar technology, leading to more efficient and aesthetically pleasing solar panels that integrate seamlessly into residential settings.

The Commercial segment also exhibited substantial growth, driven by businesses seeking to reduce their operational costs and carbon footprints. Companies are increasingly investing in solar installations to meet sustainability goals and to leverage financial benefits from energy savings.

The Industrial segment, while growing, remains less dominant compared to Residential and Commercial applications. This segment's growth is supported by large-scale industrial facilities seeking to mitigate energy expenses and improve energy independence. The integration of solar power in industrial applications is gaining traction, particularly in regions with high solar irradiance and robust industrial activities.

By Technology Analysis

In 2023, Photovoltaic Systems dominated the Solar Power Market technology segment.

In 2023, Photovoltaic (PV) Systems held a dominant market position in the By Technology segment of the Solar Power Market. This prominence is attributed to several factors, including advancements in PV technology, cost reductions, and increased efficiency. PV systems, which convert sunlight directly into electricity using semiconductor materials, have become increasingly favored due to their scalability and applicability in various settings, from residential rooftops to large-scale solar farms. The global push for renewable energy sources, coupled with supportive government policies and subsidies, has further fueled the adoption of PV systems. Additionally, innovations such as bifacial panels and improved inverter technologies have enhanced the performance and attractiveness of PV installations.

In contrast, Concentrated Solar Power (CSP) Systems, which use mirrors or lenses to concentrate sunlight to generate heat and produce electricity, accounted for a smaller share of the market. While CSP offers advantages like thermal storage capabilities, its higher installation costs and geographical limitations have constrained its growth compared to PV systems. As a result, PV systems are anticipated to continue leading the technology segment in the solar power industry.

By End-Use Analysis

Electricity Generation dominated the solar power market end-use in 2023.

In 2023, Electricity Generation held a dominant market position in the end-use segment of the Solar Power Market. This segment accounted for a substantial share due to the increasing adoption of solar panels for residential, commercial, and industrial power generation. The transition towards renewable energy sources and government incentives significantly boosted the deployment of solar power systems for electricity generation.

Lighting applications also contributed significantly to the market, driven by the growing use of solar-powered streetlights and off-grid lighting solutions, especially in remote and rural areas. The need for sustainable and cost-effective lighting solutions has accelerated the demand for solar lighting, further supported by advancements in LED technology.

Heating applications, including solar water heaters and solar space heating systems, witnessed steady growth. The push for energy-efficient heating solutions and the rising cost of conventional fuels have made solar heating an attractive alternative, particularly in regions with high solar insolation.

Lastly, Charging applications, including solar chargers for electronic devices and electric vehicles, emerged as a promising segment. The rise of electric mobility and portable solar chargers for outdoor activities and remote locations have fueled this segment's growth. Overall, the solar power market's segmentation by end-use highlights the diverse applications and significant potential for growth across different sectors, underscoring the versatility and expanding reach of solar energy technologies.

By Solar Module Analysis

In 2023, Monocrystalline modules dominated the Solar Power Market segment.

In 2023, Monocrystalline held a dominant market position in the Solar Power Market's By Solar Module segment. Monocrystalline solar modules, known for their high efficiency and durability, continued to attract significant investments, particularly in regions with limited space for solar installations. Their superior performance in converting sunlight into electricity made them a preferred choice among residential and commercial users.

Polycrystalline modules, while less efficient than Monocrystalline, offered a cost-effective alternative for large-scale installations where space constraints were less of an issue. Their popularity remained strong in regions prioritizing lower upfront costs over efficiency.

Cadmium Telluride (CdTe) modules, known for their lower production costs and superior performance in hot climates, gained traction in utility-scale projects. Their thin-film technology allowed for flexibility and ease of installation, contributing to their growing market share.

Amorphous Silicon Cells, another type of thin-film technology, were recognized for their adaptability and lower cost, despite having lower efficiency compared to crystalline modules. They found niche applications in portable solar devices and building-integrated photovoltaics (BIPV).

The "Others" category included emerging technologies and hybrid solutions that combined different types of solar cells to optimize performance. Innovations in this segment focused on improving efficiency and reducing production costs, aiming to challenge the dominance of established module types in the coming years.

Key Market Segments

By Application

- Residential

- Commercial

- Industrial

By Technology

- Photovoltaic Systems

- Concentrated Solar Power Systems

By End Use

- Electricity Generation

- Lighting

- Heating

- Charging

By Solar Module

- Monocrystalline

- Polycrystalline

- Cadmium Telluride

- Amorphous Silicon Cells

- Others

Growth Opportunity

Growing Government Incentives and Subsidies as a Catalyst for Growth

The global solar power market is poised for significant growth, largely driven by increasing government incentives and subsidies. Governments worldwide are increasingly recognizing the importance of renewable energy in mitigating climate change and reducing dependence on fossil fuels. As a result, there has been a notable uptick in policies favoring solar power installations. For instance, the U.S. government has extended the Investment Tax Credit (ITC) for solar energy, which provides a 26% tax credit for residential and commercial solar systems. Similarly, the European Union's Green Deal aims to boost renewable energy projects, with substantial funding allocated for solar initiatives. These incentives not only reduce the initial cost burden for consumers but also make solar investments more attractive to private sectors, thereby driving market expansion.

Declining Costs of Solar Technology as a Major Enabler

The continuous decline in the costs of solar technology has also emerged as a major enabler for the solar power market. Over the past decade, advancements in photovoltaic technology and increased production efficiency have led to a dramatic decrease in the cost per watt of solar panels. According to the report, the global weighted average levelized cost of electricity (LCOE) for utility-scale solar photovoltaics fell by 85% between 2010 and 2020. This trend is expected to continue, making solar energy increasingly cost-competitive with traditional energy sources. The reduced costs not only lower the barriers to entry for new market players but also enhance the return on investment for solar power projects, encouraging more widespread adoption.

Latest Trends

Advancements in Solar PV Technology Drive Efficiency and Adoption

The solar power market is poised for substantial growth, primarily driven by significant advancements in solar photovoltaic (PV) technology. Innovations in PV cells, such as perovskite solar cells and bifacial modules, are expected to increase energy conversion efficiency and reduce production costs. These advancements enable solar panels to generate more electricity from the same amount of sunlight, making solar energy more competitive with traditional energy sources. Furthermore, the integration of advanced materials and improved manufacturing processes will enhance the durability and lifespan of solar panels, leading to a lower total cost of ownership for consumers and businesses alike.

AI and Automation in Solar: Enhancing System Performance and Maintenance

Artificial intelligence (AI) and automation are transforming the solar power industry by optimizing system performance and reducing operational costs. AI algorithms are being used to predict energy output, manage energy storage, and balance supply and demand more efficiently. Predictive maintenance powered by AI can identify potential issues before they become critical, minimizing downtime and extending the lifespan of solar installations. Additionally, automation in the manufacturing and installation processes is accelerating deployment rates and reducing labor costs. Automated drones and robots are increasingly being employed for site assessments, panel cleaning, and maintenance tasks, ensuring precision and safety while lowering operational expenses.

Regional Analysis

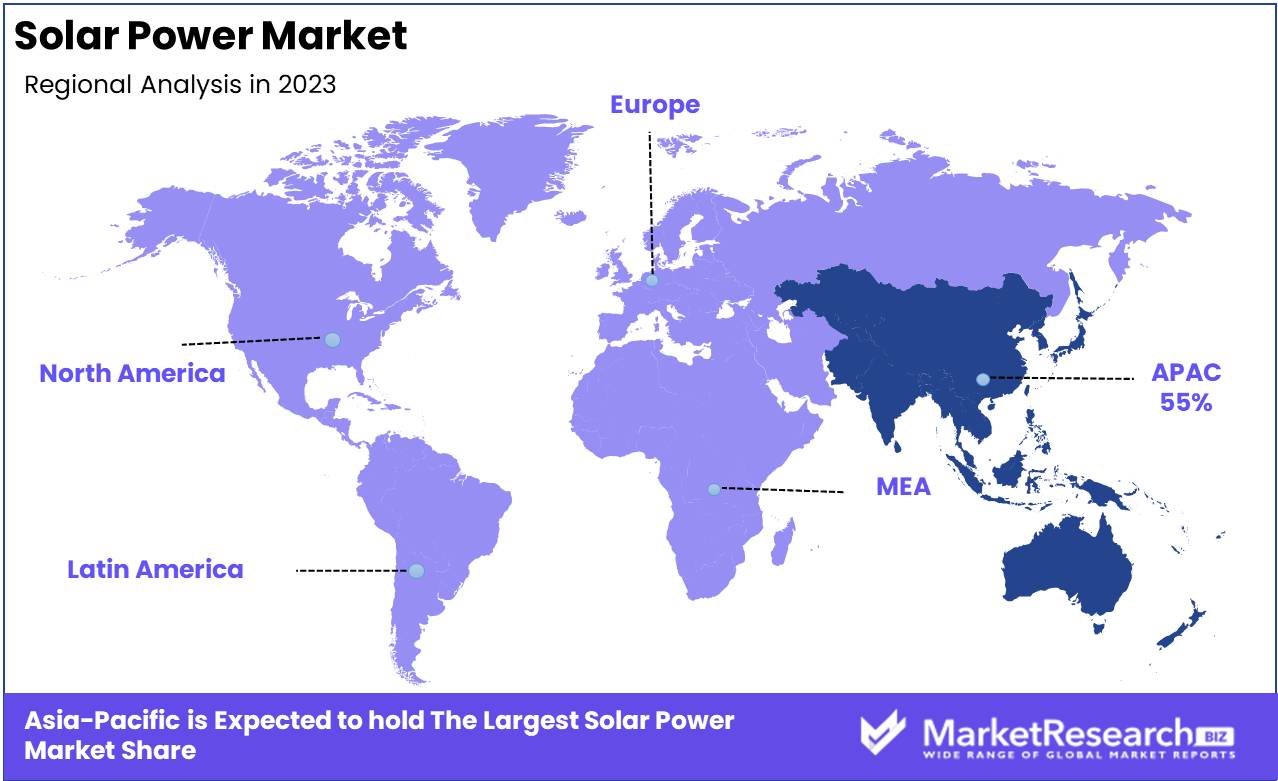

Asia Pacific dominates the global solar power market with a 55% largest share.

The Solar Power Market has witnessed significant growth across various regions, with Asia Pacific leading the charge. In Asia Pacific, countries such as China, India, and Japan have heavily invested in solar power infrastructure, driven by government initiatives and favorable policies. This region accounted for approximately 55% of the global market share in 2023, underpinned by China’s dominant position with its expansive solar farms and manufacturing capabilities.

North America follows, with the United States and Canada being the primary contributors. The region's market share stood at around 20%, propelled by federal incentives, technological advancements, and increasing adoption of residential and commercial solar systems. Europe, encompassing nations like Germany, Spain, and Italy, holds a significant market share of 15%. The region benefits from supportive regulatory frameworks and a strong focus on renewable energy targets set by the European Union.

The Middle East & Africa region is emerging as a promising market, with a market share of 5%. The sunny climate and high solar irradiance in countries like the UAE and South Africa present vast opportunities for solar power generation. Lastly, Latin America, with countries such as Brazil and Mexico, captures 5% of the market. The region's growth is fueled by rising electricity demand and government initiatives to diversify energy sources.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global solar power market continues to experience significant growth, driven by advancements in technology, government incentives, and the rising demand for clean energy. Key players are strategically positioning themselves to leverage these opportunities.

Canadian Solar Inc. and SunPower Corporation remain at the forefront, capitalizing on their established market presence and extensive portfolios of innovative solar solutions. Their commitment to research and development ensures they stay ahead in efficiency and cost-effectiveness.

Yingli Green Energy Holding Company Limited and JA Solar Holdings Co. Ltd. are expanding their global footprints, focusing on emerging markets with high solar potential. Their competitive pricing and robust supply chains provide a strong foundation for growth.

Enphase Energy, Inc. and SolarEdge Technologies continue to lead in solar inverter technologies, offering advanced systems that enhance the efficiency and reliability of solar installations. Their innovative products are critical in optimizing energy production and management.

First Solar, Inc. and JinkoSolar Holding Co., Ltd. are enhancing their manufacturing capacities and investing in new technologies to meet the growing demand. Their large-scale projects and strategic partnerships solidify their market positions.

Hanwha Q Cells Co., Ltd., Trina Solar, and Tata Power Solar System Ltd. are expanding their project portfolios, emphasizing sustainability and efficiency. Their focus on integrated solar solutions supports their growth in various regional markets.

Abengoa, Waaree Group, General Electric Company, BrightSource Energy, Inc., Urja Global Limited, and eSolar Inc. are also contributing to market dynamics through diverse offerings, from photovoltaic systems to concentrated solar power projects. Their technological advancements and strategic collaborations are pivotal in driving the global transition towards renewable energy.

This collective effort of key players is shaping a competitive and innovative landscape, propelling the solar power market toward a sustainable future.

Market Key Players

- Canadian Solar Inc.

- SunPower Corporation

- Yingli Green Energy Holding Company Limited

- Enphase Energy, Inc.

- First Solar, Inc.

- SolarEdge Technologies

- JinkoSolar Holding Co., Ltd.

- Hanwha Q Cells Co., Ltd.

- JA Solar Holdings Co. Ltd.

- Trina solar

- Tata Power Solar System Ltd

- Abengoa

- Waaree Group

- General Electric Company

- BrightSource Energy, Inc.

- Urja Global Limited

- eSolar Inc

Recent Development

- In March 2024, NextEra Energy announced the completion of the largest solar-plus-storage project in the United States, the "Manatee Energy Storage Center" in Florida. This project integrates 409 MW of solar energy with a 900 MWh battery storage system, showcasing the growing trend of combining solar power with energy storage to enhance grid reliability and efficiency.

- In January 2024, TotalEnergies commenced operations of its "Al Kharsaah" solar project in Qatar. This project, with a capacity of 800 MW, is the first large-scale solar power plant in Qatar and is part of the country's effort to diversify its energy mix and reduce its carbon footprint. The project is expected to power about 55,000 homes and offset 1.4 million tons of CO2 annually.

- In April 2023, Iberdrola, a Spanish multinational electric utility, inaugurated its "Francisco Pizarro" solar plant in Spain, which is currently the largest solar farm in Europe. The plant has an installed capacity of 590 MW and is expected to supply clean energy to approximately 375,000 homes, reducing CO2 emissions by over 245,000 tons annually.

- In June 2023, First Solar announced the expansion of its manufacturing capacity with a new 3.3 GW factory in Ohio. This expansion is part of the company’s strategy to increase its U.S. manufacturing footprint and meet the growing demand for solar modules domestically. The new facility is expected to begin production in 2025 and will create approximately 500 new jobs.

Report Scope

Report Features Description Market Value (2023) USD 185.0 Billion Forecast Revenue (2033) USD 583.3 Billion CAGR (2024-2032) 12.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Application (Residential, Commercial, Industrial), By Technology (Photovoltaic Systems and Concentrated Solar Power Systems), By End Use (Electricity Generation, Lighting, Heating, Charging), By Solar Module (Monocrystalline, Polycrystalline, Cadmium Telluride, Amorphous Silicon Cells, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Canadian Solar Inc., SunPower Corporation, Yingli Green Energy Holding Company Limited, Enphase Energy, Inc., First Solar, Inc., SolarEdge Technologies, JinkoSolar Holding Co., Ltd., Hanwha Q Cells Co., Ltd., JA Solar Holdings Co. Ltd., Trina Solar, Tata Power Solar System Ltd, Abengoa, Waaree Group, General Electric Company, BrightSource Energy, Inc., Urja Global Limited, eSolar Inc Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Canadian Solar Inc.

- SunPower Corporation

- Yingli Green Energy Holding Company Limited

- Enphase Energy, Inc.

- First Solar, Inc.

- SolarEdge Technologies

- JinkoSolar Holding Co., Ltd.

- Hanwha Q Cells Co., Ltd.

- JA Solar Holdings Co. Ltd.

- Trina solar

- Tata Power Solar System Ltd

- Abengoa

- Waaree Group

- General Electric Company

- BrightSource Energy, Inc.

- Urja Global Limited

- eSolar Inc

Our Clients

View Our Licence Options