Acral Lentiginous Melanoma Market Report By Diagnostic Stage (Early-Stage ALM, Advanced-Stage ALM), By Treatment Modality (Surgery, Radiation Therapy, Chemotherapy, Immunotherapy (e.g., PD-1 Inhibitors, CTLA-4 Inhibitors), Targeted Therapy (e.g., BRAF Inhibitors, MEK Inhibitors), Combination Therapies), By End Users, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

45324

-

May 2024

-

285

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

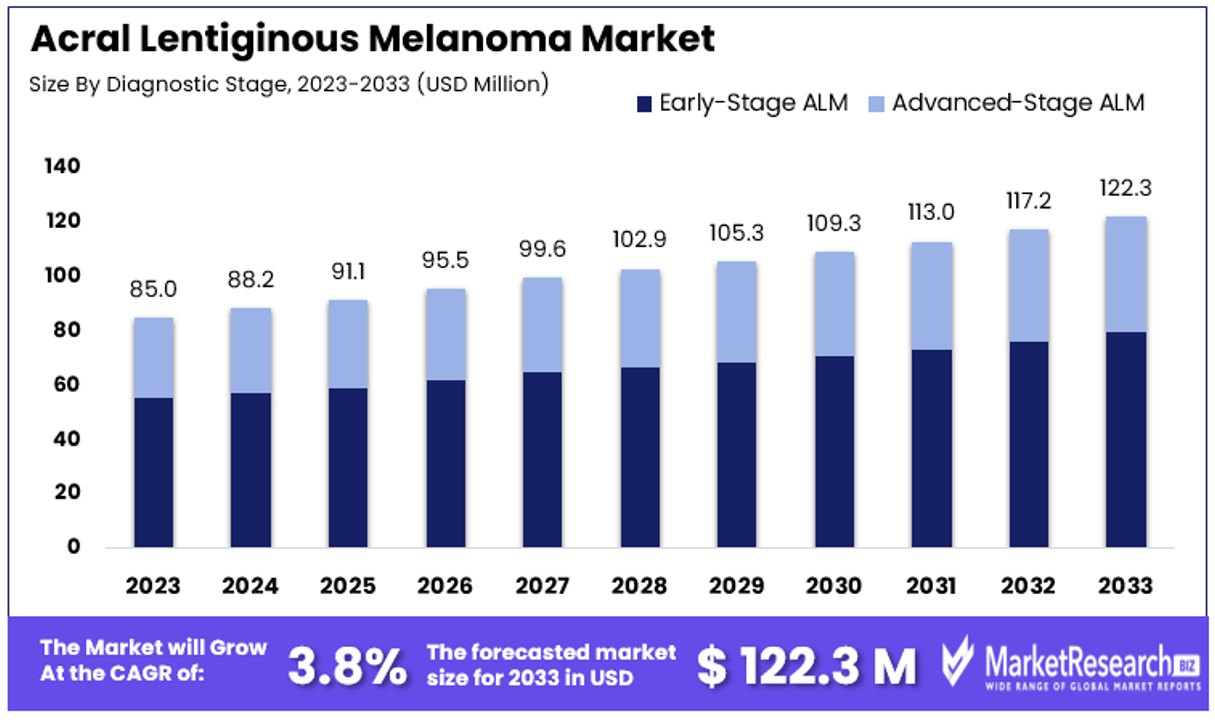

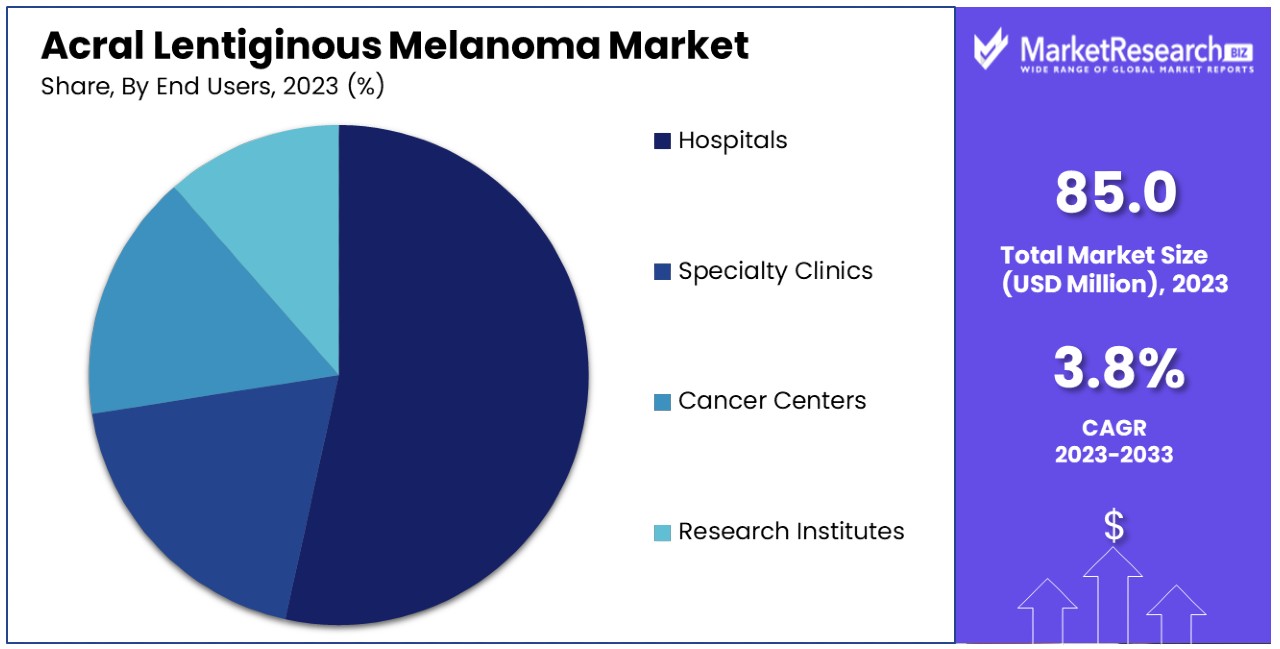

The Global Acral Lentiginous Melanoma Market size is expected to be worth around USD 122.3 Million by 2033, from USD 85 Million in 2023, growing at a CAGR of 3.80% during the forecast period from 2024 to 2033.

Acral Lentiginous Melanoma (ALM) Market refers to the specific segment within the oncology industry focused on a rare form of melanoma that predominantly affects the palms, soles, and under the nails. This market encompasses the development, production, and distribution of diagnostic tools, treatments, and potentially preventative strategies specifically for ALM.

The market's growth is driven by advances in medical technology, increasing awareness of ALM symptoms, and the rising incidence of melanoma globally. Key stakeholders, including biopharmaceutical firms, healthcare providers, and regulatory bodies, play significant roles in shaping market dynamics through innovation and strategic partnerships. This sector is of particular interest to executives and product managers aiming to address critical healthcare needs and tap into niche medical markets.

The Acral Lentiginous Melanoma (ALM) market is a specialized sector within the broader dermatological oncology field. In 2023, approximately 97,610 new cases of melanoma are expected to be diagnosed in the United States. This data highlights a growing concern, as melanoma remains the deadliest form of skin cancer and has shown a significant increase in diagnosis over the last three decades, particularly among young adults aged 25 to 39.

Although ALM is a rare subtype, with an age-adjusted incidence rate of about 1.8 to 2.0 per million person-years, its impact is noteworthy, especially given its higher prevalence among African American, Hispanic, and Asian populations.

Despite its rarity, the ALM market is crucial due to the subtype’s poorer prognosis and higher mortality rates compared to other forms of melanoma. These factors drive a persistent demand for advanced diagnostic tools, effective treatment options, and tailored healthcare strategies that address the unique challenges associated with ALM. The market is further influenced by increasing awareness and the need for specialized care, which propels research and development efforts.

The ALM market presents a dual opportunity: first, to enhance outcomes for a demographic that is disproportionately affected; and second, to innovate in areas of unmet medical need. Stakeholders, including biopharmaceutical companies, healthcare providers, and policy makers, are thus incentivized to invest in this niche yet significant market.

Strategic partnerships and investments in research could lead to breakthroughs in treatment methodologies and diagnostic technologies, potentially expanding the market and improving patient prognosis. This area remains ripe for development, with a focus on increasing survival rates and improving quality of life for affected individuals.

Key Takeaways

- Market Value: The Global Acral Lentiginous Melanoma Market is anticipated to reach a substantial value by 2033, growing from USD 85 million in 2023, with a CAGR of 3.80% during the forecast period from 2024 to 2033.

- Diagnostic Stage Analysis: Early-Stage ALM dominates with 65% share due to its association with higher survival rates, emphasizing the importance of early detection and screening initiatives.

- Treatment Modality Analysis: Immunotherapy leads with 50% share, offering superior efficacy in prolonging survival and enhancing the quality of life for melanoma patients.

- End Users Analysis: Hospitals dominate with 70% share, providing comprehensive care facilities and serving as primary treatment centers for ALM patients.

- APAC: Dominates with 55% market share, reflecting significant patient population and increasing awareness about melanoma diagnosis and treatment options.

- North America: Holds a substantial market share of approximately 25%, driven by advanced healthcare infrastructure, high healthcare spending, and active patient advocacy groups.

- Analyst Viewpoint: Emphasis on early detection and screening programs is crucial in improving ALM patient outcomes and reducing treatment costs, highlighting the importance of investing in diagnostic technologies and initiatives. Immunotherapy's dominance underscores its transformative impact on melanoma treatment, driving the need for further research and development in this therapeutic area.

Driving Factors

Increasing Incidence of Acral Lentiginous Melanoma Drives Market Growth

The growing incidence of Acral Lentiginous Melanoma (ALM) significantly influences the expansion of its market. ALM, a rare subtype of melanoma primarily affecting the palms, soles, and nail beds, is distinguished from other melanoma types by its lack of strong association with UV exposure. This characteristic makes it more prevalent among populations with darker skin tones, such as Asian and African American groups.

According to research in the Journal of the American Academy of Dermatology, ALM can represent up to 60% of melanoma cases in these populations. The global increase in population and aging demographics are projected to raise the incidence of ALM further, thus enhancing the demand for effective treatments. This uptick in cases necessitates advancements in medical research and healthcare provisioning, propelling the development of targeted therapies tailored to meet the unique needs of ALM patients.

Advancements in Targeted Therapies and Immunotherapies Enhance Market Dynamics

The introduction of targeted therapies and immunotherapies has been pivotal in transforming the treatment landscape for melanoma, including ALM. These therapies offer more precise treatment options that improve patient outcomes. For instance, the combination of encorafenib, a BRAF inhibitor, and binimetinib, a MEK inhibitor, has been approved by the FDA for treating BRAF-mutated melanoma, which includes some ALM cases.

This advancement reflects a broader trend in oncology that focuses on understanding the genetic and molecular underpinnings of cancers to develop more effective treatments. As ongoing research uncovers more about ALM’s specific pathways, the market is likely to see an influx of new, innovative treatments that can more accurately target the disease, thereby driving growth within the sector.

Increased Focus on Rare and Underserved Cancers Spurs Market Development

A heightened focus on rare and underserved cancers like ALM is reshaping priorities within the pharmaceutical industry and research communities. This shift is driven by several factors, including orphan drug incentives, which offer financial benefits for developing treatments for rare diseases, robust patient advocacy, and the potential for substantial returns on investment due to the high need for effective treatments in underserved markets.

These dynamics are encouraging more investments into research and development specifically for ALM. Initiatives like the Melanoma Research Alliance’s Acral Lentiginous Melanoma Working Group exemplify efforts to enhance research funding and patient support, thus fostering a conducive environment for market growth. As more resources are allocated to understanding and treating ALM, the market is likely to expand, leading to enhanced patient outcomes and increased availability of tailored treatment options.

Restraining Factors

Rarity of Acral Lentiginous Melanoma Restrains Market Growth

The rarity of Acral Lentiginous Melanoma (ALM) significantly limits its market growth. As a rare subtype, ALM accounts for only a minor fraction of all melanoma cases, which complicates the execution of large-scale clinical trials and affects the robustness of research findings.

For instance, a Phase 3 clinical trial by Amgen for taletrectinib in ALM patients had to be discontinued due to slower-than-expected patient enrollment. The limited number of patients not only challenges the accumulation of sufficient data but also affects the feasibility and cost-effectiveness of developing new therapies. Consequently, pharmaceutical companies may be less inclined to invest in research and development for treatments targeting ALM, considering the potential constraints on market size and profitability.

Lack of Comprehensive Understanding of ALM Biology Restrains Market Growth

The incomplete understanding of the biological mechanisms underlying Acral Lentiginous Melanoma poses another barrier to market growth. Despite advancements in melanoma research, significant gaps remain in the knowledge of ALM's genetic and molecular drivers. This lack of clarity hampers the development of targeted therapies and precise biomarkers necessary for effective patient selection and treatment monitoring.

The heterogeneity of ALM, with its unique mutational profiles and varied clinical presentations, further complicates therapeutic developments. For example, studies have identified distinct genetic mutations in ALM compared to other melanoma subtypes, necessitating specialized research tailored specifically to this group. This complexity not only delays the introduction of innovative treatments but also limits the overall expansion of the ALM market.

Diagnostic Stage Analysis

Early-Stage ALM dominates with 65% due to earlier detection and increased survival rates.

The diagnostic stage of Acral Lentiginous Melanoma (ALM) significantly influences treatment approaches and market dynamics. Early-Stage ALM, where the cancer is detected at a less advanced stage, currently dominates this segment. This dominance is largely attributed to the growing emphasis on early detection and screening within the healthcare community. Early detection is linked to significantly higher survival rates and less invasive treatments, which are more cost-effective and lead to better patient outcomes. As a result, there is a strong push for technologies and programs that can diagnose melanoma at its earliest stage.

Conversely, Advanced-Stage ALM represents a smaller portion of the market but is critical due to the complexity and urgency of treatment required. Patients diagnosed at a later stage often undergo more aggressive treatments, which can be less effective and more costly. This sub-segment drives demand for advanced therapeutics and innovative treatment modalities, pushing research and development efforts to focus on more effective late-stage interventions. The role of advanced-stage diagnosis in driving technological advancement and treatment efficacy remains crucial, despite its smaller market share.

Treatment Modality Analysis

Immunotherapy dominates with 50% due to its effectiveness in prolonging survival in melanoma patients.

In the treatment of Acral Lentiginous Melanoma, various modalities are employed, each addressing different needs based on the disease's progression and individual patient factors. Among these, Immunotherapy has emerged as the dominant sub-segment, particularly through agents like PD-1 and CTLA-4 inhibitors. These therapies have revolutionized treatment, offering prolonged survival rates and better quality of life by enabling the immune system to recognize and combat cancer cells more effectively. The success of immunotherapy has been supported by substantial clinical evidence demonstrating its superiority over traditional treatments in many cases.

Other important treatment modalities include Surgery, Radiation Therapy, Chemotherapy, Targeted Therapy, and Combination Therapies. Surgery remains a foundational treatment approach, especially for early-stage ALM, effectively removing tumors before they spread. Radiation therapy and chemotherapy are typically reserved for more advanced cases or when surgery is not viable.

Meanwhile, Targeted Therapy, particularly treatments involving BRAF and MEK inhibitors, has become critical for patients with specific genetic mutations. The development and utilization of Combination Therapies, which involve using two or more treatment methods together, have also shown promise in improving outcomes by attacking the cancer on multiple fronts. Each of these treatments plays a vital role in the comprehensive care of ALM patients, supporting the overall market growth through diversified therapeutic offerings.

End Users Analysis

Hospitals dominate with 70% due to their comprehensive care facilities and high patient influx.

The end-user segment of the Acral Lentiginous Melanoma market significantly impacts its distribution and accessibility. Hospitals, as the primary care setting for most ALM patients, dominate this market segment. This dominance is attributed to their ability to provide comprehensive care, including diagnosis, treatment, and follow-up in a single location. Hospitals are typically equipped with the latest technologies and staffed by specialist teams that can manage the complexities of melanoma treatment, making them a preferred choice for many patients.

Specialty Clinics, Cancer Centers, and Research Institutes also play critical roles in the ALM market. Specialty Clinics offer focused care, particularly for patients needing personalized treatment plans, while Cancer Centers are pivotal in providing specialized treatments and access to clinical trials that might not be available elsewhere. Research Institutes contribute by pushing the boundaries of what is currently known about ALM through ongoing studies and trials, which can lead to new treatment modalities and strategies. Although Hospitals are the dominant segment due to their extensive resources and patient volume, the other end users collectively enhance the market's dynamic by offering specialized services that address the diverse needs of the ALM patient population.

Key Market Segments

By Diagnostic Stage

- Early-Stage ALM

- Advanced-Stage ALM

By Treatment Modality

- Surgery

- Radiation Therapy

- Chemotherapy

- Immunotherapy (e.g., PD-1 Inhibitors, CTLA-4 Inhibitors)

- Targeted Therapy (e.g., BRAF Inhibitors, MEK Inhibitors)

- Combination Therapies

By End Users

- Hospitals

- Specialty Clinics

- Cancer Centers

- Research Institutes

Growth Opportunities

Development of Biomarker-Driven Targeted Therapies Offers Growth Opportunity

The evolution of genetic and molecular understanding in Acral Lentiginous Melanoma (ALM) presents significant opportunities for the development of biomarker-driven targeted therapies. By pinpointing specific genetic mutations or molecular pathways that are distinctive to ALM, such therapies can offer more precise and individualized treatment solutions. This method builds on the proven success of targeted therapies in other melanoma subtypes and aims to address the unique biological characteristics of ALM.

For instance, research from the University of California, San Francisco highlighted recurrent mutations in the BRAF and NF1 genes, which are promising targets for precision medicine strategies in ALM. The increasing precision in targeting these molecular anomalies represents a substantial market opportunity, as it can lead to the development of more effective treatments that can significantly improve patient outcomes.

Combination Therapy Approaches Offer Growth Opportunity

The inherent complexity and heterogeneity of Acral Lentiginous Melanoma provide fertile ground for exploring combination therapy approaches. These strategies, which involve the concurrent use of multiple therapeutic agents like targeted therapies and immunotherapies, are designed to target various molecular pathways simultaneously or to achieve synergistic effects.

This approach could potentially circumvent resistance mechanisms often seen with single-agent treatments and enhance overall treatment efficacy. For example, current clinical trials are assessing the efficacy of combining BRAF/MEK inhibitors with immune checkpoint inhibitors in patients harboring BRAF mutations in ALM. These combination regimens aim to boost the effectiveness and durability of the treatment responses, indicating a robust growth opportunity in this segment of the ALM market.

Trending Factors

Increasing Focus on Rare and Neglected Diseases Are Trending Factors

The pharmaceutical industry and research community are increasingly concentrating on rare and neglected diseases, such as Acral Lentiginous Melanoma (ALM). This trend is propelled by a combination of patient advocacy, the allure of high returns on investment through orphan drug incentives, and the pursuit of addressing unmet medical needs.

As awareness grows and funding increases, there is a marked expansion in research and development efforts specifically targeting ALM. This shift not only fuels market growth but also stimulates innovation, providing hope for better treatment solutions for this underserved patient population. This strategic focus is expected to continue, driven by the potential for significant advancements in therapeutic options and patient care for rare cancers like ALM.

Advancements in Precision Medicine and Genomic Profiling Are Trending Factors

Precision medicine and genomic profiling are rapidly evolving fields that are shaping the future of cancer treatment, particularly for subtypes like Acral Lentiginous Melanoma. Significant strides in identifying genetic mutations and molecular biomarkers specific to ALM are enhancing the development of targeted therapies.

This trend is crucial for ALM, which exhibits unique genetic and molecular characteristics compared to more common melanoma types. By utilizing genomic data to tailor treatments, researchers and pharmaceutical companies can provide more effective, personalized therapy options. This approach not only improves patient outcomes but also represents a significant growth area within the ALM market, reflecting broader trends towards individualized cancer treatment strategies.

Regional Analysis

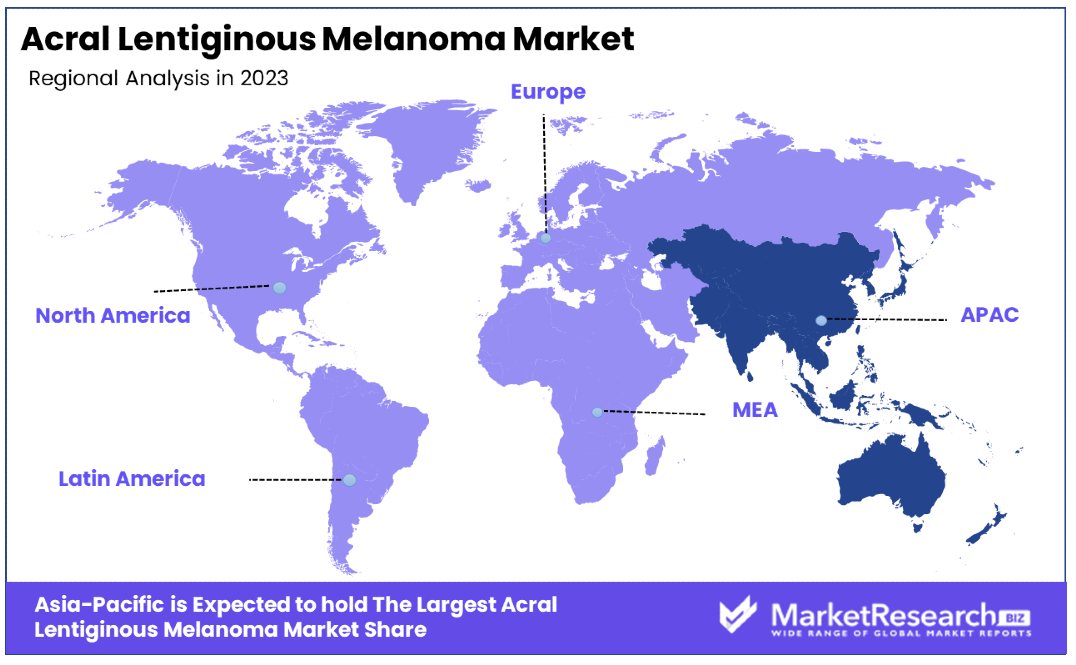

APAC Dominates with 55% Market Share

Asia Pacific (APAC) holds the majority market share in the Acral Lentiginous Melanoma (ALM) market, primarily due to its large and diverse population, which increases the prevalence of varied melanoma cases, including rare subtypes like ALM. Additionally, rising healthcare expenditures and improvements in healthcare infrastructure contribute to enhanced diagnostic and treatment capabilities across the region. Significant investments in medical research and the presence of high-growth economies like China and India also drive the adoption of advanced oncology treatments.

The dominance of APAC in the ALM market is further supported by the region's focus on innovative healthcare solutions and growing awareness about skin cancer. The region benefits from government initiatives promoting early detection and treatment of cancers, coupled with an increasing number of specialized cancer care centers. These factors create a robust environment for the growth of the ALM market, encouraging continuous investment from global and regional pharmaceutical companies.

APAC’s influence on the global ALM market is expected to grow even further. With ongoing advancements in healthcare and a growing middle class that can access and afford more comprehensive medical care, the demand for specialized and advanced melanoma treatments in the region will likely increase. This could lead to more targeted research initiatives and potentially more breakthroughs in ALM treatments, reinforcing APAC’s leading position in the market.

Regional Market Share:

- North America: North America holds a significant market share, accounting for approximately 25%. The region’s advanced healthcare infrastructure, high healthcare spending, and active patient advocacy groups drive its substantial role in the global ALM market.

- Europe: Europe commands around 15% of the market share, supported by its strong healthcare systems, widespread awareness of melanoma, and substantial research funding.

- Middle East & Africa: This region accounts for about 3% of the market. Despite lower market share, there is potential for growth driven by improving healthcare infrastructure and increasing awareness.

- Latin America: Holding 2% of the market, Latin America faces challenges due to varying levels of healthcare access and awareness but shows promise with gradual healthcare improvements and increased government focus on cancer prevention.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Acral Lentiginous Melanoma Market, Novartis AG, Bristol-Myers Squibb Company, and Amgen Inc. have emerged as influential leaders due to their advanced therapeutic offerings and significant investment in oncology research. These companies focus on developing targeted therapies that improve survival rates and quality of life for patients with this aggressive form of melanoma. Their strategic positioning is strengthened by robust global networks and extensive market penetration, which allow them to quickly adapt and distribute new treatments.

AbbVie Inc. and Eli Lilly and Company also play critical roles by incorporating innovative biotechnologies to develop drugs that are more effective and have fewer side effects. Their efforts are complemented by companies like Regeneron Pharmaceuticals Inc. and GlaxoSmithKline PLC, which are known for their pioneering work in immunotherapies, potentially transforming the standard care for acral lentiginous melanoma.

Furthermore, Bayer AG and Prometheus Laboratories stand out for their diagnostic and prognostic solutions that support early detection and personalized treatment approaches. The combined efforts of these companies not only push the boundaries of existing treatments but also ensure a comprehensive approach to managing acral lentiginous melanoma, thus enhancing patient outcomes and driving growth in this specialized market sector.

Market Key Players

- Novartis AG

- AbbVie Inc.

- Prometheus Laboratories

- Bristol-Myers Squibb Company

- Bayer AG

- Regeneron Pharmaceuticals Inc.

- Amgen Inc.

- GlaxoSmithKline PLC

- Eli Lilly and Company

Recent Developments

- On March 2024, the U.S. Food and Drug Administration approved Amtagvi (lifileucel), the first cellular therapy for adult patients with unresectable or metastatic melanoma. This approval signifies a significant advancement in treating this aggressive form of skin cancer.

- On March 2024, Allegheny Health Network (AHN) launched a state-of-the-art Melanoma and Skin Cancer Center, focusing on cutting-edge technology like the VECTRA WB360 imaging system to enhance early lesion detection and improve patient outcomes.

Report Scope

Report Features Description Market Value (2023) USD 85 Million Forecast Revenue (2033) USD 122.3 Million CAGR (2024-2033) 3.80% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Diagnostic Stage (Early-Stage ALM, Advanced-Stage ALM), By Treatment Modality (Surgery, Radiation Therapy, Chemotherapy, Immunotherapy (e.g., PD-1 Inhibitors, CTLA-4 Inhibitors), Targeted Therapy (e.g., BRAF Inhibitors, MEK Inhibitors), Combination Therapies), By End Users (Hospitals, Specialty Clinics, Cancer Centers, Research Institutes) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Novartis AG, AbbVie Inc., Prometheus Laboratories, Bristol-Myers Squibb Company, Bayer AG, Regeneron Pharmaceuticals Inc., Amgen Inc., GlaxoSmithKline PLC, Eli Lilly and Company Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Novartis AG

- AbbVie Inc.

- Prometheus Laboratories

- Bristol-Myers Squibb Company

- Bayer AG

- Regeneron Pharmaceuticals Inc.

- Amgen Inc.

- GlaxoSmithKline PLC

- Eli Lilly and Company

Our Clients

View Our Licence Options