Ultracapacitors Market Report By Type (Electrochemical Double Layer Capacitors, Pseudocapacitors, Hybrid Capacitors), By Application (Automotive, Transportation, Industrial, Consumer Electronics, Aerospace and Defense, Others), By End User (Original Equipment Manufacturers, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

47046

-

May 2024

-

321

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

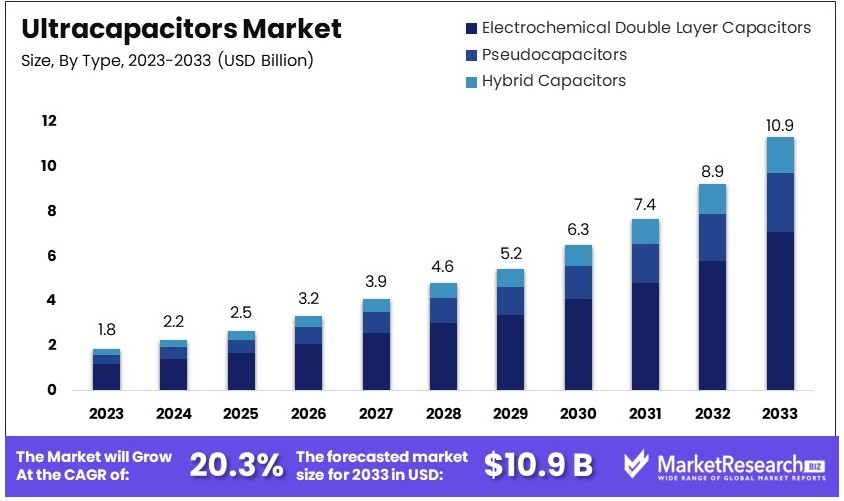

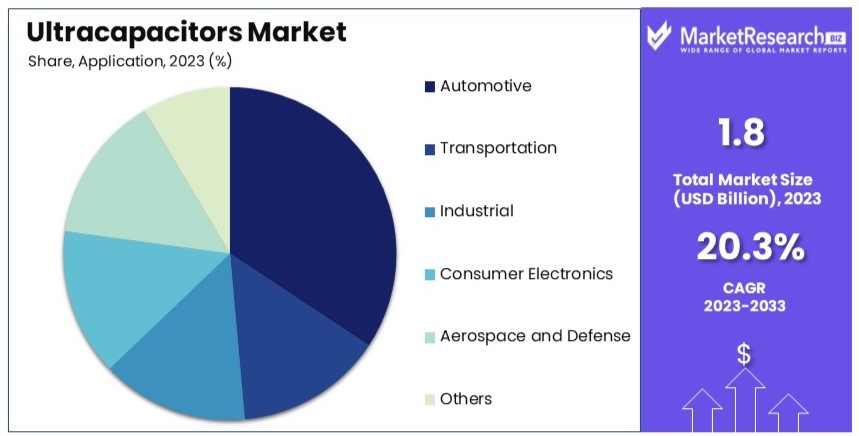

The Global Ultracapacitors Market size is expected to be worth around USD 10.9 Billion by 2033, from USD 1.8 Billion in 2023, growing at a CAGR of 20.3% during the forecast period from 2024 to 2033.

The Ultracapacitors Market focuses on energy storage devices that offer high power density and rapid charge-discharge cycles. Ultracapacitors are used in applications requiring quick bursts of energy, such as electric vehicles, renewable energy systems, and consumer electronics.

This market includes various types of ultracapacitors such as symmetric, asymmetric, and hybrid capacitors. The growing demand for energy-efficient solutions and the increasing adoption of electric vehicles drive the market's growth.

Key players in this market are investing in research to enhance the energy density and longevity of ultracapacitors. Technological advancements and the push for greener energy sources contribute to the market's expansion.

The Ultracapacitors Market is poised for significant growth due to the increasing demand for energy-efficient solutions. Ultracapacitors are energy storage devices known for their high power density and rapid charge-discharge capabilities. They are essential in applications requiring quick energy bursts, such as electric vehicles, renewable energy systems, and consumer electronics.

A key driver of this market is the rising emphasis on energy efficiency in homes and buildings. In 2022, energy-efficient homes sold for 2.7% more than unrated homes, with better-rated homes selling for 3% to 5% more. Real estate agents report that energy efficiency added $8,246 to a home's value, an increase of over $1,600 from the previous year. Given that homes and commercial buildings consume 40% of the energy used in the United States, the push for energy efficiency is substantial.

Ultracapacitors play a crucial role in enhancing the energy efficiency of these buildings by providing reliable and rapid energy storage solutions. This makes them invaluable for applications in smart grids and energy management systems.

Key players in the ultracapacitors market are investing in research to improve energy density and lifespan, making these devices more attractive for a broader range of applications. Technological advancements are expected to drive down costs and increase adoption rates, further boosting market growth.

In summary, the Ultracapacitors Market is set for robust expansion, driven by the growing demand for energy-efficient solutions. As energy efficiency becomes a more significant factor in property value and energy consumption continues to rise, the adoption of ultracapacitors is expected to increase, presenting substantial opportunities for market participants.

Key Takeaways

- Market Value: The Global Ultracapacitors Market size is expected to be worth USD 1.8 Billion in 2023, growing at a CAGR of 20.3%, expected to reach USD 10.9 Billion by 2033.

- Type Analysis: Electrochemical Double Layer Capacitors (EDLCs) dominate with 65% due to their versatility and efficiency in energy storage.

- Application Analysis: Automotive applications dominate with 40% due to increasing adoption in electric and hybrid vehicles for start-stop systems and regenerative braking.

- End User Analysis: Original Equipment Manufacturers (OEMs) dominate with 75% due to their direct integration of ultracapacitors in product designs.

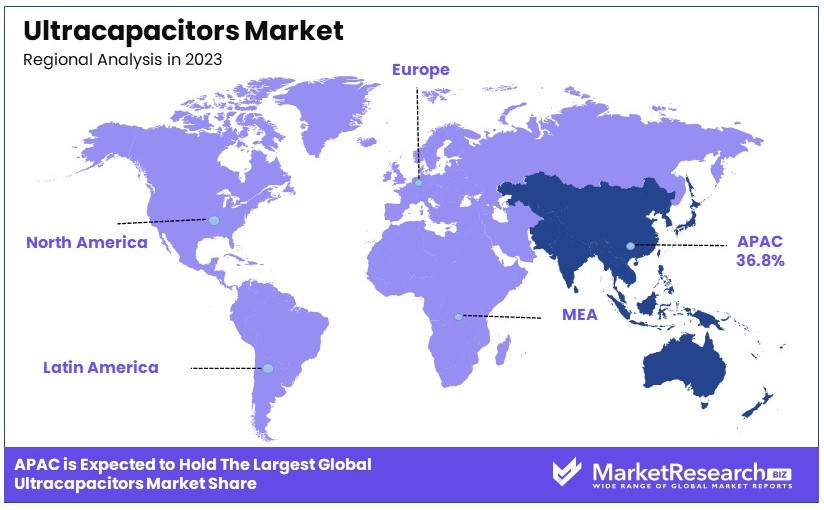

- Dominant Region: APAC with 36.8% due to rapid adoption of ultracapacitors in automotive and industrial applications.

- High Growth Region: North America holds approximately 27.5% due to advancements in renewable energy and automotive sectors.

- Analyst Viewpoint: The market is poised for significant growth with high competition; future demand will be driven by advancements in electric vehicles and energy storage technologies.

- Growth Opportunities: Key players can leverage advancements in ultracapacitor technology to cater to the growing demand in automotive and renewable energy sectors.

Driving Factors

Increasing Demand for Energy-Efficient and Sustainable Technologies Drives Market Growth

The shift towards sustainability is prominently driving the ultracapacitors market, particularly due to their ability to enhance energy efficiency. Ultracapacitors, with their rapid energy storage and release capabilities, are crucial in applications that require quick bursts of power. Their integration into regenerative braking systems is a standout example, significantly boosting fuel efficiency in hybrid and electric vehicles.

This technology not only captures and reuses energy that would otherwise be lost during braking but also reduces wear and tear on the braking system, leading to lower maintenance costs and longer vehicle life. Industry statistics suggest that the use of ultracapacitors can improve vehicle energy efficiency by up to 30%. This efficiency is critical as global energy policies increasingly favor sustainable technologies, pushing the automotive industry towards more eco-friendly solutions.

Growing Adoption in Transportation and Automotive Industries Drives Market Growth

Ultracapacitors are experiencing a surge in demand within the transportation and automotive industries, a trend driven by their ability to enhance energy management in vehicles. In the automotive sector, ultracapacitors are employed in start-stop systems and regenerative braking mechanisms, where they contribute significantly to fuel economy and reduced emissions. For instance, market leaders like Tesla and Toyota are integrating ultracapacitors into their electric and hybrid vehicles to capitalize on their quick charging and longevity benefits over traditional batteries.

This adoption is supported by data indicating that ultracapacitors can reduce carbon emissions by up to 20% in vehicles. As automotive manufacturers continue to face stringent environmental regulations, the appeal of ultracapacitors grows, fostering a complementary relationship between advanced vehicle technology and ultracapacitor manufacturers. This integration highlights a critical market synergy, as advancements in vehicle technology often drive developments in ultracapacitor production and vice versa, further stimulating market growth.

Increasing Use in Renewable Energy Systems Drives Market Growth

Ultracapacitors are becoming increasingly vital in the renewable energy sector, particularly for enhancing the reliability and efficiency of energy systems. They play a pivotal role in smoothing out power fluctuations and providing instant power during periods of low generation in wind and solar power installations. As the global commitment to renewable energy asset management escalates—with solar and wind capacity projected to grow by 60% over the next five years—the demand for ultracapacitors is expected to rise proportionately. This growth is due to their ability to stabilize power supplies and improve the operational efficiency of renewable energy systems.

Ultracapacitors complement renewable energy technologies by mitigating issues related to the intermittent nature of power generation sources like solar and wind. The integration of ultracapacitors helps prevent the loss of power during sudden drops in energy production, ensuring a steady and reliable power supply. This capability is essential for increasing the penetration of renewable technologies into the energy mix, further driving the growth of the ultracapacitors market.

Restraining Factors

Limited Energy Density Restrains Market Growth

The lower energy density of ultracapacitors compared to batteries is a significant barrier to their adoption in several key applications. Although ultracapacitors excel in delivering quick bursts of energy and boast high power density, their inability to store large amounts of energy for extended periods limits their usability in applications like electric vehicles that demand long-range energy storage.

For instance, while a typical lithium-ion battery can store about 250 watt-hours per kilogram, ultracapacitors only manage about 5 watt-hours per kilogram. This stark difference restricts ultracapacitors primarily to short-term applications, deterring their broader acceptance in markets that require sustained energy output, such as long-distance electric vehicles and uninterrupted power supplies, thereby inhibiting market growth.

Competition from Alternative Energy Storage Technologies Restrains Market Growth

Ultracapacitors face stiff competition from advancing alternative energy storage solutions, notably lithium-ion batteries and fuel cells, which continue to improve in efficiency and cost-effectiveness. This competitive pressure is compounded by the substantial investments and technological advancements in these alternatives, which increasingly meet a wider range of energy needs more effectively.

For example, the ongoing enhancement in lithium-ion technology has led to longer lifespans and lower costs, making them more attractive for a broader spectrum of applications than ultracapacitors. This competition not only challenges the market position of ultracapacitors but also slows their market growth as potential users opt for more versatile and economically viable alternatives.

Type Analysis

Electrochemical Double Layer Capacitors (EDLCs) dominate with 65% due to their versatility and efficiency in energy storage.

Electrochemical Double Layer Capacitors (EDLCs) represent the most significant sub-segment within the ultracapacitors market. Their dominance, accounting for approximately 65% of the market share, can be attributed to their superior charge storage and rapid charging capabilities. EDLCs are fundamentally crucial in applications requiring quick energy bursts due to their ability to charge and discharge swiftly and efficiently, making them ideal for use in automotive, industrial, and renewable energy sectors.

Pseudocapacitors, while not as prevalent as EDLCs, are notable for their higher energy density and are increasingly used in applications where energy storage and quick discharge are equally important. Hybrid capacitors combine the qualities of EDLCs and pseudocapacitors, offering a balance of energy density and power delivery. This sub-segment, though smaller, is growing as technologies advance, catering to niche markets that require both high energy and power density.

The remaining sub-segments, while not as dominant, play critical roles in the market. Pseudocapacitors are particularly effective in consumer electronics and medical devices due to their energy efficiency and compact size. Hybrid capacitors are finding increasing acceptance in applications that require both high power output and substantial energy storage, such as in regenerative braking systems in vehicles and renewable energy infrastructure solutions where both immediate response and energy recapture are critical. This diversification within the type segment underlines the evolving landscape of the ultracapacitors market, where each type serves distinct yet often complementary roles.

Application Analysis

Automotive applications dominate with 40% due to increasing adoption in electric and hybrid vehicles for start-stop systems and regenerative braking.

The automotive segment leads the application category of the ultracapacitors market, holding around 40% of its share, driven primarily by the increasing integration of ultracapacitors in electric and hybrid vehicles. These applications leverage the rapid charge and discharge capabilities of ultracapacitors, enhancing the efficiency of start-stop systems and regenerative braking. This not only improves fuel efficiency but also reduces emissions, aligning with global environmental targets and consumer demand for greener automotive technologies.

Transportation, encompassing trains, buses, and trams, utilizes ultracapacitors for similar reasons as the automotive sector, particularly for improving energy efficiency and operational reliability. In industrial applications, ultracapacitors find use in renewable energy storage and grid stabilization, critical as the world shifts towards more sustainable energy solutions. Consumer electronics and aerospace and defense are smaller segments where ultracapacitors contribute to energy efficiency and reliability, particularly in portable devices and critical mission systems.

The role of the remaining sub-segments, such as transportation and industrial, is increasingly significant. In transportation, ultracapacitors are used to improve the efficiency and lifespan of public transport vehicles. In the industrial sector, they are crucial for managing power fluctuations and providing emergency power, essential for maintaining stability and efficiency in power grids and renewable energy systems. Each of these applications contributes uniquely to the growth of the ultracapacitors market by expanding its utility across different sectors.

End User Analysis

Original Equipment Manufacturers (OEMs) dominate with 75% due to their direct integration of ultracapacitors in product designs.

In the end-user category, Original Equipment Manufacturers (OEMs) hold the largest market share, approximately 75%. This dominance is due to the direct incorporation of ultracapacitors in the design and manufacture of various products, particularly in the automotive and industrial sectors. OEMs integrate ultracapacitors to enhance the performance and efficiency of their products, thereby directly influencing the ultracapacitors market through product innovation and improved specifications.

The aftermarket segment, though smaller, is significant, especially in industries where upgrades to existing systems are common. In automotive applications, for example, ultracapacitors are added to older vehicles to improve energy efficiency and extend service life. This segment is poised for growth as the benefits of ultracapacitors become more widely recognized in enhancing the performance of existing systems and extending their operational life.

While OEMs continue to be the primary drivers of the ultracapacitors market, the aftermarket is an essential area of growth. This segment caters to the needs for retrofitting and upgrading existing systems, a cost-effective solution for many businesses and consumers looking to improve energy efficiency without the need for complete overhauls. As awareness and technological familiarity improve, the role of the aftermarket is expected to expand, providing substantial opportunities for the overall growth of the ultracapacitors market.

Key Market Segments

By Type

- Electrochemical Double Layer Capacitors

- Pseudocapacitors

- Hybrid Capacitors

By Application

- Automotive

- Transportation

- Industrial

- Consumer Electronics

- Aerospace and Defense

- Others

By End User

- Original Equipment Manufacturers

- Aftermarket

Growth Opportunities

Integration with Renewable Energy Systems Offers Growth Opportunity

As renewable energy sources like solar and wind continue to expand globally, ultracapacitors are increasingly becoming integral components of these energy systems. Their ability to quickly absorb and release energy makes them ideal for managing the inconsistencies and fluctuations inherent in renewable energy generation.

For instance, ultracapacitors help smooth out power outputs in wind turbines, ensuring a stable energy supply to the grid. This application is crucial for enhancing grid stability and efficiency, making ultracapacitors essential in the integration of renewable energy technologies. With the global renewable energy market expected to grow significantly, the demand for ultracapacitors in these applications is poised to increase, highlighting their critical role in the future energy landscape.

Adoption in Electric and Hybrid Vehicles Offers Growth Opportunity

The automotive industry's shift towards electric and hybrid vehicles is rapidly accelerating, spurred by environmental concerns and stringent emissions regulations. Ultracapacitors are well-suited for these vehicles, particularly in regenerative braking and start-stop systems, where their ability to rapidly charge and discharge can significantly enhance battery life and overall vehicle efficiency.

By improving energy recovery and reducing wear on batteries, ultracapacitors extend the range and lifespan of electric vehicles. As consumer demand for electric vehicles grows, so does the potential market for ultracapacitors, positioning them as a key technology in the evolution of automotive design and functionality.

Trending Factors

Emergence of Smart Grid and Energy Storage Systems Are Trending Factors

The development of smart grids and sophisticated energy storage solutions marks a significant trend influencing the ultracapacitors industry. Ultracapacitors contribute effectively to these systems by providing solutions for peak load management and frequency regulation.

Their high power density and quick response times are ideal for balancing load and ensuring stability within the grid, particularly during peak demand times or sudden drops in energy supply. As countries invest in smart grid technology to modernize their electrical systems, the demand for ultracapacitors is expected to rise, reflecting their growing importance in managing and optimizing grid performance.

Increasing Focus on Energy Harvesting and Self-Powered Devices Are Trending Factors

The proliferation of the Internet of Things (IoT) and the move towards sustainability are driving interest in energy harvesting technologies, where ultracapacitors play a crucial role. These devices capitalize on the ability of ultracapacitors to store and efficiently release energy harvested from environmental sources such as solar power, kinetic, and thermal energies.

This capability is particularly advantageous in IoT devices, which require small, efficient power sources for continuous operation. As the market for IoT and self-powered devices expands, so does the opportunity for ultracapacitors to serve as essential components in these technologies, promoting their adoption across various applications.

Regional Analysis

APAC Dominates with 36.8% Market Share

APAC's significant share of the ultracapacitors market, at 36.8%, is driven by rapid industrialization and the aggressive adoption of new technologies in countries like China, Japan, and South Korea. These nations are leaders in electronics manufacturing and automotive industries, both key users of ultracapacitors. Additionally, the region’s strong push towards renewable energy sources has catalyzed the adoption of ultracapacitors in energy storage and grid applications.

The regional dynamics of APAC are characterized by a robust manufacturing sector and a growing emphasis on sustainable technologies. This combination has created a fertile ground for ultracapacitors, which are essential for energy efficiency and advanced electrical solutions. The presence of major ultracapacitor manufacturers in the region also supports the market, along with government policies favoring technological innovation.

Other Regions:

North America: North America holds approximately 27.5% of the ultracapacitors market. The region's commitment to renewable energy and advanced automotive technologies, particularly in the United States and Canada, drives this significant market share. The presence of leading technology firms and substantial investments in R&D activities are also crucial factors supporting the market's growth here.

Europe: Europe accounts for around 21.6% of the global ultracapacitors market. The region's stringent environmental regulations and high adoption rate of electric vehicles contribute to its strong market presence. European countries are also pioneers in renewable energy projects, which utilize ultracapacitors for energy storage and stabilization.

Middle East & Africa: The Middle East & Africa region holds a smaller share of the ultracapacitors market, at about 7.3%. However, investments in modernizing infrastructure and increasing renewable energy installations are expected to drive growth in the market within this region.

Latin America: Latin America, with a market share of about 6.8%, has seen a slower uptake in ultracapacitor technology. Factors such as economic volatility and slower industrial growth have restrained market expansion. Nonetheless, potential growth could arise from increasing interest in renewable energy and industrial modernization in the region.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Ultracapacitors Market is shaped by several leading companies with substantial market influence. Maxwell Technologies (Tesla, Inc.) and Skeleton Technologies are at the forefront, known for their innovative technologies and extensive product ranges. Ioxus, Inc. and Nesscap Energy Inc. are key contributors, leveraging advanced designs and strategic partnerships to strengthen their market positions.

CAP-XX Limited and Nippon Chemi-Con Corporation are notable for their high-quality products and strong research and development capabilities. NEC Energy Solutions and Panasonic Corporation have a significant market presence due to their comprehensive portfolios and global distribution networks. Murata Manufacturing Co., Ltd. and Nichicon Corporation play crucial roles, focusing on technological advancements and customer-centric strategies.

AVX Corporation and LS Mtron Ltd. are recognized for their robust production capabilities and strategic market expansions. Vina Technology Corporation and Eaton Corporation enhance their market influence through continuous innovation and strategic alliances. Tesla, Inc. also impacts the market significantly with its cutting-edge technologies and broad market reach.

These companies collectively drive market growth by introducing new technologies, expanding their global presence, and maintaining competitive pricing. Their strategic positioning involves continuous product development and adapting to market demands. Overall, their influence ensures the Ultracapacitors Market remains dynamic and responsive to technological advancements and customer needs.

Market Key Players

- Maxwell Technologies (Tesla, Inc.)

- Skeleton Technologies

- Ioxus, Inc.

- Nesscap Energy Inc.

- CAP-XX Limited

- Nippon Chemi-Con Corporation

- NEC Energy Solutions

- Panasonic Corporation

- Murata Manufacturing Co., Ltd.

- Nichicon Corporation

- AVX Corporation

- LS Mtron Ltd.

- Vina Technology Corporation

- Eaton Corporation

- Tesla, Inc.

Recent Developments

- February 2024: Recent research by Prof. Jianqiang Bi's team has highlighted the potential of oxygen vacancies engineering to enhance the electrochemical performance of metal oxides for supercapacitors. Their study focused on synthesizing NiFe2O4−δ, characterized by a high density of oxygen vacancies, through a heat treatment process within an activated carbon bed. This process was built upon the hydrothermal synthesis of NiFe2O4.

- November 2023: Guided by machine learning, chemists at the Department of Energy's Oak Ridge National Laboratory (ORNL) have designed a groundbreaking carbonaceous supercapacitor material. This material stores four times more energy than the best commercial material, offering significant improvements for applications like regenerative brakes, power electronics, and auxiliary power supplies.

- July 2023: Researchers at MIT have developed an innovative supercapacitor made from a mixture of cement, carbon black, and water, significantly advancing renewable energy storage. The MIT team discovered that combining cement with carbon black in a specific manner creates a highly conductive network within the cement. This network has an extensive internal surface area, crucial for energy storage. When water is added to the mix, it facilitates the formation of these conductive pathways.

Report Scope

Report Features Description Market Value (2023) USD 1.8 Billion Forecast Revenue (2033) USD 10.9 Billion CAGR (2024-2033) 20.3% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Electrochemical Double Layer Capacitors, Pseudocapacitors, Hybrid Capacitors), By Application (Automotive, Transportation, Industrial, Consumer Electronics, Aerospace and Defense, Others), By End User (Original Equipment Manufacturers, Aftermarket) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Maxwell Technologies (Tesla, Inc.), Skeleton Technologies, Ioxus, Inc., Nesscap Energy Inc., CAP-XX Limited, Nippon Chemi-Con Corporation, NEC Energy Solutions, Panasonic Corporation, Murata Manufacturing Co., Ltd., Nichicon Corporation, AVX Corporation, LS Mtron Ltd., Vina Technology Corporation, Eaton Corporation, Tesla, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Maxwell Technologies (Tesla, Inc.)

- Skeleton Technologies

- Ioxus, Inc.

- Nesscap Energy Inc.

- CAP-XX Limited

- Nippon Chemi-Con Corporation

- NEC Energy Solutions

- Panasonic Corporation

- Murata Manufacturing Co., Ltd.

- Nichicon Corporation

- AVX Corporation

- LS Mtron Ltd.

- Vina Technology Corporation

- Eaton Corporation

- Tesla, Inc.

Our Clients

View Our Licence Options