Synthetic Gypsum Market By Type (FGD Gypsum, Citrogypsum, Fluro Gypsum, Phosphogypsum, Others), By Application (Soil Amendment, Drywall, Cement, Glass Manufacturing, Plaster, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

45973

-

May 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

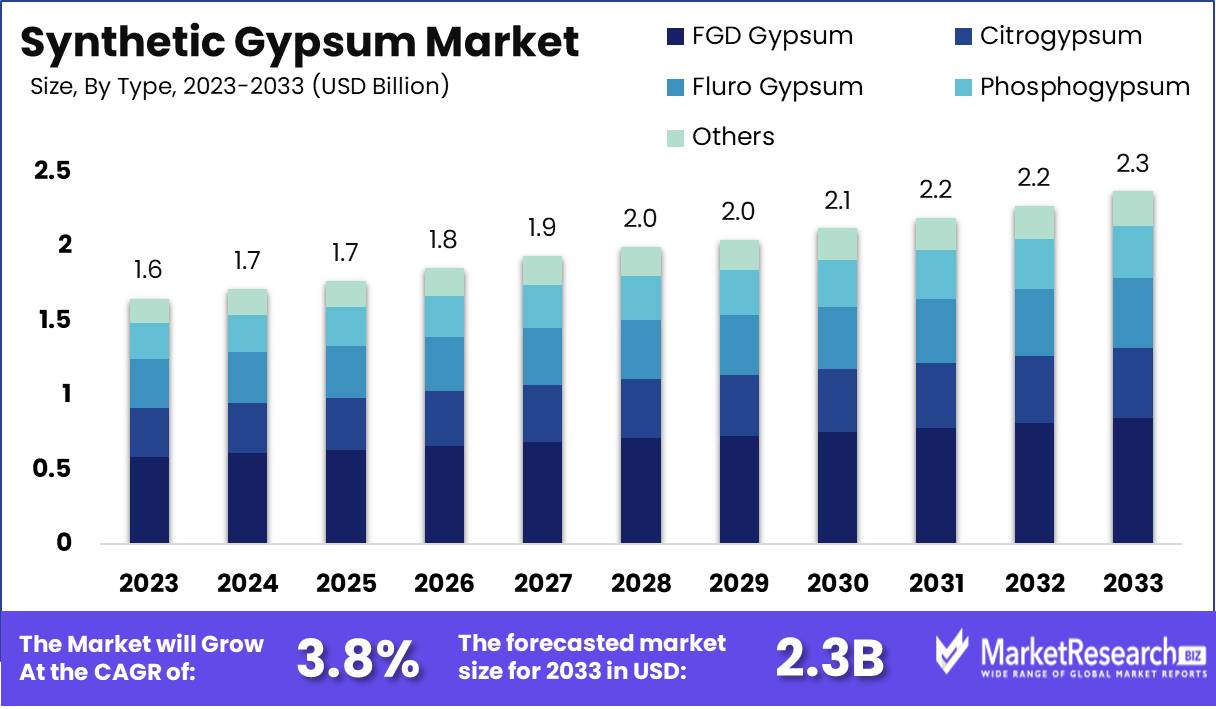

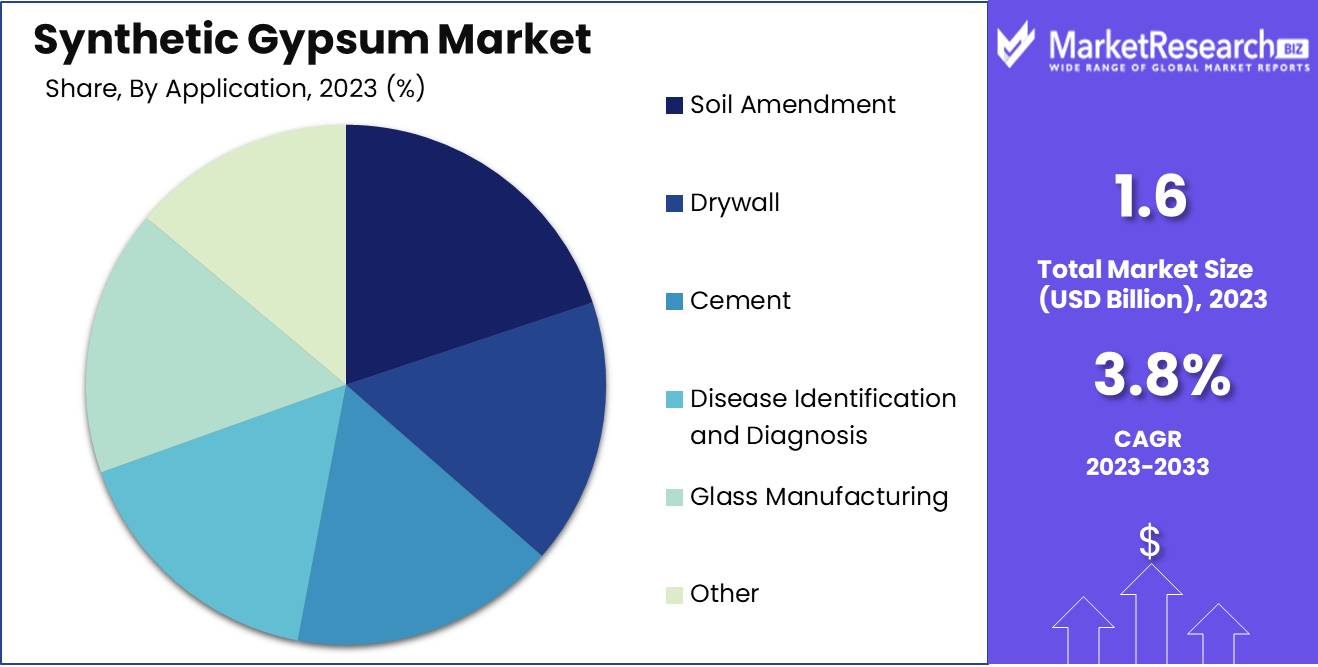

The Synthetic Gypsum Market size is estimated at USD 1.63 billion in 2023 and is expected to reach USD 2.3 billion by 2033, growing at a CAGR of 3.8% during the forecast period 2024-2033.

The Synthetic Gypsum Market encompasses the production, distribution, and sale of synthetic gypsum, a byproduct derived primarily from the desulfurization of flue gases in fossil-fueled power plants. This market has expanded due to its cost-effectiveness and environmental benefits, offering a sustainable alternative to natural gypsum. Synthetic gypsum is indistinguishable in performance from its natural counterpart and is extensively used in drywall, cement, and soil amendment applications. The growth of this market is propelled by the construction sector's increasing demand for eco-friendly materials, stringent environmental regulations, and the ongoing global shift towards sustainable development practices.

In the evolving landscape of sustainable construction materials, the market for synthetic gypsum emerges as a significant player, propelled by stringent environmental regulations and shifting industry preferences towards green building practices. Synthetic gypsum, a byproduct primarily derived from flue-gas desulfurization (FGD) processes in power plants, offers a compelling alternative to natural gypsum, aligning with global sustainability goals. This material finds extensive applications across various industries, most notably in construction for the manufacturing of products such as drywall and cement, and in agriculture as a soil amendment. Its diverse types, including FGD gypsum, fluorogypsum, and phosphogypsum, cater to a wide range of industrial needs.

The burgeoning adoption of synthetic gypsum is largely driven by its cost-effectiveness and the increasing implementation of FGD technologies, which not only aid in adhering to environmental standards but also provide an economic use for the byproducts of desulfurization. Furthermore, the market is buoyed by the growing endorsement of green building materials. As the construction industry continues to embrace sustainable practices, the demand for synthetic gypsum is expected to rise, offering substantial opportunities for market expansion.

The integration of sustainable materials is becoming a cornerstone in modern construction projects, underpinned by both regulatory support and evolving consumer preferences towards environmentally responsible products. This trend positions synthetic gypsum at the forefront of a shift towards more sustainable construction methodologies, ensuring its role as a pivotal material in the future of construction and agriculture.

Key Takeaways

- Market Growth: The Synthetic Gypsum Market size is estimated at USD 1.63 billion in 2023 and is expected to reach USD 2.3 billion by 2033, growing at a CAGR of 3.8% during the forecast period 2024-2033.

- By Type: FGD Gypsum dominates due to environmental benefits and regulatory support.

- By Application: Soil Amendment dominates the Synthetic Gypsum Market with sustainable agriculture impact.

- Regional Dominance: Asia Pacific leads the synthetic gypsum market with over 40% share.

- Growth Opportunity: The synthetic gypsum market will thrive by expanding globally and embracing sustainable production practices.

Driving factors

Increased Demand from the Construction Industry: A Catalyst for Synthetic Gypsum Market Expansion

The construction industry serves as a pivotal driver for the synthetic gypsum market, primarily due to the material's extensive use in products like drywall, cement, and plaster. Synthetic gypsum, derived from flue-gas desulfurization in power plants, offers a cost-effective and environmentally friendly alternative to natural gypsum. As global construction activity escalates, fueled by economic growth and infrastructure development, the demand for building materials correspondingly rises. This surge directly enhances the market for synthetic gypsum.

Urbanization: Intensifying Demand and Market Dynamics

Urbanization acts as a significant force multiplier in the synthetic gypsum market's growth. The influx of populations into urban areas, especially in Asia and Africa, has led to an unprecedented need for new housing and infrastructure. This urban expansion is not merely a matter of volume but also involves the modernization of building techniques and materials to meet higher standards of sustainability and efficiency. Synthetic gypsum's role in this transformation is critical due to its environmental benefits and compliance with green building standards. As cities expand and renew their infrastructure, the demand for synthetic gypsum is projected to rise, supporting the market's expansion.

Environmental Regulations: Steering Market Adoption and Innovation

Environmental regulations are profoundly shaping the synthetic gypsum market, guiding it toward sustainable practices. Governments worldwide are imposing stricter controls on industrial emissions, with a significant focus on sulfur dioxide (SO2) emissions from coal-fired power plants. This regulatory landscape compels power plants to adopt flue-gas desulfurization processes, which produce synthetic gypsum as a byproduct.

Consequently, this not only mitigates environmental impact but also provides an additional revenue stream for power producers through the sale of synthetic gypsum to the construction industry. In regions like the European Union and North America, stringent environmental laws have led to a robust market for synthetic gypsum, as industries seek to align with these standards while ensuring supply chain sustainability. The regulatory push thus fosters both the production and consumption of synthetic gypsum, catalyzing further market growth.

Restraining Factors

Fluctuating Costs of Raw Materials: Impeding Predictability and Financial Planning

The synthetic gypsum market, much like other construction material sectors, is significantly influenced by the volatility in raw material costs. Synthetic gypsum is primarily derived from flue-gas desulfurization (FGD) in power plants, a process dependent on the availability and price of limestone and coal. Fluctuations in the prices of these commodities can directly impact the production costs of synthetic gypsum. For instance, sudden increases in coal prices due to geopolitical tensions or supply chain disruptions can escalate production costs, making it challenging for manufacturers to maintain stable pricing. This unpredictability complicates financial planning and operational budgeting for producers.

Furthermore, the reliance on coal-fired power plants for synthetic gypsum production introduces additional variables. The global shift towards renewable energy sources and the resulting decline in coal use could constrain the availability of synthetic gypsum, creating a volatile market where prices and supply are unpredictable. This scenario discourages long-term investments and could potentially deter new entrants into the market, thereby stifling growth.

Infrastructure Challenges in Developing Countries: Limiting Market Expansion

Developing countries, which are pivotal markets for the expansion of the synthetic gypsum industry, often face significant infrastructure challenges that can restrain market growth. These include inadequate transportation networks, unreliable power supply, and underdeveloped industrial bases. Such infrastructural deficits make it difficult to establish and maintain efficient production facilities. For example, poor road and rail networks can impede the distribution of synthetic gypsum to construction sites, increasing logistics costs and delaying project timelines.

Moreover, the lack of advanced industrial technology in these regions can limit the capacity for high-quality synthetic gypsum production. This scenario not only affects local manufacturers but also international businesses looking to tap into these markets. The result is a constrained growth trajectory for the synthetic gypsum market in regions that could otherwise offer substantial expansion opportunities due to rapid urbanization and industrialization.

By Type Analysis

FGD Gypsum dominates due to environmental benefits and regulatory support.

In 2023, FGD Gypsum held a dominant market position in the "By Type" segment of the Synthetic Gypsum Market. This prominence can be attributed to several factors. First, FGD Gypsum, or flue-gas desulfurization gypsum, arises from pollution control processes in coal-fired power plants, offering an environmentally beneficial byproduct that supports sustainability goals. The increasing regulatory focus on reducing sulfur dioxide emissions globally has bolstered the supply of FGD Gypsum, making it readily available for various applications such as drywall, cement, and soil amendment.

Citrogypsum, another key segment, is derived from citric acid production. Its specialized applications in agriculture and industrial sectors, although niche, highlight its significance in regions with substantial citric acid manufacturing. Fluorgypsum, produced from the treatment of phosphate rock with sulfuric acid, primarily finds its use in the manufacture of plaster and plasterboard products. Its market share is driven by the construction sector's demand, particularly in rapidly developing economies.

Phosphogypsum, similar to fluoro gypsum, results from processing phosphate ore into fertilizers. Despite its large volume availability, environmental concerns regarding radionuclides limit its application, constraining its market potential. The 'Others' category encompasses lesser-known types of synthetic gypsum such as titanogypsum and borogypsum, each with specific uses that depend on regional industrial activities.

By Application Analysis

Soil Amendment dominates the Synthetic Gypsum Market with sustainable agriculture impact.

In 2023, Soil Amendment held a dominant market position in the "By Application" segment of the Synthetic Gypsum Market. Synthetic gypsum, primarily derived from flue-gas desulfurization in power plants, offers a sustainable alternative to natural gypsum. Its utilization in soil amendments has been particularly notable, addressing soil compaction and salinity issues which are critical in improving crop yield. This segment's growth is driven by increasing awareness of soil health and the need for sustainable agricultural practices.

The application of synthetic gypsum extends into other significant areas. In the production of drywall, synthetic gypsum acts as a core material due to its fire resistance and durability, making it a preferred choice in the construction industry. In cement manufacturing, it serves as a performance enhancer, helping in the control of cement setting times. The glass manufacturing sector uses synthetic gypsum as a fluxing agent, contributing to the melting process and enhancing product quality. Additionally, in plaster production, synthetic gypsum offers superior smoothness and aesthetic qualities. The diverse construction applications underscore its versatility and growing indispensability across multiple industries.

Key Market Segments

By Type

- FGD Gypsum

- Citrogypsum

- Fluro Gypsum

- Phosphogypsum

- Others

By Application

- Soil Amendment

- Drywall

- Cement

- Glass Manufacturing

- Plaster

- Others

Growth Opportunity

Geographic Expansion: Capturing Emerging Markets

The global synthetic gypsum market presents substantial growth opportunities through geographic expansion. Emerging economies in Asia, Africa, and South America are witnessing rapid industrialization and urban development, creating a burgeoning demand for building materials, including synthetic gypsum. This product, primarily derived from flue-gas desulfurization in power plants, offers a cost-effective and environmentally friendly alternative to natural gypsum. By entering these new markets, companies can tap into increasing local demands while also benefiting from less stringent competition compared to saturated markets in North America and Europe.

Organic and Sustainable Production: Meeting Evolving Market Demands

Another significant opportunity for the synthetic gypsum industry lies in focusing on organic and sustainable production methods. As global awareness and regulations surrounding environmental sustainability tighten, there is a marked shift towards products that are both eco-friendly and economically viable. Synthetic gypsum inherently supports sustainability through its recycling of industrial byproducts, reducing landfill waste, and the extraction of natural gypsum resources. Enhancing these processes to further reduce carbon footprints and embracing certifications for sustainable practices can not only improve operational efficiencies but also attract a growing segment of environmentally conscious consumers.

Latest Trends

Versatility and Cost-Effectiveness Drive Wider Adoption Across Industries

The synthetic gypsum market is poised to expand significantly, driven by its versatility and cost-effectiveness. Synthetic gypsum, primarily derived from desulfurization processes in coal-fired power plants, offers a compelling alternative to natural gypsum. Its applications are diverse, ranging from cement to drywall production, and even in agriculture as a soil structure amendment. This versatility not only opens up multiple market segments for synthetic gypsum but also presents a cost-effective solution for industries aiming to reduce raw material expenses.

Manufacturers benefit from the consistent quality and availability of synthetic gypsum, which, unlike natural sources, is less subject to geographical and environmental constraints. This reliability and cost efficiency are expected to boost its integration into various industrial processes, making synthetic gypsum a cornerstone material in construction and agriculture.

Sustainable Development Initiatives Bolster the Demand for Synthetic Gypsum

The focus on sustainable development is increasingly influencing corporate strategies, particularly in the construction and building materials sector. Synthetic gypsum’s role in sustainable practices is gaining prominence as industries seek to lower their environmental footprint. Utilizing synthetic gypsum helps reduce industrial waste and promotes recycling efforts, aligning with global environmental regulations and sustainability goals. This environmentally friendly profile enhances the attractiveness of synthetic gypsum, encouraging its adoption over less sustainable alternatives.

Furthermore, as governments worldwide implement stricter environmental policies, the demand for green building materials like synthetic gypsum is expected to rise, thereby fostering growth in the market. This trend underscores the material's significance in achieving eco-friendly development goals, reinforcing its market position in 2024 and beyond.

Regional Analysis

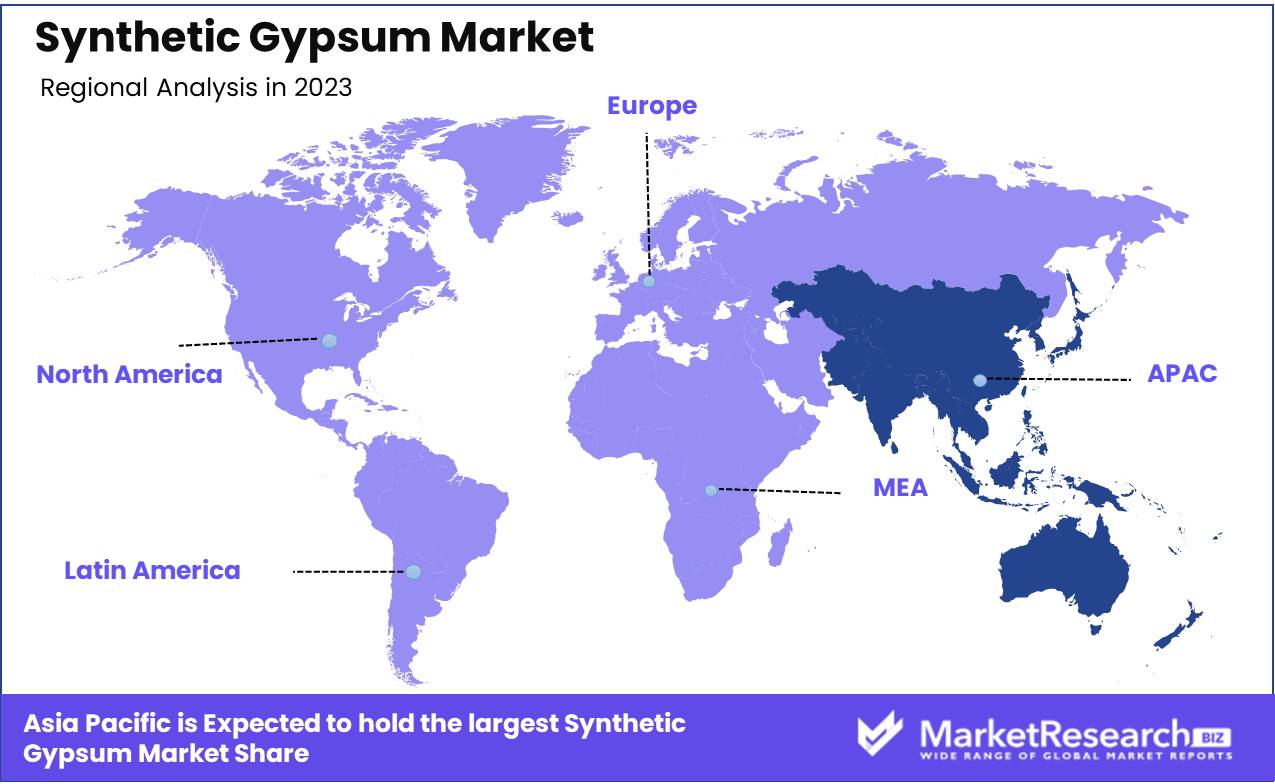

Asia Pacific leads the synthetic gypsum market with over 40% share.

The synthetic gypsum market exhibits distinct characteristics and growth dynamics across various global regions. In North America, the market is driven by stringent environmental regulations and the adoption of sustainable building materials. The United States leads in the production and utilization of synthetic gypsum, primarily sourced from flue gas desulfurization in power plants. The increased retrofitting and renovation activities in the construction sector further bolster the demand for synthetic gypsum products such as wallboard and plaster. Europe follows a similar trend, with additional impetus from the EU directives aimed at circular economy practices, which encourage the use of synthetic gypsum. Germany, France, and the UK significantly contribute to the regional market, focusing on eco-friendly construction materials.

Conversely, Asia Pacific is the dominating region, commanding a substantial share of the global synthetic gypsum market, primarily due to rapid urbanization and industrial growth in countries such as China and India. The region’s market share is estimated at over 40%. The construction boom in Asia Pacific, coupled with increasing infrastructural investments and the availability of synthetic gypsum as a by-product of industrial processes, particularly in power plants and the chemical industry, drives the demand. Meanwhile, regions like the Middle East & Africa, and Latin America are experiencing gradual growth, fueled by expanding construction sectors and evolving regulatory landscapes that favor sustainable materials. These regions, though smaller in market share, are anticipated to offer potential growth opportunities due to increasing industrial activities and urban development.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In the evolving landscape of the global synthetic gypsum market, key players such as LafargeHolcim, PABCO Building Products LLC, National Gypsum Properties LLC, Saint-Gobain, FEECO International, Knauf Gips KG, American Gypsum, Georgia-Pacific Gypsum LLC, Synthetic Materials LLC, and USG Corporation are pivotal in driving innovation and sustainability. These companies collectively illustrate a dynamic and competitive environment, each contributing to the industry's growth with strategic initiatives and technological advancements.

LafargeHolcim and Saint-Gobain stand out for their extensive geographic footprint and commitment to sustainability, leveraging their capabilities to produce synthetic gypsum through environmentally friendly industrial processes. This aligns with global regulatory trends favoring sustainable materials, presenting significant growth opportunities for these corporations.

Companies like FEECO International and Knauf Gips KG focus on optimizing manufacturing processes and enhancing material properties to meet the stringent requirements of modern construction standards, thereby ensuring product quality and consistency.

Meanwhile, U.S.-based entities such as American Gypsum and Georgia-Pacific Gypsum LLC are adept at navigating the local regulatory landscape, which is crucial for maintaining compliance and operational excellence in the North American market.

Market Key Players

- LafargeHolcim

- PABCO Building Products LLC

- National Gypsum Properties LLC

- Saint-Gobain

- FEECO International

- Knauf Gips KG

- American Gypsum,

- Georgia-Pacific Gypsum LLC

- Synthetic Materials LLC

- USG Corporation

Recent Development

- In May 2024, Georgia-Pacific Gypsum, a subsidiary of Koch Industries, announced a strategic partnership with a leading technology firm to enhance synthetic gypsum production processes. Through collaborative research and development efforts, the companies aim to optimize manufacturing efficiency and product quality. This initiative reflects Georgia-Pacific Gypsum's commitment to innovation and continuous improvement in delivering high-performance gypsum solutions to the market.

- In April 2024, National Gypsum Company, a prominent player in the gypsum industry, introduced a new line of synthetic gypsum-based products. This innovation underscores the company's dedication to leveraging alternative materials and reducing environmental impact. The launch of these products signifies National Gypsum Company's proactive approach to adapting to market trends and fulfilling customer needs for sustainable building solutions.

- In March 2024, USG Corporation, a leading manufacturer of building materials, announced a strategic expansion in synthetic gypsum production. The company unveiled plans to invest in advanced manufacturing facilities aimed at increasing synthetic gypsum output. This move aligns with USG Corporation's commitment to sustainable practices and meeting the growing demand for environmentally friendly construction materials.

Report Scope

Report Features Description Market Value (2023) USD 1.63 Billion Forecast Revenue (2033) USD 2.3 Billion CAGR (2024-2032) 3.8% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (FGD Gypsum, Citrogypsum, Fluro Gypsum, Phosphogypsum, Others), By Application (Soil Amendment, Drywall, Cement, Glass Manufacturing, Plaster, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape LafargeHolcim, PABCO Building Products LLC, National Gypsum Properties LLC, Saint-Gobain, FEECO International, Knauf Gips KG, American Gypsum, Georgia-Pacific Gypsum LLC, Synthetic Materials LLC, USG Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- LafargeHolcim

- PABCO Building Products LLC

- National Gypsum Properties LLC

- Saint-Gobain

- FEECO International

- Knauf Gips KG

- American Gypsum,

- Georgia-Pacific Gypsum LLC

- Synthetic Materials LLC

- USG Corporation

Our Clients

View Our Licence Options