Prostaglandin Market Report By Type (Human Prostaglandins, Veterinary Prostaglandins), By Application (Obstetrics and Gynecology, Cardiovascular Diseases, Erectile Dysfunction, Glaucoma Treatment, Gastrointestinal Diseases, Respiratory Diseases, Renal Diseases), By Route of Administration (Oral, Intravenous, Topical, Intramuscular, Subcutaneous, Intraocular), By End Users, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

45122

-

April 2024

-

285

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

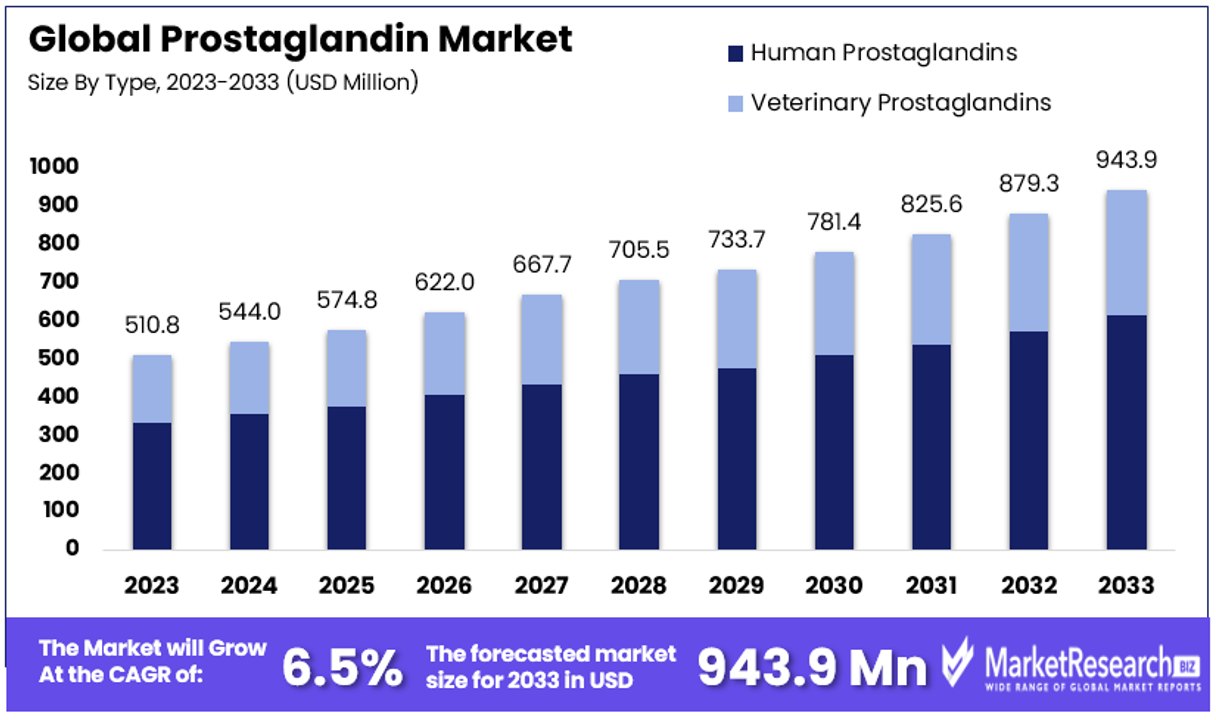

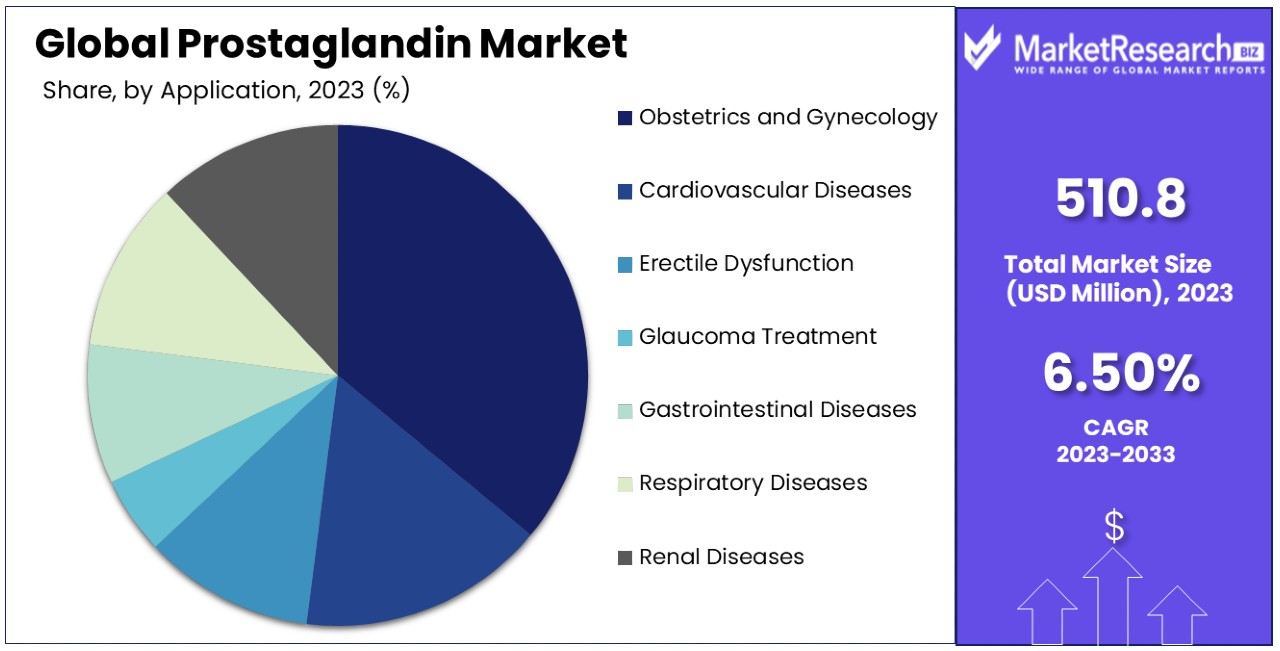

The Global Prostaglandin Market size is expected to be worth around USD 943.9 Million by 2033, from USD 510.8 Million in 2023, growing at a CAGR of 6.50% during the forecast period from 2024 to 2033.

The prostaglandin market refers to the industry focused on the production and distribution of prostaglandins, which are lipid compounds that perform hormone-like functions in various medical and therapeutic applications. This market serves critical roles in pharmaceuticals, particularly in treatments for glaucoma, induction of labor, and managing ulcers.

Key players in the market are involved in research and development, manufacturing, and commercialization of synthetic and natural prostaglandins. Growth in this market can be attributed to increasing demands in reproductive health and eye care, along with advancements in medical research that expand applications of prostaglandins. This sector is vital for companies looking to innovate in biologically active compounds.

The prostaglandin market is poised for significant growth, driven primarily by increasing incidences of glaucoma and cardiovascular diseases (CVD). In 2023, the escalation in global glaucoma cases, particularly among individuals aged 40 to 80, is noteworthy. The prevalence is projected to expand from 76 million in 2020 to 111.8 million by 2040.

This increase underscores the urgent need for effective treatment options, wherein prostaglandins play a crucial role due to their efficacy in managing this condition. Importantly, the awareness of glaucoma remains alarmingly low, with at least half of those affected unaware of their diagnosis, which can reach up to 90% in certain developing regions. This gap represents a substantial opportunity for market expansion through education and access initiatives.

Moreover, in the United States, CVD continues to be the predominant cause of mortality, with 928,741 deaths recorded in 2020 alone. Prostaglandins contribute valuable therapeutic benefits in managing CVD, further augmenting their demand in the pharmaceutical sector.

Manufacturers and stakeholders in the prostaglandin market are therefore encouraged to invest in research and development to innovate and improve prostaglandin formulations and delivery methods. Furthermore, expanding market outreach in underdiagnosed regions could significantly enhance global health outcomes while driving market growth.

Key Takeaways

- Market Value Projection: The Global Prostaglandin Market is forecasted to reach USD 943.9 Million by 2033, with a Compound Annual Growth Rate (CAGR) of 6.50% during the period from 2024 to 2033.

- Type Analysis: Human Prostaglandins lead the market due to their extensive use across various medical treatments, especially in addressing conditions like glaucoma and cardiovascular diseases.

- Application Analysis: Obstetrics and Gynecology is the dominant application segment, fueled by the critical role of prostaglandins in labor induction and related gynecological treatments.

- Route of Administration Analysis: Topical application is the primary route due to its convenience and effectiveness, particularly in ophthalmic and dermatological uses.

- End Users Analysis: Hospitals are the primary end users, given their capacity for professional oversight and comprehensive medical facilities required for administering prostaglandin treatments.

- Europe Dominance: Europe leads the market with a 36% share, attributed to advanced medical technologies and a strong focus on healthcare research.

- North American Influence: North America, especially the United States, holds a significant market share (approximately 30%) due to its advanced medical technologies and robust healthcare research focus.

- Key players in the Prostaglandin Market include pharmaceutical companies involved in the production and distribution of prostaglandin medications.

- Growth Opportunities: Continued research into novel applications and formulations of prostaglandins presents opportunities for market growth and innovation. Targeting emerging markets and increasing accessibility to prostaglandin treatments in developing regions can drive market expansion.

Driving Factors

Increasing Prevalence of Cardiovascular Diseases Drives Market Growth

The role of prostaglandins in managing cardiovascular diseases is a significant driver of their market growth. Prostacyclin analogs such as epoprostenol and treprostinil, essential in treating pulmonary arterial hypertension (PAH) and primary pulmonary hypertension (PPH), have seen increased demand as the incidence of these conditions rises.

As cardiovascular diseases remain a leading cause of death globally, with 928,741 deaths in the United States alone in 2020, the need for effective treatments propels the prostaglandin market forward. The synergistic effect of healthcare's focus on innovative, effective cardiovascular drugs therapies and the expanding patient population needing long-term disease management solutions underlines the continued growth in this segment.

Growth in the Ophthalmology Segment Drives Market Growth

Prostaglandin analogs are pivotal in the treatment of glaucoma, leveraging their capacity to reduce intraocular pressure effectively. With the global aging population, the prevalence of glaucoma is projected to increase from 76 million in 2020 to 111.8 million by 2040.

This demographic shift drives the demand for prostaglandin-based ophthalmic solutions, including widely used drugs like latanoprost, bimatoprost, and travoprost. The intersection of an aging population, the rising incidence of glaucoma, and the critical need for effective treatment options positions prostaglandins as essential components in managing eye health, thereby fueling market expansion.

Expanding Applications in Reproductive Health Drives Market Growth

In the domain of reproductive health, prostaglandins are integral to inducing labor and managing postpartum hemorrhage, pivotal areas as focus on maternal and child health intensifies globally. The adoption of prostaglandin-based medications like misoprostol and dinoprostone is on the rise, attributed to their efficacy and cost-efficiency compared to more invasive treatments.

This trend reflects broader healthcare strategies prioritizing accessible and effective solutions in maternal health, pushing the prostaglandin market's growth as these applications broaden and healthcare systems invest in safe, scalable options for women's health services.

Rising Demand for Pain Management Solutions Drives Market Growth

Prostaglandins such as diclofenac and ibuprofen, known for their anti-inflammatory and analgesic properties, are increasingly utilized in pain management. With chronic pain conditions becoming more prevalent and the ongoing search for effective pain relief solutions, the demand for prostaglandin-based medications is expected to escalate.

This growth is further supported by the broader pharmaceutical industry's focus on developing more efficient and patient-friendly pain management drugs, reflecting a market response to a growing need among the global population for long-term, sustainable pain management strategies.

Restraining Factors

Cost and Accessibility Challenges Restrain Market Growth

The economic and logistical barriers associated with prostaglandin-based medications significantly restrain their market growth. While some prostaglandin formulations are cost-effective, others, particularly advanced delivery systems, are prohibitively expensive for patients in low-income regions.

This discrepancy leads to uneven access across different socioeconomic groups and countries, especially those with underdeveloped healthcare infrastructures. High costs deter widespread adoption and limit market penetration, as not all potential users can afford these treatments. This factor is a critical consideration for pharmaceutical companies aiming to expand their global footprint in the prostaglandin market but face substantial hurdles in making their products accessible and affordable for all.

Competition from Alternative Therapies Restrains Market Growth

Prostaglandin-based medications, while effective, often contend with significant competition from alternative therapies, particularly in areas like glaucoma treatment. Other medication classes, such as beta-blockers and alpha-agonists, offer competitive efficacy and sometimes more favorable side effect profiles or pricing structures.

This competition can fragment the market and limit the growth potential of prostaglandin analogs. As newer drug classes emerge and existing alternatives continue to be optimized for better results and patient compliance, prostaglandins may see their market share squeezed, particularly in well-resourced healthcare settings where multiple therapeutic options are available and commonly prescribed.

Type Analysis

Human Prostaglandins dominate with a significant market share due to their extensive use in various medical treatments.

Human Prostaglandins represent the dominant sub-segment within the Prostaglandin Market. Their widespread application in treating a range of conditions from glaucoma and cardiovascular diseases to labor induction in obstetrics significantly contributes to their leading position. The efficacy and essential role of human prostaglandins in therapeutic protocols ensure their continued dominance. This segment's growth is driven by increasing clinical research that aims to expand the potential uses of prostaglandins, enhancing their effectiveness and safety profile.

In contrast, Veterinary Prostaglandins, while smaller in market share, serve an important role in animal health, particularly in the management of reproductive health and certain diseases in livestock and pets. This segment benefits from research in veterinary medicine that seeks to improve reproductive efficiency and animal welfare, thus supporting market growth. However, the human prostaglandins segment continues to overshadow veterinary applications due to the broader scope of health conditions addressed and the larger market demand in human healthcare settings.

Application Analysis

Obstetrics and Gynecology dominates with a major percentage due to the critical role of prostaglandins in labor induction and related gynecological treatments.

The application of prostaglandins in Obstetrics and Gynecology is pivotal, especially in labor induction and the management of postpartum hemorrhage, making it the dominant sub-segment. The demand in this segment is driven by the need for safe and effective labor-inducing agents across global healthcare systems. As birth rates and the focus on safe childbirth practices increase, particularly in developing regions, the usage of prostaglandins in obstetrics is expected to grow significantly.

Other applications such as Cardiovascular Diseases, Erectile Dysfunction, Glaucoma Treatment, Gastrointestinal Diseases, Respiratory Diseases, and Renal Diseases also contribute to the market but to a lesser extent. Each of these areas utilizes prostaglandins for their unique therapeutic properties, such as vasodilation and inflammation control.

For instance, in Glaucoma Treatment, prostaglandins help reduce intraocular pressure, an essential treatment parameter. Similarly, their anti-inflammatory properties are crucial in managing Cardiovascular and Gastrointestinal Diseases. These segments are expected to see gradual growth as advancements in medical research discover new uses and delivery methods for prostaglandins.

Route of Administration Analysis

Topical application dominates due to its convenience and effectiveness in delivering prostaglandins for ophthalmic and dermatological uses.

The dominance of Topical prostaglandins is primarily due to their ease of application and effectiveness, particularly in treating conditions like glaucoma, where prostaglandin analogs reduce intraocular pressure by increasing aqueous humor outflow. The convenience of topical administration, coupled with lower systemic absorption leading to fewer side effects, makes it highly favorable in both clinical settings and home care.

Other routes of administration such as Oral, Intravenous, Intramuscular, Subcutaneous, and Intraocular play significant roles but are less predominant than topical applications. Each route has specific advantages depending on the condition being treated. For example, intravenous and intramuscular routes are crucial in acute hospital settings for immediate effect, especially in Obstetrics and Gynecology for inducing labor or managing severe postpartum hemorrhage. The choice of administration route often depends on the required speed of action, the targeted tissue, and patient compliance factors.

End Users Analysis

Hospitals dominate as they are the primary healthcare settings for administering prostaglandins due to the need for professional oversight.

Hospitals are the leading end-user segment in the Prostaglandin Market, given their comprehensive medical facilities and the need for specialized healthcare personnel to administer and monitor treatments involving prostaglandins. The complexity of conditions treated with prostaglandins, such as in obstetric care and acute cardiovascular management, necessitates an environment where patient response can be closely monitored.

Specialty Clinics, Ambulatory Surgical Centers, and Pharmacies also constitute important end-user segments but have a smaller share compared to hospitals. Specialty clinics offer targeted treatments, particularly for chronic conditions like glaucoma, where ongoing outpatient care is essential. Ambulatory Surgical Centers provide a setting for procedures that can be completed on an outpatient basis, often involving less complex cases of prostaglandin use. Pharmacies support the distribution and access to prostaglandin medications, particularly for conditions that can be managed with self-administered treatments such as topical prostaglandins for eye conditions.

Key Market Segments

By Type

- Human Prostaglandins

- Veterinary Prostaglandins

By Application

- Obstetrics and Gynecology

- Cardiovascular Diseases

- Erectile Dysfunction

- Glaucoma Treatment

- Gastrointestinal Diseases

- Respiratory Diseases

- Renal Diseases

By Route of Administration

- Oral

- Intravenous

- Topical

- Intramuscular

- Subcutaneous

- Intraocular

By End Users

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Pharmacies

Growth Opportunities

Development of Novel Drug Delivery Systems Offers Growth Opportunity

The innovation in drug delivery systems represents a substantial growth opportunity within the Prostaglandin Market. By integrating advanced technologies such as nanoparticles, transdermal patches, and implantable devices, pharmaceutical companies can significantly enhance the efficacy and user experience of prostaglandin-based medications.

For instance, nanoparticle-based formulations are being explored for their ability to provide sustained release of drugs, which is particularly advantageous in the treatment of chronic conditions like glaucoma. This approach could minimize the frequency of dosing, thereby improving patient adherence and overall treatment outcomes. Improved bioavailability and reduced side effects further support patient compliance and can expand the usage of prostaglandins across different medical fields, potentially opening up new sub-markets within the broader pharmaceutical landscape.

Expansion into Emerging Markets Offers Growth Opportunity

Emerging markets present a significant growth avenue for the Prostaglandin Market due to the expansion of healthcare infrastructure and increasing accessibility to medical services. These regions host large populations that have historically been underserved in terms of healthcare, particularly for cost-effective treatments. The prostaglandin segment can capitalize on this by forming alliances with local distributors, setting up production within these markets to reduce costs, and implementing competitive pricing strategies.

Such strategic moves not only enable market penetration but also help in building brand loyalty and awareness in new geographic regions. The increasing demand for healthcare solutions in these areas, coupled with improvements in local healthcare systems, creates a ripe environment for growth, allowing prostaglandin products to fill crucial treatment gaps and drive substantial revenue increases.

Trending Factors

Focus on Personalized Medicine and Precision Dosing Are Trending Factors

The shift towards personalized medicine and precision dosing in the prostaglandin market is a key trending factor. This trend emerges from the understanding that treatment outcomes can vary widely among individuals due to differences in genetic profiles, environmental factors, and lifestyles. In response, the prostaglandin market is moving towards developing dosing strategies and formulations that are tailored to individual needs.

This approach aims to optimize therapeutic effects while minimizing adverse reactions, thereby enhancing the overall effectiveness and safety of prostaglandin medications. Such innovations not only meet the increasing demand for customized healthcare solutions but also strengthen the market's competitive edge by improving patient satisfaction and treatment outcomes.

Integration of Digital Technologies and Telemedicine Are Trending Factors

The incorporation of digital technologies and telemedicine into the prostaglandin market represents a significant trend. These technologies enable more dynamic patient management, allowing for continuous monitoring and timely adjustments to treatment plans.

For instance, the development of mobile apps and wearable devices to monitor patients' responses to prostaglandin therapies provides healthcare providers with real-time data, facilitating more precise and effective management of conditions. This trend enhances medication adherence and patient engagement by making health management more accessible and interactive. Additionally, it helps pharmaceutical companies to gather large amounts of data on drug performance, which can be used to refine drug formulations and dosing regimens, further driving innovation and market growth.

Regional Analysis

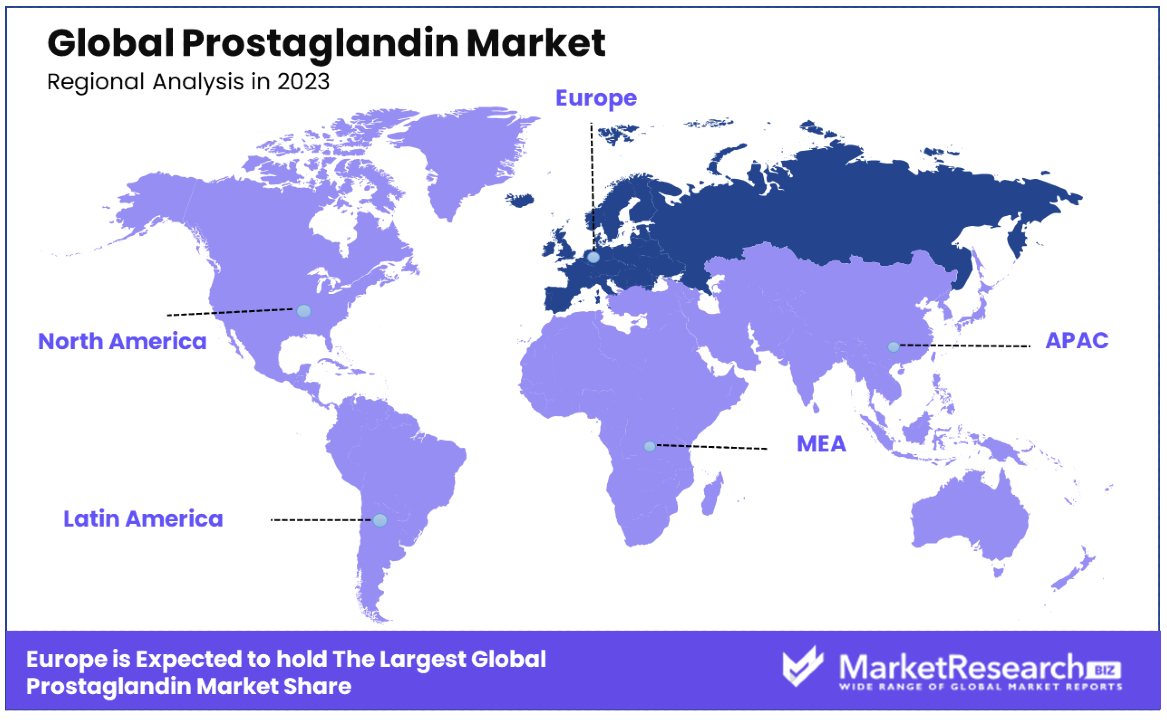

Europe Dominates with 36% Market Share

Europe's substantial 36% market share in the Prostaglandin Market can be attributed to its advanced healthcare infrastructure, robust regulatory frameworks, and significant investment in pharmaceutical R&D. The region's focus on innovative healthcare solutions and widespread acceptance of new therapeutic methods contribute to the high usage of prostaglandins, especially in areas like obstetrics and ophthalmology.

The presence of leading pharmaceutical companies and research institutions in Europe enhances its market dynamics. These entities drive innovation and development within the prostaglandin sector, supported by favorable government policies and healthcare spending. The market benefits from the region's high healthcare standards and patient access to new treatment options.

Europe is expected to maintain a strong position in the Prostaglandin Market. Continued emphasis on healthcare innovation and patient care quality, along with demographic trends such as an aging population, will likely sustain demand for prostaglandin products, ensuring Europe remains a key player in the global market.

Regional Market Shares and Dynamics

- North America: Holding a significant market share, North America, especially the United States, is a major player due to its advanced medical technologies and strong focus on healthcare research. Market share: approximately 30%.

- Asia Pacific: This region is experiencing the highest growth in the Prostaglandin Market, with a CAGR of 6.2%. Factors such as improving healthcare infrastructure, increasing healthcare spending, and rising awareness of treatments contribute to this growth.

- Middle East & Africa: While still developing in terms of market share, the Middle East and Africa show potential for growth due to increasing investments in healthcare and an expanding pharmaceutical sector. Market share: smaller but growing.

- Latin America: Latin America's market share is gradually increasing as the region develops its healthcare infrastructure and local governments push for better healthcare standards and access. Market share: modest but improving.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Prostaglandin Market, the key players including Cayman Chemical, Johnson Matthey, Yonsung Fine Chemicals, Chirogate, Everlight Chemical, Kyowa Hakko Pharma, and ANVI Pharma, significantly impact the competitive landscape through their strategic initiatives. These companies continuously enhance their market estimation and share by focusing on strategic product launches tailored to address critical health issues such as ocular hypertension in patients with glaucoma, facilitating the inflammatory response, and aiding the healing process.

The robust product portfolios of these firms encompass a wide range of applications, underpinned by rigorous clinical studies that validate the efficacy and safety of their products. This scientific backing is crucial for gaining a competitive edge. Furthermore, these players employ key strategies during the forecast period that include scaling up production capabilities and entering into partnerships and collaborations, which are vital for expanding their market presence.

Their efforts in the market are documented through in-depth analysis and detailed company profiles that highlight their achievements and advancements in technology. As the market evolves, these firms are expected to adapt by innovating and improving their offerings, thereby reinforcing their standing in the market and continuing to influence its growth trajectory.

Market Key Players

- Cayman Chemical

- Johnson Matthey

- Yonsung Fine Chemicals

- Chirogate

- Everlight Chemical

- Kyowa Hakko Pharma

- ANVI Pharma

Recent Developments

- On July 2023, EUROAPI announced a €50 million investment for the installation of a new state-of-the-art production plant at its Budapest site. The project is focused on the debottlenecking of the current capacity and the construction of new multi-purpose manufacturing equipment that will more than double the overall prostaglandin capacity of the Budapest site by 2027 in two phases: 2023-2025 and 2026-2027.

Report Scope

Report Features Description Market Value (2023) USD 510.8 Million Forecast Revenue (2033) USD 943.9 Million CAGR (2024-2033) 6.50% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Human Prostaglandins, Veterinary Prostaglandins), By Application (Obstetrics and Gynecology, Cardiovascular Diseases, Erectile Dysfunction, Glaucoma Treatment, Gastrointestinal Diseases, Respiratory Diseases, Renal Diseases), By Route of Administration (Oral, Intravenous, Topical, Intramuscular, Subcutaneous, Intraocular), By End Users (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Pharmacies) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Cayman Chemical, Johnson Matthey, Yonsung Fine Chemicals, Chirogate, Everlight Chemical, Kyowa Hakko Pharma, ANVI Pharma Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Cayman Chemical

- Johnson Matthey

- Yonsung Fine Chemicals

- Chirogate

- Everlight Chemical

- Kyowa Hakko Pharma

- ANVI Pharma

Our Clients

View Our Licence Options