Gastritis Market Report By Type (Acute Gastritis, Chronic Gastritis, Erosive Gastritis, Non-Erosive Gastritis), By Drug Type (Antacids, Antibiotics, Cytoprotective Agents, Prokinetics, Otheres), By Route of Administration (Oral, Parenteral), By End-User (Hospitals and Clinics, Specialty Centers, Homecare Settings), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

37549

-

March 2024

-

137

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

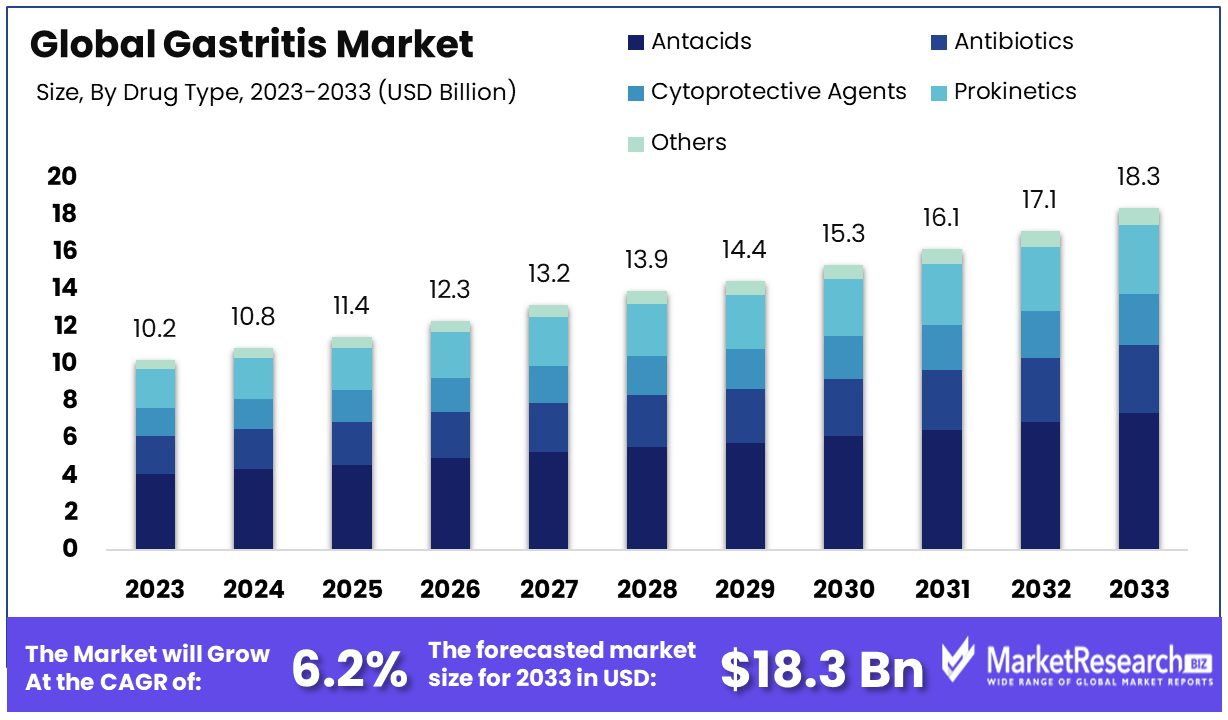

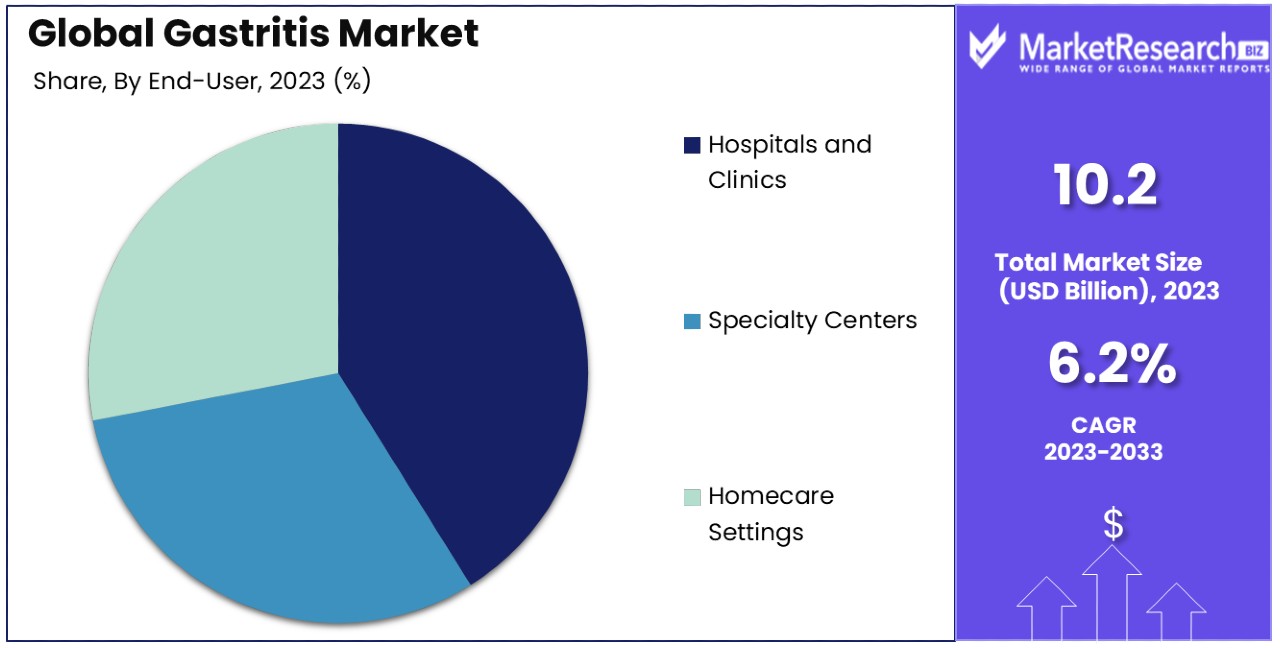

The Global Gastritis Market size is expected to be worth around USD 18.3 Billion by 2033, from USD 10.2 Billion in 2023, growing at a CAGR of 6.20% during the forecast period from 2024 to 2033.

The surge in demand for fast food globally, new advancement in the endoscopy devices and change in lifestyles are some of the main key driving factors for the gastritis market.

Gastritis is defined as the most common medical condition which is characterised by inflammation of the lining of the stomach. Such conditions can be acute by prevailing suddenly and lasting for a short duration and chronic, continuing for over a prolonged period.

The inflammation may be elicited by several reasons, by containing infections with Helicobacter pylori bacteria, huge amount of alcohol consumption, longer use of non-steroidal anti-inflammatory drugs (NSAIDs) or stress. The signs of the gastritis can be abdominal pain, nausea, bloating, Loss of appetite, vomiting and indigestions. Treatment and diagnosis generally consists of combination of past medical history, physical examination and tests like endoscopy and blood tests.

The treatments also include medications to minimize stomach acid production, antibiotics to eliminate H. pylori infection if detected, dietary change and lifestyle modifications. Some of the serious cases may also need hospitalization and blood fluids. Long term management aims on identifying underlying causes and avoid recurrence through lifestyle modifications and daily follow-up with healthcare providers.

According to an article Gastro Journal in September 2023, highlights that a global digestive disease study was conducted which covered 18 digestive disease all across 204 regions and territories. In 2019, there was 7.32 billion incidents and 2.86 billion occurrence cases of digestive disease that results in 8 million deaths and 277 million DALYs lost.

It was also observed that from 1990 to 2019 with 95,582 and 35,106 cases per 100,000 individuals in 2019 respectively. The age-standardized death was 102 per 100,000 individuals. Digestive diseases have been accounted for an important portions of the whole disease burden with more than ½ of occurrence cases having a digestive Etiology.

Gastritis can substantially effect lifestyle by causing discomfort by affecting eating habits and minimizing whole quality of life. Such treatment consists of maintaining a healthy lifestyle by avoiding spicy and acidic foods, restraining alcohol and caffeine intake and eliminating smoking. The medications such as proton pump inhibitors and antacids are generally prescribed to decrease stomach acid and improve symptoms.

A healthy lifestyle includes decreasing the stress methods and daily exercise that can also help to manage gastritis effectively. The demand for the gastritis will increase due to its high consumptions of the fast foods and digestive issues that will help in market expansion in the coming years.

Key Takeaways

- Market Value: The Global Gastritis Market is projected to reach USD 18.3 Billion by 2033, experiencing significant growth from its 2023 value, with a CAGR of 6.20% during the forecast period from 2024 to 2033.

- Dominant Segments:

- Acute Gastritis Analysis: Acute gastritis emerges as the dominant sub-segment due to its immediate and common manifestation, driven by factors such as NSAIDs use, alcohol consumption, and bacterial infections.

- Drug Type Analysis: Antacids lead the drug type category, offering immediate relief from gastritis symptoms with widespread availability, affordability, and minimal side effects.

- Route of Administration Analysis: Oral administration commands a significant 62% share due to its convenience and patient compliance, with antacids being the dominant oral medication.

- End-User Analysis: Hospitals and clinics hold 40% of the end-user market share, offering comprehensive care including diagnosis, treatment, and follow-up care.

- Regional Analysis: Europe dominates the market with a 36% share, followed by North America with approximately 29% market share, driven by high healthcare expenditure and advanced infrastructure.

- Analyst Viewpoint: The gastritis market's growth is fueled by factors such as the high incidence rate of acute gastritis, increasing awareness and diagnosis, advancements in treatment options, and the prevalence of chronic cases. The market's diversity in sub-segments and treatment modalities ensures comprehensive care and sustained growth opportunities.

- Market Key Players: Major players in the global gastritis market include Novartis AG, Pfizer Inc., Perrigo Pharmaceutical, Takeda Pharmaceutical Company Limited, and AbbVie Inc., among others. These companies offer a range of medications and treatment options, contributing to innovation and competition in the market.

Driving Factors

Increasing Prevalence of Gastritis Drives Market Growth

The escalating number of gastritis cases worldwide significantly propels the gastritis market forward. Approximately 8 million people in the United States are diagnosed with gastritis annually, a figure that underscores the widespread nature of the condition. This increase can be largely attributed to factors such as unhealthy eating habits, heightened stress levels, and the widespread occurrence of Helicobacter pylori infections. The direct correlation between the rising incidence of gastritis and market expansion is clear, as more individuals seeking diagnosis and treatment contribute to the demand for related healthcare services and products.

This trend not only highlights the immediate need for effective management strategies but also indicates a broader impact on the healthcare industry, including pharmaceuticals, diagnostic tools, and therapeutic procedures. The increasing prevalence of gastritis acts as a catalyst for enhanced research and development efforts, aiming to provide more effective and efficient treatment solutions, thereby further stimulating market growth.

Increasing Healthcare Expenditure Spurs Market Growth

The gastritis market is significantly bolstered by the global rise in healthcare expenditure. In 2022, the National Health Expenditure (NHE) in the United States alone grew by 4.1% to reach $4.5 trillion, with spending on prescription drugs rising by 8.4% to $405.9 billion. This trend is reflective of a broader global movement towards increased investment in healthcare infrastructure and services. As countries enhance their healthcare systems and expand access to medical services, there is a notable increase in the number of individuals seeking diagnosis and treatment for conditions like gastritis.

This is particularly evident in nations with growing economies, such as China, where rising disposable incomes are contributing to higher healthcare spending. The direct impact of this increased expenditure is a more robust gastritis market, characterized by greater demand for medical services, pharmaceuticals, and diagnostic tools. This influx of funding and resources into the healthcare sector not only facilitates the growth of the gastritis market but also contributes to the overall improvement of patient care and disease management strategies.

Technological Advancements in Diagnosis and Treatment Fuel Market Expansion

Technological innovations within the gastritis diagnosis and treatment landscape serve as a major impetus for market growth. The advent of endoscopic procedures, advanced imaging techniques, and personalized medicine has revolutionized the management of gastritis, offering more precise and less invasive options for patients.

Notably, the development of non-invasive diagnostic tests, such as breath tests for Helicobacter pylori detection, has significantly improved patient care by simplifying the diagnosis process and enhancing accuracy. These technological strides not only improve patient outcomes but also increase the efficiency of healthcare providers, thereby driving market growth. As these technologies continue to evolve and become more widely adopted, the gastritis market is expected to see sustained expansion, fueled by the combination of improved diagnostic and treatment methodologies and the ongoing need to address the high prevalence of the condition.

Restraining Factors

Side Effects of Medications Restrains Market Growth

The gastritis market is significantly hampered by the adverse effects associated with long-term use of common medications like proton pump inhibitors (PPIs). These drugs, while effective in managing symptoms, can lead to serious side effects including vitamin deficiencies, an increased risk of infections, and rebound acid hypersecretion upon sudden discontinuation.

For instance, extended PPI usage has been linked to a heightened risk of Clostridium difficile infection. These side effects present a considerable challenge for patient compliance and long-term treatment success, as they may deter individuals from continuing their medication regimen. Consequently, the market faces limitations in its expansion, as the potential risks of treatment might outweigh the benefits for some patients, leading to decreased demand for such medications and a search for alternative treatments with fewer side effects.

High Cost of Treatment Restrains Market Growth

The financial implications of diagnosing and managing gastritis serve as a major barrier to market growth. Diagnostic processes like endoscopic examinations, along with the costs associated with laboratory tests, prescription medications, and necessary follow-up consultations, compile a substantial financial burden.

This is particularly impactful in areas with limited healthcare coverage or significant out-of-pocket expenses, making access to quality care challenging for a vast segment of the global population. In regions with economic constraints, such as certain parts of Africa, the high cost of treatment can prevent individuals from seeking or continuing care for gastritis. This financial hurdle directly limits the expansion of the gastritis market, as the affordability and accessibility of treatment become crucial factors influencing patient engagement and overall market potential.

Type Analysis

Acute gastritis stands out as the dominant sub-segment within the gastritis market, primarily because it represents the most immediate and common manifestation of the condition. Triggered by factors such as nonsteroidal anti-inflammatory drugs (NSAIDs) use, excessive alcohol consumption, and bacterial infections, acute gastritis showcases a high incidence rate globally. The straightforward diagnosis process, coupled with a generally effective short-term treatment regimen, contributes significantly to its prominence in the market. Despite its dominance, the acute gastritis segment's growth is complemented by the roles of chronic, erosive, and non-erosive gastritis sub-segments.

Chronic gastritis, while not as immediately prevalent as its acute counterpart, plays a crucial role in the long-term health market. Its management often requires ongoing monitoring and treatment, contributing to steady revenue streams for healthcare providers and pharmaceutical companies. Erosive and non-erosive gastritis, although smaller in market size, address niche patient needs and treatment modalities. These sub-segments cater to specific patient demographics, offering tailored treatment options that underscore the market's diversity.

This diversity within the gastritis market allows for a broad range of therapeutic approaches and supports sustained growth by catering to a wide patient base. Research and development efforts, alongside technological advancements in diagnostic methods, continue to refine the understanding and treatment of all gastritis types, further shaping the market dynamics.

Drug Type Analysis

In the gastritis market, antacids emerge as the dominant sub-segment within the drug type category, primarily due to their effectiveness in providing immediate relief from the symptoms of gastritis. Antacids work by neutralizing stomach acid, offering quick relief from discomfort and pain associated with the condition.

Their widespread availability, over-the-counter status, and affordability contribute significantly to their leading position in the market. Additionally, the simplicity of their mechanism and the minimal risk of side effects make them a preferred choice for both patients and healthcare providers.

Other segments within the drug type category, including antibiotics, cytoprotective agents, and prokinetics, play crucial roles in the comprehensive management of gastritis. Antibiotics are essential for treating gastritis caused by H. pylori infection, directly addressing the root cause of a significant proportion of gastritis cases.

Cytoprotective agents help protect the stomach's lining from acid, thereby aiding in the healing process, while prokinetics are used to improve gastric motility, beneficial in cases where gastritis is accompanied by gastric emptying delays. Each of these drug types caters to specific needs within the gastritis treatment landscape, contributing to the overall growth of the market by offering a range of therapeutic options tailored to the diverse manifestations of gastritis.

Route of Administration Analysis

The oral route of administration holds a commanding 62% share in the gastritis market, underscoring its convenience and ease of use. Oral medications, including the dominant antacids, antibiotics, and cytoprotective agents, are preferred for their non-invasive nature, ease of administration, and patient compliance.

This route's predominance is facilitated by the widespread availability of oral formulations, which allows for self-administration and management of symptoms in a home setting, thereby enhancing patient comfort and adherence to treatment regimens.

Parenteral administration, while less common, is crucial in situations where oral administration is not feasible, such as severe nausea or vomiting, or when a rapid onset of action is required. This route plays a complementary role in the gastritis treatment landscape, ensuring that patients can receive effective treatment even under challenging circumstances.

End-User Analysis

Hospitals and clinics, accounting for 40% of the end-user market share, represent the primary care settings for gastritis treatment. This dominance is attributed to the comprehensive care these institutions provide, including diagnosis, treatment, and follow-up care.

Hospitals and clinics are equipped with the necessary facilities for endoscopic examinations and other diagnostic procedures, making them integral to the management of gastritis. The availability of a wide range of treatment options, including both medication and, if necessary, surgical intervention, further solidifies their position as the primary care providers for gastritis patients.

Specialty centers and homecare settings are also pivotal to the gastritis market's growth. Specialty centers offer focused care for more severe or complicated cases of gastritis, often employing multidisciplinary approaches that can include advanced diagnostic and treatment methods.

Homecare settings are increasingly becoming important as they support the ongoing management of chronic gastritis, emphasizing the role of lifestyle modifications and medication adherence in long-term disease management. Together, these segments ensure a holistic approach to gastritis treatment, catering to the needs of diverse patient populations and contributing to the overall expansion of the market.

Key Market Segments

By Type

- Acute Gastritis

- Chronic Gastritis

- Erosive Gastritis

- Non-Erosive Gastritis

By Drug Type

- Antacids

- Antibiotics

- Cytoprotective Agents

- Prokinetics

- Otheres

By Route of Administration

- Oral

- Parenteral

By End-User

- Hospitals and Clinics

- Specialty Centers

- Homecare Settings

Growth Opportunities

Personalized Medicine Offers Growth Opportunity

The shift towards personalized medicine is carving out substantial growth opportunities within the gastritis market. This approach leverages individual patient profiles, including genetic predispositions and lifestyle factors, to tailor treatments specifically to each person's needs. Personalized medicine has the potential to significantly improve treatment outcomes and patient satisfaction by offering more precise and effective management strategies for gastritis.

With the healthcare sector's growing focus on individualized care, investments in genetic testing and other technologies that support personalized treatment plans are becoming increasingly important. These advancements not only enhance patient care but also position companies at the forefront of the gastritis market. By providing tailored therapies, healthcare providers can better meet the diverse needs of patients, leading to improved health outcomes and a stronger demand for personalized healthcare solutions.

Digital Health Solutions Integration Offers Growth Opportunity

Integrating digital health solutions, especially telemedicine, is opening new avenues for growth in the gastritis market. Telemedicine services, which enable remote consultations with healthcare professionals, significantly improve access to care for patients with gastritis. This technological advancement supports more efficient patient care processes, from diagnosis through treatment and follow-up, by facilitating easier communication between patients and healthcare providers.

Additionally, digital health platforms can enhance treatment adherence and patient experience by offering convenient, timely, and personalized care options. The adoption of digital health technologies by companies within the gastritis market is poised to drive market expansion, as patients increasingly seek accessible and efficient healthcare services. This trend towards digital integration reflects a broader shift in healthcare towards more patient-centered and technologically enabled care models, providing a significant opportunity for growth in the management and treatment of gastritis.

Trending Factors

Natural Remedies Are Trending Factors

The increasing inclination towards natural and herbal remedies in managing gastritis signifies a burgeoning market segment. Recent data reveals a surge in demand for alternative therapies, with a significant portion of consumers favoring holistic approaches. Statistics indicate a notable uptick in sales of natural gastritis management products, reflecting consumers' growing trust in these remedies.

This trend presents a lucrative opportunity for companies specializing in natural supplements, herbal teas, and tailored dietary solutions. By catering to the preferences of health-conscious consumers, companies can expand their market reach and capitalize on the shift towards natural remedies. Moreover, this trend addresses concerns about the potential side effects associated with conventional medications, further bolstering its appeal.

Changing Lifestyles Are Trending Factors

Modern lifestyles characterized by erratic eating patterns and heightened stress levels are pivotal drivers behind the escalating prevalence of gastritis. Recent statistics underscore the profound impact of lifestyle choices on gastritis incidence rates, with a notable correlation between fast-paced living and digestive health issues.

This trend creates a fertile ground for market expansion, as consumers seek effective treatments and management options to alleviate gastritis symptoms. Companies can leverage this trend by developing tailored marketing strategies and innovative products that address the specific needs of individuals grappling with hectic lifestyles. By aligning offerings with consumer preferences and lifestyle demands, companies can position themselves for substantial growth within the gastritis market.

Regional Analysis

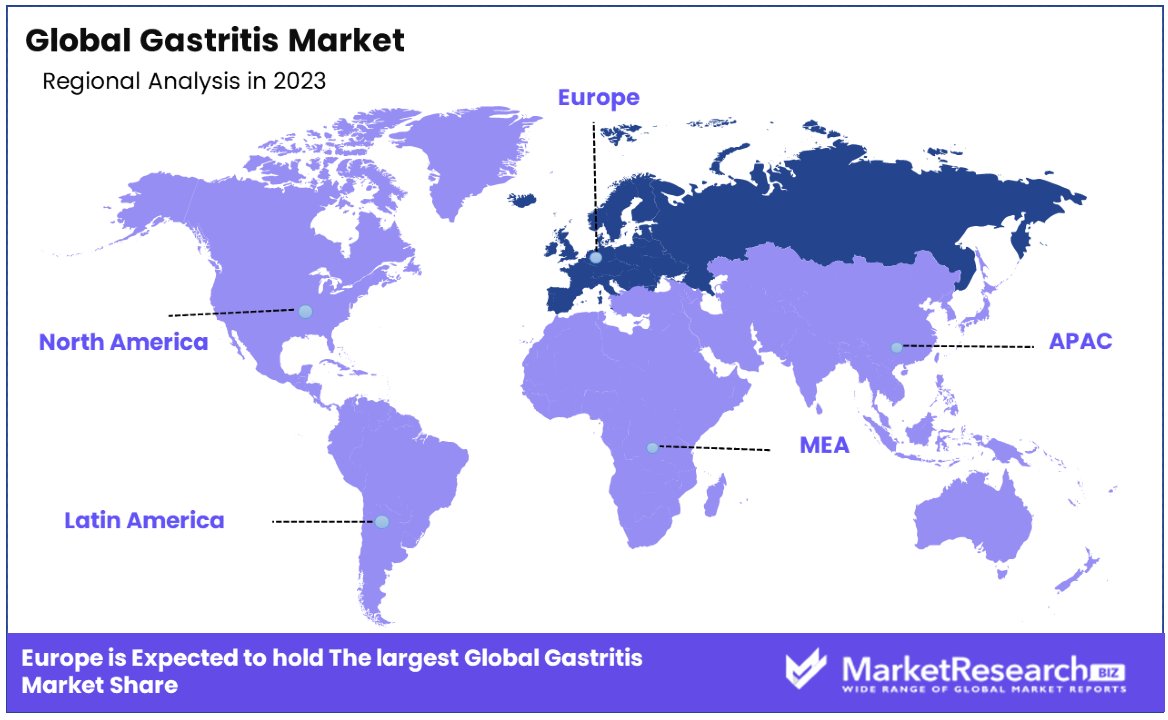

Europe Dominates with 36% Market Share

Europe's prominent position in the gastritis market, holding a 36% share, is a reflection of several key factors. The region's advanced healthcare infrastructure, high awareness regarding gastrointestinal health, and significant healthcare spending contribute to its dominance. Additionally, Europe's stringent regulatory environment ensures the availability of effective and safe treatment options, further driving market growth. The prevalence of Helicobacter pylori infection, coupled with lifestyle factors such as diet and stress, also plays a crucial role in the high incidence of gastritis across European countries. This situation is bolstered by robust research and development activities in the pharmaceutical and healthcare sectors, promoting innovation in gastritis diagnosis and treatment.

Market dynamics within Europe are influenced by its comprehensive healthcare systems, which ensure widespread access to medical services. This accessibility, along with a growing elderly population susceptible to gastrointestinal conditions, amplifies the demand for gastritis treatments. The region's emphasis on preventive healthcare and early diagnosis further strengthens the market.

Europe is expected to maintain its influence in the gastritis market. The ongoing investment in healthcare infrastructure and research, along with increasing awareness about the importance of gastrointestinal health, will likely sustain Europe's market share. The introduction of new and innovative treatments, supported by a strong regulatory framework, will continue to facilitate market growth.

- North America: With a market share of approximately 29%, North America stands as a pivotal region in the gastritis market. High healthcare expenditure in the region supports advanced diagnostics and treatment options for gastritis, while its advanced medical technology and infrastructure facilitate efficient diagnosis and management.

- Asia Pacific: Asia Pacific holds an approximate market share of 20%, making it a significant player in the gastritis market. Rapidly increasing healthcare awareness among the population has led to early detection and management of gastritis. Improvements in healthcare infrastructure and services across the region have expanded access to quality diagnostics and treatment options.

- Middle East & Africa: With a market share of approximately 8%, the Middle East & Africa region plays a crucial role in the gastritis market. Gradual improvements in healthcare systems and infrastructure are enhancing access to diagnostics and treatment for gastritis.

- Latin America: Latin America holds around 7% of the market share, positioning it as an emerging player in the gastritis market. Improvements in healthcare systems and increased access to healthcare services are benefiting gastritis management and treatment in the region.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Gastritis Market, key companies like Novartis AG, Pfizer Inc., and Takeda Pharmaceutical Company Limited hold significant influence and strategic positioning.

Their impact is evident in various aspects, including pharmaceutical interventions, product launches, and market entry strategies. For instance, Novartis AG's innovative pharmaceutical solutions cater to different Route of Administration preferences, ensuring widespread accessibility and efficacy.

Pfizer Inc. and Takeda Pharmaceutical Company Limited also play crucial roles, leveraging their extensive product portfolios and global reach to address gastritis-related concerns effectively.

These major market players continually invest in research and development to introduce new treatments and enhance existing ones. Their strategic pricing analysis and market entry strategies enable them to capture a significant portion of the market share, particularly in regions like North America and the United Kingdom.

Industry experts closely monitor their key developments, including advancements in pharmaceutical formulations and adaptations to changing dietary patterns. Overall, the Gastritis Market's largest market share is held by these major players, shaping the industry landscape and improving patient outcomes through innovative solutions.

Market Key Players

- Novartis AG

- Pfizer Inc.

- Perrigo Pharmaceutical

- Takeda Pharmaceutical Company Limited

- Lupin Ltd

- AbbVie Inc.

- Katsura Chemical

- SAURAV CHEMICALS

- Bio-Rad Laboratories

- SUN Pharmaceuticals Industries

- Johnson & Johnson

- Wuhan Senwayer Century

- Siemens Healthineers AG

Recent Developments

- On December 2023, Phathom Pharmaceuticals announced that the U.S. Food and Drug Administration (FDA) accepted for review its New Drug Application (NDA) for Voquenza as a daily treatment for adults with Non-Erosive Gastroesophageal Reflux Disease (GERD)

- On April 2023, Akums Drugs and Pharmaceuticals introduced a novel Combikit for the treatment of duodenal ulcer and H. pylori infection. The Combikit consists of a unique combination of Amoxicillin, Clarithromycin, and Esomeprazole.

- On August 2022, Daewoong Pharmaceuticals announced that its drug Fexuclue (Fexuprazan hydrochloride) received an adaptation certificate for improving gastric mucosal lesions of acute and chronic gastritis, securing additional indications within a month of its official launch in Korea.

Report Scope

Report Features Description Market Value (2023) USD 10.2 Billion Forecast Revenue (2033) USD 18.3 Billion CAGR (2024-2033) 6.20% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Acute Gastritis, Chronic Gastritis, Erosive Gastritis, Non-Erosive Gastritis), By Drug Type (Antacids, Antibiotics, Cytoprotective Agents, Prokinetics, Otheres), By Route of Administration (Oral, Parenteral), By End-User (Hospitals and Clinics, Specialty Centers, Homecare Settings) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Novartis AG, Pfizer Inc., Perrigo Pharmaceutical, Takeda Pharmaceutical Company Limited, Lupin Ltd, AbbVie Inc., Katsura Chemical, SAURAV CHEMICALS, Bio-Rad Laboratories, SUN Pharmaceuticals Industries, Johnson & Johnson, Wuhan Senwayer Century, Siemens Healthineers AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- AstraZeneca PLC

- Takeda Pharmaceutical Company Limited

- Pfizer Inc.

- AbbVie Inc.

- Bayer AG

- Eli Lilly and Company

- Novartis AG

- Merck & Co., Inc.

- Sanofi S.A.

- Johnson & Johnson

- Bio-Rad Laboratories, Inc.

- F. Hoffmann-La Roche Ltd

- Siemens Healthineers AG

- Other Key Players

Our Clients

View Our Licence Options