Power Plant Boiler Market Report By Fuel Type/Heat Source (Coal, Natural Gas, Nuclear Reactor, Petroleum, Others), By Material (Conventional Materials, Designed Materials), By Technology (Ultra-Critical, Super Critical, Subcritical, Advanced Ultra-Supercritical), By Process, By Type, By Capacity, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

4148

-

March 2024

-

182

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Report Overview

- Key Takeaways

- Driving Factors

- Restraining Factors

- Fuel Type/Heat Source Segmentation Analysis

- Material Segmentation Analysis

- Technology Segmentation Analysis

- Type Segmentation Analysis

- Capacity Segmentation Analysis

- Key Market Segments

- Growth Opportunities

- Trending Factors

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

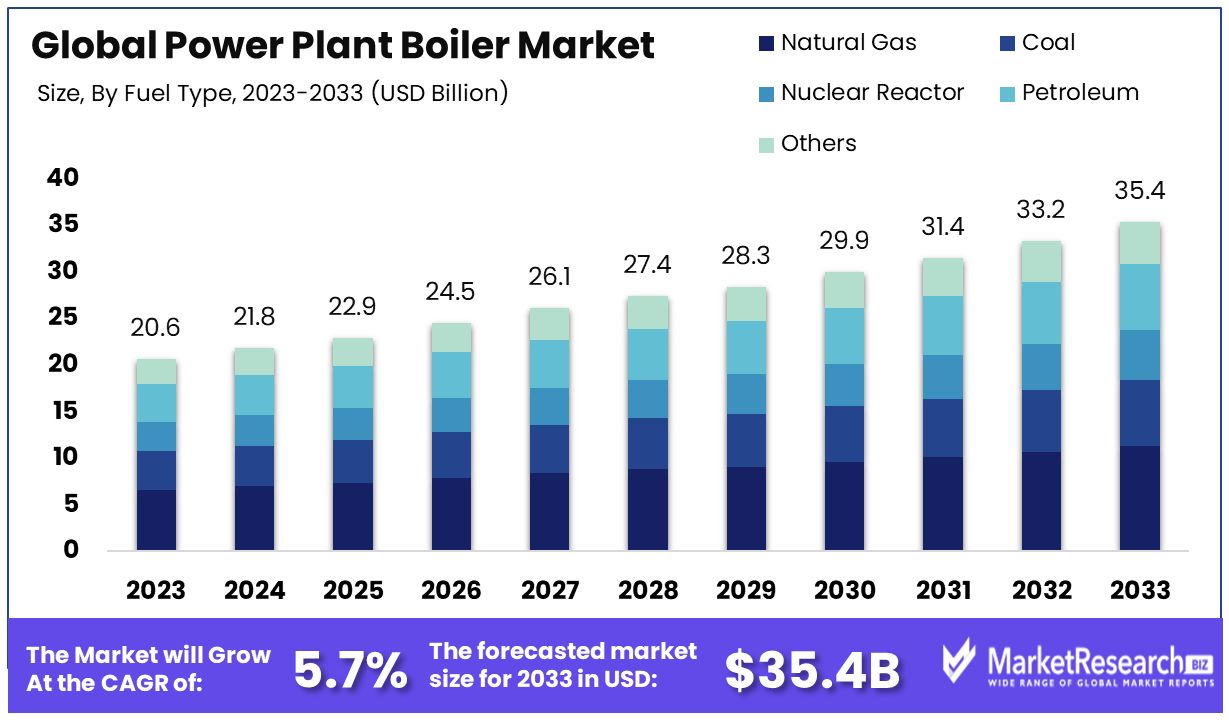

The Global Power Plant Boiler Market size is expected to be worth around USD 35.4 Billion by 2033, from USD 20.6 Billion in 2023, growing at a CAGR of 5.70% during the forecast period from 2024 to 2033.

The surge in demand for supercritical and ultra-supercritical boiler technologies, the rise in thermal plant production, and the use of natural fuels are some of the main driving factors for the power plant boiler market.

A power plant boiler is defined as an important element in electricity generation facilities that is responsible for transforming water into steam. This steam is further used to propel turbines connected to generators for generating electrical energy.

These power plant boilers generally use fossil fuels such as natural gas, oil, coal, or any other renewable source like biomass. The combustion of fuel inside the boiler produces high-pressure and high-temperature steam, which can drive the turbine blades to produce electricity.

Moreover, advanced technologies such as supercritical and ultra-supercritical boilers improve efficacy and minimize environmental impact by boosting the steam generation method. Boilers also play a vital role in cogeneration, where excess heat is used for different industrial methods or district heating that enable power plant boilers, which are important to the efficient and sustainable production of electricity.

According to an article published by Energy World in March 2024, a series of ambitious projects have been launched under the National Thermal Power Corporation by PM Narendra Modi. These projects, with a combined investment of Rs. 30,023 crore, mark an important advancement in India’s commitment to improve its power infrastructure while focusing on environmental conservation and job creation.

Moreover, the main highlights of this launch include the 800 MW Unit 2 of the NTPC’s Telangana super thermal power project, stage 1, in Peddapalli district, Telangana. Additionally, with the investment of Rs. 8,007 crores and imposing ultra-supercritical technology, this project will decrease CO2 emissions while augmenting the highest power generation efficacy among NTPC’s power stations in India at approx. 42%.

There will be another launch of 660 MW Unit 2 of the North Karanpura super thermal power project in Jharkhand, India’s first supercritical thermal power project, which is equipped with air-cooled condenser technology. The total investment in this project is Rs. 4,609 crore.

Modern power plant boilers are important for sustainable energy generation because they facilitate the effective conversion of diverse fuels into electricity. Their importance lies in boosting energy production, decreasing environmental effects, and supporting the transition to renewable energy sources by contributing to a more sustainable and resilient power setup. The demand for the power plant boiler will increase due to its high requirement for thermal production, which will help in market expansion in the coming years.

Key Takeaways

- Market Value:The Global Power Plant Boiler Market is projected to reach approximately USD 35.4 Billion by 2033, experiencing robust growth from USD 20.6 Billion in 2023, with a CAGR of 5.70% during the forecast period from 2024 to 2033.

- Natural gas emerges as the dominant fuel type, reflecting the market's shift towards lower-emission energy sources, holding a significant market share.

- Designed materials lead the material segmentation, essential for the efficiency and longevity of boilers, particularly in advanced technologies, with a prominent market share.

- Supercritical boilers dominate the technology segmentation, characterized by enhanced efficiency and reduced emissions compared to subcritical boilers, commanding a considerable market share.

- Pulverized Coal Tower Boilers stand out as the dominant type, favored for their efficiency and widespread adoption, holding a significant market share.

- The 400 MW to 800 MW capacity range leads the capacity segmentation, offering an optimal balance of efficiency, cost, and flexibility, with a prominent market share.

- Regional Insights: Asia Pacific dominates the Power Plant Boiler Market with a substantial 37% market share, driven by factors like rapid industrialization, urbanization, and increasing energy demands. North America holds a significant market share of approximately 20%

- Analyst Viewpoint: The dominance of natural gas reflects the industry's response to environmental concerns and the global push for lower-emission energy sources. Advancements in designed materials, supercritical technology, and other segments underscore the industry's commitment to innovation, sustainability, and performance optimization.

- Growth Opportunities: Opportunities lie in developing sustainable and efficient boiler technologies to meet growing energy demands while reducing environmental impact. Market players can capitalize on the demand for advanced materials, supercritical technologies, and alternative fuel sources to drive innovation and market expansion.

Driving Factors

Increasing Demand for Electricity Drives Market Growth

The global surge in electricity demand, propelled by population growth, industrialization, and urbanization, particularly in developing economies, serves as a key driver for the Power Plant Boiler Market. This rising need for electricity necessitates the construction of new power plants and the modernization of existing ones, thereby fueling the demand for efficient and reliable boilers.

For instance, on March 2, 2024, at 8 p.m. EST, the U.S. Energy Information Administration reported an hourly electricity demand of 434,806 megawatt-hours in the United States. Similarly, countries like China and India have observed a notable increase in electricity consumption, which, in turn, boosts the requirement for power plant boilers. This trend underlines the critical role of power plant boilers in meeting the burgeoning electricity needs, highlighting their importance in the energy infrastructure development across the globe.

Emphasis on Energy Efficiency and Emissions Reduction Propels Market Expansion

The Power Plant Boiler Market is significantly influenced by the growing focus on energy efficiency and emissions reduction within the power generation sector. Advanced boiler technologies, such as supercritical and ultra-supercritical boilers, are being adopted for their higher thermal efficiencies and lower emission rates, aligning with stringent environmental regulations and operational cost reduction goals.

For example, in 2022, the U.S. Energy Information Administration noted the total primary energy consumption in the United States to be 100.41 quadrillion British thermal units (Btu), with the electric power sector consuming 37.75 quadrillion Btu. The implementation of rigorous emissions standards in countries including the United States and various European nations has spurred utilities to upgrade their boiler systems, illustrating the significant impact of regulatory policies on market growth.

Shift towards Renewable and Cleaner Energy Sources Stimulates Market Demand

The global transition towards renewable and cleaner energy sources, including biomass, municipal solid waste, and solar power, is generating demand for specialized boilers capable of handling diverse fuel types.

Biomass-fired boilers, for instance, are increasingly popular in countries such as Sweden, Finland, and Germany, where renewable energy targets support the adoption of such technologies. This shift not only emphasizes the adaptability of the Power Plant Boiler Market to evolving energy landscapes but also highlights the sector's potential for innovation in response to changing environmental priorities.

Aging Infrastructure and Boiler Replacement Needs Encourage Market Opportunities

The necessity for replacing or modernizing aging boiler systems in existing power plants presents significant growth opportunities for the Power Plant Boiler Market. Many coal-fired power plants in the United States are approaching retirement age, necessitating either boiler replacements or retrofits to enhance efficiency, reliability, and compliance with environmental regulations.

This scenario underscores the continuous need for investment in boiler technology and infrastructure, ensuring the sector's resilience and adaptability to both market and regulatory demands.

Restraining Factors

High Capital Costs and Investment Requirements Restrain Market Growth

The high initial capital costs and investment requirements for constructing and installing power plant boilers act as a major barrier to market entry, particularly for smaller utilities or projects with constrained budgets. The comprehensive expenses associated with power plant boilers—spanning equipment, engineering, and construction—can escalate into millions or even billions of dollars, based on the project's scale and intricacy.

For instance, the installation of a new ultra-supercritical coal-fired boiler can necessitate financial outlays ranging from hundreds of millions to beyond a billion dollars. This formidable financial commitment can deter potential market entrants, limiting the expansion of the Power Plant Boiler Market by making it challenging for some entities to engage in new installations or upgrades.

Stringent Environmental Regulations and Compliance Challenges Restrain Market Growth

Stringent environmental regulations, designed to curtail emissions and diminish the environmental footprint of power generation, impose significant compliance challenges and financial burdens on boiler manufacturers and power plant operators. Adhering to these regulations necessitates considerable investment in upgrading boiler systems and pollution control technologies.

Failure to meet these standards can lead to severe penalties, operational limitations, or even the closure of facilities. The implementation of standards such as the Mercury and Air Toxics Standards (MATS) in the United States exemplifies the extensive investments required from coal-fired power plants to comply with regulatory mandates. This compliance burden not only increases operational costs but also limits market growth by hindering the development of new projects and the modernization of existing infrastructure.

Fuel Type/Heat Source Segmentation Analysis

In the Power Plant Boiler Market, the segmentation by fuel type or heat source is crucial for understanding the market dynamics and preferences. Among these, natural gas emerges as the dominant sub-segment, driven by its cleaner combustion, availability, and efficiency in power generation.

Coal, nuclear reactors, petroleum, and other fuel sources also play significant roles in the market, each catering to specific geographic and technological contexts. Coal-fired boilers, despite their environmental impact, continue to support electricity generation in regions with abundant coal reserves. Nuclear reactors offer a low-emission alternative, with advancements aimed at enhancing safety and efficiency. Petroleum-based boilers are less common due to higher fuel costs and environmental concerns but remain vital in areas with limited access to alternative fuels.

The "others" category, including renewable energy sources and waste-to-energy technologies, reflects a growing interest in sustainable and innovative energy solutions. The natural gas segment's dominance is attributed to the shift towards lower-emission energy sources, the retrofitting of existing coal-fired plants, and the development of new, efficient natural gas-fired plants. This trend is reinforced by global efforts to reduce carbon footprints and improve air quality, making natural gas a preferred choice for new power generation capacities.

Material Segmentation Analysis

In the material segmentation of the Power Plant Boiler Market, designed materials stand out as the dominant sub-segment. These materials, engineered to withstand extreme temperatures and pressures, are essential for the efficiency and longevity of boilers, particularly in advanced technologies like supercritical and ultra-supercritical systems.

Conventional materials, although still widely used, are gradually being supplanted by designed materials due to their limitations in handling the operational demands of modern boiler technologies. The transition towards designed materials is driven by the need for higher efficiency, reduced emissions, and extended operational life of boilers.

This shift is particularly evident in the development and deployment of advanced materials that can endure the rigorous conditions of ultra-critical and supercritical technologies. The emphasis on designed materials reflects an industry-wide move towards innovation, sustainability, and performance optimization, highlighting their pivotal role in the market's future growth.

Technology Segmentation Analysis

The technology segmentation of the Power Plant Boiler Market reveals supercritical boilers as the dominant sub-segment, characterized by their enhanced efficiency and reduced carbon emissions compared to subcritical boilers. Ultra-critical, subcritical, and advanced ultra-supercritical technologies represent the spectrum of options available to power plant operators, each with distinct operational and environmental implications.

Supercritical boilers have gained prominence due to their ability to operate at higher temperatures and pressures, resulting in better fuel utilization and lower greenhouse gas emissions. While subcritical boilers remain in use for their cost-effectiveness and reliability, the push for cleaner and more efficient energy production has led to increased investment in supercritical and advanced ultra-supercritical technologies.

These advanced technologies offer even greater efficiencies and environmental benefits, setting the stage for future advancements in the sector. The dominance of supercritical technology underscores the industry's commitment to balancing operational efficiency with environmental stewardship, a trend that is expected to continue as technological innovations and regulatory pressures evolve.

Type Segmentation Analysis

Within the Power Plant Boiler Market, the type segmentation reveals that the Pulverized Coal Tower Boiler is the dominant sub-segment. This dominance is attributed to the efficiency and widespread adoption of pulverized coal technology in power generation. Pulverized Coal Tower Boilers are favored for their ability to burn coal into a fine powder, which enhances combustion efficiency and reduces emissions.

This technology is well-established and continues to be preferred in regions heavily reliant on coal for electricity generation. On the other hand, the Circulating Fluidized Bed Boiler represents an alternative technology that offers benefits in terms of fuel flexibility and environmental performance. These boilers can efficiently combust a wide range of fuels, including low-quality coal and biomass, making them a viable option for locations with diverse fuel sources.

Despite the advantages of Circulating Fluidized Bed Boilers, the Pulverized Coal Tower Boiler remains the market leader due to its proven performance and technological maturity. However, the evolving landscape of energy production, with a growing emphasis on sustainability and emissions reduction, suggests potential growth opportunities for Circulating Fluidized Bed Boiler technology, especially in markets aiming to diversify their energy mix and reduce reliance on high-grade coal.

Capacity Segmentation Analysis

The Capacity Segmentation of the Power Plant Boiler Market is significantly led by the 400 MW to 800 MW range, which has emerged as the dominant sub-segment. This segment's prominence is largely due to the optimal balance it offers between efficiency, cost, and flexibility for medium to large-scale power generation projects. Boilers within this capacity range are capable of meeting the electricity demands of large urban centers and industrial complexes, making them a preferred choice for new installations and upgrades.

The less than 400 MW segment caters primarily to smaller power plants and decentralized energy generation systems, where the emphasis is on meeting local energy needs or serving specific industrial processes. Although important for the market, these smaller units often face challenges in achieving the economies of scale and efficiency levels of their larger counterparts. Conversely, boilers with a capacity of more than 800 MW cater to very large power generation projects, where high output and efficiency are critical.

While this segment represents the high end of the market, the significant capital investment and operational complexities involved limit its growth compared to the 400 MW to 800 MW segment. The dominance of the 400 MW to 800 MW boilers underscores their role as a versatile and economically viable solution for a broad range of power generation needs, positioning them as a key driver in the global Power Plant Boiler Market's growth.

Key Market Segments

By Fuel Type/Heat Source

- Coal

- Natural Gas

- Nuclear Reactor

- Petroleum

- Others

By Material

- Conventional Materials

- Designed Materials

By Technology

- Ultra-Critical

- Super Critical

- Subcritical

- Advanced Ultra-Supercritical

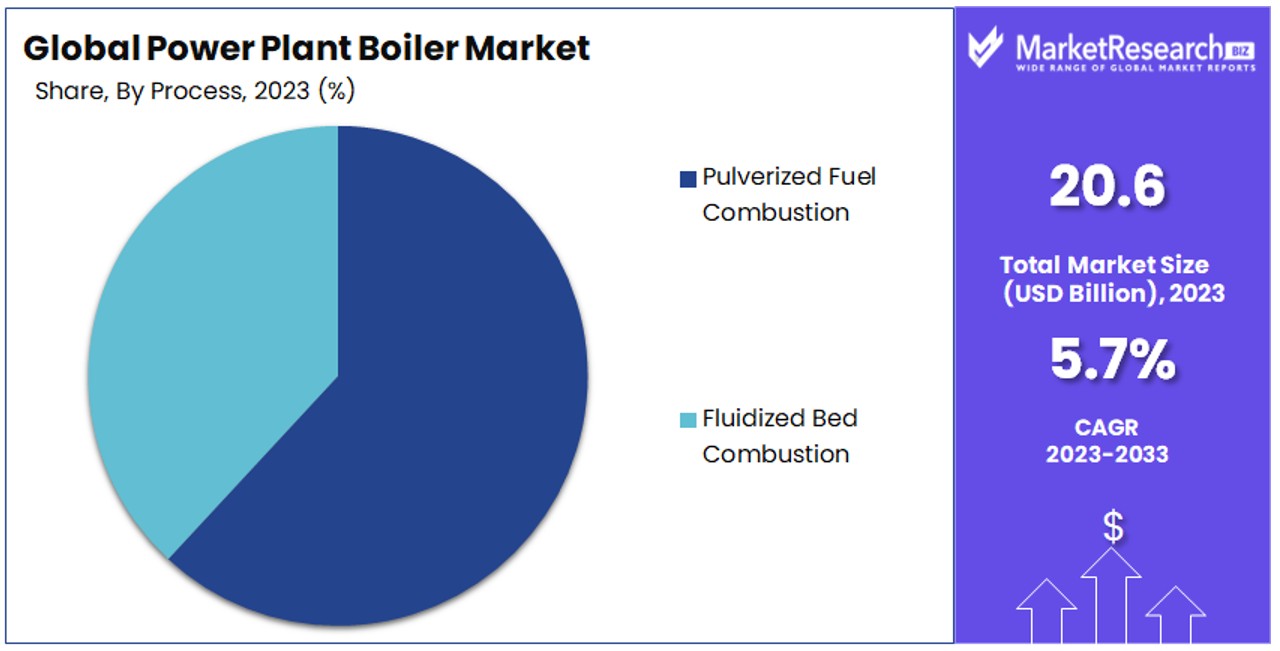

By Process

- Fluidized Bed Combustion

- Pulverized Fuel Combustion

By Type

- Pulverized Coal Tower Boiler

- Circulating Fluidized Bed Boiler

By Capacity

- Less than 400 MW

- 400 MW to 800 MW

- More than 800 MW

Growth Opportunities

Retrofitting and Upgrades of Existing Power Plants Offers Growth Opportunity

The opportunity to retrofit and upgrade existing power plants presents a significant growth avenue for the Power Plant Boiler Market. As power plants worldwide reach or exceed their designed operational lifespans, the demand for modernization to enhance efficiency, reduce emissions, and extend operational life is rising. For instance, numerous coal-fired power plants in the United States and Europe are currently undergoing boiler retrofits to meet environmental regulations and boost performance.

These modifications not only ensure compliance with increasingly stringent environmental standards but also offer a cost-effective alternative to constructing new facilities. By upgrading existing boilers with advanced technologies, plants can achieve higher efficiency levels and lower emission outputs, thereby prolonging their useful life and supporting the global transition towards cleaner energy production. This trend underscores the market potential for boiler manufacturers capable of providing innovative retrofitting and upgrading solutions.

Adoption of Flexible and Hybrid Power Generation Solutions Offers Growth Opportunity

The integration of renewable energy sources into the power grid necessitates the development of flexible and hybrid power generation solutions, marking a promising growth opportunity for the Power Plant Boiler Market. The variability of renewable energy sources like wind and solar requires power generation systems that can quickly adjust output to maintain grid stability. This scenario opens up prospects for boiler manufacturers to innovate boilers capable of operating in load-following or cycling modes, efficiently complementing intermittent renewable energies.

Furthermore, the development of hybrid systems that merge renewable energy with traditional power sources poses a demand for specialized boiler designs capable of seamless integration. These advancements facilitate the transition towards a more sustainable and resilient energy infrastructure, positioning boiler manufacturers at the forefront of the evolving power generation landscape. Together, these factors highlight a shift in market dynamics, where flexibility and sustainability become key drivers of growth and innovation in the Power Plant Boiler Market.

Trending Factors

Digitalization and Advanced Process Control Are Trending Factors

The integration of digital technologies, including advanced process control systems, data analytics, and predictive maintenance, marks a significant trending factor in the Power Plant Boiler Market. These innovations enhance operational efficiency, improve monitoring and control, and facilitate predictive maintenance, leading to optimized performance, increased reliability, and minimized downtime.

The adoption of digital solutions allows for real-time data analysis and decision-making, improving the responsiveness of boiler operations to changing conditions and demands. This digital transformation is reshaping the power plant boiler landscape by introducing efficiencies that reduce operational costs and environmental impacts, positioning digitalization and advanced process control as key drivers of the market's future direction.

Focus on Modular and Compact Boiler Designs Are Trending Factors

The shift towards modular and compact boiler designs is a notable trend, especially relevant for smaller power plants, distributed generation systems, and industrial applications. These designs offer significant advantages, such as ease of transportation, quicker installation, and the ability to scale operations to meet specific capacity needs efficiently.

Modular boilers cater to the growing demand for flexible and adaptable energy solutions, allowing for phased investment and expansion in line with demand. This trend reflects the market's adaptation to changing energy generation landscapes, where speed, flexibility, and scalability are increasingly valued, driving the popularity of modular and compact boiler systems.

Emphasis on Fuel Flexibility and Diversification Are Trending Factors

The emphasis on fuel flexibility and diversification is increasingly becoming a trending factor within the Power Plant Boiler Market. As concerns over energy security and sustainability grow, operators are looking for boilers capable of burning a wide array of fuels, including renewable and alternative options.

This drive for fuel flexibility encourages boiler manufacturers to innovate and develop systems that can easily switch between fuel types such as coal, natural gas, biomass, and waste-derived fuels. Such versatility not only enhances the adaptability of power generation systems to fluctuating fuel markets and regulations but also supports the integration of renewable energy sources, underscoring the industry's move towards more sustainable and resilient energy solutions.

Regional Analysis

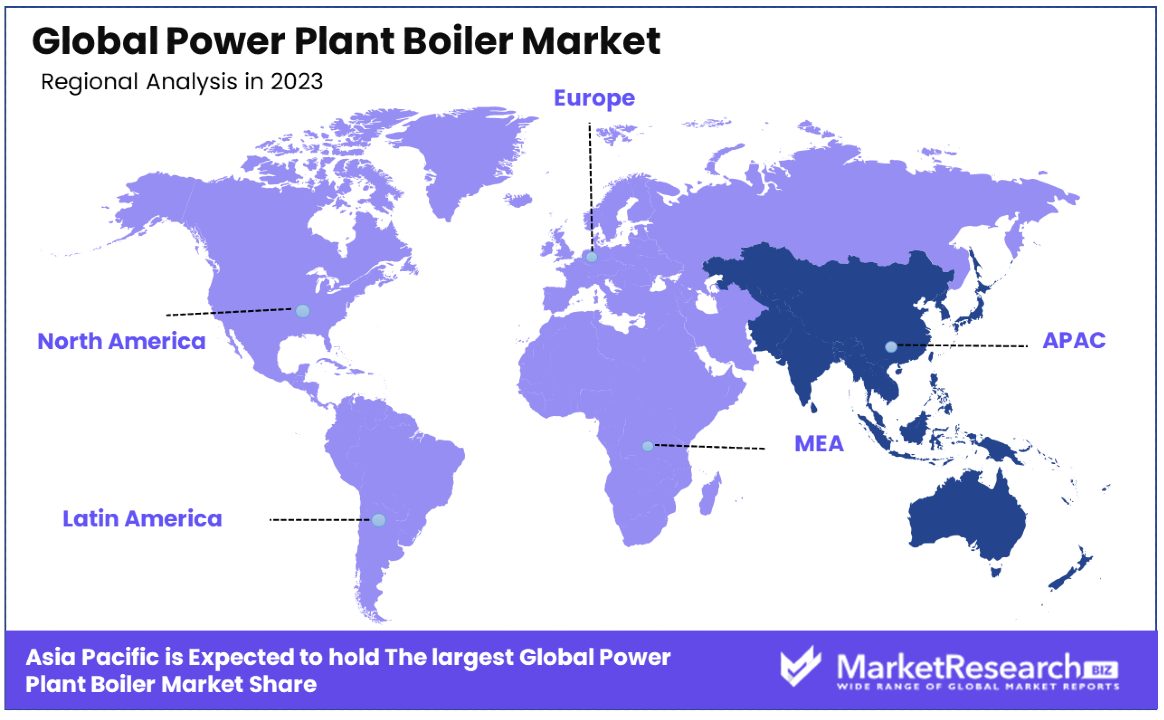

Asia Pacific Dominates with 37% Market Share

The Asia Pacific region holds a commanding 37% share of the Power Plant Boiler Market, a testament to its significant impact on the global energy landscape. This dominance is driven by rapid industrialization, urbanization, and an increasing demand for electricity in populous countries like China and India.

The region's commitment to expanding its energy infrastructure, alongside investments in both conventional and renewable energy sources, further contributes to its high market share. The Asia Pacific's diverse energy needs and the push towards reducing carbon emissions have also accelerated the adoption of advanced, efficient boiler technologies.

Several factors contribute to the Asia Pacific's dominance in the Power Plant Boiler Market. High population growth rates and economic expansion in countries within this region have led to a surge in energy demand. Furthermore, governments in the Asia Pacific are heavily investing in infrastructure development, including power generation, to support continued industrial growth and urbanization. The region's vast coal reserves have historically fueled its power sector, although there is now a significant shift towards cleaner and renewable energy sources to meet international environmental standards.

Regional Market Shares and Dynamics

- North America: Holding a market share of approximately 20%, North America's focus on modernizing aging infrastructure and integrating renewable energy sources contributes to its significant but smaller share compared to Asia Pacific. The region's stringent environmental regulations also drive the adoption of advanced boiler technologies.

- Europe: Europe accounts for about 25% of the market share, with a strong emphasis on sustainability and reducing carbon emissions. The region's advanced economies are investing in cleaner energy technologies and phasing out coal-fired power plants in favor of natural gas and renewables.

- Middle East & Africa: This region represents a smaller share of the market at around 10%. However, investments in infrastructure development and increasing access to electricity in African countries offer potential growth opportunities.

- Latin America: With a 8% market share, Latin America's power plant boiler market is influenced by increasing demand for electricity and investments in renewable energy sources, albeit from a smaller base compared to other regions.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Power Plant Boiler Market, key players like IHI Corporation, Siemens AG, Dongfang Electric Corporation Limited, and Harbin Electric Corporation lead the field, showcasing significant impact, strategic positioning, and market influence.

These major players, along with others like John Wood Group PLC, Alstom SA, and Bharat Heavy Electricals Limited, are pivotal in driving technological innovation and adoption across the market. Their strategic focus on developing efficient, environmentally friendly boiler technologies underscores the industry's shift towards sustainability and efficiency.

Companies such as Doosan Heavy Industries & Construction Co., Ltd., Siemens Energy, and Mitsubishi Hitachi Power Systems, Ltd. are notable for their contributions to the advancement of supercritical and ultra-supercritical boiler technologies, enhancing the market's overall efficiency and reducing carbon footprints.

Meanwhile, entities like ALFA LAVAL, Shanghai Electric, and Babcock & Wilcox Enterprises, Inc. offer specialized solutions that cater to the evolving needs of power plant operators worldwide, including retrofitting and upgrades for existing facilities. Collectively, these key players' efforts in research and development, global expansion, and collaboration with governments and private entities shape the competitive landscape and growth trajectory of the Power Plant Boiler Market.

Their roles in introducing cutting-edge technologies and engaging in strategic partnerships position them as leaders in addressing the pressing energy needs and environmental concerns of today's world.

Market Key Players

- IHI Corporation

- Siemens AG

- Dongfang Electric Corporation Limited

- Harbin Electric Corporation

- John Wood Group PLC

- Alstom SA

- Kawasaki Heavy Industries,

- Bharat Heavy Electricals Limited

- Doosan Heavy Industries & Construction Co., Ltd.

- Siemens Energy

- JFE Engineering Corporation

- Thermax Limited

- ALFA LAVAL

- Shanghai Electric

- Sofinter S.p.a

- Babcock & Wilcox Enterprises, Inc.

- Mitsubishi Hitachi Power Systems, Ltd.

- Sumitomo Heavy Industries, Ltd.

Recent Developments

- On Feb 2024, Wyoming's coal carbon capture mandate made legislative advances with Senate File 42 (SF 42) aiming to update a 2020 law, primarily to extend the compliance deadline of 2030 to allow carbon capture technologies to advance and attract private investors

- On Dec 2023, the Grant Town Power Plant in West Virginia initiated a three-year partnership with Gecko Robotics to leverage AI-powered technology aimed at outage prevention.

- On Nov 2023, JERA commenced the implementation of an AI-based boiler operation optimization system at a thermal power plant, envisioning a digital power plant that leverages digital transformation to create new value by integrating data about power plant facilities and personnel in real-time

- On March 2022, ANDRITZ successfully initiated the Carpe Futurum project at Vattenfall AB in Uppsala, Sweden, focusing on a biomass boiler plant. This endeavor signifies a significant step towards sustainable energy solutions and underscores the commitment of both ANDRITZ and Vattenfall to environmental initiatives in the energy sector.

Report Scope

Report Features Description Market Value (2023) USD 20.6 Billion Forecast Revenue (2033) USD 35.4 Billion CAGR (2024-2033) 5.70% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Fuel Type/Heat Source (Coal, Natural Gas, Nuclear Reactor, Petroleum, Others), By Material (Conventional Materials, Designed Materials), By Technology (Ultra-Critical, Super Critical, Subcritical, Advanced Ultra-Supercritical), By Process (Fluidized Bed Combustion, Pulverized Fuel Combustion), By Type (Pulverized Coal Tower Boiler, Circulating Fluidized Bed Boiler), By Capacity (Less than 400 MW, 400 MW to 800 MW, More than 800 MW) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape IHI Corporation, Siemens AG, Dongfang Electric Corporation Limited, Harbin Electric Corporation, John Wood Group PLC, Alstom SA, Kawasaki Heavy Industries,, Bharat Heavy Electricals Limited, Doosan Heavy Industries & Construction Co., Ltd., Siemens Energy, JFE Engineering Corporation, Thermax Limited, ALFA LAVAL, Shanghai Electric, Sofinter S.p.a, Babcock & Wilcox Enterprises, Inc., Mitsubishi Hitachi Power Systems, Ltd., Sumitomo Heavy Industries, Ltd., Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Siemens AG

- Mitsubishi Heavy Industries Ltd.

- Babcock & Wilcox Enterprises

- Dongfang Electric Corporation

- General Electric

- AMEC Foster Wheeler

- Doosan Heavy Industries & Construction

- IHI Corporation

- Bharat Heavy Electricals Ltd.

- Thermax Ltd.

Our Clients

View Our Licence Options