Noble Ferroalloys Market Report By Type of Ferroalloy (Ferrovanadium, Ferromolybdenum, Ferrotungsten, Ferroniobium, Ferrotitanium, Others), By Application (Steel Production, Alloy Production, Welding Electrodes, Superalloys, Chemical Industry, Others), By End User Industry (Automotive, Aerospace, Construction, Energy, Machinery, Electronics, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46688

-

May 2024

-

325

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

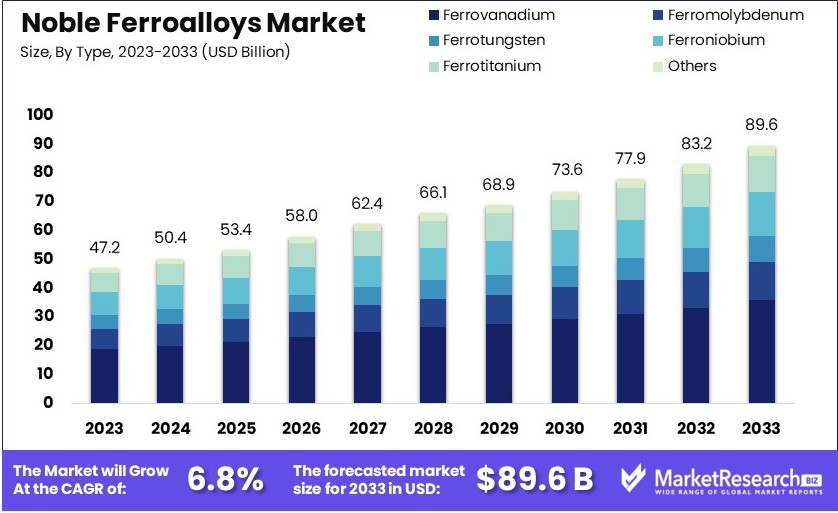

The Global Noble Ferroalloys Market size is expected to be worth around USD 89.6 Billion by 2033, from USD 47.2 Billion in 2023, growing at a CAGR of 6.8% during the forecast period from 2024 to 2033.

The Noble Ferroalloys Market includes high-quality alloys used in steelmaking and metallurgy. These alloys, like ferrochrome and ferromanganese, improve steel’s strength, durability, and resistance to corrosion. Key sectors using noble ferroalloys include construction, automotive, and manufacturing. The market's growth is driven by rising steel production and infrastructure development.

Innovations in alloy production and sustainable practices are also enhancing market dynamics. Major players invest in research to improve product quality and reduce costs. Overall, the noble ferroalloys market is crucial for advancing modern steel applications and supporting global industrial growth.

The Noble Ferroalloys Market is poised for significant growth, driven by the robust expansion of the construction industry and the increasing demand for steel. In 2022, global expenditure on construction activities surpassed $11 trillion, representing approximately 13% of the global GDP. This expenditure is projected to escalate to nearly $14.8 trillion by 2030, underscoring the critical role of construction in global economic development.

Notably, the construction sector is a substantial contributor to many countries' GDPs. For instance, in the United States, construction work valued at around $1.4 trillion was ongoing as of February 2020, with over $1 trillion attributed to the private sector.

Steel production, a key driver of the noble ferroalloys market, also exhibits strong growth trends. In 2020, global steel production reached 1,878 million tonnes, with the top 10 steel-producing countries contributing 86% of this output. By 2022, total world crude steel production had approached 1.9 billion tonnes, with China accounting for 54% of the global production. The European steel industry, with a turnover of approximately €130 billion, directly employed a significant workforce, reflecting its vital role in the region's economy. In the same year, the EU imported 28.9 million tonnes of finished steel products.

The increasing demand for high-quality steel, essential in various construction and industrial applications, is expected to drive the growth of the noble ferroalloys market. These alloys, which include elements like vanadium, tungsten, and molybdenum, enhance the strength, durability, and corrosion resistance of steel. As construction activities and steel production continue to rise globally, the demand for noble ferroalloys is anticipated to follow suit, presenting substantial growth opportunities for market participants.

Key Takeaways

- Market Value:The Global Noble Ferroalloys Market is expected to reach USD 89.6 billion by 2033, from USD 47.2 billion in 2023, growing at a CAGR of 6.8%.

- Type of Ferroalloy Analysis: Ferrovanadium dominates due to its crucial role in enhancing steel strength and hardness.

- Application Analysis: Steel production leads with the largest market share due to extensive use in enhancing steel properties.

- End User Industry Analysis: Construction industry dominates with the largest share due to high demand for durable and corrosion-resistant steel.

- Dominant Region: APAC dominates with 39.8% market share, driven by construction and automotive growth.

- High Growth Region: North America holds 25% market share, significant for advanced industrial applications.

- Analyst Viewpoint: The market exhibits strong growth with increasing demand in construction and automotive sectors, fostering competition.

- Growth Opportunities: Key players can leverage technological advancements and expanding applications in emerging markets to stand out.

Driving Factors

Increasing Demand from the Steel Industry Drives Market Growth

The steel industry is a primary consumer of noble ferroalloys like ferrosilicon, ferromanganese, and ferrochrome. These alloys enhance steel's properties, such as strength, hardness, and corrosion resistance. As global steel production rises, particularly in developing economies like China and India, the demand for noble ferroalloys grows correspondingly.

According to the World Steel Association, global crude steel production reached 1,950.5 million metric tons in 2022, with China contributing around 53% of the global output. This massive production volume underscores the critical role of noble ferroalloys in steel manufacturing. The ongoing urbanization and industrialization in these regions further fuel the steel industry's expansion. Consequently, the noble ferroalloys market is experiencing significant growth, driven by the increasing need for high-quality steel in various applications. This demand is likely to continue as these economies develop, ensuring steady market growth for noble ferroalloys.

Increasing Construction and Infrastructure Activities Drive Market Growth

The construction and infrastructure sectors are major consumers of steel and noble ferroalloys. Rapid urbanization and infrastructure projects in emerging economies drive the demand for these materials. For instance, India's National Infrastructure Pipeline envisions a $1.4 trillion investment in infrastructure projects between 2019 and 2025. Such large-scale projects significantly boost the demand for steel, and by extension, noble ferroalloys.

These alloys are essential in producing high-strength steel required for building bridges, roads, and buildings. As urban areas expand and new infrastructure is developed, the need for robust construction materials increases, leading to higher consumption of noble ferroalloys. This trend is particularly evident in regions undergoing significant development, where the construction boom directly translates into increased market growth for noble ferroalloys.

Technological Advancements Drive Market Growth

Technological advancements in ferroalloy production, such as the use of electric arc furnaces and energy-efficient processes, have improved product quality and reduced production costs. These developments make noble ferroalloys more accessible and cost-effective, driving their adoption across various industries. Improved production technologies enhance the efficiency of manufacturing processes, resulting in higher output and better-quality products.

This increased efficiency reduces costs and allows for competitive pricing, making noble ferroalloys more attractive to end-users. As industries seek cost-effective solutions without compromising quality, the adoption of technologically advanced ferroalloys rises. This trend supports the market's growth by meeting the demand for high-performance materials while maintaining economic feasibility.

Restraining Factors

High Production Costs Restrain Market Growth

The production of noble ferroalloys requires significant capital investments in equipment, energy, and raw materials. These high production costs can limit the profitability of ferroalloy producers, especially in regions with limited access to low-cost raw materials and energy sources. The need for expensive machinery and the consumption of large amounts of electricity contribute to these costs.

Additionally, fluctuations in the prices of raw materials like manganese, silicon, and chromium further impact production expenses. High operational costs can reduce profit margins and make it challenging for producers to compete, particularly against those in regions with cheaper resources. This financial strain can slow market expansion as companies struggle to maintain competitive pricing while covering production expenses.

Trade Tensions and Tariffs Restrain Market Growth

The noble ferroalloys market is global, involving producers and consumers across various regions. Trade tensions and tariffs imposed by different countries on ferroalloy imports can disrupt supply chains and affect market dynamics. For instance, ongoing trade tensions between the United States and China have led to tariffs on various steel and ferroalloy products.

These tariffs increase costs for importers, disrupt trade flows, and create uncertainty in pricing. Such trade barriers can hinder market growth by limiting the availability of noble ferroalloys in key markets and increasing costs for manufacturers and end-users. This disruption can cause volatility in the market, making it difficult for companies to plan and invest confidently in the sector.

Type of Ferroalloy Analysis

Ferrovanadium dominates with a significant market share due to its crucial role in enhancing steel strength and hardness.

The noble ferroalloys market is segmented into various types, including ferrovanadium, ferromolybdenum, ferrotungsten, ferroniobium, ferrotitanium, and others. Among these, ferrovanadium dominates with a significant market share. Ferrovanadium is crucial in enhancing the strength and hardness of steel, making it essential for high-strength low-alloy (HSLA) steels used in construction, automotive, and pipeline applications. The increasing demand for HSLA steels, particularly in emerging economies, drives the demand for ferrovanadium.

For example, the construction boom in China and India, coupled with their expanding automotive industries, significantly boosts ferrovanadium consumption. Additionally, ferrovanadium’s ability to improve the durability and corrosion resistance of steel makes it indispensable in various critical applications, thereby reinforcing its market dominance. Other segments, such as ferromolybdenum and ferrotungsten, also play vital roles in the industry. Ferromolybdenum is essential for producing stainless steel foil and alloy steels, enhancing their strength and corrosion resistance. This alloy is crucial in industries where durability and resistance to harsh environments are paramount, such as in the chemical and oil and gas industries.

Ferrotungsten, known for its high melting point and hardness, is vital in manufacturing cutting tools and wear-resistant materials. These applications drive the demand for ferrotungsten, although its market share is smaller compared to ferrovanadium. Ferroniobium and ferrotitanium are also important but serve more niche markets, contributing to specialized steel and alloy productions. The demand for these ferroalloys is growing, driven by advancements in technology and the need for high-performance materials in various industrial applications.

Application Analysis

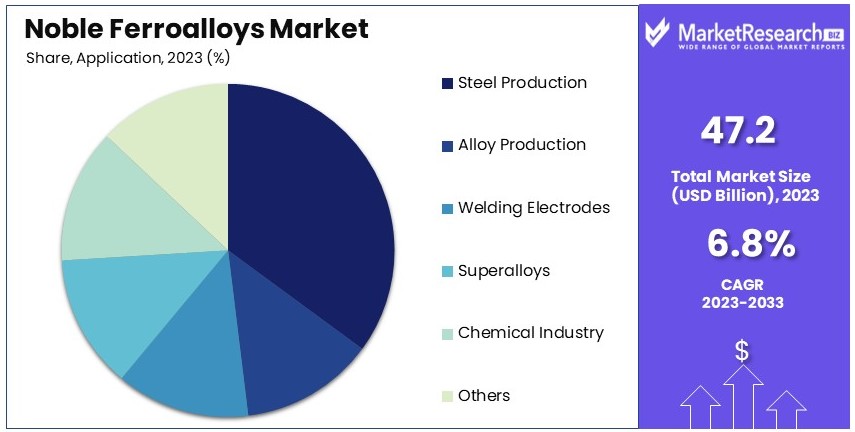

Steel production dominates with the largest market share due to the extensive use of noble ferroalloys in enhancing steel properties.

In the noble ferroalloys market, the application segment includes steel production, alloy production, welding electrodes, superalloys, chemical industry, and others. Steel production is the dominant application, accounting for the largest market share. Noble ferroalloys like ferrovanadium, ferromolybdenum, and ferrotungsten are essential in steelmaking due to their ability to enhance the mechanical properties of steel.

As global steel production continues to rise, driven by infrastructure development and industrialization, the demand for noble ferroalloys in steel production is expected to grow. According to the World Steel Association, global crude steel production reached 1,950.5 million metric tons in 2022, highlighting the immense scale of this segment. Alloy production is another critical application, where noble ferroalloys are used to produce various high-performance alloys. These alloys are essential in industries requiring materials with exceptional strength, heat resistance, and corrosion resistance, such as aerospace and automotive.

Welding electrodes and superalloys are specialized applications that also contribute to market growth. Welding electrodes containing noble ferroalloys are vital for producing high-quality welds in construction and manufacturing. Superalloys, which incorporate noble ferroalloys, are crucial in high-temperature applications, particularly in the aerospace and power generation sectors. The chemical industry, while a smaller segment, utilizes noble ferroalloys for their catalytic properties and in the production of specialized chemicals. Overall, each application segment plays a significant role in driving the noble ferroalloys market, with steel production leading the charge due to its extensive and varied uses across multiple industries.

End User Industry Analysis

Construction industry dominates with the largest share due to high demand for durable and corrosion-resistant steel.

The noble ferroalloys market is segmented by end-user industries, including automotive, aerospace, construction, energy, machinery, electronics, and others. The construction industry is the dominant end-user, driving the largest share of the market. Noble ferroalloys are essential in producing high-strength and corrosion-resistant steel used in construction. The ongoing urbanization and infrastructure development in emerging economies, such as China's Belt and Road Initiative and India's Smart Cities Mission, significantly boost the demand for noble ferroalloys in the construction sector.

The automotive industry is another major consumer of noble ferroalloys, utilizing them in the production of high-strength steel and specialized alloys for vehicle manufacturing. As the automotive industry shifts towards lighter and stronger materials to improve fuel efficiency and safety, the demand for noble ferroalloys is expected to grow. The aerospace industry also significantly contributes to the market, using noble ferroalloys in the production of superalloys for aircraft engines and components that require exceptional strength and heat resistance.

The energy sector, particularly in renewable energy and oil and gas, relies on noble ferroalloys for producing durable and high-performance materials needed for energy infrastructure. Machinery and electronics industries, while smaller segments, also use noble ferroalloys in various applications, contributing to overall market growth. Each of these end-user industries drives the demand for noble ferroalloys, with the construction industry leading due to the extensive use of steel in infrastructure projects.

Key Market Segments

By Type of Ferroalloy

- Ferrovanadium

- Ferromolybdenum

- Ferrotungsten

- Ferroniobium

- Ferrotitanium

- Others

By Application

- Steel Production

- Alloy Production

- Welding Electrodes

- Superalloys

- Chemical Industry

- Others

By End User Industry

- Automotive

- Aerospace

- Construction

- Energy

- Machinery

- Electronics

- Others

Growth Opportunities

Increasing Demand for High-Grade Steel Offers Growth Opportunity

The demand for high-grade steel is rising due to its strength, durability, and performance in industries like automotive, construction, and machinery. Noble ferroalloys are crucial in producing high-grade steel by enhancing properties like strength, hardness, and corrosion resistance.

The automotive industry's need for lightweight, high-strength steel for better fuel efficiency and safety is driving the demand for ferroalloys like ferrochrome and ferromanganese. For instance, the global push towards electric vehicles and more stringent fuel efficiency standards in traditional vehicles are significant drivers. This trend presents a substantial growth opportunity for noble ferroalloy producers, enabling them to capitalize on the increasing need for superior steel products in various applications.

Expansion into Emerging Markets Offers Growth Opportunity

Emerging economies in Asia, Africa, and Latin America are rapidly industrializing and urbanizing, leading to higher demand for steel and related products. These regions offer significant growth opportunities for noble ferroalloy producers. In India, for example, ambitious infrastructure development plans and a growing construction sector are driving demand for noble ferroalloys like ferrosilicon and ferromanganese.

The National Infrastructure Pipeline in India, which envisions substantial investments, highlights this potential. As these economies expand, noble ferroalloy producers can tap into the burgeoning steel production and construction activities, ensuring sustained market growth.

Trending Factors

Sustainability and Environmental Considerations Are Trending Factors

Environmental concerns and stricter regulations are driving the trend towards sustainable and eco-friendly production processes in the noble ferroalloys industry. Producers are focusing on reducing emissions, optimizing energy consumption, and smart waste management. Regulatory pressures, consumer demands, and industry efforts to reduce environmental footprints are fueling this trend.

The adoption of electric arc furnaces and energy-efficient technologies in ferroalloy production is becoming more prevalent. These advancements not only comply with environmental standards but also reduce production costs, thereby enhancing market appeal and positioning noble ferroalloy producers as environmentally responsible and economically efficient.

Vertical Integration and Consolidation Are Trending Factors

Vertical integration and consolidation are trending in the noble ferroalloys market as companies aim to enhance supply chain efficiency, reduce costs, and gain a competitive edge. Major steel producers are acquiring or partnering with ferroalloy producers to secure a stable supply of raw materials. Mergers and acquisitions among ferroalloy producers are also occurring to achieve economies of scale and expand market reach.

For instance, ArcelorMittal's acquisition of a majority stake in Sideralba in 2021 exemplifies this trend. These strategic moves help companies streamline operations, improve profitability, and strengthen their market position, making vertical integration and consolidation critical trends in the noble ferroalloys industry.

Regional Analysis

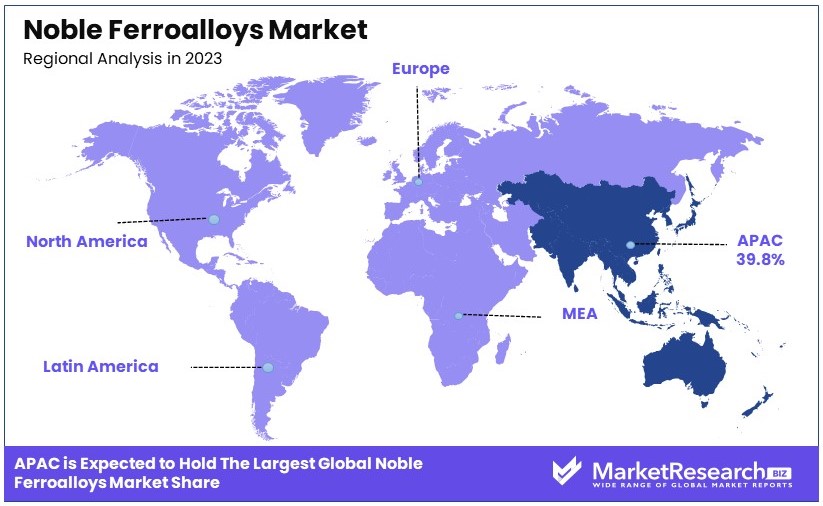

APAC Dominates with 39.8% Market Share

APAC's dominance in the noble ferroalloys market is driven by rapid industrialization and urbanization. Major economies like China and India lead in steel production, which heavily relies on noble ferroalloys. For instance, China alone accounted for 53% of global crude steel production in 2022. The region's robust infrastructure projects and growing automotive industry further fuel demand.

Regional characteristics such as abundant raw materials and lower production costs enhance market performance. APAC's favorable government policies and significant investments in infrastructure projects also play a crucial role. For example, India's National Infrastructure Pipeline envisions a $1.4 trillion investment, boosting steel and ferroalloy demand.

APAC's market presence is expected to grow, driven by continued industrial expansion and urbanization. The increasing adoption of advanced production technologies will also enhance market growth. By 2025, APAC is projected to maintain its leading position with a steady increase in market share.

North America Holds 25% Market Share

North America holds a 25% market share in the noble ferroalloys market. The region benefits from advanced technological infrastructure and a strong automotive sector. The U.S. and Canada are key players, with significant investments in high-grade steel production. North America's focus on innovation and sustainability will continue to drive market growth.

Europe Accounts for 20% Market Share

Europe accounts for 20% of the noble ferroalloys market. The region's emphasis on sustainable and eco-friendly production methods drives demand. Germany and France lead in automotive and machinery manufacturing, which boosts the need for high-quality steel and ferroalloys. Europe's commitment to green technologies will support steady market growth.

Middle East & Africa Holds 10% Market Share

The Middle East & Africa region holds a 10% market share. This region's market is driven by ongoing infrastructure projects and urbanization efforts, particularly in Gulf countries. The construction boom and industrial developments in these areas contribute significantly to the demand for noble ferroalloys.

Latin America Accounts for 5.2% Market Share

Latin America accounts for 5.2% of the noble ferroalloys market. Brazil is a key player, with its growing steel industry and expanding construction sector. The region's focus on industrialization and infrastructure development will continue to foster market growth in the coming years.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Noble Ferroalloys market features a diverse array of influential companies that significantly shape industry dynamics. Notable among these are Eurasian Resources Group (ERG), Glencore plc, and China Minmetals Corporation, each holding substantial global footprints and extensive resource control. These entities excel in production capabilities and distribution networks, enhancing their market leverage.

Samancor Chrome, Tata Steel, and Jindal Stainless Limited stand out for their vertical integration strategies, controlling both raw material sourcing and end-product manufacturing. This integration not only stabilizes their supply chains but also allows for aggressive market positioning in response to industry demands.

Firms like OM Holdings Ltd., Sakura Ferroalloys, and Ferroglobe are pivotal in specialized product segments, offering customized solutions that cater to specific industry needs. Their focus on niche markets provides them with a competitive edge, particularly in regions with unique market requirements.

Additionally, Erdos Group and Henan Xibao Metallurgy Group Co., Ltd. are key players in the Chinese market, the largest consumer of noble ferroalloys. Their strategic positioning within China supports their influence over pricing and market trends, impacting global market dynamics.

Smaller, yet significant players such as Votorantim Metais, Hindustan Ferro Alloy Industries, Gulf Ferro Alloys Company (SABAYEK), and Yildirim Group contribute to the market by fulfilling regional demand and specializing in specific types of ferroalloys.

Collectively, these companies drive the noble ferroalloys market through strategic resource management, innovative production techniques, and adaptive market strategies, maintaining robustness in the face of fluctuating economic and industrial conditions. Their roles are crucial in setting industry standards and directing future market trajectories.

Market Key Players

- Eurasian Resources Group (ERG)

- Glencore plc

- Samancor Chrome

- Tata Steel

- Erdos Group

- Henan Xibao Metallurgy Group Co., Ltd.

- Jindal Stainless Limited

- OM Holdings Ltd.

- Sakura Ferroalloys

- Ferroglobe

- China Minmetals Corporation

- Votorantim Metais

- Hindustan Ferro Alloy Industries

- Gulf Ferro Alloys Company (SABAYEK)

- Yildirim Group

Recent Developments

- Expected on November 2024: Fastmarkets 40th International Ferroalloys 2024 in Istanbul, Turkey, will host Europe's largest gathering of ferroalloys traders, featuring extensive networking opportunities and key industry representatives from major international steel mills.

- April 2024: India's Ministry of Steel mandates BIS certification for ferroalloys, including ferrosilicon, ferrochrome, ferromanganese, and silicomanganese, to enhance quality, safety, and reliability for imports and domestic sales.

- March 11, 2024: The ferro-alloys sector in China showed a muted response to the 2024 economic targets announced at the Two Sessions conference, with key prices in ferro-silicon, tungsten, and vanadium fluctuating modestly.

- February 1, 2024: Indian Metals & Ferro Alloys Q3 FY24 results: Profit surged 899.91% YoY, revenue up 9.89% YoY, and EPS increased by 535.81% YoY. Operating income rose 497.01% YoY.

Report Scope

Report Features Description Market Value (2023) USD 47.2 Billion Forecast Revenue (2033) USD 89.6 Billion CAGR (2024-2033) 6.8% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type of Ferroalloy (Ferrovanadium, Ferromolybdenum, Ferrotungsten, Ferroniobium, Ferrotitanium, Others), By Application (Steel Production, Alloy Production, Welding Electrodes, Superalloys, Chemical Industry, Others), By End User Industry (Automotive, Aerospace, Construction, Energy, Machinery, Electronics, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Eurasian Resources Group (ERG), Glencore plc, Samancor Chrome, Tata Steel, Erdos Group, Henan Xibao Metallurgy Group Co., Ltd., Jindal Stainless Limited, OM Holdings Ltd., Sakura Ferroalloys, Ferroglobe, China Minmetals Corporation, Votorantim Metais, Hindustan Ferro Alloy Industries, Gulf Ferro Alloys Company (SABAYEK), Yildirim Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Eurasian Resources Group (ERG)

- Glencore plc

- Samancor Chrome

- Tata Steel

- Erdos Group

- Henan Xibao Metallurgy Group Co., Ltd.

- Jindal Stainless Limited

- OM Holdings Ltd.

- Sakura Ferroalloys

- Ferroglobe

- China Minmetals Corporation

- Votorantim Metais

- Hindustan Ferro Alloy Industries

- Gulf Ferro Alloys Company (SABAYEK)

- Yildirim Group

Our Clients

View Our Licence Options