Global Stainless Steel Foil Market By Product Type(Type 200, Type 300, Type 400, Others), By Thickness(Up to 0.025 mm, 025-0.1 mm, 1-0.2 mm, Above 0.2 mm), By End-Use(Electronics, Automotive, Aerospace, Pharmaceutical, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

45342

-

May 2024

-

300

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

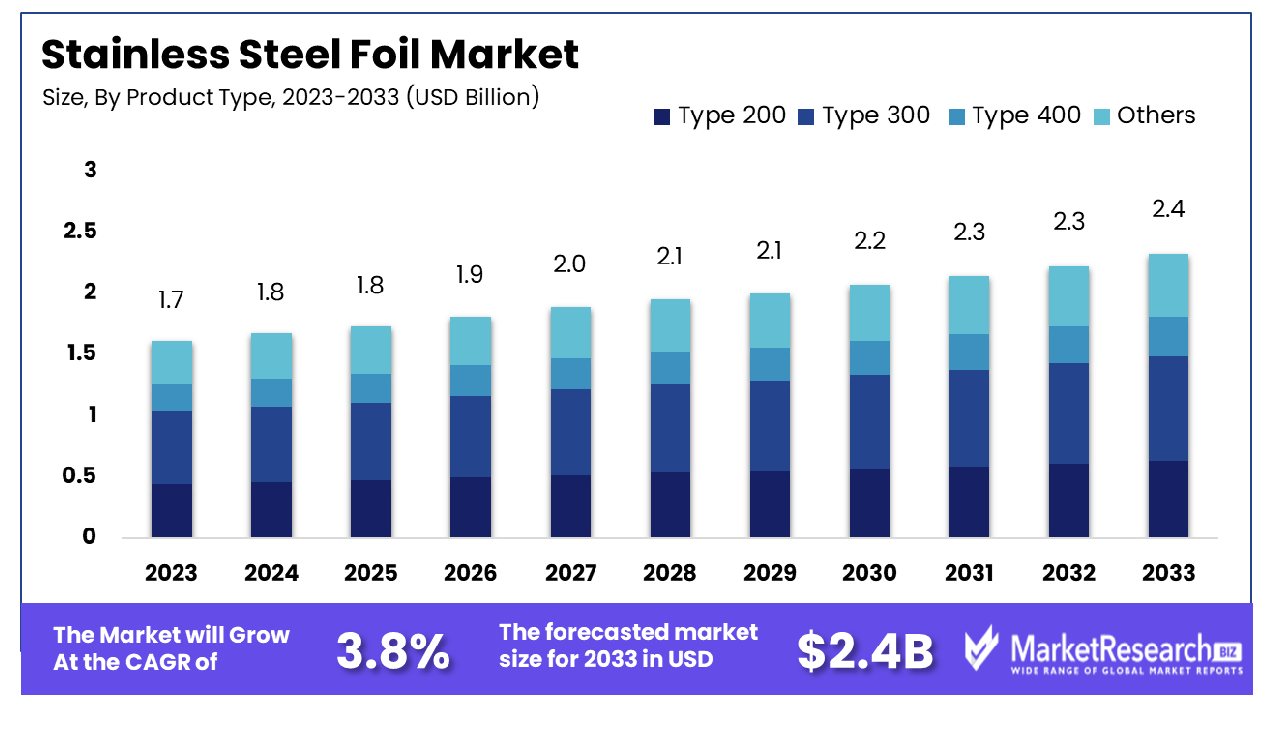

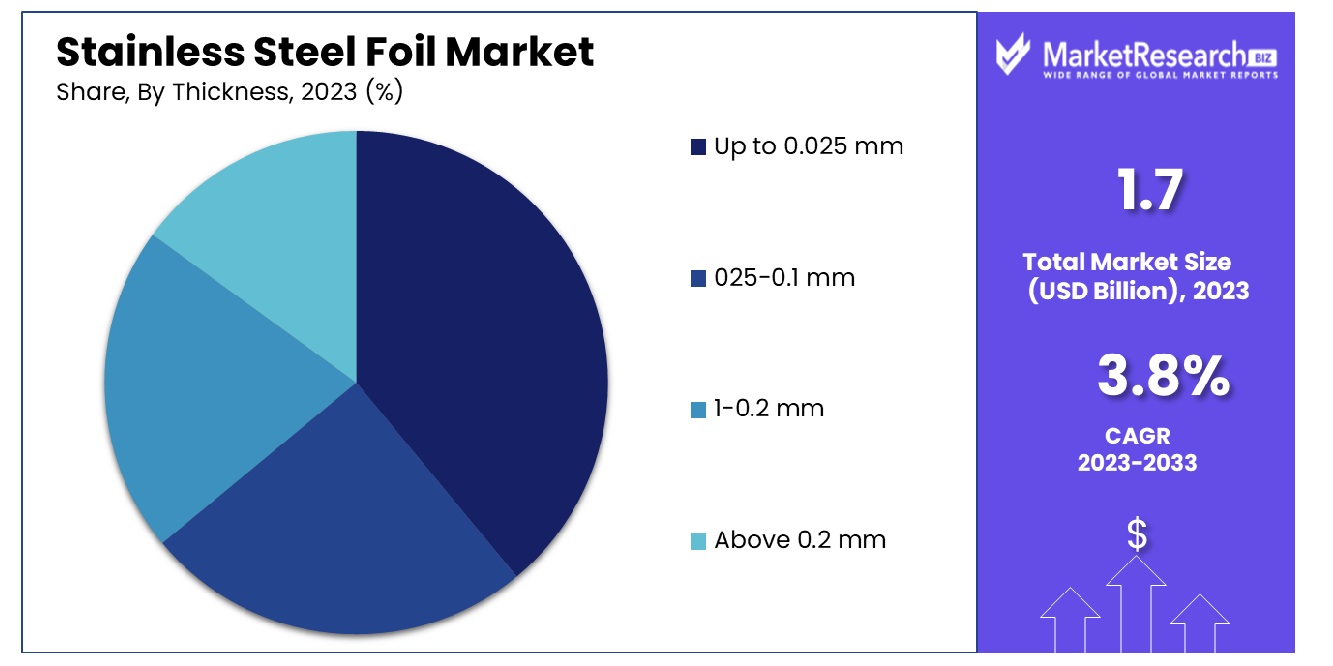

The Global Stainless Steel Foil Market was valued at USD 1.7 billion in 2023. It is expected to reach USD 2.4 billion by 2033, with a CAGR of 3.8% during the forecast period from 2024 to 2033.

The Stainless Steel Foil Market encompasses producing, distributing, and applyingultra-thin stainless steel strips, typically less than 0.2 mm in thickness. Renowned for its strength, corrosion resistance, and thermal conductivity, this foil is integral in various industries, including automotive, aerospace, electronics, and medical devices.

As businesses strive for efficiency and innovation, the demand for durable and lightweight materials drives the market. Strategic insights into the market focus on supply chain dynamics, technological advancements, and regulatory impacts, providing executives and product managers with critical data to navigate market challenges and leverage growth opportunities.

The global market for stainless steel foil is characterized by its critical role in various industrial applications, including electronics, automotive, and aerospace sectors. The unique properties of stainless steel foil, such as corrosion resistance, heat tolerance, and durability, drive its demand across these industries. The market is influenced by trends in these sectors, with a notable emphasis on sustainable and efficient manufacturing processes.

Furthermore, the increasing adoption of electric vehicles and the expansion of telecommunications infrastructure are anticipated to propel the demand for stainless steel foil. However, the market faces challenges such as fluctuating raw material costs and the need for continuous technological advancements to enhance product features and production methods.

The comparative analysis with aluminum foil, another significant segment in the metal foil market, reveals insightful trends. In 2021, aluminum foil ranked as the world's 255th most traded product, amassing a total trade of $15.9 billion, underscoring its substantial economic impact. Additionally, deliveries from European aluminum rollers experienced a decline of 3.3% in Q1 2023 compared to the previous year, totaling 231,700 tonnes.

This slight decrease from pre-pandemic levels indicates resilience in the market, which could have indirect implications for the stainless steel foil sector, particularly in terms of competitive dynamics and material substitution trends.

Key Takeaways

- Market Growth: The Global Stainless Steel Foil Market was valued at USD 1.7 billion in 2023. It is expected to reach USD 2.4 billion by 2033, with a CAGR of 3.8% during the forecast period from 2024 to 2033.

- By Product Type: Type 300 stainless steel foil accounted for 65% of the market share.

- By Thickness: In terms of thickness, foils up to 0.025 mm thick dominated, capturing 75% of the market.

- By End-Use: In the electronics sector, this type of foil was the most used, representing 40% of end-use.

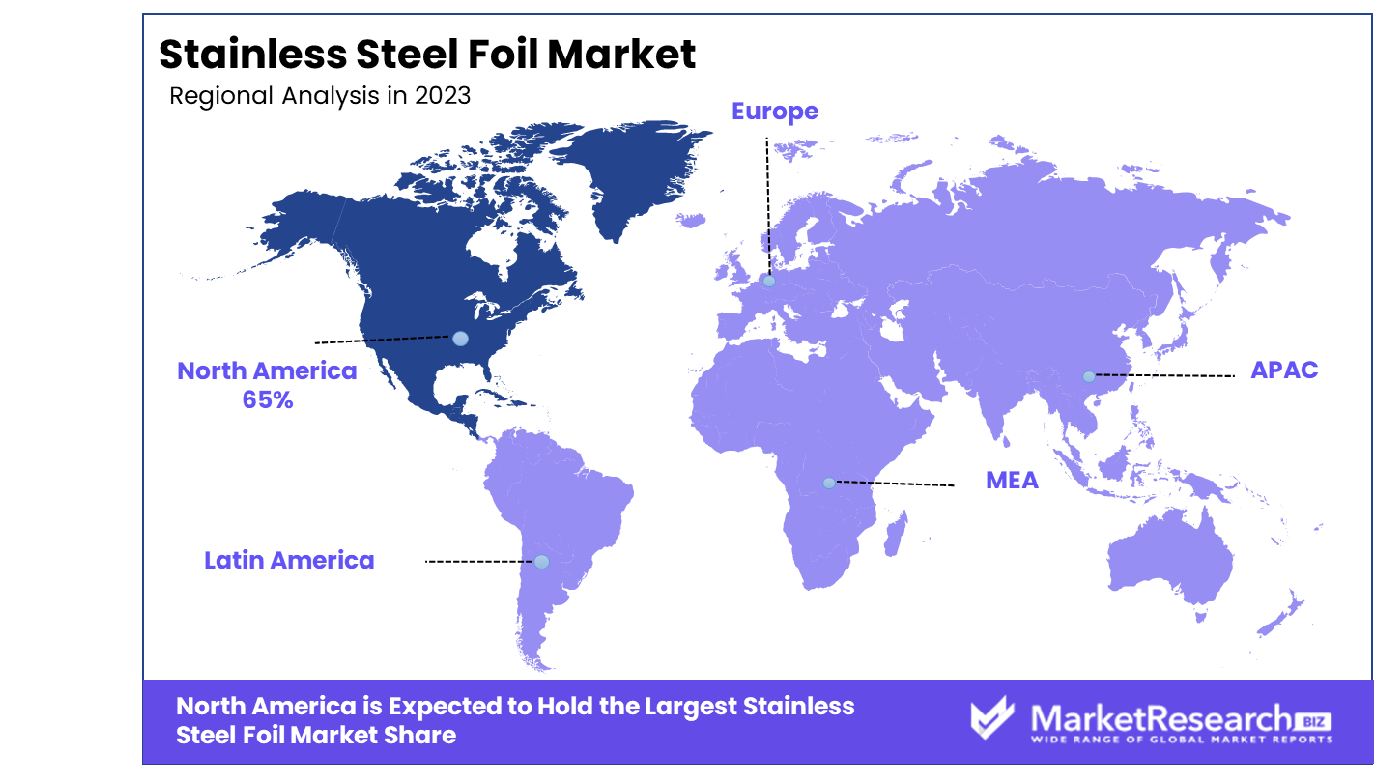

- Regional Dominance: North America holds 65% of the global stainless steel foil market.

- Growth Opportunity: In 2023, the global stainless steel foil market grew through advanced production techniques and strategic collaborations, enhancing product quality and expanding international business opportunities.

Driving factors

Enhanced Market Prospects Driven by Corrosion Resistance in Critical Industries

The Stainless Steel Foil Market is experiencing significant growth, primarily fueled by the escalating demand for corrosion-resistant metal packaging. Industries such as food, chemical, and pharmaceutical rely on stainless steel foil to ensure product integrity and extend shelf life.

This metal's inherent resistance to oxidation and degradation not only preserves contents but also supports industry compliance with stringent health and safety regulations. This factor alone substantially broadens the market scope of stainless steel foils, as these industries continually expand and evolve in response to consumer needs and regulatory standards.

Diverse Industrial Applications Propel Market Expansion

Stainless steel foil serves a vital role across a multitude of sectors including automotive, electrical and electronics, building and construction, and various industrial applications. In the automotive sector, its usage in parts that require excellent thermal and electrical conductivity—such as gaskets and heat shields—demonstrates its versatility and essential function.

Similarly, in the electronics industry, stainless steel foil is indispensable for its effectiveness in electromagnetic shielding and thermal management. The building and construction industry further leverages this material for its durability and aesthetic qualities, making it a preferred choice for both structural and design elements. These widespread applications underscore the material’s utility and contribute robustly to the market’s growth trajectory.

Technological Advancements in Manufacturing Enhance Product Appeal

Significant advancements in the manufacturing processes of stainless steel foils have led to improvements in surface quality, dimensional accuracy, and mechanical properties. These enhancements not only meet the increasingly stringent specifications required by high-performance applications but also elevate the overall quality of the end products.

As manufacturers continue to innovate and refine these processes, the performance parameters of stainless steel foils are pushed to new heights, thereby enhancing their attractiveness to industries requiring precision and reliability. This ongoing improvement in product quality directly correlates with increased market penetration and customer satisfaction, further driving the market’s expansion.

Restraining Factors

Health Concerns Impede Market Acceptance

Health concerns associated with the excessive use of stainless steel foil, particularly in snack food packaging and cooking applications, pose a significant restraint on the market’s growth. Consumers and regulatory bodies are increasingly wary of the potential for heavy metal leaching into food, which can occur with certain grades of stainless steel under specific conditions.

These health concerns can lead to stricter regulations and a shift in consumer preferences towards alternatives perceived as safer, such as glass or aluminum foil. This shift not only affects the demand in the consumer market but also pressures manufacturers to innovate safer and more compliant products, which could increase production costs and impact profitability.

Supply Chain Disruptions Curb Market Stability

The availability of raw materials necessary for the production of stainless steel foil significantly influences market dynamics. Factors such as geopolitical tensions, trade disputes, and unforeseen global events can lead to disruptions in the supply chain, resulting in raw material shortages and subsequent price volatility.

This volatility can deter investment and expansion plans, as manufacturers and end-users grapple with fluctuating costs and supply uncertainty. The lack of predictability in pricing and availability of raw materials not only hampers operational planning but also poses a substantial barrier to market growth, affecting the stability of the stainless steel foil industry.

By Product Type Analysis

Type 300 dominated the market with a commanding 65% share.

In 2023, Type 300 held a dominant market position in the By Product Type segment of the Stainless Steel Foil Market, capturing more than a 65% share. This segment outperformed other categories such as Type 200, Type 400, and Others, which collectively accounted for the remaining market share.

The robust performance of Type 300 can be attributed to its superior corrosion resistance and heat resistance properties, making it highly sought after in various industrial applications including chemical processing, aerospace, and automotive sectors.

Type 200, though possessing lower nickel content and therefore more cost-effective, garnered a smaller portion of the market due to its relatively inferior mechanical properties and corrosion resistance compared to Type 300. Type 400, characterized by its magnetic qualities and higher carbon content, found niche applications in fields requiring high strength and durability at elevated temperatures, contributing marginally to the overall market composition.

The 'Others' category, comprising specialized stainless steel grades, captured the smallest market share, utilized in specific applications that demand unique properties not typically provided by the standard types.

By Thickness Analysis

Products up to 0.025 mm led, securing a substantial 75% of the market.

In 2023, the "Up to 0.025 mm" category held a dominant market position in the By Thickness segment of the Stainless Steel Foil Market, capturing more than a 75% share. This segment significantly outpaced other thickness ranges, such as 0.025-0.1 mm, 0.1-0.2 mm, and Above 0.2 mm, which collectively accounted for the remaining portion of the market. The predominant use of ultra-thin foils in high-precision applications across electronics, medical, and automotive industries underscores this dominance.

The "0.025-0.1 mm" range, while offering slightly thicker options suitable for robust applications, attracted a moderate market share, utilized primarily in components requiring higher strength and durability. Meanwhile, the "0.1-0.2 mm" thickness range found its niche in industrial and construction applications, benefiting from a balance of flexibility and structural integrity.

The thickest category, "Above 0.2 mm," held the smallest market share. This category is typically designated for specialized industrial applications where higher thickness and strength are paramount, such as in parts and components that must withstand extreme conditions.

The overwhelming preference for the "Up to 0.025 mm" thickness can be attributed to the critical need for material efficiency and precision in manufacturing processes, particularly in technologically advanced sectors. As industries continue to evolve towards more sophisticated manufacturing techniques and higher quality standards, the demand for ultra-thin stainless steel foils is anticipated to remain robust, further influencing the strategic focus and development within this market segment.

By End-Use Analysis

In the electronics sector, this category claimed a significant 40% of the end-use market share.

In 2023, Electronics held a dominant market position in the By End-Use segment of the Stainless Steel Foil Market, capturing more than a 40% share. This segment outperformed other sectors such as Automotive, Aerospace, Pharmaceutical, and Others, which collectively rounded out the remainder of the market.

The substantial share held by Electronics can be attributed to the extensive utilization of stainless steel foils in various components and assemblies where high conductivity, durability, and corrosion resistance are required.

The Automotive sector, leveraging stainless steel foils for their thermal and electrical properties, secured a significant portion of the market. These foils are critical in applications ranging from battery solutions to decorative trim, underscoring the sector's diverse needs.

Aerospace followed, with a focus on the high-strength, lightweight characteristics of stainless steel foils that are essential for both structural and engine components. This industry’s rigorous standards for performance and safety further fuel the demand for high-quality stainless steel materials.

The Pharmaceutical industry also made notable use of these foils, primarily for their chemical stability and non-reactive properties, which are crucial in environments where contamination must be strictly controlled.

The 'Others' category, encompassing a variety of industries including construction and consumer goods, utilized stainless steel foils to a lesser extent, driven by specific application needs that require the unique attributes of stainless steel.

Key Market Segments

By Product Type

- Type 200

- Type 300

- Type 400

- Others

By Thickness

- Up to 0.025 mm

- 025-0.1 mm

- 1-0.2 mm

- Above 0.2 mm

By End-Use

- Electronics

- Automotive

- Aerospace

- Pharmaceutical

- Others

Growth Opportunity

Development of High-Quality Stainless Steel Foils

In 2023, the global market for stainless steel foils has witnessed significant growth opportunities, primarily driven by technological advancements in the production process. The development of high-quality stainless steel foils, characterized by precise thickness control and enhanced surface characteristics, has been pivotal. Such advancements have enabled manufacturers to cater to the stringent requirements of various end-use industries, including electronics, automotive, and aerospace.

The improved product quality has not only enhanced the performance attributes of these foils but also extended their applicability, thereby broadening the market scope. This technological progression is attributed to increased R&D investments and the integration of modern manufacturing techniques, which have collectively elevated the standard of the final product.

Collaboration Activities Between Companies

Strategic collaborations have emerged as a key trend among major companies operating in the stainless steel foil market in 2023. These partnerships aim to leverage mutual strengths to enhance business operations, expand geographic footprints, and accelerate entry into new markets. By combining resources, companies are better positioned to optimize production capabilities and achieve cost efficiencies, which are crucial in maintaining competitiveness in the global market.

Furthermore, such collaborations often lead to innovation, as companies bring together diverse expertise to develop new applications for stainless steel foils. The international expansion through collaborative ventures not only diversifies business risks but also enhances the visibility and accessibility of products across different regions, thereby driving market growth.

Latest Trends

Rise in Demand for Exhaust Systems in the Automotive Industry

The global stainless steel foil market has experienced significant growth in 2023, largely fueled by the escalating demand for exhaust systems in the automotive industry. As environmental regulations become stricter and the push for more fuel-efficient vehicles intensifies, automotive manufacturers are increasingly incorporating stainless steel foils into exhaust system designs.

These foils are prized for their ability to withstand high temperatures and corrosive environments, which are typical in exhaust applications. The enhanced durability and performance characteristics of stainless steel foils not only meet the stringent standards set by regulatory bodies but also contribute to the overall efficiency and longevity of vehicle exhaust systems. This trend is expected to continue driving market expansion as the automotive sector seeks innovative solutions to meet environmental challenges.

Surge in Demand for Corrosion-Resistant Materials

Another key trend observed in 2023 is the surge in demand for corrosion-resistant materials, further propelling the stainless steel foil market. Industries such as chemical processing, oil and gas, and marine are increasingly relying on stainless steel foils to prevent the detrimental effects of exposure to harsh environments. The inherent properties of stainless steel, including its resistance to oxidation and corrosion, make it an ideal choice for these applications.

The market has seen a notable increase in the adoption of high-grade stainless steel foils designed to provide long-term protection against corrosion, thereby ensuring the safety, reliability, and durability of various industrial components. This rising demand underscores the material's critical role in operational sustainability and efficiency across multiple sectors.

Regional Analysis

North America dominates with 65% of the global stainless steel foil market share.

In North America, the market is notably robust, accounting for approximately 65% of the global demand. This dominance is largely driven by extensive utilization in automotive, aerospace, and food processing industries, where high-grade stainless steel foil is prized for its strength, corrosion resistance, and thermal conductivity. The United States leads in consumption within the region, buoyed by stringent environmental regulations and a strong presence of manufacturing facilities requiring advanced materials for high-performance applications.

Europe follows, with a focus on sustainability and energy efficiency driving demand for stainless steel foil in renewable energy projects, particularly solar energy applications. Germany, Italy, and France are key contributors, leveraging their technological prowess to enhance product quality and application scope. The region's emphasis on recycling and reducing carbon footprints also propels the adoption of stainless steel foil in new green projects.

Asia Pacific is identified as a rapidly growing market, spurred by industrial growth in China, India, and Southeast Asia. These countries benefit from escalating infrastructure projects and expanding automotive production. The region's competitive manufacturing costs and escalating demand for consumer electronics, where stainless steel foil is used for electromagnetic shielding, furbolsterslster the market.

Meanwhile, the Middle East &, Africa and Latin America are emerging as potential growth areas. Investments in infrastructure and increased industrialization, particularly in GCC countries and Brazil, respectively, are creating new opportunities for the deployment of stainless steel foil in various applications, including construction and petrochemicals.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Resthe t of Middle East & Africa

Key Players Analysis

In the global stainless steel foil market, several key players are shaping industry dynamics in 2023. ArcelorMittal continues to leverage its extensive infrastructure and production capacity to meet diverse global demands. Similarly, Outokumpu, known for its high-quality stainless steel, focuses on sustainability and efficiency in manufacturing industry processes, appealing to environmentally conscious markets.

UACJ Corporation and Allegheny Technologies Incorporated are noteworthy for their specialized products in high-performance alloys and precision rolling capabilities, respectively. These attributes cater to niche applications in aerospace industry and medical industries, where exacting standards are paramount. Jindal Stainless Limited's strategic positioning in emerging markets helps it exploit regional growth opportunities, particularly in Asia.

Aperam Stainless distinguishes itself with a robust product portfolio that includes both austenitic and martensitic stainless steel foils. This diversity enables Aperam to serve a broad spectrum of industries, from automotive to consumer goods. Nippon Steel Corporation, with its advanced research and development capabilities, remains a leader in innovation, pushing the boundaries of what can be achieved with stainless steel in terms of strength and durability.

Precision Strip Inc. excels in providing custom solutions and precision slitting, addressing the high-precision requirements of clients. ThyssenKrupp AG's integrated business model ensures consistency and quality control from raw material sourcing to finished products, enhancing its competitiveness in the global market.

Market Key Players

- ArcelorMittal

- Outokumpu

- UACJ Corporation

- Allegheny Technologies Incorporated

- Jindal Stainless Limited

- Aperam Stainless

- Nippon Steel Corporation

- Precision Strip Inc.

- ThyssenKrupp AG

- Poongsan Corporation

Recent Development

- In December 2023, Tsingtuo Group, a Chinese company, successfully produced the world's thinnest stainless steel foil, boosting China's domestic high-end steel foil production capabilities.

- In May 2022, Shanxi Taigang Stainless Steel Precision Strip Co., Ltd., a subsidiary of China Baowu, has tripled its production and sales of "hand-torn steel," enhancing its aerospace and electronics applications.

Report Scope

Report Features Description Market Value (2023) USD 1.7 Billion Forecast Revenue (2033) USD 2.4 Billion CAGR (2024-2032) 3.8% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type(Type 200, Type 300, Type 400, Others), By Thickness(Up to 0.025 mm, 025-0.1 mm, 1-0.2 mm, Above 0.2 mm), By End-Use(Electronics, Automotive, Aerospace, Pharmaceutical, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape ArcelorMittal, Outokumpu, UACJ Corporation, Allegheny Technologies Incorporated, Jindal Stainless Limited, Aperam Stainless, Nippon Steel Corporation, Precision Strip Inc., ThyssenKrupp AG, Poongsan Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- ArcelorMittal

- Outokumpu

- UACJ Corporation

- Allegheny Technologies Incorporated

- Jindal Stainless Limited

- Aperam Stainless

- Nippon Steel Corporation

- Precision Strip Inc.

- ThyssenKrupp AG

- Poongsan Corporation

Our Clients

View Our Licence Options