MOCVD Market By Type (GaN-MOCVD, GaAs-MACVD, Others), By Application (LED Lighting, Advanced Packaging, MEMS), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

45399

-

April 2024

-

250

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

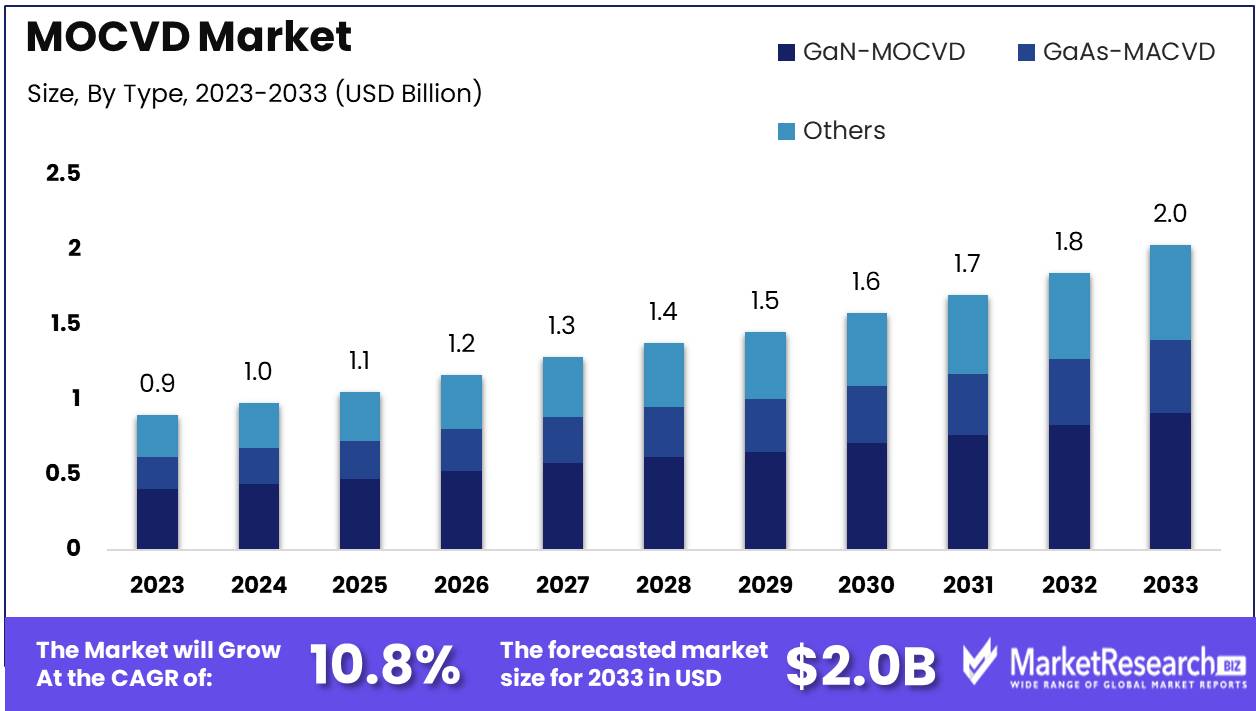

The Global MOCVD Market was valued at USD 0.9 Bn in 2023. It is expected to reach USD 2.0 Bn by 2033, with a CAGR of 10.8% during the forecast period from 2024 to 2033.

The MOCVD Market encompasses the global landscape of semiconductor manufacturing technology, specifically focusing on the deposition of thin films for electronic and optoelectronic devices. This market facilitates the precise growth of semiconductor materials through the controlled chemical reaction of metal-organic precursors in a high-temperature vapor phase environment. MOCVD technology plays a pivotal role in the production of various semiconductor devices, including LEDs, power electronics, and photovoltaic cells, driving innovation and enabling advancements in industries such as lighting, telecommunications, and renewable energy.

The MOCVD market continues to exhibit robust growth and innovation, fueled by advancements in semiconductor technology and increasing demand for energy-efficient lighting solutions. The market is poised for significant expansion driven by key factors such as rising LED adoption, expanding applications in power electronics, and technological advancements.

Supporting this growth trajectory is the development of advanced reactor chambers made of materials like stainless steel or quartz, engineered to withstand the high temperatures and chemical reactions inherent in the MOCVD process. These chambers ensure optimal performance and reliability, enhancing the efficiency and productivity of MOCVD systems.

The imperative to reduce the cost-of-ownership (COO) of MOCVD tools by 50% every 5 years to maintain competitiveness in the LED industry underscores the need for continuous innovation and cost optimization. Manufacturers are increasingly focused on enhancing equipment efficiency, streamlining production processes, and minimizing operational expenses to meet this critical requirement.

As the MOCVD market evolves, companies must navigate dynamic market forces and strategic imperatives to capitalize on emerging opportunities and sustain growth. This includes leveraging technological advancements to develop next-generation MOCVD systems, expanding into new application areas such as automotive electronics and 5G infrastructure, and forging strategic partnerships to enhance market penetration and global reach.

Key Takeaways

- Market Growth: The Global MOCVD Market was valued at USD 0.9 Bn in 2023. It is expected to reach USD 2.0 Bn by 2033, with a CAGR of 10.8% during the forecast period from 2024 to 2033.

- By Type: GaN-MOCVD technology was dominating the MOCVD market, capturing around 62% of the market share.

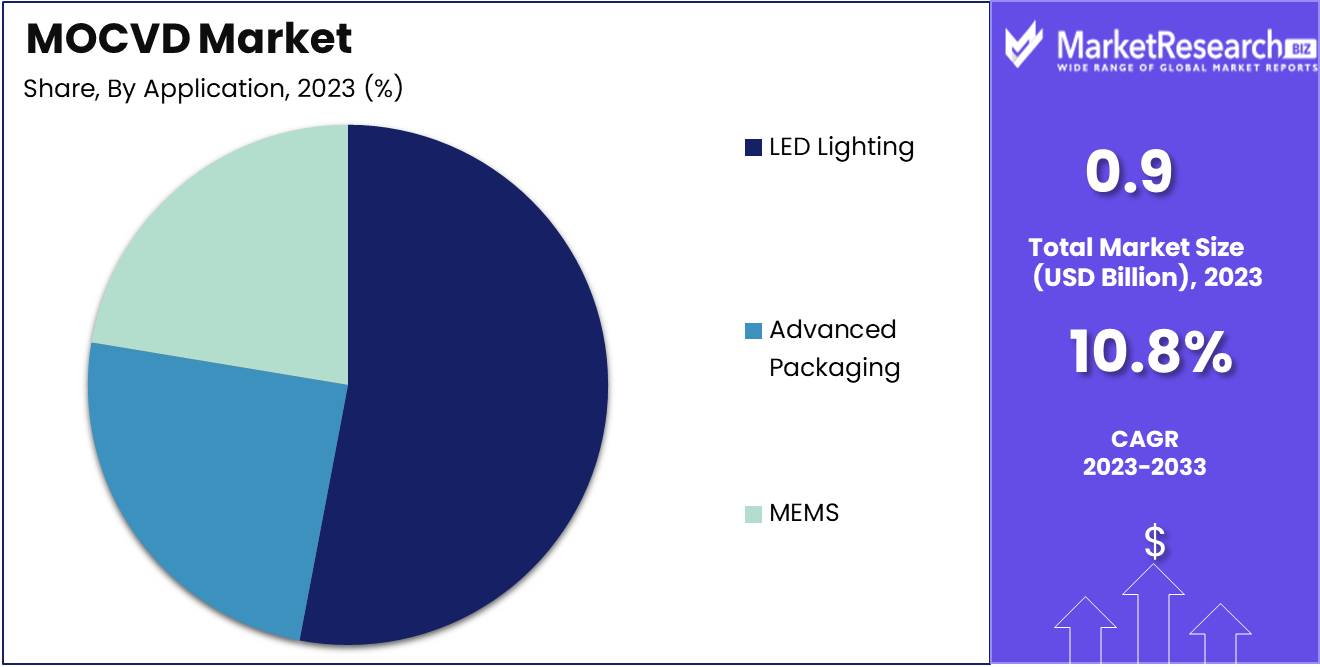

- By Application: In terms of applications, LED lighting was the leading segment, constituting approximately 71% of the MOCVD market.

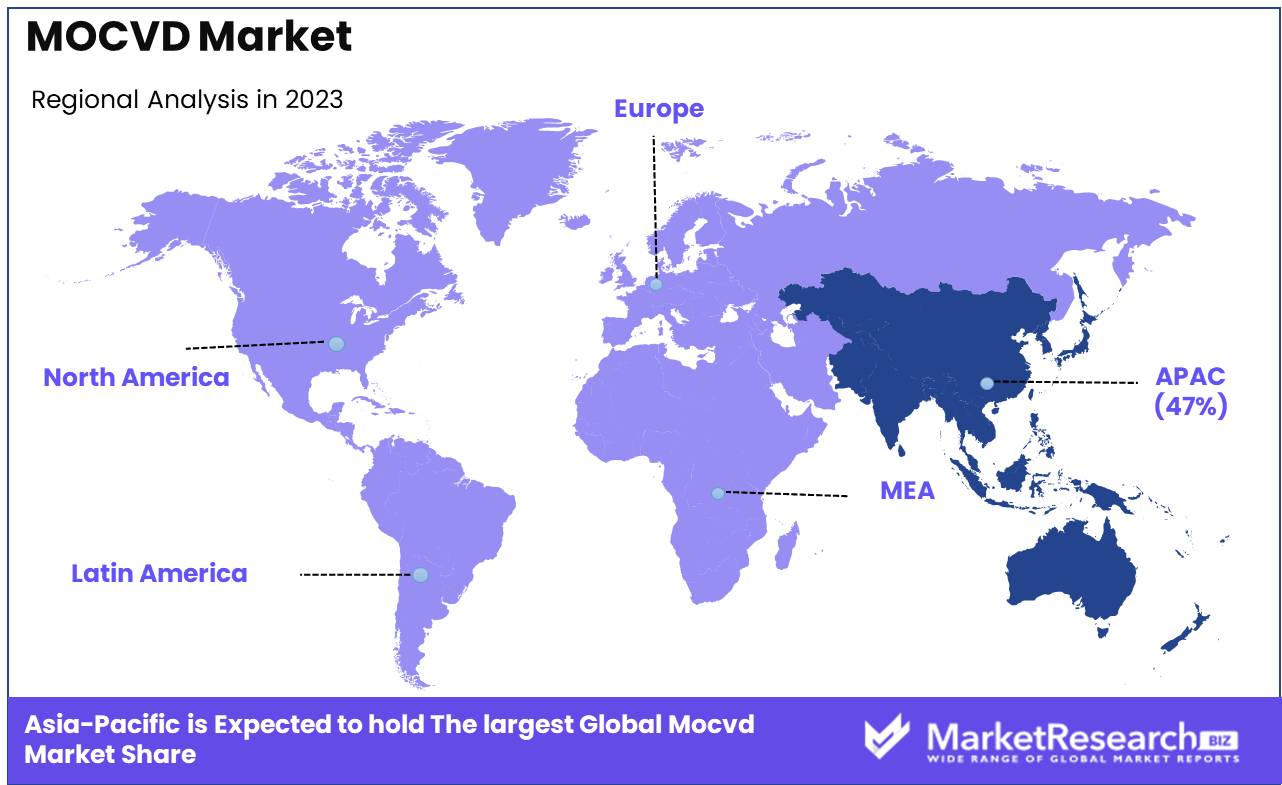

- Regional Dominance: The Asia-Pacific region emerged as the dominant region in the MOCVD market, accounting for over 47% of the global market share.

- Growth Opportunity: The MOCVD market offers growth opportunities fueled by LED demand, power electronics applications, technological advancements, semiconductor investments, emerging markets, and sustainability focus.

Driving factors

Catalyzing Innovation and Market Growth

Continuous advancements in MOCVD technology play a pivotal role in expanding the market. These technological innovations lead to improvements in equipment efficiency, productivity, and the quality of deposited materials. Enhanced reactor designs, novel precursors, and better process control mechanisms contribute to higher deposition rates, superior material properties, and reduced manufacturing costs. As a result, manufacturers are able to meet the escalating demand for semiconductor materials while staying competitive in the global market.

Driving Demand for Specialized Applications

The evolving preferences of consumers towards energy-efficient lighting solutions, high-resolution LED displays, and compact electronic devices are reshaping the landscape of the MOCVD market. As consumers increasingly prioritize sustainability, durability, and performance, manufacturers are compelled to develop new materials and technologies to meet these demands. This shift is driving investments in MOCVD equipment tailored for specific applications such as gallium nitride (GaN) LEDs, which offer superior energy efficiency and longer lifespans compared to traditional lighting solutions.

Fostering Demand for Biomedical Applications

Rising consumer awareness of health and wellness is fostering the development of biomedical applications that require advanced semiconductor materials produced through MOCVD. These applications include medical imaging devices, biosensors, implantable medical devices, and drug discovery services. As the healthcare industry increasingly adopts semiconductor-based solutions for diagnosis, treatment, and monitoring, the demand for MOCVD equipment grows. Manufacturers are thus investing in R&D to optimize MOCVD processes for biomedical applications, driving further market expansion.

Restraining Factors

Development of CVD Equipment

The development of Chemical Vapor Deposition (CVD) equipment is instrumental in driving the expansion of the MOCVD market. CVD processes are essential for depositing thin films of semiconductor materials with precise control over thickness, composition, and uniformity. As demand for advanced electronic devices continues to rise, there is a corresponding need for more sophisticated CVD equipment capable of meeting stringent manufacturing requirements.

Recent trends in CVD equipment development focus on enhancing process efficiency, scalability, and flexibility. This includes innovations in reactor design, automation, and control systems to optimize material deposition and increase production throughput. Furthermore, advancements in deposition techniques, such as atomic layer deposition (ALD) and plasma-enhanced CVD (PECVD), offer greater versatility in depositing a wide range of materials for diverse applications.

Population's Demand for Electronics

The population's increasing demand for electronics is a fundamental driver of growth in the MOCVD market. As global populations grow and technology becomes more ingrained in everyday life, there is a constant need for electronic devices ranging from smartphones and laptops to smart appliances and automotive electronics. This surge in demand directly translates into a higher requirement for semiconductor materials, which are essential components in electronic devices. Emerging trends such as the Internet of Things (IoT), 5G connectivity, and electric vehicles further amplify the demand for advanced semiconductor materials produced through MOCVD processes. These technologies rely on high-performance chips and components to enable connectivity, processing power, and energy efficiency, driving the need for continued innovation in the semiconductor industry.

By Type

GaN-MOCVD dominates MOCVD market with over 62% share in By Type segment.

In 2023, GaN-MOCVD held a dominant market position in the By Type segment of the MOCVD (Metal-Organic Chemical Vapor Deposition) Market, capturing more than a 62% share. GaN-MOCVD technology, known for its efficiency and versatility in producing high-quality thin films, emerged as the preferred choice among manufacturers and researchers alike. Its widespread adoption can be attributed to its ability to facilitate the production of various semiconductor materials, including gallium nitride (GaN), which find applications in LEDs, power electronics, and RF devices, among others.

Following GaN-MOCVD, GaAs-MACVD accounted for a notable share in the MOCVD market, showcasing its significance in semiconductor manufacturing processes. GaAs-MACVD technology specializes in the deposition of gallium arsenide (GaAs) thin films, which are integral components in solar cells, optical devices, and wireless communication systems. While GaAs-MACVD trailed behind GaN-MOCVD in market share, its importance in specific applications underscores its relevance in the semiconductor industry.

Besides GaN-MOCVD and GaAs-MACVD, the Others category encompassed a spectrum of MOCVD technologies catering to diverse semiconductor materials and applications. This segment included emerging technologies, alternative deposition methods, and niche applications that complemented the offerings of GaN-MOCVD and GaAs-MACVD.

By Application

LED Lighting maintained a commanding market presence within the By Application segment of the MOCVD Market, securing over 71% of the market share.

In 2023, LED Lighting held a dominant market position in the By Application segment of the MOCVD (Metal-Organic Chemical Vapor Deposition) Market, capturing more than a 71% share. LED Lighting, driven by its energy efficiency, durability, and versatility, emerged as the leading application area for MOCVD technology. The widespread adoption of LED lighting solutions across various sectors such as residential, commercial, industrial, and automotive contributed significantly to the dominance of this segment. Additionally, the growing focus on sustainability and the increasing demand for eco-friendly lighting alternatives further propelled the adoption of LED lighting, cementing its position as the primary application segment for MOCVD technology.

Following LED Lighting, Advanced Packaging accounted for a notable share in the MOCVD market's application landscape. Advanced Packaging involves the integration of semiconductor devices into compact and efficient packages, enhancing their performance, reliability, and functionality. MOCVD technology plays a crucial role in the fabrication of semiconductor materials and structures essential for advanced packaging applications, including flip-chip bonding, wafer-level packaging, and through-silicon via (TSV) fabrication. While Advanced Packaging trailed behind LED Lighting in market share, its significance in enabling miniaturization, performance optimization, and cost reduction in semiconductor packaging processes remains undeniable.

The MEMS (Micro-Electro-Mechanical Systems) category constituted another important segment within the MOCVD market's application spectrum. MEMS technology involves the integration of mechanical and electrical components on a microscopic scale, enabling the development of sensors, actuators, and other microsystems with diverse functionalities. MOCVD technology plays a vital role in the fabrication of semiconductor materials required for MEMS devices, including epitaxial layers, thin films, and heterostructures.

Key Market Segments

By Type

- GaN-MOCVD

- GaAs-MACVD

- Others

By Application

- LED Lighting

- Advanced Packaging

- MEMS

Growth Opportunity

Increased Usages of LED Lighting

The escalating adoption of LED lighting across various sectors, including residential, commercial, and industrial, presents a compelling growth opportunity for the MOCVD market. LEDs offer superior energy efficiency, longer lifespan, and better environmental sustainability compared to traditional lighting solutions, driving their widespread adoption worldwide. As manufacturers strive to meet the growing demand for high-quality LED chips, the demand for MOCVD equipment for the production of gallium nitride (GaN) and other semiconductor materials is expected to surge.

Semiconductors and Advanced Packaging

The semiconductor industry continues to be a major driver of MOCVD market growth, with increasing demand for advanced chips used in applications such as smartphones, automotive electronics, and IoT devices. Additionally, the rise of advanced packaging technologies, such as System-in-Package (SiP) and 3D integration, further propels the demand for MOCVD equipment for the deposition of thin-film materials essential for semiconductor fabrication.

Rise in Demand for Efficient Power Systems

The global shift towards sustainability and energy efficiency is fueling the demand for efficient power systems, including renewable energy generation, electric vehicles, and energy storage solutions. MOCVD technology plays a critical role in producing high-performance semiconductor materials for power electronics, enabling the development of efficient and compact devices that meet the evolving needs of modern power systems.

Latest Trends

Rise in Investment in Semiconductor Equipment

One prominent trend driving the MOCVD market in 2024 is the substantial increase in investment in semiconductor equipment. With the semiconductor industry experiencing unprecedented growth fueled by demand for advanced electronics, manufacturers are ramping up their investments in equipment and infrastructure to meet market demands. This surge in investment translates into higher demand for MOCVD systems, which are essential for producing semiconductor materials used in a wide range of applications.

Development of CVD Equipment

The continuous development of Chemical Vapor Deposition (CVD) equipment is another notable trend driving the MOCVD market forward. Manufacturers are focusing on enhancing the efficiency, scalability, and flexibility of CVD systems to meet evolving industry requirements. These advancements enable precise control over material deposition, leading to the production of high-quality semiconductor films essential for various electronic devices.

Increased Demand for Solar Cells

In 2024, there is a significant uptick in demand for solar cells, driven by growing concerns over climate change and the transition towards renewable energy sources. MOCVD technology plays a crucial role in the production of thin-film materials used in solar cell fabrication, making it a key beneficiary of this trend.

Growth in End-User Industries in Developing Countries

Developing countries are witnessing rapid growth in end-user industries such as electronics, automotive, and telecommunications. This growth is fueled by factors such as urbanization, rising disposable incomes, and technological advancements. As these industries expand, so does the demand for semiconductor materials produced using MOCVD technology.

Regional Analysis

Asia-Pacific emerged as the powerhouse of the MOCVD market, commanding an impressive 47% share.

Asia-Pacific emerges as the dominating region in the MOCVD market, commanding a substantial 47% share in 2023. The region's dominance can be attributed to the presence of key semiconductor manufacturing hubs in countries such as China, South Korea, Taiwan, and Japan. China, in particular, has emerged as a global leader in semiconductor production, with significant investments in infrastructure and technology. The rapid growth of industries such as LED lighting, consumer electronics, and automotive electronics in Asia-Pacific fuels the demand for MOCVD equipment and services. With favorable government policies, a skilled workforce, and a thriving ecosystem of semiconductor companies, Asia-Pacific remains a critical region driving the growth of the MOCVD market.

North America represents a prominent market for MOCVD technology, driven by its robust semiconductor industry and technological innovation. In 2023, North America accounted for approximately 30% of the global MOCVD market share. The United States, in particular, emerged as a key player in semiconductor manufacturing, with major companies investing in research and development initiatives.

Europe is a significant contributor to the MOCVD market, representing around 15% of the global market share in 2023. Countries like Germany, the United Kingdom, and France are at the forefront of semiconductor research and manufacturing in the region. Europe's emphasis on sustainability, coupled with investments in renewable energy and smart technologies, has led to a growing demand for MOCVD equipment for applications such as LED lighting and solar cells.

The Middle East & Africa region represents a smaller yet growing market for MOCVD technology. While precise market share data may vary, the region is witnessing increasing investments in semiconductor manufacturing and technology infrastructure. Countries like Israel, Saudi Arabia, and the United Arab Emirates are focusing on diversifying their economies and promoting high-tech industries, including semiconductor manufacturing. The adoption of MOCVD technology is driven by applications in sectors such as telecommunications, energy, and healthcare.

Latin America presents emerging opportunities for the MOCVD market, fueled by the region's growing electronics manufacturing sector and increasing investments in technology. While specific market share data may vary, countries like Brazil, Mexico, and Argentina are witnessing a rise in semiconductor production and research activities. The demand for MOCVD equipment is driven by applications in LED lighting, consumer electronics, and telecommunications. As Latin American countries focus on economic development and industrialization, the MOCVD market is poised to witness steady growth in the region.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global MOCVD market is poised for continued growth and innovation, with key players competing to maintain their positions and seize emerging opportunities. Among these players, CVD Equipment Corporation stands out for its consistent delivery of high-quality MOCVD solutions, supported by a robust research and development framework. With a focus on customer satisfaction and technological advancement, CVD Equipment Corporation remains a formidable force in the market, catering to the evolving needs of semiconductor manufacturers worldwide.

Another notable contender is AIXTRON SE, renowned for its extensive experience and technological expertise in MOCVD systems. The company's commitment to innovation enables it to stay ahead of industry trends, offering cutting-edge solutions to meet the demands of diverse applications. AIXTRON SE's global presence and strategic partnerships position it as a key player driving innovation and growth in the MOCVD market.

Veeco Instruments Inc. is also a prominent player in the MOCVD market, offering a comprehensive portfolio of solutions tailored to various semiconductor manufacturing needs. With a focus on customer-centricity and technological excellence, Veeco Instruments Inc. maintains a competitive edge, serving as a trusted partner for semiconductor manufacturers worldwide. The company's dedication to continuous improvement and market responsiveness solidifies its position as a leader in the MOCVD market.

Lastly, Nichia Corporation, a major manufacturer of LEDs and optoelectronic devices, plays a significant role in shaping the MOCVD market landscape. Leveraging its vertically integrated approach and strong research capabilities, Nichia Corporation delivers innovative solutions that drive the adoption of MOCVD technology across diverse applications. As the demand for energy-efficient lighting and advanced optoelectronic devices continues to rise, Nichia Corporation remains at the forefront of innovation, driving growth and market penetration in the MOCVD segment.

Market Key Players

- CVD Equipment Corporation

- Samco Inc.

- Advanced Micro-Fabrication Equipment Inc. China

- AIXTRON SE

- Toshiba Corporation (NuFlare Technology Inc.)

- Nichia Corporation

- Agnitron Technology, Inc.

- Nippon Sanso Holding Corporation (Taiyo Nippon Sanso Corporation)

- Veeco Instruments Inc.

- Qingdao Jason Electric Co. Ltd.

- JUSUNG ENGINEERING Co. Ltd.

- Alliance MOCVD, LLC

Recent Development

- In August 2023, Samsung Electronics and its domestic foundry peers DB Hitek and Key Foundry reportedly are set to procure metal-organic chemical vapor deposition (MOCVD) equipment from Germany's Aixtron to facilitate their foray into the GaN and SiC chips manufacturing.

- In November 2022, Aixtron SE anticipates record revenue in Q4/2022 due to shipment push-outs from Q3, driven by strong demand for GaN- and SiC-based power electronics. Q3 order intake increased by 25% year-on-year. Full-year guidance upgraded for 2022 with double-digit revenue growth expected.

- In January 2021, In the ongoing U.S.-China semiconductor rivalry, technological independence is sought, but challenges persist. China makes strides in back-end manufacturing and fabless design, prompting policy reassessment by the Biden administration

Report Scope

Report Features Description Market Value (2023) USD 0.9 Bn Forecast Revenue (2033) USD 2.0 Bn CAGR (2024-2033) 10.8% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (GaN-MOCVD, GaAs-MACVD, Others), By Application (LED Lighting, Advanced Packaging, MEMS) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape CVD Equipment Corporation, Samco Inc., Advanced Micro-Fabrication Equipment Inc. China, AIXTRON SE, Toshiba Corporation (NuFlare Technology Inc.), Nichia Corporation, Agnitron Technology, Inc., Nippon Sanso Holding Corporation (Taiyo Nippon Sanso Corporation), Veeco Instruments Inc., Qingdao Jason Electric Co. Ltd., JUSUNG ENGINEERING Co. Ltd., Alliance MOCVD, LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- CVD Equipment Corporation

- Samco Inc.

- Advanced Micro-Fabrication Equipment Inc. China

- AIXTRON SE

- Toshiba Corporation (NuFlare Technology Inc.)

- Nichia Corporation

- Agnitron Technology, Inc.

- Nippon Sanso Holding Corporation (Taiyo Nippon Sanso Corporation)

- Veeco Instruments Inc.

- Qingdao Jason Electric Co. Ltd.

- JUSUNG ENGINEERING Co. Ltd.

- Alliance MOCVD, LLC

Our Clients

View Our Licence Options