Kitchenware Market By Product(Cookware, Bakeware, Others), By Distribution Channel(Offline, Online), By End Use(Residential Kitchen, Commercial Kitchens), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

13644

-

Feb 2024

-

166

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Report Overview

- Driving Factors

- Restraining Factors

- Kitchenware Market Segmentation Analysis

- Kitchenware Industry Segments

- Kitchenware Market Growth Opportunities

- Kitchenware Market Regional Analysis

- Kitchenware Industry By Region

- Kitchenware Market Competitive Analysis

- Kitchenware Industry Key Players

- Kitchenware Market Recent Development

- Report Scope

Report Overview

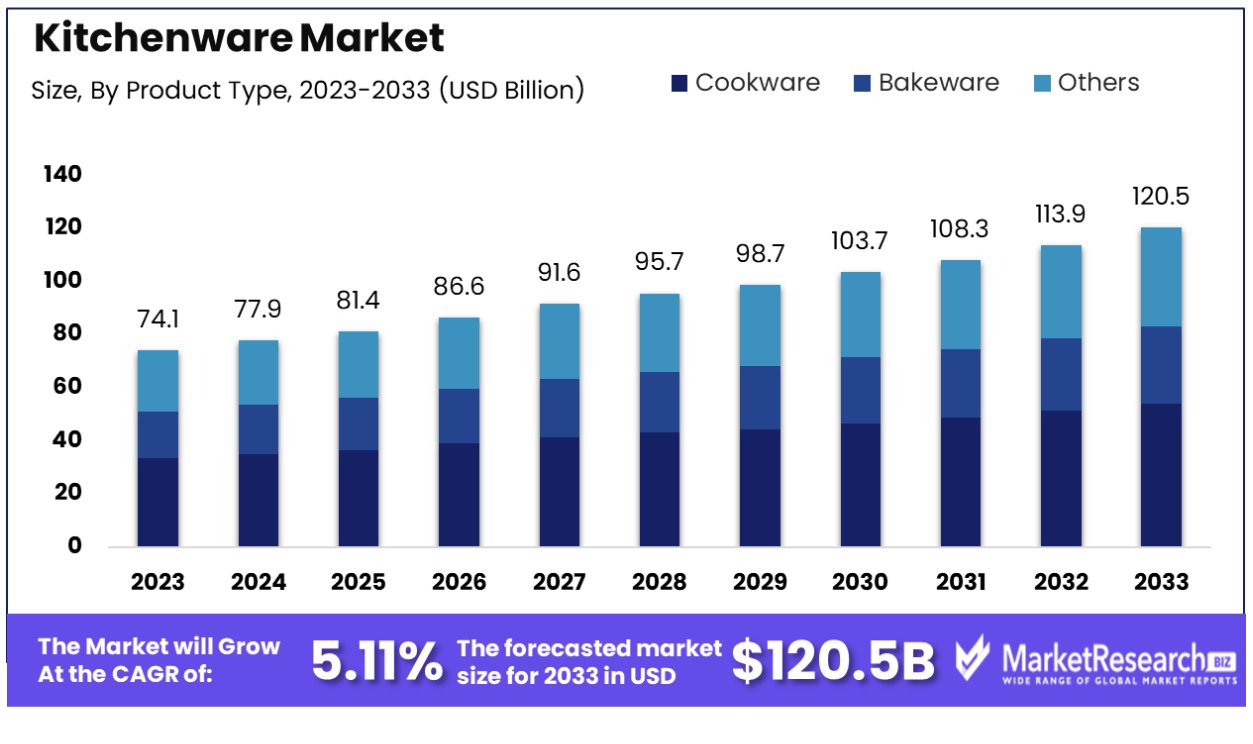

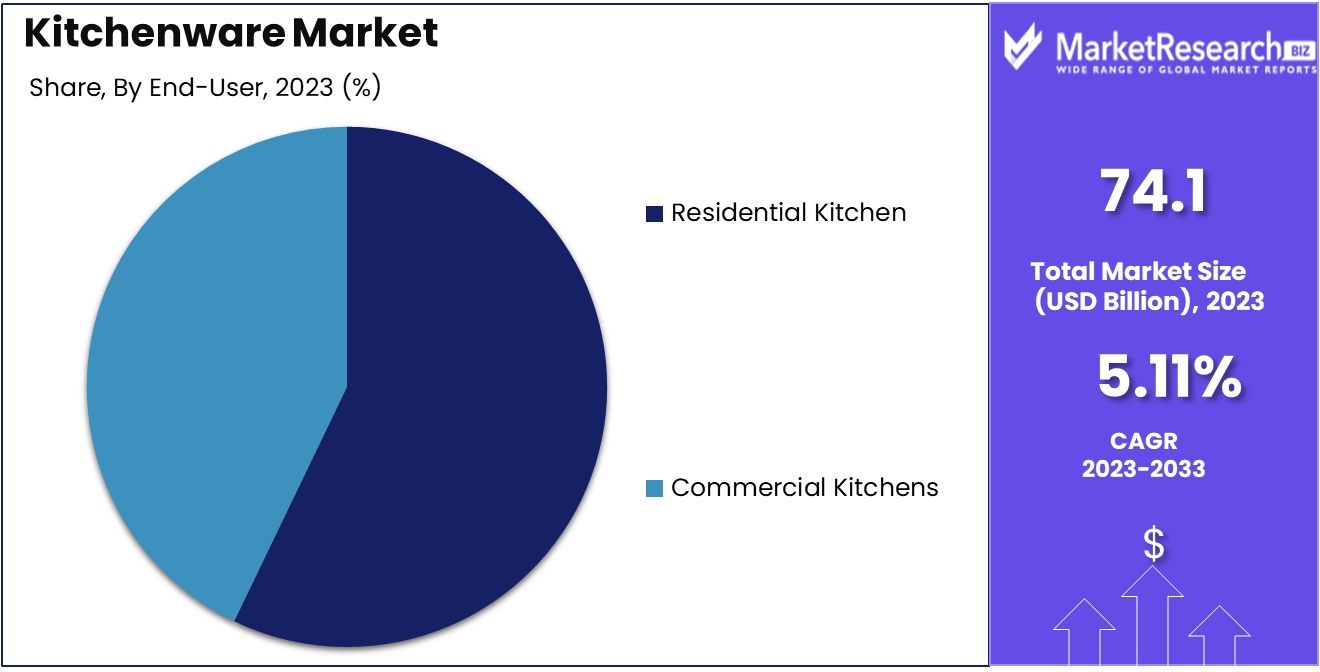

The kitchenware market was valued at USD 74.1 billion in 2023. It is expected to reach USD 120.5 billion by 2033, with a CAGR of 5.11% during the forecast period from 2024 to 2033.

The surge in demand for various kitchenware appliances that are electronic and non-electric as well as the rise in global population are some of the main key driving factors for the kitchenware market.

Kitchenware defines different types of equipment, tools, and utensils that are used in kitchens and other restaurants for making food and serving it. There is a wide range of kitchenware items that are specially designed to simplify various facets of food preparations and cooking. Daily kitchenware comprises pans, knives, pots, mixing bowls, bakeware, and other equipment that are used inside the kitchens. These materials and designs of kitchenware can change and they are often chosen based on their requirements, functionalities, aesthetic appeals, and longevity. It plays a key role in the cooking process and contributes to the efficacy and culinary experience.

The kitchen is the main hub for cooking, socializing, and dining. A well-designed kitchen augments the whole quality of life by promoting good and healthy eating habits. Several types of kitchenware are commonly used in the kitchen. Such types of kitchenware are frying pans, pressure cookers, roasting pans, and other kitchen equipment. These kitchenwares are important as they keep the food warm and cold as well. They are also used to pre-heat the stovetop and make the cleaning process easier. Kitchenwares are also used in the making of healthy meals.

In industrial manufacturing, kitchenware holds great importance as it ensures efficient and standardized methods. In industrial kitchens, there are good quality kitchenwares that are used from cutting tools to cooking kitchenware appliances. These kitchenware appliances are vital as they streamline the food preparation method which ultimately leads to great productivity and outcomes. Longevity kitchen materials and constructions are important for durability, decreasing replacements, and maintaining cost efficacy.

They also play an important role in adhering the food safety and hygiene, by maintaining industrial standards and regulations. Similarly, new innovative and smart kitchenware technologies augment productivity by improving accuracy and eliminating human errors. Well-designed kitchenware is a main part of the success of industrial kitchens, supporting operational efficacy and delivering high-quality food items. The demand for kitchenware will increase due to its requirement for household purposes and other industrial purposes which will lead to market expansion during the forecast period.

Driving Factors

Increasing Disposable Incomes Drive Market Growth

The escalation of disposable incomes globally, particularly in emerging economies, has a profound impact on the kitchenware market. Consumers, with more financial resources, are inclined to invest in premium and branded kitchenware items, viewing them as symbols of status and lifestyle enhancements. This trend is notably visible in countries like India, where a burgeoning middle class is propelling the demand for high-end kitchenware products. The increased purchasing power enables consumers to prioritize quality and aesthetics, leading to a surge in market growth.

The synergy between rising incomes and consumer preferences for luxury kitchenware items not only drives immediate market expansion but also sets the stage for sustained growth. As disposable incomes continue to rise, the demand for innovative and premium kitchenware is expected to grow, encouraging manufacturers to introduce a wider range of high-quality products.

Growing Demand for Multifunctional and Smart Kitchenware

The shift towards multifunctional and smart kitchenware is a significant growth driver in the industry. Consumers' preference for space-saving, efficient, and technologically advanced products, such as multi-cookers, air fryers, and smart ovens, is accelerating innovation and new product development. This demand reflects a broader trend of integrating technology into everyday life to enhance convenience and functionality in the kitchen.

This trend is closely linked with the growing emphasis on smart homes and connected living, where kitchenware becomes a part of a larger ecosystem of smart devices. The convergence of technology and kitchenware not only meets the current demand for efficiency and convenience but also anticipates future consumer needs, ensuring long-term market growth. Manufacturers who capitalize on this trend by continually innovating and integrating smart features into their products are likely to remain competitive and drive market expansion.

Changing Lifestyles and Eating Habits Impact Market Dynamics

The transformation in lifestyles and eating habits, characterized by busier schedules and a heightened awareness of health and nutrition, is driving the demand for kitchenware that supports quick, convenient, and healthy cooking. Products like steamers, induction cooktops, and non-stick cookware are increasingly popular as they align with the consumer's desire for cooking solutions that cater to a health-conscious lifestyle without sacrificing convenience.

This trend is not isolated but interacts synergistically with the growing fitness and wellness movement, further amplifying the demand for kitchenware that supports healthy living. The shift towards convenient and health-oriented kitchenware is not a transient trend but a reflection of deeper changes in consumer priorities. As these lifestyle changes become more entrenched, the kitchenware market is expected to continue growing, driven by the demand for products that facilitate healthy eating habits and fit into fast-paced lifestyles.

Restraining Factors

Intense Competition Restrains Market Growth

The kitchenware market is characterized by intense competition, featuring a mix of well-established brands and numerous unorganized players. This diversity in market participants leads to a highly competitive environment where pricing power is significantly diluted, impacting the profit margins of all involved. Brands like Prestige and Hawkins, known for their stainless steel cookware, face fierce competition not only from each other but also from emerging brands and unorganized sectors offering similar products at competitive prices. The result is a market where differentiation becomes difficult, and companies must continuously innovate to maintain profitability. This competition, while fostering innovation, also serves as a barrier to market growth by limiting the potential for price increases and reducing overall profitability for companies.

Threat from Substitute Products Limits Market Expansion

The rise of substitute products, such as non-stick coatings and alternatives made from aluminum and glassware, presents a significant challenge to traditional kitchenware categories. For instance, the preference for non-stick cookware over stainless steel options reflects a shift in consumer demand towards products that offer convenience and health benefits, such as reduced need for cooking oils. This shift not only impacts the demand for stainless steel cookware but also limits the growth potential of certain segments within the kitchenware market. As consumers become more inclined towards substitutes that offer additional conveniences, traditional materials, and products find it increasingly difficult to compete, thereby restraining market growth in these categories.

Kitchenware Market Segmentation Analysis

By Product: Cookware Dominates

Dominant Sub-Segment: Cookware Cookware stands as the dominant sub-segment within the kitchenware market, driven by consumer demand for high-quality, durable, and innovative cooking solutions. The rising interest in home cooking, fueled by health consciousness and the popularity of culinary shows, has significantly contributed to the growth of the cookware segment. Stainless steel, non-stick, and cast iron cookware are particularly popular for their durability, ease of use, and ability to enhance the cooking experience. This segment's growth is further propelled by innovations such as induction-compatible and smart-connected cookware, catering to the modern kitchen's needs.

Other Segments:

- Bakeware: While not as large as the cookware segment, bakeware remains vital due to the growing interest in baking at home, especially amid the recent global events that have led more people to try baking as a hobby or profession.

- Cutlery & Knife Accessories, Appliances, Utensils & Small Gadgets: These segments, though smaller in comparison, play crucial roles in complementing the cookware market. They are essential for a fully equipped kitchen, from preparation to cooking and serving. Innovations and aesthetics in these segments also contribute significantly to market growth, meeting the demand for functionality and style in kitchenware.

By Distribution Channel: Offline Channels Lead

Dominant Sub-Segment: Offline Offline distribution channels, including department stores, specialty stores, and direct seller outlets, historically dominate the kitchenware market's distribution landscape. This dominance is attributed to the consumer preference for physically examining products before purchase, seeking quality assurance and the right fit for their needs. The tactile experience, immediate availability, and personalized customer service offered by offline channels significantly influence purchasing decisions, especially for high-end and premium kitchenware products.

Other Segment: Online The online segment, though not dominant, is rapidly growing, driven by the convenience of home shopping, a wider range of products, and often competitive pricing. The rise of e-commerce platforms and direct-to-consumer brands in the kitchenware sector is reshaping consumer purchasing habits, offering the potential for significant growth. This channel's expansion is further accelerated by technological advancements and the increasing consumer comfort with online shopping, making it a critical area for future market expansion.

By End User: Residential Kitchens Take the Lead

Dominant Sub-Segment: Residential Kitchens Residential kitchens represent the largest end-user segment in the kitchenware market, driven by the global trend of home cooking and baking. The desire to prepare healthy, home-cooked meals and the pleasure of cooking as a leisure activity has elevated the demand for various kitchenware products in residential settings. The growth in this segment is supported by the increasing number of households, the trend toward home renovation and kitchen upgrades, and the interest in culinary arts among the general population.

Other Segment: Commercial Kitchens Commercial kitchens, including those in restaurants, hotels, and catering services, though not as large as the residential segment, are vital to the kitchenware market. The demand in this segment is driven by the need for durable, high-volume, and efficient kitchenware that can withstand the rigors of commercial cooking. The growth in the hospitality and food service industry indirectly supports the expansion of the kitchenware market, highlighting the importance of this segment.

Kitchenware Industry Segments

By Product

- Cookware

- Bakeware

- Others

By Distribution Channel

- Offline

- Online

By End User

- Residential Kitchen

- Commercial Kitchens

Kitchenware Market Growth Opportunities

Innovation in Materials and Designs Offers Growth Opportunities

The kitchenware market is witnessing a significant transformation through the introduction of new materials like ceramic, glass, and advanced non-stick coatings. These innovations not only enhance the functionality and durability of kitchenware but also offer opportunities for premium product positioning. For instance, BlueStone's artificial marble kitchenware stands out for its unique aesthetic appeal, catering to consumers seeking both style and substance in their kitchen tools. Unique shapes, colors, and designs further appeal to the desire for personalization and can attract a niche market segment looking for kitchenware that complements their home décor. This drive towards innovation in materials and designs not only meets the evolving consumer expectations but also opens up new avenues for market growth by differentiating products in a crowded marketplace.

Advanced Technology Integration Offers Growth Opportunity

The integration of advanced technology into kitchenware presents a substantial growth opportunity within the market. Smart kitchenware, equipped with connectivity, sensors, and digital features, addresses the growing demand for user-friendly and intelligent cooking solutions. Products like app-enabled pressure cookers and smart weighing scales exemplify how technology can add value to everyday kitchen tools, making cooking more efficient, convenient, and enjoyable for the user. This trend not only solves the pain point associated with traditional kitchenware but also taps into the larger smart home ecosystem, appealing to tech-savvy consumers and those interested in culinary innovation. The potential for expansion in this area is significant, as consumers increasingly look for products that integrate seamlessly with their connected lives, offering manufacturers a lucrative avenue to explore innovative, technology-driven kitchenware solutions.

Kitchenware Market Regional Analysis

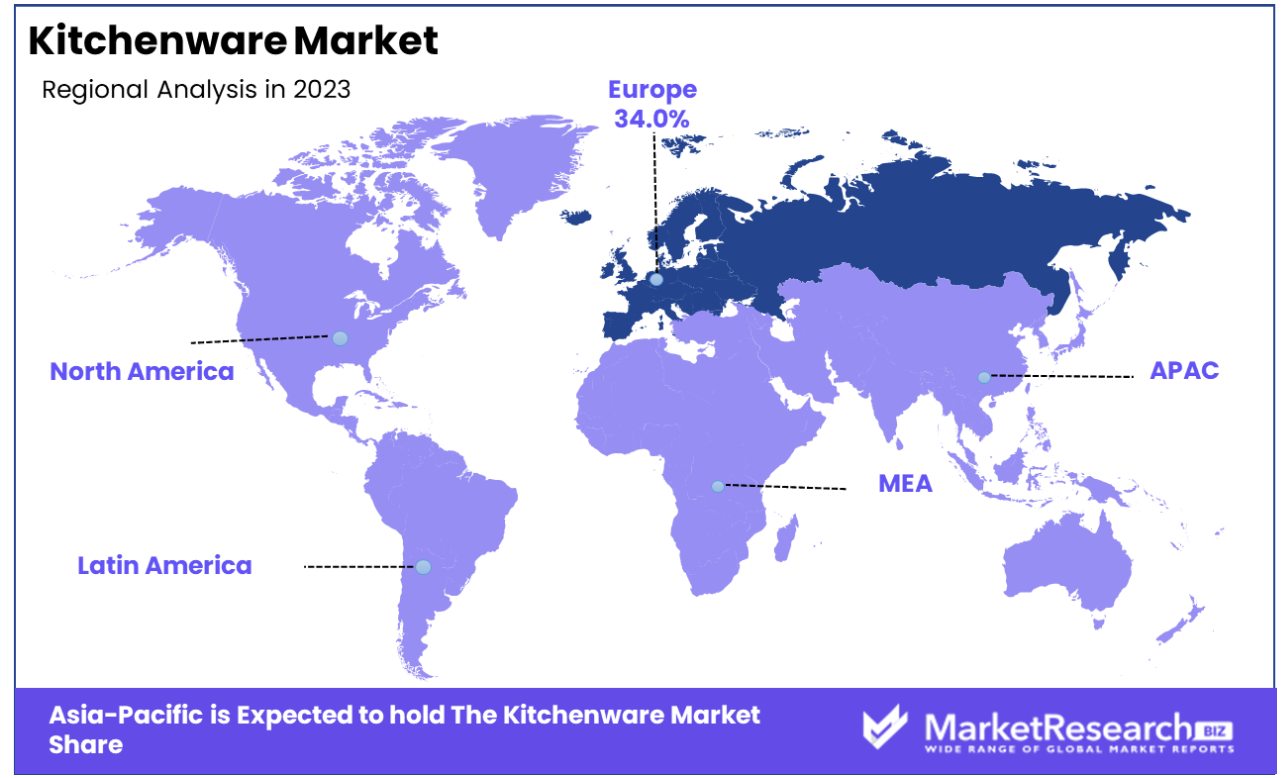

Europe Dominates with 34.0% Market Share

Europe's commanding 34.0% share of the global kitchenware market can be attributed to its high standard of living, a strong tradition of culinary excellence, and the presence of numerous legacy brands known for quality and innovation. The region benefits from a consumer base that values quality kitchenware as essential to both daily life and special occasions, driving demand for premium and innovative products.

Europe's market dynamics are characterized by a blend of tradition and innovation. The region's rich culinary history fosters a culture that appreciates high-quality cookware, bakeware, and utensils, while its focus on sustainability and technology integration meets modern consumer demands. This unique combination supports a diverse and competitive market landscape, encouraging constant innovation among manufacturers.

North America: A Key Player in the Kitchenware Market

North America, particularly the United States, plays a pivotal role in the kitchenware market due to its large consumer market, high disposable incomes, and a culture that embraces culinary exploration and home cooking. The region's enthusiasm for diverse cuisines and cooking shows, along with a robust online retail sector, fuels demand for a wide range of kitchenware products.

The North American market is highly dynamic, characterized by the rapid adoption of trends such as smart kitchen devices and sustainable products. The strong presence of e-commerce platforms facilitates easy access to both domestic and international kitchenware brands, further stimulating market growth.

Asia-Pacific: The Emerging Powerhouse

The Asia-Pacific region is rapidly emerging as a significant force in the kitchenware market, driven by expanding middle-class populations, increasing urbanization, and growing interest in cooking as a leisure activity. Countries like China and India are witnessing a surge in demand for both traditional and modern kitchenware, supported by rising incomes and the proliferation of cooking-related content on social media.

Kitchenware Industry By Region

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Kitchenware Market Competitive Analysis

The kitchenware market is characterized by a diverse array of key players, each contributing to the industry's dynamics through strategic positioning and innovative product offerings. Companies like Tupperware and Pampered Chef are renowned for their direct selling approach, which allows for personalized customer engagement and loyalty. Meyer Corporation and KitchenAid have established themselves as leaders in high-quality cookware and appliances, emphasizing durability and performance. Cuisinart and Hobart Corporation further enrich the market with their wide range of kitchen tools and professional equipment, catering to both home cooks and commercial kitchens.

Electronics giants such as LG Electronics Inc., Samsung Electronics Co Ltd., and Koninklijke Philips N.V. bring advanced technology integration into the kitchenware sector, offering smart kitchen appliances that enhance user convenience and efficiency. Morphy Richards Ltd. and AB Electrolux (publ) stand out for their focus on innovation in ease of use and energy efficiency. Whirlpool Corporation, with its vast portfolio, continues to influence market trends through its commitment to sustainability and smart home ecosystems.

Pyrex Cookware (Corning Inc.) contributes with its strong heritage in glassware, offering durability and versatility. Meanwhile, Illinois Tools Works Inc. and Dover Corporation underscore the industry’s breadth with their specialized equipment and solutions for food preparation and storage.

Kitchenware Industry Key Players

- Tupperware

- Pampered Chef

- Meyer Corporation

- KitchenAid

- Cuisinart

- Hobart Corporation

- LG Electronics Inc.

- Samsung Electronics Co Ltd.

- Morphy Richards Ltd.

- Koninklijke Philips N.V.

- AB Electrolux (publ)

- Whirlpool Corporation

- Pyrex Cookware (Corning Inc.)

- Illinois tools Works Inc.

- Dover Corporation

Kitchenware Market Recent Development

- Sept 2023 Caraway The iconic home and lifestyle brand that is a leader in eco-friendly, stylish kitchenware and household goods has announced it has raised a $35 million capital investment facilitated by McCarthy Capital. McCarthy Capital has a portfolio of investments that exceed $3 billion. it is focused on expanding companies with solid management teams.

- June 2023. Great Jones, a quickly growing top brand in premium cooking items was purchased by the world's largest cookware manufacturer Meyer Corporation. The partnership aims to combine Meyer's ingenuity and superior operational and product expertise with Great Jones's enthusiasm for giving home cooks the tools they need to succeed.

Report Scope

Report Features Description Report Features Description Market Value (2022) USD 74.1 Bn Forecast Revenue (2032) USD 120.5 Bn CAGR (2023-2032) 5.11% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Cookware, Bakeware, Others), By Distribution Channel(Offline, Online), By End Use(Residential Kitchen, Commercial Kitchens) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Tupperware, Pampered Chef, Meyer Corporation, KitchenAid, Cuisinart, Hobart Corporation, LG Electronics Inc., Samsung Electronics Co Ltd., Morphy Richards Ltd., Koninklijke Philips N.V., AB Electrolux (publ), Whirlpool Corporation, Pyrex Cookware (Corning Inc.), Illinois tools Works Inc., Dover Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Tupperware

- Pampered Chef

- Meyer Corporation

- KitchenAid

- Cuisinart

- Hobart Corporation

- LG Electronics Inc.

- Samsung Electronics Co Ltd.

- Morphy Richards Ltd.

- Koninklijke Philips N.V.

- AB Electrolux (publ)

- Whirlpool Corporation

- Pyrex Cookware (Corning Inc.)

- Illinois tools Works Inc.

- Dover Corporation

Our Clients

View Our Licence Options