Hot Drinks Market By Type (Coffee, Tea, Others), By Distribution Channel (Hypermarkets and Supermarkets, Department Stores, Coffee Shops, Online, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

15906

-

July 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

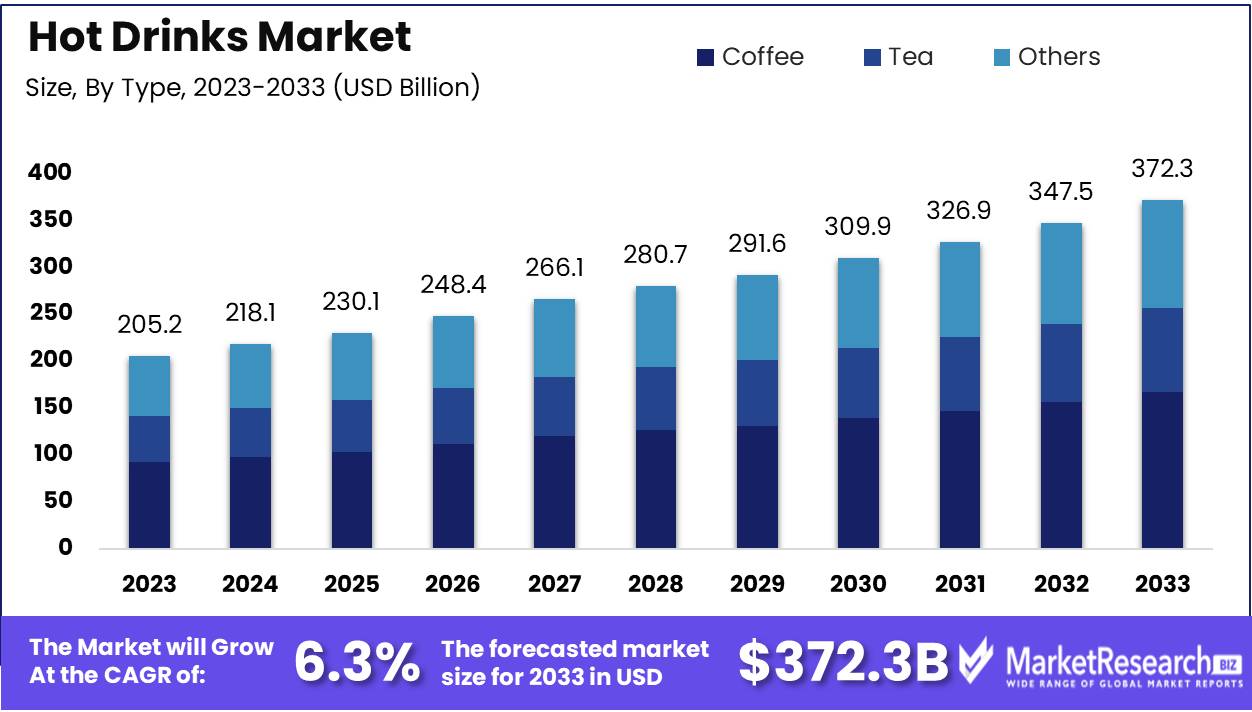

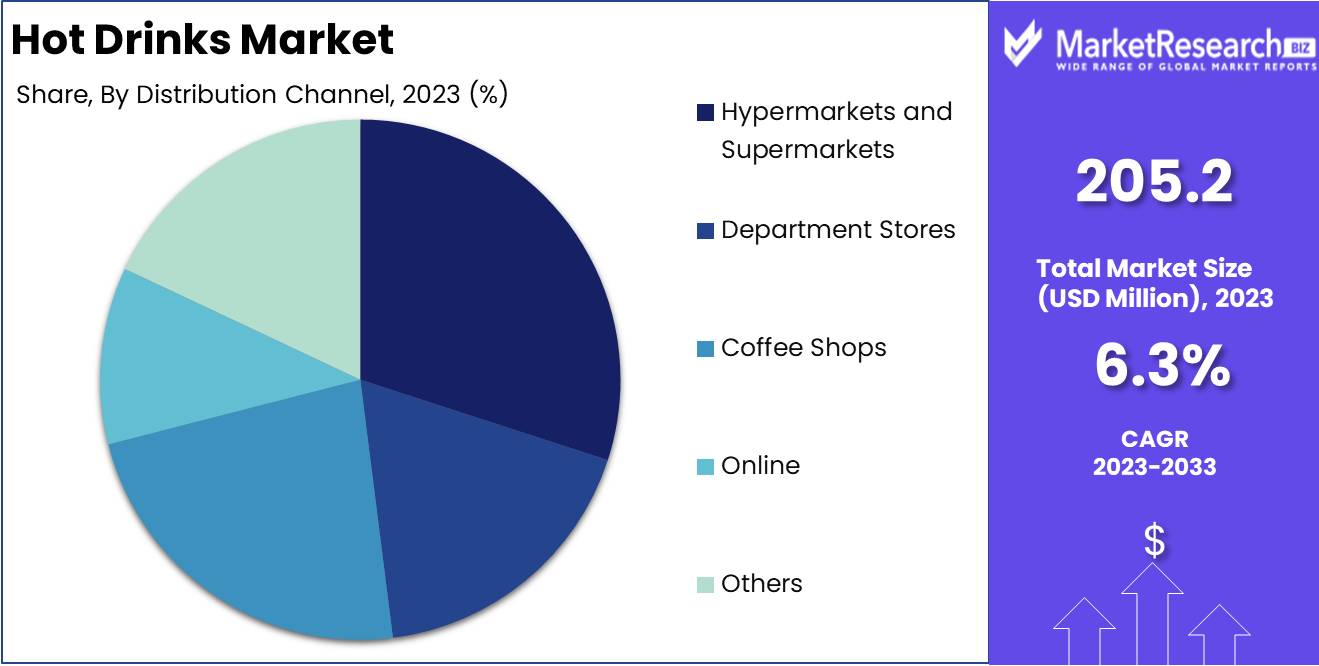

The Hot Drinks Market was valued at USD 205.2 billion in 2023. It is expected to reach USD 372.3 billion by 2033, with a CAGR of 6.3% during the forecast period from 2024 to 2033.

The Hot Drinks Market encompasses the global trade of beverages traditionally served hot, such as coffee, tea, and hot chocolate. This market is driven by increasing consumer demand for premium and specialty beverages, the health benefits of certain hot drinks, and the expanding café culture.The market's growth is further propelled by innovations in flavor, packaging, and sustainability. Major players focus on product diversification and strategic partnerships to capture diverse consumer preferences and expand their global footprint.

The hot drinks market is experiencing significant growth driven by a combination of health awareness and rising disposable incomes. Increasing awareness of the health benefits associated with certain hot drinks, such as tea and herbal infusions, is a primary driver of this market expansion. Consumers are becoming more health-conscious, leading to a higher demand for beverages that offer functional benefits, such as antioxidants and other natural ingredients found in herbal teas.

Moreover, the trend towards premiumization is gaining momentum, with consumers willing to pay more for high-quality and specialty hot drinks. This willingness to invest in premium products is particularly evident in developed markets but is also emerging in developing regions. These factors collectively create a robust market environment for the hot drinks sector.

However, certain challenges may temper this growth trajectory. Increasing health concerns related to high caffeine and sugar content in some hot drinks pose a potential obstacle. As consumers become more health-aware, they may shy away from beverages perceived to contribute to negative health outcomes. Despite this, the overall market outlook remains positive. Growing disposable income, especially in developing regions, is enabling consumers to spend more on premium and specialty hot drinks.

Key Takeaways

- Market Growth: The Hot Drinks Market was valued at USD 205.2 billion in 2023. It is expected to reach USD 372.3 billion by 2033, with a CAGR of 6.3% during the forecast period from 2024 to 2033.

- By Type: Coffee dominated the Hot Drinks Market driven by consumer preferences.

- By Distribution Channel: Hypermarkets and Supermarkets dominated the hot drinks market distribution.

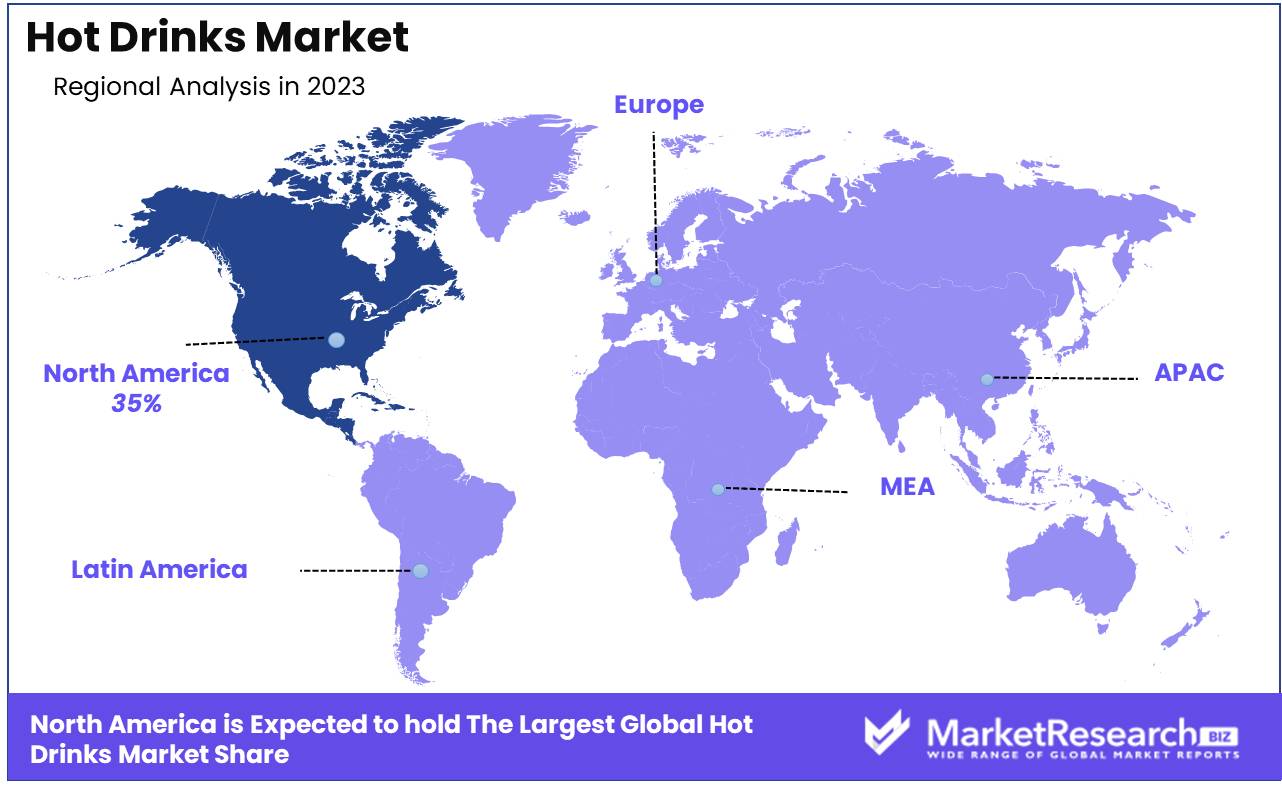

- Regional Dominance: North America dominates the hot drinks market with a 35% largest share.

- Growth Opportunity: The global hot drinks market offers vast opportunities through premiumization and wellness-focused innovations, driving consumer satisfaction and market growth.

Driving factors

Innovation in Flavors and Varieties: Enhancing Consumer Engagement

Innovation in flavors and varieties has significantly contributed to the growth of the hot drinks market. The introduction of unique and diverse flavors caters to the evolving tastes and preferences of consumers, thereby increasing market penetration. For instance, the incorporation of exotic flavors like matcha, turmeric, and various fruit infusions has attracted a broader consumer base. According to recent market data, flavored hot beverages accounted for approximately 35% of total hot drinks sales in 2023, indicating a substantial impact on market dynamics. This trend is expected to continue, driving further market expansion as companies continue to innovate and introduce novel flavors that resonate with consumers.

Convenience and On-the-Go Consumption: Meeting Modern Lifestyle Needs

The increasing demand for convenience and on-the-go consumption options has propelled the growth of the hot drinks market. Modern consumers seek products that align with their fast-paced lifestyles, leading to a surge in the popularity of ready-to-drink (RTD) beverages and single-serve coffee pods. The global market for RTD hot beverages was valued at USD 12.3 billion in 2023, demonstrating a strong preference for convenient consumption formats. Moreover, the proliferation of coffee shops and vending machines offering quick and easy access to hot drinks has further fueled this trend. By providing convenient options, the hot drinks market can effectively capture the attention of busy consumers, thereby driving sustained growth.

Health-Focused Product Development: Catering to Health-Conscious Consumers

Health-focused product development has emerged as a crucial driver of growth in the hot drinks market. With a growing awareness of health and wellness, consumers are increasingly opting for beverages that offer functional benefits. Products such as herbal teas, organic coffees, and hot drinks fortified with vitamins and minerals have gained substantial traction. In 2023, health-focused hot beverages saw a 20% increase in sales, highlighting the market's responsiveness to health trends. Companies are investing in research and development to create products that not only satisfy taste preferences but also contribute to overall well-being. This focus on health is expected to continue driving market growth as consumers prioritize healthier lifestyle choices.

Restraining Factors

Impact of Cold Beverage Alternatives on the Hot Drinks Market

The hot drinks market faces significant competition from cold beverages, which have gained popularity due to their refreshing qualities and convenience. This competition has been intensified by the increasing availability and variety of cold beverage options such as iced coffee, iced tea, and ready-to-drink (RTD) beverages. These alternatives are particularly appealing in warmer climates and during summer months, reducing the overall demand for hot drinks.

A notable statistic illustrating this trend is the growth of the global RTD tea and coffee market, which was valued at approximately USD 86 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 6.5% from 2023 to 2028. This rapid growth indicates a shifting consumer preference toward cold beverages, thereby restraining the expansion of the hot drinks market.

Environmental and Ethical Challenges Restricting Hot Drinks Market Growth

Sustainability concerns play a pivotal role in shaping consumer preferences and behaviors, affecting the growth of the hot drinks market. Issues such as the environmental impact of coffee and tea cultivation, deforestation, and the carbon footprint associated with production and transportation have led consumers to seek more eco-friendly alternatives. This shift in consumer behavior is reflected in the increasing demand for sustainably sourced and certified products, which often come at a higher cost and can limit market expansion.

For instance, the coffee industry alone is responsible for a significant portion of deforestation in tropical regions. It is estimated that 2.5 million acres of forest are cleared annually for coffee cultivation. Additionally, the carbon footprint of coffee production is considerable, with each cup of coffee contributing approximately 59 grams of CO2 emissions.

Moreover, ethical concerns regarding labor practices in coffee and tea plantations have prompted consumers to prioritize products with fair trade and ethical certifications. These certifications, while beneficial for social responsibility, often result in higher production costs, which can be a barrier to market growth as price-sensitive consumers may opt for less expensive, non-certified alternatives.

By Type Analysis

Coffee dominated the Hot Drinks Market in 2023, driven by consumer preferences.

In 2023, Coffee held a dominant market position in the By Type segment of the Hot Drinks Market. Coffee accounted for the largest share, driven by a growing consumer preference for specialty coffee and the proliferation of coffee shops globally. The segment's growth can be attributed to the increasing demand for premium and convenient coffee products, such as single-serve pods and ready-to-drink (RTD) coffee beverages. Technological advancements in coffee brewing and a shift towards sustainable sourcing practices have also played significant roles in boosting the coffee market.

Tea ranked second, experiencing robust growth due to rising health consciousness among consumers. The demand for herbal and specialty teas, particularly green and matcha tea, has seen a significant uptick. Tea's versatility, offering various flavors and health benefits, has enhanced its appeal across diverse demographics.

Others in the segment, which include hot chocolate, malted drinks, and other traditional beverages, maintained a steady market presence. These drinks are particularly popular among younger consumers and in regions with strong cultural preferences for specific hot drinks. Innovations in flavor and packaging have helped sustain their market share.

By Distribution Channel Analysis

In 2023, Hypermarkets and Supermarkets dominated the hot drinks market distribution.

In 2023, Hypermarkets and Supermarkets held a dominant market position in the distribution channel segment of the hot drinks market. This dominance can be attributed to the wide availability and accessibility of hot drink products in these retail environments, where consumers prefer the convenience of one-stop shopping. Hypermarkets and supermarkets cater to a broad consumer base, offering a vast range of hot drink options, from premium brands to budget-friendly choices, thus appealing to diverse consumer preferences.

Department stores also play a significant role in the distribution of hot drinks, particularly in urban areas, where they provide a premium shopping experience and often feature exclusive or high-end brands. Coffee shops, meanwhile, are crucial for the on-the-go consumer, providing freshly brewed hot drinks and becoming increasingly popular as social hubs.

The online distribution channel has witnessed substantial growth, driven by the convenience of home delivery and the rising trend of e-commerce platforms. Consumers are increasingly turning to online platforms for purchasing their favorite hot drinks, benefiting from easy price comparisons and a wide selection of products. Lastly, other channels, including specialty stores and vending machines, contribute to the market by catering to niche segments and offering unique product experiences.

Key Market Segments

By Type

- Coffee

- Tea

- Others

By Distribution Channel

- Hypermarkets and Supermarkets

- Department Stores

- Coffee Shops

- Online

- Others

Growth Opportunity

Focusing on Premiumization and Specialty Products

The global hot drinks market is poised for significant growth driven by a shift towards premiumization and specialty products. Consumers are increasingly willing to pay a premium for high-quality, ethically sourced hot drinks. This trend is especially notable in the coffee and tea segments, where single-origin and artisanal products are gaining traction. Companies that focus on offering unique, high-quality products are well-positioned to capture market share. For example, the rise of specialty coffee shops and tea boutiques underscores this opportunity, with consumers seeking exceptional taste experiences and sustainable sourcing practices.

Developing Functional and Wellness-focused Products

Another key growth driver is the development of functional and wellness-focused hot drinks. As health and wellness trends continue to influence consumer behavior, there is a growing demand for beverages that offer additional health benefits. Functional hot drinks, such as those enriched with vitamins, minerals, or adaptogens, are becoming increasingly popular. This segment is particularly attractive as it caters to health-conscious consumers looking for beverages that support their overall well-being. Brands that innovate in this space by incorporating functional ingredients can differentiate themselves in a competitive market.

Latest Trends

Increased Demand for Natural and Eco-Responsible Products

The hot drinks market is witnessing a significant shift towards natural and eco-responsible products. Consumers are increasingly prioritizing sustainability and health, driving demand for beverages made with organic ingredients and minimal environmental impact. This trend is propelled by a growing awareness of climate change and health consciousness. Companies are responding by sourcing raw materials sustainably, reducing packaging waste, and obtaining certifications such as Fair Trade and Organic. The result is a competitive edge for brands that align with these values, fostering loyalty and enhancing market share.

Expansion of Tea Varieties and Flavors

The diversification of tea varieties and flavors is another prominent trend shaping the hot drinks market. Traditional tea categories are expanding to include innovative blends and exotic flavors, catering to an adventurous consumer base seeking new experiences. Herbal teas, functional teas infused with health benefits, and specialty teas from different regions are gaining traction. This expansion is supported by advancements in flavor extraction and blending techniques, enabling brands to offer unique and appealing products. The proliferation of specialty tea shops and online platforms further facilitates consumer access to these diverse offerings, driving growth in this segment.

Regional Analysis

North America dominates the hot drinks market with a 35% largest share.

The global hot drinks market exhibits significant regional variation, driven by diverse consumer preferences and purchasing power. In North America, the market is robust, characterized by a high demand for premium coffee and specialty teas. The region commands approximately 35% of the global largest market share, driven by a strong coffee culture in the United States and Canada.

Europe follows closely, accounting for around 30% of the market share. Countries like Germany, the UK, and France show a high consumption of both coffee and tea, with a growing trend towards organic and ethically sourced products. The Asia Pacific region is experiencing rapid growth, contributing about 20% to the global market. This growth is propelled by increasing urbanization, rising disposable incomes, and a growing middle class in countries like China, India, and Japan.

In the Middle East & Africa, the market holds approximately 10% of the share, with a notable preference for traditional hot beverages such as tea and coffee, alongside an emerging market for premium brands. Latin America represents around 5% of the market, driven largely by Brazil's significant coffee production and consumption.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global hot drinks market in 2024 is poised for robust growth, driven by a diverse array of key players, each contributing unique strengths and strategic initiatives.

The Coffee Bean & Tea Leaf and Harney & Sons Fine Teas are expected to maintain their strong presence with premium offerings, leveraging their established brand loyalty and expanding their product lines to include healthier and organic options. Unilever and Nestlé SA, giants in the consumer goods sector, are anticipated to further innovate in product formulations and sustainable practices, aligning with the increasing consumer demand for eco-friendly products.

Gourmesso and Dualit will likely continue to capitalize on the growing popularity of convenient, high-quality single-serve coffee pods, while Dilmah Ceylon Tea Company PLC and Ippodo Tea Co. Ltd. focus on their rich heritage and premium tea offerings to attract discerning tea enthusiasts.

New entrants such as Tranquini, Chillbev, Som Sleep, and Phi Drinks, Inc. are expected to disrupt the market with their wellness-focused beverages, catering to the rising trend of functional drinks that promote relaxation and health benefits.

Associated British Foods and JAB Holding will likely strengthen their market position through strategic acquisitions and expanding their product portfolios. At the same time, Food Empire Holdings, Starbucks Corporation and Tchibo continue to explore emerging markets and diversify their offerings.

Overall, the competitive landscape of the hot drinks market in 2024 will be marked by innovation, sustainability, and a keen focus on consumer preferences, driven by these key players' strategic initiatives and market adaptations.

Market Key Players

- The Coffee Bean & Tea Leaf

- Unilever

- Gourmesso

- Harney & Sons Fine Teas

- Dualit

- Nestlé SA

- Dilmah Ceylon Tea Company PLC

- Ippodo Tea Co. Ltd.

- Tranquini

- Chillbev

- Som Sleep

- Phi Drinks, Inc.

- BevNet.com

- Associated British Foods

- JAB Holding

- Food Empire Holdings

- Starbucks Corporation

- Tchibo

Recent Development

- In May 2024, The Kraft Heinz Company debuted a new line of functional teas under its Tassimo brand. These teas are infused with ingredients designed to boost energy, enhance relaxation, and support immune health, aligning with the increasing consumer interest in health and wellness.

- In April 2024, Unilever launched a new initiative focused on sustainable packaging for its hot drinks products, particularly for its Lipton and Brooke Bond tea brands. The initiative includes the introduction of fully recyclable packaging materials and aims to reduce plastic waste significantly.

- In March 2024, Nestlé announced the expansion of its plant-based hot drinks portfolio. The company introduced new variants of its popular brands, including plant-based options for Nescafé and Starbucks at Home products. This move caters to the growing demand for vegan and plant-based beverages.

Report Scope

Report Features Description Market Value (2023) USD 205.2 Billion Forecast Revenue (2033) USD 372.3 Billion CAGR (2024-2032) 6.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Coffee, Tea, Others), By Distribution Channel (Hypermarkets and Supermarkets, Department Stores, Coffee Shops, Online, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape The Coffee Bean & Tea Leaf, Unilever, Gourmesso, Harney & Sons Fine Teas, Dualit, Nestlé SA, Dilmah Ceylon Tea Company PLC, Ippodo Tea Co. Ltd., Tranquini, Chillbev, Som Sleep, Phi Drinks, Inc., BevNet.com, Associated British Foods, JAB Holding, Food Empire Holdings, Starbucks Corporation, Tchibo Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- The Coffee Bean & Tea Leaf

- Unilever

- Gourmesso

- Harney & Sons Fine Teas

- Dualit

- Nestlé SA

- Dilmah Ceylon Tea Company PLC

- Ippodo Tea Co. Ltd.

- Tranquini

- Chillbev

- Som Sleep

- Phi Drinks, Inc.

- BevNet.com

- Associated British Foods

- JAB Holding

- Food Empire Holdings

- Starbucks Corporation

- Tchibo

Our Clients

View Our Licence Options