Fiberglass Roving Market Report By Type (E-glass , H-glass , ECR-glass , S-glass , Other Types), By Processing Technique (Hand Lay-Up , Spray-Up , Filament Winding , Compression Molding , Injection Molding , Pultrusion , Resin Transfer Molding (RTM) , Others), By End-user Industry (Construction and Infrastructure , Transportation , Electrical and Electronics , Pipes and Tanks , Energy , Other End-user Industries), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

7063

-

April 2024

-

290

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

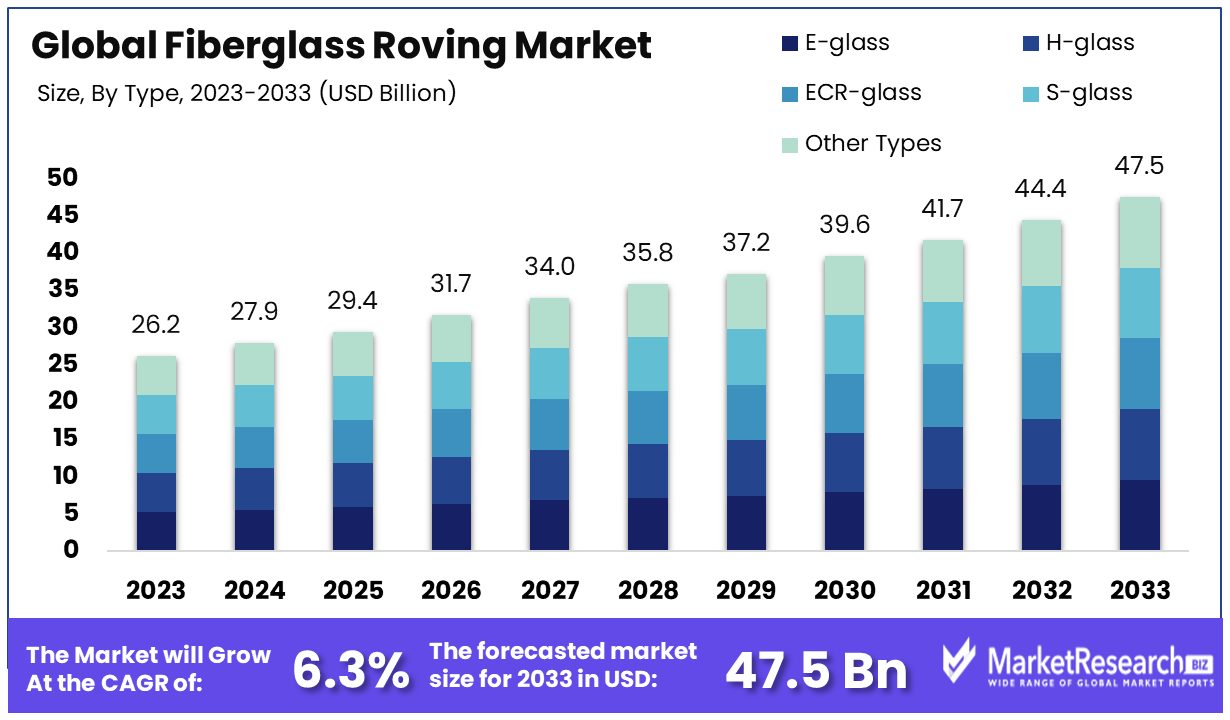

The Global Fiberglass Roving Market size is expected to be worth around USD 47.5 Billion by 2033, from USD 26.2 Billion in 2023, growing at a CAGR of 6.30% during the forecast period from 2024 to 2033.

The surge in demand in the automobile, transportation, electrical, construction, and other applications are some of the main driving factors for the fiberglass roving market. Fibreglass roving is a type of filament that does not require twisting or folding and is one of the general types of glass fiber products. The fiberglass roving can be classified into two segments: alkali-free glass roving and medium-alkali glass roving.

It has an ideal antistatic element, moistness, immersion resistance, banding element, and less furriness, can be hastily and carefully drenched in the resin, and can be used widely. Depending upon the application usage, the fiberglass roving is essentially classified into two more segments, such as the chop roving, which is tough and hard, and the soft roving for woven applications.

These fiberglass rovings have less weight and are sturdy materials that can be used to develop composite elements. It is a perfect choice for several applications due to its strength and lightness. It can also be used to gather panels, gun roving, and other essential products.

Due to its lighter nature, it is easy to transport, and its resistance to erosion makes it an ideal choice for several industrial purposes. Fiberglass roving has multiple uses, such as being used to develop lightweight elements for boats, planes, and cars. This can also be used while manufacturing fiberglass insulation and laminates. Similarly, fiberglass roving is commonly used for soundproofing and fireproofing.

Automobile manufacturers are using fiberglass roving materials in the production and manufacturing of their vehicles. The demand for wind turbines has increased due to growing awareness about the benefits of renewable energy sources. These rovings are used while building multiple mechanical elements of wind turbines that comprise the wind turbine blades. It is also used in the construction domain for the insulation objective.

Fiberglass roving is used in electrical and heat insulation applications in the construction industry. The upsurge requirement for the fiberglass market can be attributed to more spending in the construction field in both developed and developing regions. The demand for fiberglass roving will increase due to its high-end requirements in several industrial sectors, which will help in market expansion in the coming years.

Key Takeaways

Market Value: The Global Fiberglass Roving Market is projected to reach approximately USD 47.5 Billion by 2033, indicating significant growth from USD 26.2 Billion in 2023, with a CAGR of 6.30% during the forecast period from 2024 to 2033.

Dominant Segments:

- Type Analysis: E-glass dominates the fiberglass roving market, holding a substantial share due to its versatile properties and cost-effectiveness. Other types such as H-glass, ECR-glass, and S-glass also contribute significantly, offering specialized properties for specific applications.

- Processing Technique Analysis: Hand Lay-Up leads the processing techniques segment, prized for its flexibility and customization capabilities, particularly in producing large or complex shapes. While automated processes like filament winding and RTM are gaining traction for high-volume production, hand lay-up remains essential for custom projects and small production runs.

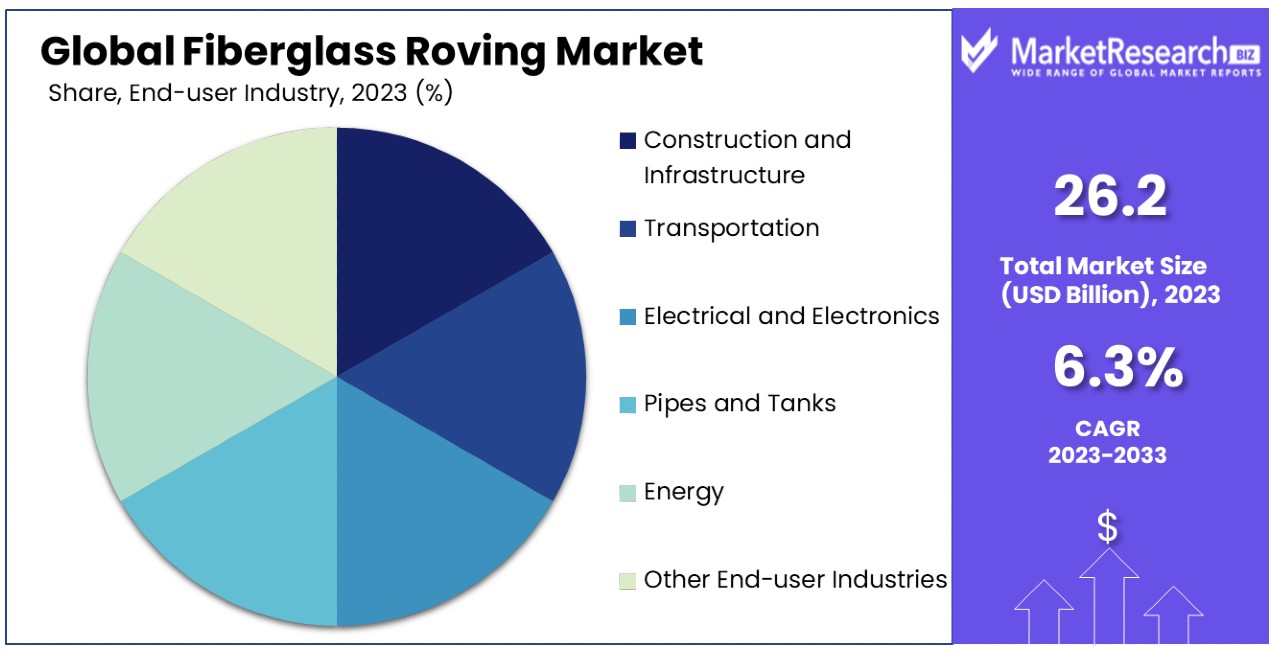

- End-user Industry Analysis: The Construction and Infrastructure sector drives market growth, leveraging fiberglass rovings for reinforcing materials due to their strength, lightweight, and resistance to corrosion and fatigue. Transportation and Energy sectors also show significant demand, driven by the need for lightweight materials in vehicles and wind turbine blades, respectively.

Regional Insights:

- North America: Dominates the market with a 32% share, owing to advanced industries and sustainability efforts, highlighting its key role in driving market growth.

- Europe: Holds approximately 28% of the market, supported by stringent environmental regulations and a significant shift in the automotive industry towards lightweight materials.

Analyst Viewpoint: Analysts foresee continued growth in the fiberglass roving market, driven by the versatility of E-glass, increasing demand from the construction and transportation sectors, and advancements in processing techniques. Additionally, sustainability efforts and stringent regulations in regions like North America and Europe are expected to further propel market expansion.

Growth Opportunities:

- Innovation in Materials: Research and development in fiberglass materials to enhance performance and sustainability.

- Expansion in Emerging Markets: Penetrating emerging regions with tailored solutions to capitalize on growing demand.

- Customization and Personalization: Offering customized products to meet specific application requirements.

Driving Factors

Increasing Demand from the Construction Industry Drives Market Growth

The construction industry stands as a pivotal force propelling the fiberglass roving market forward. Fiberglass-reinforced polymer (FRP) composites, celebrated for their superior strength-to-weight ratio, corrosion resistance, and enduring quality, are increasingly employed across a broad spectrum of construction applications, including reinforcement bars, panels, gratings, and ladders. This surge in utilization is closely tied to the escalating pace of urbanization and the expansion of infrastructure development projects, especially within burgeoning economies.

Statistical insights underscore the burgeoning demand: the global construction market is projected to escalate at a CAGR of approximately 4% from 2023 to 2033. This growth trajectory is mirrored in the fiberglass roving market, which is anticipated to experience a parallel uplift in demand. The unique attributes of FRP, such as its ability to withstand environmental stresses and its longevity, make it an ideal choice for modern construction endeavors, further cementing its position within the industry.

Growth of the Wind Energy Sector Energizes Market Expansion

The wind energy sector's rapid ascension as a key consumer of fiberglass rovings marks a significant chapter in the market's expansion story. Fiberglass-reinforced composites, prized for their lightweight, high strength, and fatigue resistance properties, are integral to the fabrication of wind turbine blades. The global shift towards renewable energy, with wind power at its vanguard, predicates a substantial surge in demand for wind turbines and, by extension, for fiberglass rovings.

Current statistics reveal a compelling growth narrative: the wind energy market is forecasted to grow at a CAGR of over 7% through the next decade, signaling robust demand for fiberglass rovings. This demand is fueled not only by the sector's expansion but also by the evolving design and engineering standards of wind turbine blades, which increasingly rely on fiberglass composites for enhanced performance and longevity.

Increasing Adoption in the Automotive Industry Accelerates Market Growth

The automotive industry's shift towards fiberglass-reinforced composites underscores a strategic pivot aimed at achieving weight reduction and fuel efficiency improvements in vehicles. Fiberglass rovings, employed in the production of various automotive components such as body panels, interior components, and structural reinforcements, are at the forefront of this transformation. The industry's growing preference for lightweight and high-performance materials is a direct response to stringent environmental regulations and consumer demand for more fuel-efficient vehicles.

Statistical evidence supports this trend, with the automotive sector projected to register significant growth, partly fueled by the adoption of fiberglass composites. The global automotive composites market, within which fiberglass rovings play a crucial role, is expected to witness a CAGR of approximately 6.5% from 2021 to 2028. This growth is indicative of the broader trend towards lightweight materials, which not only enhance vehicle performance but also contribute to the reduction of carbon emissions.

Restraining Factors

Availability and Price Volatility of Raw Materials Restrains Market Growth

The production of fiberglass rovings depends significantly on the steady supply and pricing of essential raw materials, including glass fibers and sizing chemicals. Fluctuations in these factors can lead to increased costs for manufacturers, which may then be passed on to consumers, affecting the market's competitive edge. For instance, any disruption in the supply chain, such as geopolitical tensions or trade restrictions, can lead to shortages of key raw materials. This not only escalates the price but also interrupts production schedules, posing significant challenges for the fiberglass roving market.

Recent trends indicate a notable volatility in raw material prices, influenced by global economic conditions and environmental regulations. This unpredictability complicates budgeting and operational planning for manufacturers, potentially deterring investment in the sector. Additionally, the reliance on specific raw materials exposes the market to risks associated with their availability, further inhibiting growth potential in an increasingly competitive landscape.

Competition from Alternative Reinforcement Materials Restrains Market Growth

Alternative reinforcement materials, including carbon fibers, aramid fibers, and natural fibers, present a formidable challenge to the fiberglass roving market. These competitors, often boasting superior strength, lighter weight, or more environmentally friendly profiles, can edge out fiberglass rovings in certain applications. For example, in high-performance automotive and aerospace sectors, carbon fibers are preferred for their exceptional strength-to-weight ratio, despite their higher cost.

The competitive pressure is exacerbated by ongoing innovation and cost optimization in the production of alternative materials, making them more accessible and appealing to a broader range of applications. As a result, fiberglass rovings must continuously evolve to maintain their market position, necessitating significant investment in research and development.

Statistics reflect this competitive tension, with markets for alternative fibers growing at a steady pace. For instance, the carbon fiber market is projected to expand at a CAGR of over 9% in the coming years, signaling increasing preference and potential displacement of traditional materials like fiberglass in some sectors. This competitive landscape underscores the need for the fiberglass roving industry to adapt and innovate to sustain growth amidst the challenges posed by alternative reinforcement materials.

Type Analysis

E-glass Dominates Fiberglass Roving Market with Versatility and Cost-effectiveness

In the Fiberglass Roving Market, the "By Type" segment showcases E-glass as its dominant sub-segment, with H-glass, ECR-glass, S-glass, and other types also contributing to market dynamics. E-glass rovings are predominant due to their excellent balance of mechanical properties, cost-effectiveness, and electrical insulating characteristics, making them highly desirable across various applications. They are particularly favored in the construction and infrastructure, transportation, and energy sectors for products like reinforcement materials, vehicle parts, and wind turbine blades.

E-glass's dominance is underpinned by its widespread availability and the continuous advancement in manufacturing techniques that enhance its performance and application scope. The versatility of E-glass, coupled with its cost efficiency, positions it as a preferred choice for manufacturers seeking to optimize product performance while maintaining economic viability. The demand for E-glass is further bolstered by the global push towards more sustainable and energy-efficient materials, given its role in producing lightweight and durable composite materials.

Although E-glass holds a significant share, the importance of other types such as H-glass, ECR-glass, and S-glass cannot be understated. These variants offer superior properties for specific applications that require enhanced strength, corrosion resistance, or thermal stability. For instance, S-glass is sought after in defense and aerospace applications for its high tensile strength, whereas ECR-glass is preferred in environments where corrosion resistance is critical.

Processing Technique Analysis

Processing Techniques in Fiberglass Roving Market: Hand Lay-Up Leads with Flexibility and Customization

Within the "By Processing Technique" segment, Hand Lay-Up emerges as a significant method, sharing the stage with Spray-Up, Filament Winding, Compression Molding, Injection Molding, Pultrusion, and Resin Transfer Molding (RTM), among others. The hand lay-up technique is widely used due to its simplicity, low cost, and flexibility in producing large or complex shapes, making it especially prevalent in the manufacturing of boats, recreational vehicles, and custom automotive components.

This method's dominance is attributed to its straightforward application, which does not require expensive machinery or molds, allowing for greater design versatility and customization. The ability to adjust the fiber orientation and laminate thickness manually provides manufacturers with control over the mechanical properties of the final product, an essential factor in bespoke or specialized applications.

Despite its advantages, the labor-intensive nature of the hand lay-up process and the quest for increased efficiency have led to the development and adoption of automated processes like filament winding and RTM for high-volume production. Nonetheless, the hand lay-up technique remains indispensable for custom projects and small production runs, where its flexibility and cost-effectiveness are unrivaled.

End-user Industry Analysis

Construction and Infrastructure Drive Fiberglass Roving Market Growth, Transportation and Energy Sectors Follow Suit

In the "By End-user Industry" category, the Construction and Infrastructure segment stands out, with Transportation, Electrical and Electronics, Pipes and Tanks, Energy, and other industries also playing vital roles. The construction and infrastructure sector's lead is driven by the extensive use of fiberglass rovings in reinforcing materials, such as in the production of rebar, panels, and gratings, which benefit from the material's strength, lightweight, and resistance to corrosion and fatigue.

The adoption of fiberglass rovings in construction is closely linked to the industry's shift towards more sustainable and resilient building practices. The material's durability and maintenance-free characteristics make it an attractive alternative to traditional construction materials, contributing to energy-efficient buildings and infrastructure.

While the construction sector commands a significant portion of the market, the transportation and energy sectors are also notable for their increasing use of fiberglass rovings. In transportation, the emphasis on lightweight materials for fuel efficiency and performance has spurred the use of fiberglass in vehicles. Similarly, the energy sector's focus on renewable sources has elevated the demand for fiberglass rovings in wind turbine blades, highlighting the material's cross-industry appeal and versatility.

Key Market Segments

By Type

- E-glass

- H-glass

- ECR-glass

- S-glass

- Other Types

By Processing Technique

- Hand Lay-Up

- Spray-Up

- Filament Winding

- Compression Molding

- Injection Molding

- Pultrusion

- Resin Transfer Molding (RTM)

- Others

By End-user Industry

- Construction and Infrastructure

- Transportation

- Electrical and Electronics

- Pipes and Tanks

- Energy

- Other End-user Industries

Growth Opportunities

Development of High-Performance and Specialty Rovings Offers Growth Opportunity

The creation of high-performance and specialty fiberglass rovings represents a significant avenue for market expansion. By engineering rovings with advanced materials, coatings, or surface treatments, manufacturers can achieve superior properties such as enhanced strength, chemical resistance, or thermal stability. These innovations allow fiberglass rovings to meet the rigorous demands of industries like aerospace, automotive, and energy.

Companies like Owens Corning and Nippon Electric Glass have already made strides in this direction, producing specialty rovings for use in extreme environments. This specialization not only meets the unique needs of these industries but also commands higher prices, contributing to market growth. As industries continue to evolve and require more from their materials, the demand for these specialized rovings is expected to increase, highlighting their potential to drive significant market opportunities.

Sustainable and Recycled Fiberglass Roving Solutions Offer Growth Opportunity

The shift towards sustainability and the rising environmental concerns present a lucrative opportunity for the fiberglass roving market. Developing sustainable and recycled fiberglass roving solutions is becoming increasingly important. Manufacturers that incorporate recycled fiberglass or bio-based materials into their products can tap into the growing segment of environmentally conscious consumers and industries looking for eco-friendly materials.

Moreover, investing in recycling technologies and advocating for closed-loop production processes not only reduces waste but also supports a circular economy. This approach not only positions companies as sustainable leaders but also meets regulatory requirements and consumer expectations for environmental stewardship. As the global focus on sustainability intensifies, the demand for these eco-friendly solutions is expected to rise, offering a clear path for growth in the fiberglass roving market.

Trending Factors

Lightweighting and Fuel Efficiency Are Trending Factors

The drive towards lightweighting and fuel efficiency has become a dominant trend in the fiberglass roving market, especially within the automotive and transportation industries. This trend is a response to the global push for reduced emissions and improved fuel economy, with manufacturers increasingly opting for lightweight composite materials reinforced by fiberglass rovings.

Notably, in the electric and hybrid vehicle sectors, weight reduction is pivotal for enhancing battery range and performance. As such, the demand for fiberglass rovings, known for their lightweight properties, is expected to rise, signifying their vital role in meeting both regulatory requirements and consumer expectations for more efficient, eco-friendly vehicles.

Integration of Advanced Manufacturing Technologies Are Trending Factors

The adoption of advanced manufacturing technologies marks a significant trend within the fiberglass roving market. Automation, robotics, and the principles of Industry 4.0 are being leveraged to streamline production processes, elevate quality control, and minimize waste.

Techniques like automated fiber placement (AFP) and automated tape laying (ATL) facilitate the precise placement of fiberglass rovings, allowing for the creation of complex structures and optimized material performance. This integration not only enhances efficiency and product quality but also positions manufacturers to better meet the evolving demands of industries seeking innovative composite solutions.

Emphasis on Product Traceability and Certification Are Trending Factors

An increasing focus on product traceability and certification is shaping trends in the fiberglass roving market. As industries face stricter quality and safety standards, manufacturers are implementing sophisticated tracking systems and achieving certifications like ISO and REACH to document and verify the origin, production, and quality of their products.

This trend reflects the growing demand for transparency and assurance of compliance with regulatory standards. It not only ensures the reliability and safety of fiberglass rovings but also strengthens customer trust, further driving the market's expansion by aligning with the heightened expectations for product excellence and regulatory adherence.

Regional Analysis

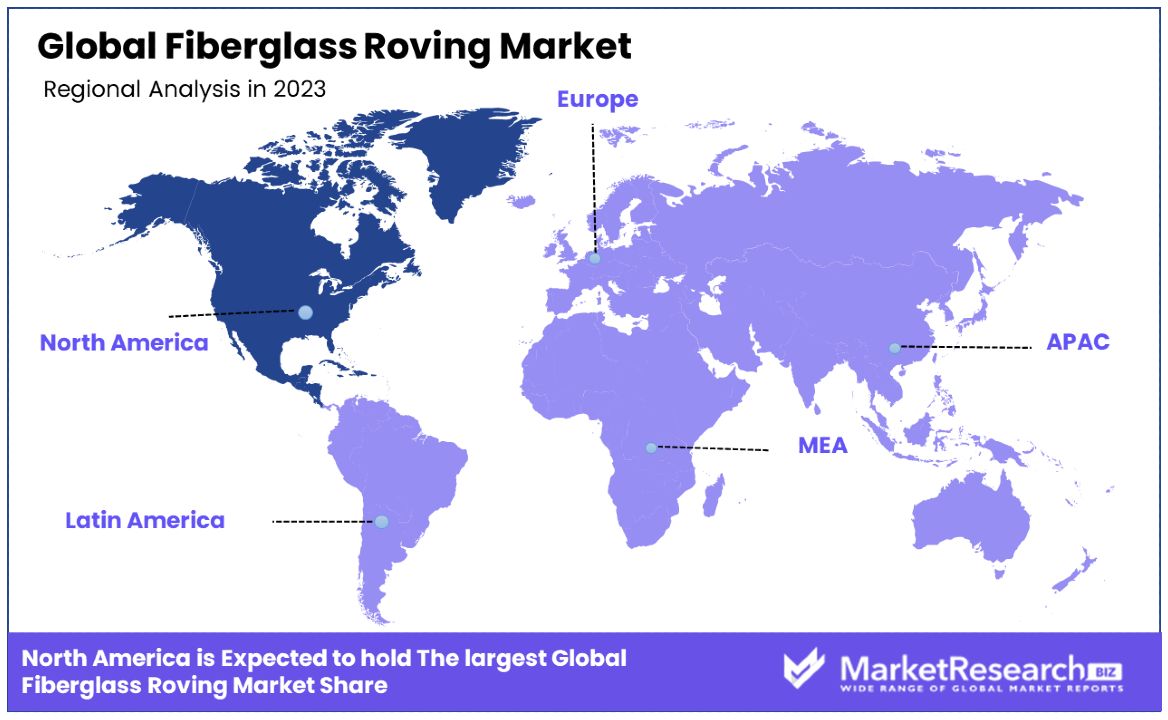

North America Dominates with 32% Market Share

North America's commanding 32% share of the Fiberglass Roving Market is propelled by its robust automotive and aerospace industries, which are keen adopters of fiberglass roving for lightweighting and strength. The region's emphasis on renewable energy, particularly wind power, further fuels demand for fiberglass rovings in turbine blade manufacturing. Advanced manufacturing technologies and a strong regulatory framework supporting sustainability and energy efficiency also contribute to the market's strength in this region.

The dynamics of the North American market are influenced by its technological leadership, the presence of key industry players, and a market-driven approach to innovation in materials science. The region's advanced infrastructure for research and development allows for rapid adaptation to evolving industry requirements, reinforcing its dominant position.

North America is expected to maintain its lead in the Fiberglass Roving Market due to ongoing investments in technology and renewable energy. The region's commitment to reducing carbon emissions and the automotive industry's shift towards electric vehicles are likely to keep demand for fiberglass rovings buoyant. However, competition from emerging markets, especially in Asia Pacific, may challenge this dominance in the future.

Regional Market Shares and Growth:

Europe:

Europe holds approximately 28% of the market, supported by stringent environmental regulations and a significant shift in the automotive sector toward electric vehicles. This transition is spurring demand for new technologies and materials. Europe's focus on reducing carbon emissions across various industries, coupled with substantial investments in technology and infrastructure, reinforces its strong market position while aligning with broader sustainability goals.

Asia Pacific:

The Asia Pacific region claims about 27% of the market, driven by rapid growth in infrastructure projects and an escalating commitment to renewable energy sources. This region's expansion is further supported by government initiatives and investments in technology that facilitate the adoption of sustainable practices. The growing industrial base, coupled with increasing urbanization and economic development, continues to propel the market forward.

Middle East & Africa:

Holding around 7% of the market, the Middle East and Africa are experiencing growth primarily through extensive infrastructure development and a focused expansion of the renewable energy sector. These initiatives are often supported by governmental policies aimed at diversifying the economy and reducing dependence on oil, thus fostering a more sustainable and stable market environment.

Latin America:

Latin America, with a 6% market share, shows promising potential for growth, particularly in the automotive and construction industries. Emerging economies within the region are increasingly investing in these sectors, which are pivotal for regional development. This growth is driven by both local demand and an increasing focus on integrating more sustainable practices and technologies, positioning Latin America as an emerging player in the global market.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the fiberglass roving market, key players demonstrate diverse strategic positioning and market influence. Companies like Johns Manville Corporation and Saint-Gobain Vetrotex lead with robust global distribution networks and a focus on innovation and quality.

Asian manufacturers such as China Jushi Co., Ltd., and Taishan Fiberglass Inc., dominate in terms of production volume, benefiting from regional growth in construction and automotive sectors. Nippon Electric Glass and Taiwan Glass Industry Corporation specialize in high-performance products for electronics and industrial applications, respectively.

Firms like Nitto Boseki Co. and AGY Holding Corporation focus on niche markets with specialized products, enhancing their competitive edge. Meanwhile, newer entrants like Chongqing Polycomp International Corp and China Beihai Fiberglass Co., Ltd., are expanding rapidly, leveraging local manufacturing advantages. Collectively, these companies drive the market through strategic expansions, technological advancements, and strong customer relationships, shaping industry dynamics and future growth trajectories.

Market Key Players

- Johns Manville Corporation

- Nitto Boseki Co.

- Chongqing Polycomp International Corp.

- Taishan Fiberglass Inc.

- China Jushi Co., Ltd.

- Nippon Electric Glass Co., Ltd.

- Nitto Boseki Co., Ltd.

- Chomarat Group

- Binani Industries Ltd

- AGY Holding Corporation

- China Beihai Fiberglass Co., Ltd.

- Taiwan Glass Industry Corporation

- Jushi Group Co., Ltd.

- PFG Fiberglass Corporation

- Saint-Gobain Vetrotex

Recent Developments

- On May 2023, AGY Holding Corp.'s plant in Aiken, South Carolina, plays a crucial role in producing glass fiber used in a wide range of applications, including aircraft, automobile exhaust and ignition systems, surfboards, and handheld electronic devices. The facility, spanning 1.4 million square feet and employing approximately 700 individuals, is a significant contributor to the local economy.

- On July 2023, the fiberglass manufacturing industry in Egypt is highlighted for its significant contributions to the country's economic development. Jushi Egypt, a subsidiary of the Chinese fiberglass giant, has been operating in Egypt for over a decade, providing employment opportunities and career growth for many local employees.

- On May 2022, Jiangsu Changhai Composite Materials, a Chinese producer of glass-fiber-based composite materials, announced a significant upgrade to one of its glass fiber production lines. Changzhou Tianma Group Co., Ltd. (Tianma), a wholly-owned subsidiary of the company, intends to expand production capacity, optimize product performance, and improve the company's industrial chain layout.

Report Scope

Report Features Description Market Value (2023) USD 26.2 Billion Forecast Revenue (2033) USD 47.5 Billion CAGR (2024-2033) 6.30% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (E-glass , H-glass , ECR-glass , S-glass , Other Types), By Processing Technique (Hand Lay-Up , Spray-Up , Filament Winding , Compression Molding , Injection Molding , Pultrusion , Resin Transfer Molding (RTM) , Others), By End-user Industry (Construction and Infrastructure , Transportation , Electrical and Electronics , Pipes and Tanks , Energy , Other End-user Industries) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Johns Manville Corporation, Nitto Boseki Co., Chongqing Polycomp International Corp., Taishan Fiberglass Inc., China Jushi Co., Ltd., Nippon Electric Glass Co., Ltd., Nitto Boseki Co., Ltd., Chomarat Group, Binani Industries Ltd, AGY Holding Corporation, China Beihai Fiberglass Co., Ltd., Taiwan Glass Industry Corporation, Jushi Group Co., Ltd., PFG Fiberglass Corporation, Saint-Gobain Vetrotex Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Johns Manville Corporation

- Nitto Boseki Co.

- Chongqing Polycomp International Corp.

- Taishan Fiberglass Inc.

- China Jushi Co., Ltd.

- Nippon Electric Glass Co., Ltd.

- Nitto Boseki Co., Ltd.

- Chomarat Group

- Binani Industries Ltd

- AGY Holding Corporation

- China Beihai Fiberglass Co., Ltd.

- Taiwan Glass Industry Corporation

- Jushi Group Co., Ltd.

- PFG Fiberglass Corporation

- Saint-Gobain Vetrotex

Our Clients

View Our Licence Options