Edge Data Center Market By Component(Solution, Services), By Enterprise Size ( SMEs, Large Enterprises) By Industry Vertical,(IT & Telecom, Manufacturing, Government & Public Sector, Healthcare, Automotive, BFSI, Gaming & Entertainment, Other Industry Verticals), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

51315

-

Sept 2024

-

215

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

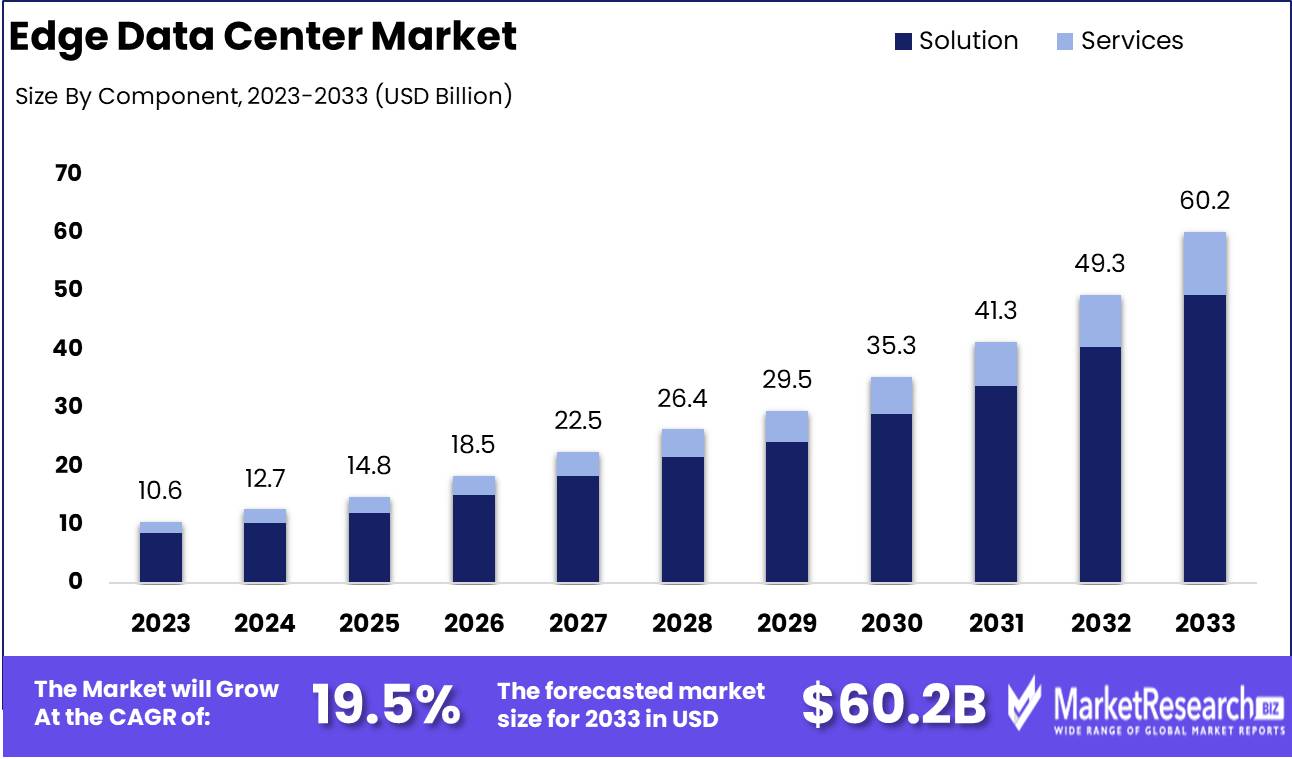

The Edge Data Center Market was valued at USD 10.6 billion in 2023. It is expected to reach USD 60.2 billion by 2033, with a CAGR of 19.5% during the forecast period from 2024 to 2033.

The Edge Data Center Market is a rapidly expanding segment of the broader data infrastructure landscape, driven by the increasing need for real-time data processing and low-latency solutions. Edge data centers are decentralized facilities strategically located closer to end-users or devices, facilitating faster data handling and reducing reliance on traditional centralized data centers. This shift is largely fueled by the rise of artificial intelligence (AI), the Internet of Things (IoT), and 5G networks, all of which demand high-speed processing at the network of edge data. As organizations prioritize greater agility, scalability, and cost-efficiency in managing their data needs, edge data centers industry are becoming integral to transforming modern IT and digital infrastructures

The edge data center market is undergoing a rapid transformation, driven by increasing demand for low-latency applications, data-intensive services, and advancements in 5G networks. Edge data centers decentralized facilities that process data closer to the source are becoming critical to supporting industries like telecommunications, healthcare, and cloud computing.

As businesses seek to improve efficiency and enhance user experience, the edge infrastructure allows for faster processing of data, minimizing latency, and ensuring seamless connectivity in real-time applications. In particular, the rise of 5G networks is significantly accelerating the need for these edge solutions, with telecom operators investing heavily in infrastructure to support high-bandwidth services. Furthermore, the modular data center solutions that companies like Schneider Electric are investing in, alongside Compass Datacenters, signal a growing trend toward flexible, scalable infrastructures to meet the evolving demands of digital transformation across industries.

Recent strategic initiatives by key industry players underscore the global expansion and importance of edge computing in the data center space. Amazon Web Services’ (AWS) approval for a $205 million data center project in Chile, set for June 2024, highlights the push to expand cloud capabilities in South America, aligning with the broader trend of cloud providers strengthening their global edge presence. Meanwhile, LightEdge’s acquisition of Connectria in April 2024 enhances its multi-cloud infrastructure services, reflecting the industry’s move toward integrated and hybrid cloud solutions.

The joint venture between DigitalBridge and Liberty Global, operating under AtlasEdge, emphasizes the increasing importance of edge computing across Europe, while Dell’s partnership with Airspan in 2023 to develop pre-integrated wireless edge solutions showcases a collaborative approach to meeting the demands of 5G deployment. As these developments unfold, the edge data center market is poised for significant growth, driven by both technological advancements and strategic partnerships that aim to provide scalable, efficient, and low-latency solutions.

Key Takeaways

- Market Growth: The Edge Data Center Market Size is forecasted to grow from USD 10.6 billion in 2023 to USD 60.2 billion by 2033, driven by a robust 19.5% CAGR.

- Analyst Viewpoint Summary: Edge data centers are rapidly transforming IT infrastructures by enabling real-time processing and low-latency applications, essential for IoT, 5G, and AI-driven services.

- By Component : Solution sub-segment dominated with an 82.3% market share in 2023, reflecting the high demand for scalable edge infrastructure solutions.

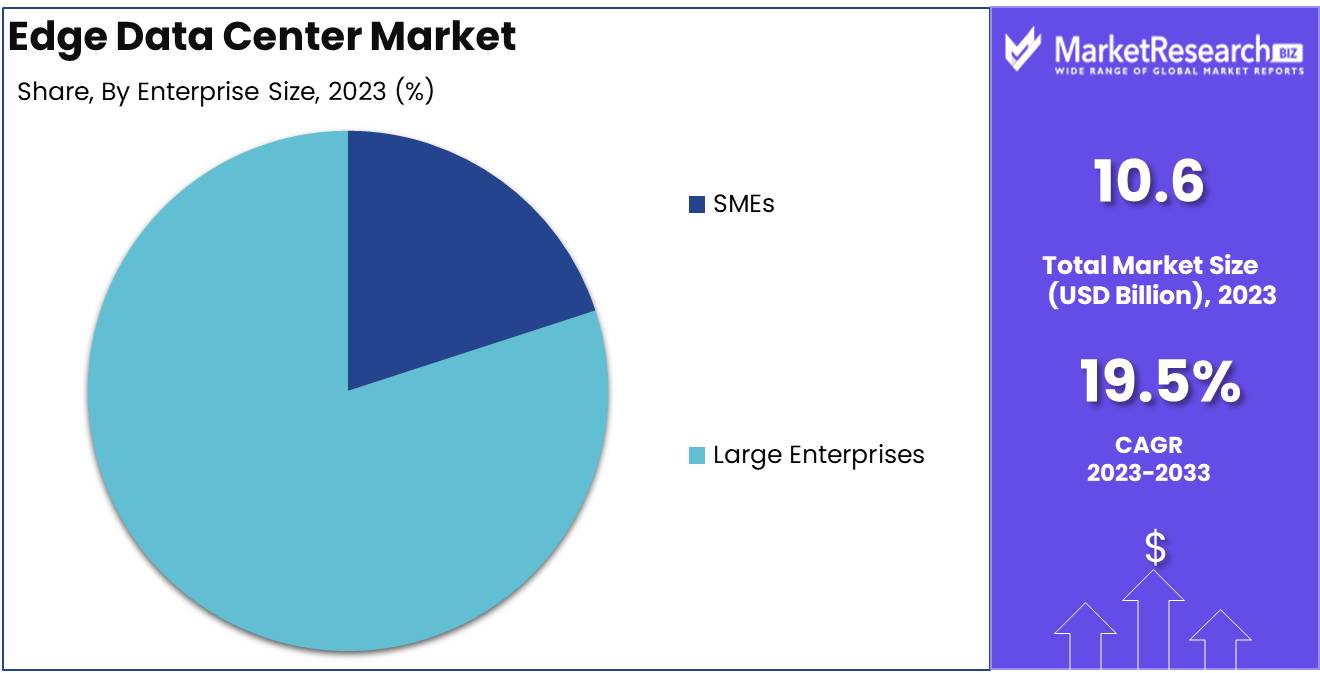

- By Enterprise Size: Large Enterprises dominated with a 79.7% market share in 2023 due to their substantial investments in high-performance edge computing infrastructure.

- By Industry Vertical: IT & Telecom led the market with a 37.3% share in 2023, driven by demand for low-latency data processing and real-time services.

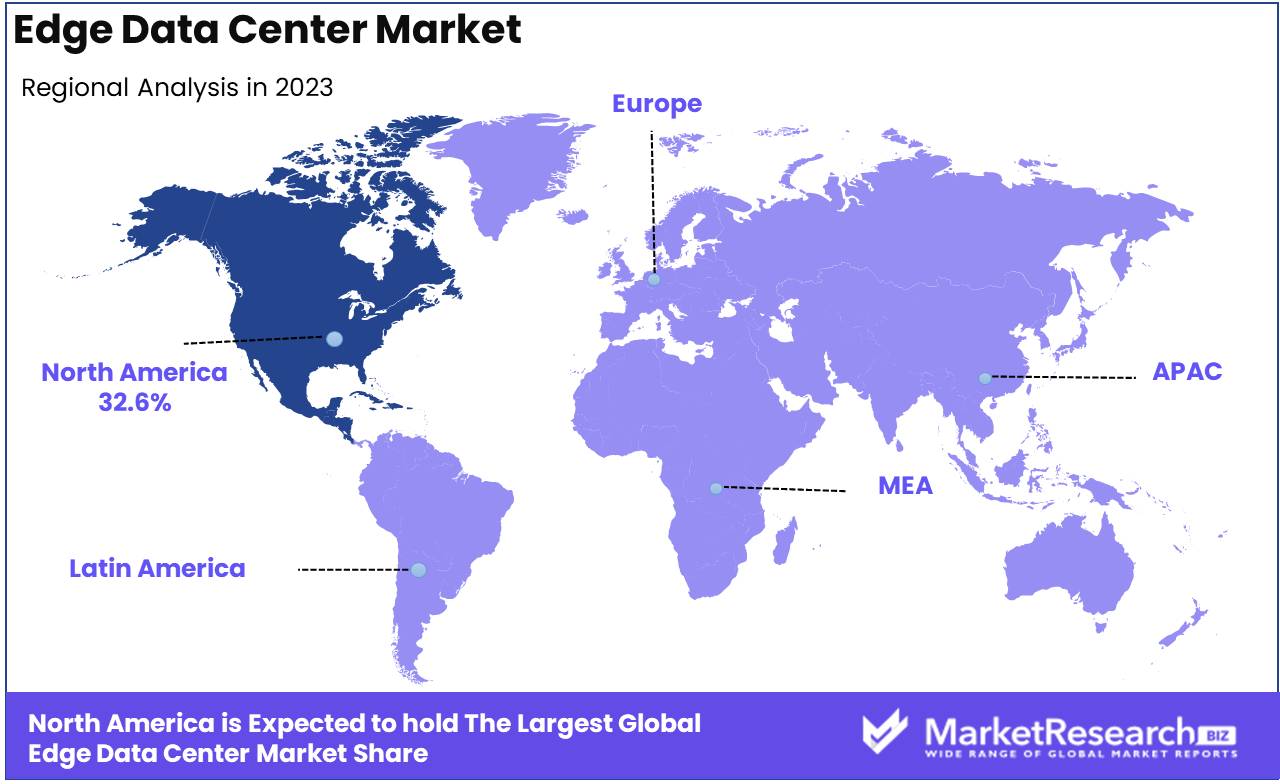

- Regional Growth : North America held a dominant 32.6% market share in 2023, led by advanced IT infrastructure and the proliferation of 5G networks.

- Growth Opportunity: The proliferation of IoT devices, projected to surpass 30 billion by 2030, is driving demand for edge data centers that can handle real-time data at the network’s edge.

- Restraining Factor: Infrastructure challenges, including unreliable power and network connectivity in remote areas, remain a significant bottleneck for edge data center expansion.

Driving Factors

Demand for Low Latency

As the demand for real-time data processing continues to rise, low-latency requirements have become a critical driver in the expansion of the edge data center market. Applications such as video streaming, online gaming, augmented reality (AR), and virtual reality (VR) rely on ultra-fast data transmission to ensure seamless user experiences. According to industry reports, latency reductions from edge computing can improve user experience by up to 40%, especially in latency-sensitive sectors like gaming and AR/VR.

Edge data centers, which are located closer to the end-user, play a pivotal role in minimizing delays by processing data closer to its source. This proximity ensures that data does not need to travel back to centralized cloud servers, thereby significantly reducing latency. With AR and VR markets expected to grow at a compound annual growth rate (CAGR) of over 25% in the next five years, edge infrastructure is set to become indispensable. Moreover, industries like telemedicine, autonomous vehicles, and smart cities—where split-second decision-making is crucial—further emphasize the need for low-latency infrastructure, positioning edge data centers as a backbone of future technological ecosystems.

The increasing volume of IoT devices, predicted to reach over 30 billion by 2030, amplifies this trend by generating massive amounts of data that must be processed with minimal delay. As enterprises prioritize real-time insights and data analytics, the demand for edge solutions that ensure low-latency performance will continue to drive market growth.

5G Deployment

The global rollout of 5G networks is reshaping the digital landscape and serving as a major catalyst for the edge data center market. 5G’s ultra-low latency and high-bandwidth capabilities enable data-heavy applications like autonomous vehicles, smart manufacturing, and advanced mobile services. The synergy between 5G and edge computing lies in their shared objective of minimizing latency while supporting real-time data processing. Current estimates suggest that 5G infrastructure investments will reach $2.7 trillion by 2035, underscoring the scale of telecom operators' commitments to this technology.

As 5G proliferates, the need for edge data centers becomes critical for managing the surge in data traffic and ensuring the performance of next-generation applications. Telecom operators are partnering with cloud providers and edge computing firms to establish distributed networks of edge data centers, ensuring that high-performance, low-latency computing is available to businesses and consumers alike.

Additionally, the integration of 5G and edge data centers supports advancements in smart cities, industrial IoT, and healthcare by enabling real-time analytics and decision-making. The global smart city market, for example, is projected to grow at a CAGR of 18%, with 5G-enabled edge infrastructure playing a foundational role in supporting services such as traffic management, energy optimization, and public safety. As these applications expand, edge data centers will become essential in managing decentralized data workloads, positioning them at the forefront of digital transformation across industries.

Restraining Factors

Infrastructure Challenges

Infrastructure challenges represent another key factor limiting the rapid growth of the edge data center market. Edge data centers, by design, need to be deployed in close proximity to end-users to deliver low-latency services. However, establishing these facilities in remote or underserved areas—where demand for edge computing is highest—requires significant investment in local infrastructure such as power grids, network connectivity, and cooling systems.

The global edge data center market is projected to grow from $5.3 billion in 2021 to $19.7 billion by 2026, yet this expansion is heavily contingent on addressing these infrastructure gaps. For instance, lack of reliable power sources in emerging markets adds substantial risk and cost to edge deployments. Many rural or industrial areas, which would benefit most from edge computing, do not have the necessary fiber or network bandwidth to support these data centers. This results in a concentration of edge facilities in urban areas, limiting their broader utility.

Moreover, edge data centers often require advanced cooling technologies to function efficiently, especially in areas with extreme weather conditions. The absence of cost-effective, scalable solutions for these challenges is further complicating large-scale rollouts. Companies may also face regulatory hurdles when constructing new facilities, as zoning laws or environmental concerns can delay projects and increase capital expenditure.

Combined Impact

Standardization and interoperability issues, along with infrastructure challenges, create a compounded effect that significantly slows the edge data center market’s ability to scale efficiently. The technical fragmentation caused by a lack of uniform standards increases costs and complexity, while the infrastructural barriers impede the physical deployment of edge facilities where they are most needed. Together, these factors act as a bottleneck to the widespread adoption of edge data centers across industries and geographies.

Overcoming these challenges will require collaborative efforts from all stakeholders, including technology vendors, governments, and regulatory bodies. Standardization efforts that reduce integration costs and enhance operational compatibility, coupled with targeted investments in infrastructure, will be pivotal in unlocking the full potential of the edge data center market in the coming years. Without addressing these foundational issues, the market’s anticipated growth trajectory could face significant setbacks, slowing innovation and limiting the benefits of edge computing in emerging sectors such as autonomous vehicles, smart cities, and telemedicine.

By Component Analysis

Solution Segment Dominates the Edge Data Center Market in 2023 with 82.3% Market Share

In 2023, Solution held a dominant market position within the Component segment of the Edge Data Center Market, capturing a significant 82.3% market share. This commanding presence is largely attributed to the growing demand for scalable and efficient data center infrastructure solutions, as enterprises increasingly shift to edge computing to reduce latency and enhance data processing capabilities closer to the source. Solutions such as micro-modular data centers and prefabricated modular solutions have gained traction, offering flexibility and speed of deployment, which are crucial in enabling real-time data processing at the network’s edge.

Meanwhile, the Services segment accounted for the remaining 17.7% of the market. Although smaller in share, the services component is experiencing steady growth, driven by the increasing need for specialized support, maintenance, consulting, and integration services. As organizations continue to navigate the complexities of deploying and managing edge data centers, there is a rising demand for services that ensure operational efficiency and reliability. This trend is expected to accelerate as edge deployments become more complex, requiring tailored service offerings such as managed services, on-site support, and remote monitoring solutions.

Looking ahead, the Services segment is likely to gain momentum as organizations increasingly seek end-to-end solutions that encompass both hardware and long-term operational support. While Solution is expected to maintain its market dominance in the near term, growth opportunities in the Services space will become more pronounced, especially with the expansion of edge ecosystems and the rise of IoT and 5G applications.

By Enterprise Size Analysis

Large Enterprises Dominate Edge Data Center Market with 79.7% Largest Share in 2023

In 2023, Large Enterprises held a dominant market position in the Enterprise Size segment of the Edge Data Center Market, capturing more than 79.7% share. This substantial dominance is attributed to the robust demand for edge computing solutions among large organizations, driven by their need to process vast amounts of data closer to the source. Large enterprises, especially those in industries such as telecommunications, financial services, and manufacturing, are heavily investing in edge data centers to enhance operational efficiency, reduce latency, and improve data security.

The scale of operations in large enterprises often requires high-performance computing infrastructure, which is why edge data centers serve as a strategic asset to streamline operations and support the growing adoption of IoT, 5G, and AI-driven applications. Moreover, these companies have the capital to invest in cutting-edge technology, further fueling their dominance in this segment.

In contrast, Small and Medium Enterprises (SMEs), while steadily increasing their adoption of edge data center solutions, accounted for a significantly smaller market share in 2023. Their contribution remained below 20.3%, primarily due to budget constraints, limited IT resources, and slower technology adoption rates. However, the SME segment is projected to grow over the coming years as the cost of edge computing infrastructure decreases and as cloud service providers offer more tailored solutions that address the specific needs of smaller businesses. Additionally, the increasing digital transformation among SMEs is expected to drive higher demand for localized data processing, positioning them for stronger future growth in the Edge Data Center market.

By Industry Vertical Analysis

IT & Telecom Dominate Edge Data Center Market with 37.3% Largest Share in 2023

In 2023, the IT & Telecom sector commanded a significant presence in the Industry Vertical Size segment of the Edge Data Center Market, securing more than a 37.3% share. This prominent position underscores the pivotal role of IT & Telecom in driving demand for edge computing solutions, attributed to the increasing need for low-latency processing and data storage close to end-users.

Following IT & Telecom, the Manufacturing sector also represented a substantial portion of the market, reflecting the industry's shift towards smart manufacturing and Industry 4.0 technologies, which rely heavily on real-time data processing capabilities provided by edge data centers. The Government & Public Sector followed, leveraging edge data centers to enhance civic operations and public services through improved data accessibility and security.

Healthcare, another key player, utilized edge data centers to expedite medical data processing and support telemedicine, especially in remote diagnostics and patient monitoring, where immediate data processing is crucial. The Automotive sector capitalized on these facilities to bolster innovations in autonomous driving and vehicle-to-everything (V2X) communications.

The BFSI sector employed edge data centers to manage the increasing volume of real-time financial transactions and data analysis, ensuring compliance and enhanced customer service. Meanwhile, the Gaming & Entertainment industries utilized these centers to deliver high-speed content streaming and gaming experiences, reducing latency and improving user engagement.

Key Market Segments

Based On Component

- Solution

- Services

Based on Enterprise Size

- SMEs

- Large Enterprises

Based On Industry Vertical

- IT & Telecom

- Manufacturing

- Government & Public Sector

- Healthcare

- Automotive

- BFSI

- Gaming & Entertainment

- Other Industry Verticals

Growth Opportunity

Growth in IoT and Connected Devices

The proliferation of Internet of Things (IoT) devices and the expansion of connected technology ecosystems are pivotal drivers for the Edge Data Center Market in 2024. As industries continue to integrate IoT solutions at an unprecedented scale ranging from smart home devices to industrial IoT applications—there is a significant surge in data production at the edge of networks. This trend is compelling enterprises to adopt edge data centers to reduce latency and manage data traffic effectively. By processing data closer to its source, edge data centers minimize the strain on core networks and optimize the performance of IoT applications, fostering enhanced operational efficiency.

Real-Time Data Processing and Analytics

Real-time data processing and analytics represent a critical competitive advantage in today's fast-paced business environments. Edge data centers are increasingly crucial in scenarios where rapid data processing is essential to decision-making and operational agility. By enabling quicker access to analytics, businesses can respond more swiftly to market changes, customer needs, and emergent opportunities. This capability is especially beneficial in sectors like healthcare, finance, and manufacturing, where real-time data can result in significant improvements in service delivery, risk management, and production processes.

Latest Trends

Decentralization of Data Management

In 2024, the Edge Data Center Market is significantly influenced by the ongoing decentralization of data management. This trend is driven by the need to manage the voluminous data generated by dispersed geographic locations, particularly in remote and underserved areas. As businesses continue to embrace digital transformation, the decentralization strategy enhances data accessibility and processing speeds, thereby improving operational agility and service delivery. This trend is crucial for sectors requiring real-time data analysis, such as logistics and e-commerce, where timely data processing directly impacts operational success.

Energy Efficiency and Sustainability

Sustainability practices are now at the forefront of the edge data center development strategy, with a marked emphasis on energy efficiency. In 2024, operators are increasingly investing in green technologies and designs that minimize environmental impact while maximizing operational efficiency. Innovations such as advanced cooling techniques, energy-efficient power solutions, and the integration of renewable energy sources are becoming standard. These efforts not only reduce the carbon footprint of data centers but also cater to the growing regulatory and consumer demand for greener technologies.

Regional Analysis

North America Leads the Edge Data Center Market with 32.6% Largest Share

The Edge Data Center Market is experiencing diverse growth dynamics across regions, driven by a wide range of factors including increasing data consumption, the proliferation of IoT devices, and the rapid expansion of cloud computing resources. In North America, which holds a dominant 32.6% share of the global market, the U.S. leads the region due to its highly advanced IT infrastructure, significant data generation, and the presence of major cloud service providers. Canada and the rest of North America are also witnessing growing demand for edge data centers, fueled by the adoption of 5G networks and ongoing digital transformation initiatives.

In Europe, leading countries such as Germany, the UK, and the Netherlands are at the forefront of edge data center deployment, driven by stringent data privacy regulations like GDPR and an increasing reliance on digital services. France, Spain, Russia, and Italy are similarly contributing to the market’s growth, supported by strong investments in telecommunications and energy-efficient computing resources.

The Asia-Pacific region is undergoing rapid expansion, led by China, Japan, and South Korea, where rising internet penetration, cloud computing, and smart city initiatives are key drivers of demand for edge data centers. Singapore and India are emerging as significant markets due to increased demand for localized data storage and computing capacity, particularly as IoT and AI-based applications expand. Other nations, including Thailand, Vietnam, and New Zealand, are also investing in edge data center infrastructure to support their growing digital economies.

In Latin America, moderate growth is being led by Brazil and Mexico as the region's digital infrastructure continues to mature. Government efforts to improve connectivity and the rising adoption of digital services are driving demand for edge data centers, with the rest of Latin America also seeing increased investments in advanced technologies.

In the Middle East & Africa, the UAE and Saudi Arabia are leading edge data center development, supported by national strategies such as Saudi Vision 2030 and the UAE’s ambitions to become a global technology hub. In Africa, South Africa plays a central role, where improved internet penetration and efforts toward data localization are fostering growth. Additionally, countries like Egypt and Nigeria, along with others in the rest of the Middle East and Africa, are exploring investments in edge data center infrastructure to meet the region’s growing need for computing resources.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The competitive landscape of the global Edge Data Center Market in 2024 is shaped by the strategic initiatives and technological advancements of key players. IBM Corporation and Dell Technologies continue to lead with robust edge computing solutions that integrate AI, cloud, and IoT, enabling enterprises to efficiently manage data closer to its source. NVIDIA Corporation plays a critical role by providing powerful GPUs that enhance the processing power of edge data centers, essential for AI and machine learning workloads.

Cisco Systems Inc. and Huawei Technologies Co., Ltd. are pivotal in offering networking solutions that facilitate seamless data transmission between edge and core centers. Their expansive product portfolios and global reach strengthen their competitive positioning. Schneider Electric SE and Vertiv Group Corp are key players in providing essential power management and cooling solutions, which are crucial for maintaining operational efficiency in edge environments, especially as data volumes and processing requirements grow.

Fujitsu Limited and Eaton Corporation Plc focus on infrastructure reliability and sustainability, addressing energy efficiency challenges that are becoming increasingly important for data centers worldwide. Meanwhile, 365 Data Centers Service, LLC and Zella DC are emerging players providing innovative, modular data center solutions that cater to small-to-medium enterprises looking for scalable edge deployments.

Market Key Players

- IBM Corporation

- Dell

- NVIDIA Corporation

- Dell Technologies

- Cisco Systems Inc.

- Huawei

- Fujitsu Limited

- Eaton Corporation Plc

- 365 Data Centers Service, LLC

- Huawei Technologies Co, Ltd.

- Schneider Electric SE

- Vertiv Group Corp

- Zella DC

- CommScope

- Other Key Players

Recent Development

- In June 2024, AWS received approval for a $205 million data center project in Chile, marking a significant step in expanding cloud service capabilities in South America.

- In April 2024, LightEdge acquired Connectria, a multi-cloud infrastructure service provider, enhancing its edge computing capabilities.

- In July 2023, Dell announced a collaboration with Airspan to deliver pre-integrated solutions for wireless edge deployments, combining Dell's modular data center technology with Airspan’s advanced wireless networking technology.

Report Scope

Report Features Description Market Value (2023) USD 10.6 Bn Forecast Revenue (2033) USD 60.2 Bn CAGR (2024-2032) 19.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component(Solution, Services), By Enterprise Size ( SMEs, Large Enterprises) By Industry Vertical,(IT & Telecom, Manufacturing, Government & Public Sector, Healthcare, Automotive, BFSI, Gaming & Entertainment, Other Industry Verticals) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape IBM Corporation, Dell, NVIDIA Corporation, Dell Technologies, Cisco Systems Inc., Huawei, Fujitsu Limited, Eaton Corporation Plc, 365 Data Centers Service, LLC, Huawei Technologies Co, Ltd., Schneider Electric SE, Vertiv Group Corp, Zella DC, CommScope, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- IBM Corporation

- Dell

- NVIDIA Corporation

- Dell Technologies

- Cisco Systems Inc.

- Huawei

- Fujitsu Limited

- Eaton Corporation Plc

- 365 Data Centers Service, LLC

- Huawei Technologies Co, Ltd.

- Schneider Electric SE

- Vertiv Group Corp

- Zella DC

- CommScope

- Other Key Players

Our Clients

View Our Licence Options