Healthcare Provider Network Management Market By Component (Software/Platforms and Services), By Delivery Mode (On-premise Delivery and Cloud-based Delivery), By End User (Payers, Private Health Insurance, Public Health Insurance), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48431

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

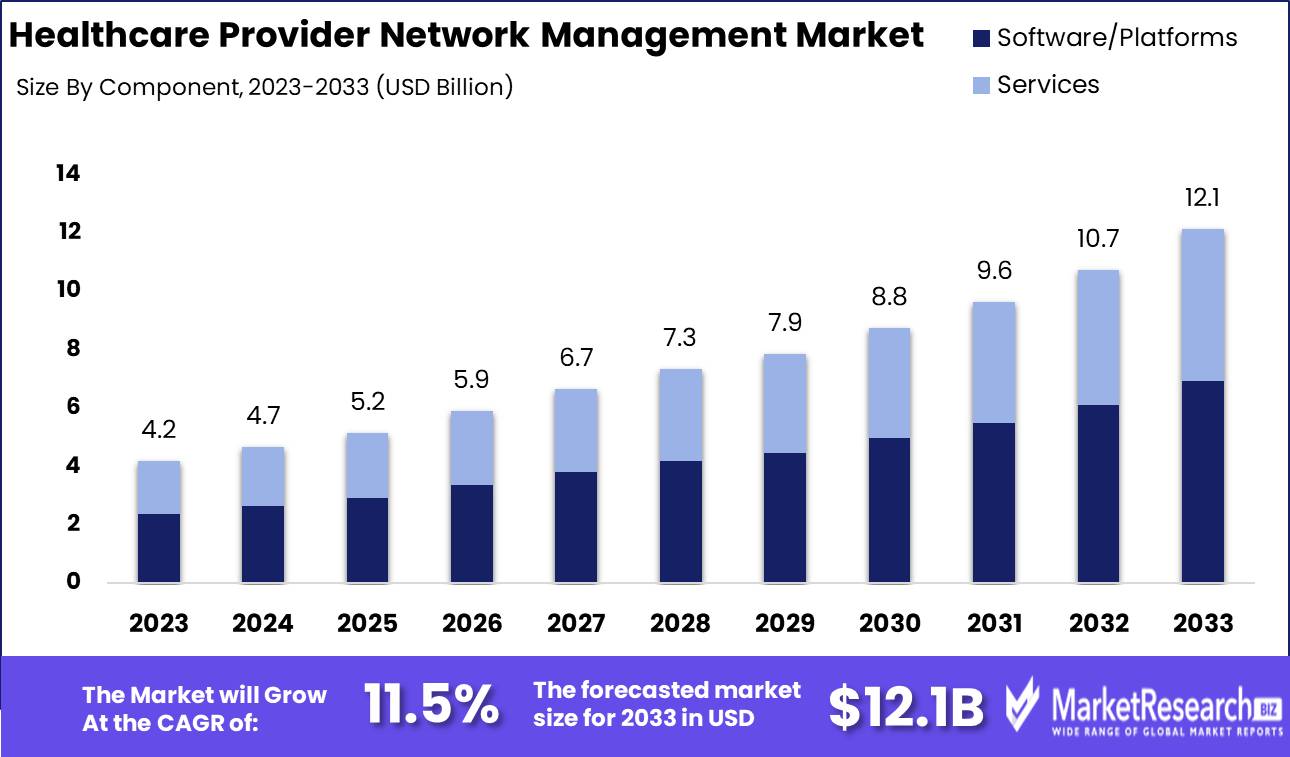

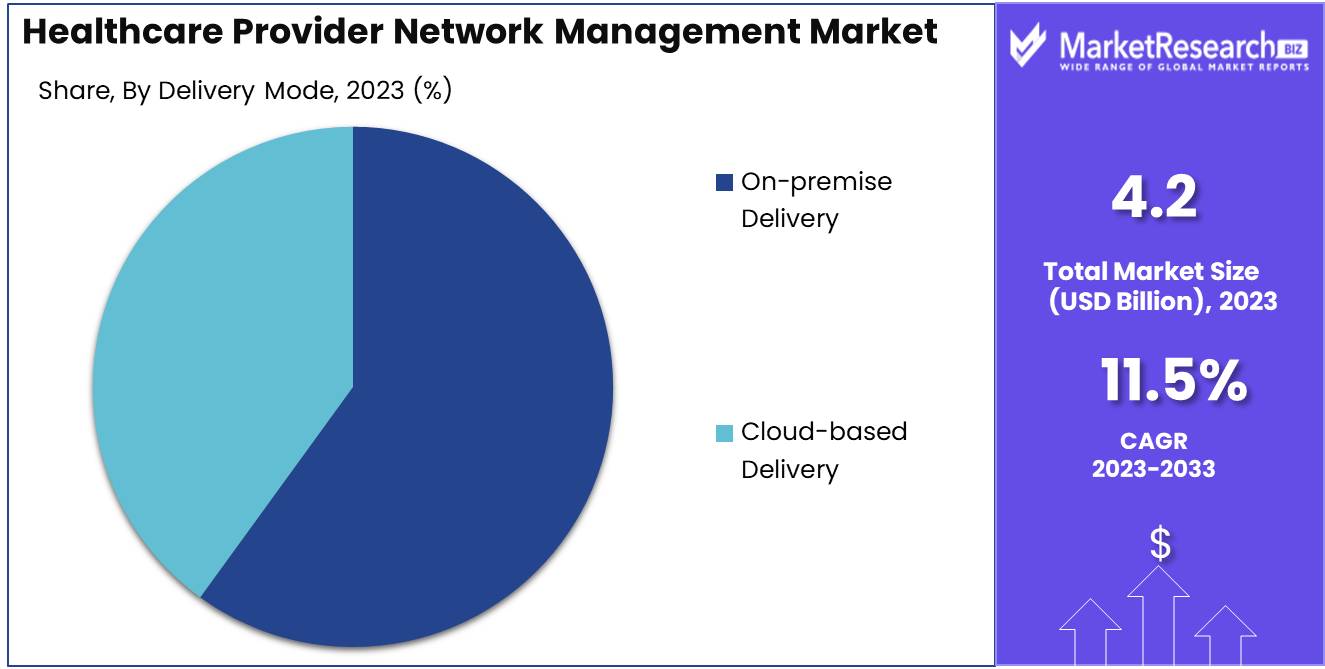

The Healthcare Provider Network Management Market was valued at USD 4.2 billion in 2023. It is expected to reach USD 12.1 billion by 2033, with a CAGR of 11.5% during the forecast period from 2024 to 2033.

The Healthcare Provider Network Management Market encompasses the solutions and services designed to streamline the operations and administration of healthcare provider networks. This market includes software platforms for credentialing, contracting, network monitoring, and analytics, aiming to enhance efficiency, regulatory compliance, and patient care quality. These solutions enable healthcare organizations to manage provider data, optimize network performance, reduce operational costs, and improve coordination across various healthcare entities.

The Healthcare Provider Network Management Market is witnessing significant growth, driven by the escalating complexity of healthcare provider networks and the critical need for efficient management solutions. The integration of diverse healthcare entities, often a result of mergers and acquisitions (M&As), is adding layers of complexity to the management landscape. These strategic M&As are not only expanding product portfolios but also enhancing market presence, underscoring the necessity for sophisticated network management systems. Effective management solutions are paramount to ensure seamless integration, operational efficiency, and improved patient outcomes. Moreover, the adoption of advanced technologies, such as AI and machine learning, is revolutionizing network management by providing predictive analytics and actionable insights, thereby streamlining operations and reducing administrative burdens.

Regulatory compliance further accentuates the importance of robust network management solutions. In the U.S., stringent regulations like the Health Insurance Portability and Accountability Act (HIPAA) compel healthcare organizations to maintain high standards of data security and privacy. This regulatory pressure is a catalyst for the widespread adoption of comprehensive network management systems designed to meet these rigorous standards. As healthcare providers strive to navigate this complex regulatory environment, the demand for innovative and compliant network management solutions is poised to grow.

In summary, the convergence of increased network complexity, strategic M&As, and stringent regulatory requirements are shaping the future of the Healthcare Provider Network Management Market, highlighting the need for integrated, compliant, and efficient management solutions to drive operational excellence and enhance patient care.

Key Takeaways

- Market Growth: The Healthcare Provider Network Management Market was valued at USD 4.2 billion in 2023. It is expected to reach USD 12.1 billion by 2033, with a CAGR of 11.5% during the forecast period from 2024 to 2033.

- By Component: Software/Platforms dominated healthcare provider network management, complemented by growing services.

- By Delivery Mode: On-premise Delivery dominated over Cloud-based Delivery despite growing traction.

- By End User: Payers dominated through advanced technologies and strategic initiatives.

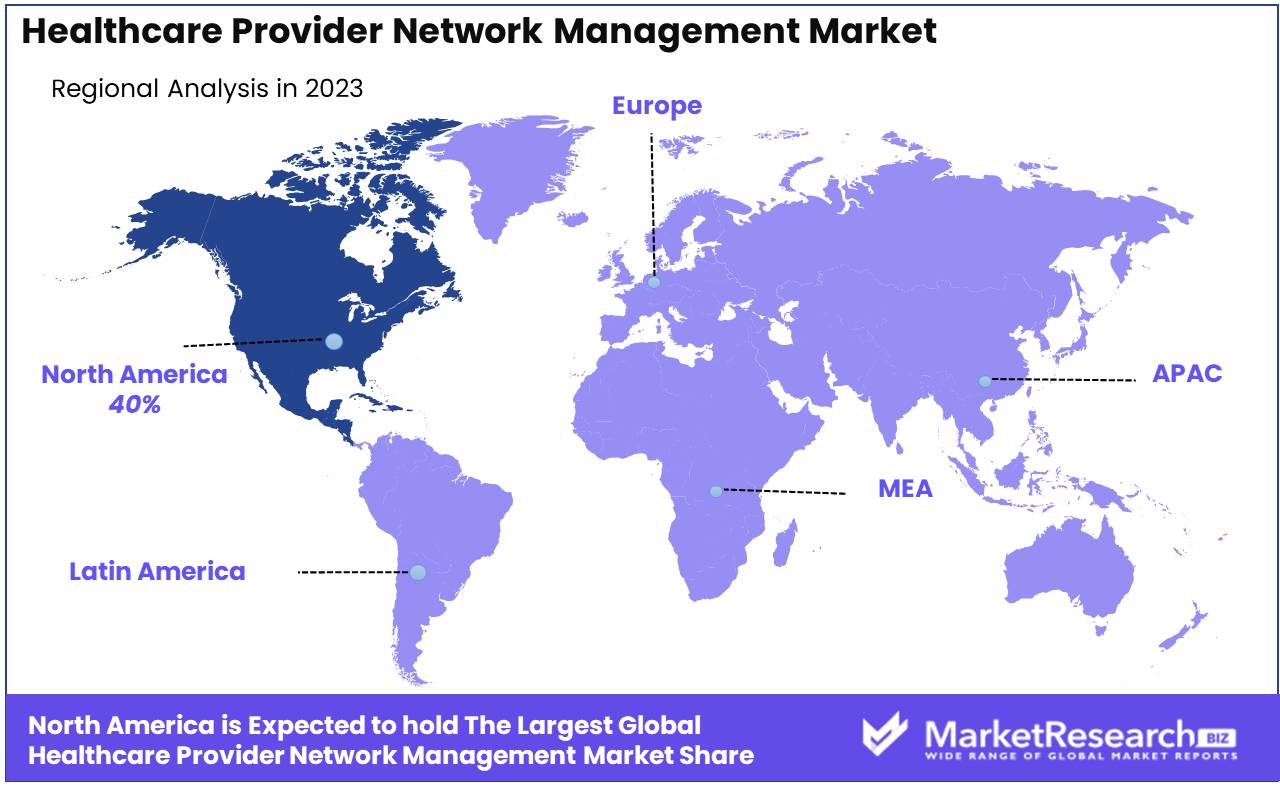

- Regional Dominance: North America dominates the market with 40% due to advanced infrastructure.

- Growth Opportunity: The healthcare provider network management market will grow significantly through AI-powered solutions and strategic technology partnerships.

Driving factors

Cost Efficiency Driving Market Expansion

The healthcare industry is increasingly prioritizing cost-effective solutions as a response to rising healthcare expenditures. This demand significantly propels the growth of the Healthcare Provider Network Management (HPNM) market. By integrating advanced network management systems, healthcare providers can optimize resource allocation, streamline administrative processes, and reduce operational costs. For instance, automated claims processing and effective utilization management facilitated by HPNM solutions can cut administrative costs by up to 30%. This cost efficiency not only enhances the financial health of healthcare organizations but also enables them to offer more affordable care to patients, thereby expanding their market reach and customer base.

Shift to Value-Based Care Enhances Network Management Adoption

The transition from volume-based to value-based care models is a pivotal factor accelerating the HPNM market's growth. Value-based care emphasizes outcomes and patient satisfaction, requiring robust data management and analytics capabilities to track performance metrics and ensure compliance with value-based contracts. HPNM solutions facilitate this shift by providing tools for performance monitoring, care coordination, and patient engagement. For example, these systems enable providers to monitor patient outcomes in real time and adjust care plans accordingly, leading to improved patient satisfaction and better health outcomes. As healthcare providers increasingly adopt these models, the need for sophisticated network management solutions that can handle complex data integration and analysis becomes imperative, driving market growth.

Enhanced Quality of Care through Rigorous Reporting and Accountability

Improving the quality of care has become a central objective for healthcare providers, driven by stringent payer reporting requirements. These requirements mandate comprehensive reporting on various performance indicators, necessitating advanced HPNM systems capable of detailed data collection and analysis. Effective provider network management ensures that healthcare organizations can meet these reporting standards efficiently. By leveraging HPNM solutions, providers can track and report on key metrics such as patient outcomes, service utilization, and compliance with care protocols. This capability not only helps in meeting regulatory demands but also fosters a culture of continuous quality improvement within healthcare organizations. Consequently, the focus on quality of care through payer reporting requirements directly contributes to the increased adoption of HPNM solutions, thereby fueling market growth.

Restraining Factors

Data Security and Privacy Concerns: A Persistent Barrier to Market Expansion

Data security and privacy concerns significantly restrain the growth of the Healthcare Provider Network Management (HPNM) market. In an era where digital transformation is pivotal, healthcare organizations are increasingly vulnerable to cyber threats. This heightened financial risk deters healthcare providers from adopting new network management solutions, which might not have robust security measures in place.

Additionally, stringent regulatory requirements such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States and the General Data Protection Regulation (GDPR) in Europe impose significant compliance burdens. Non-compliance can result in severe financial penalties and reputational damage. Consequently, healthcare providers may be hesitant to implement innovative network management technologies that could potentially expose them to compliance risks. The complexity of ensuring data protection while managing large volumes of sensitive patient information further complicates this landscape, thereby slowing market growth.

Interoperability Challenges: Hindering Seamless Integration and Efficiency

Interoperability challenges present another major hurdle for the HPNM market. The lack of standardized data exchange formats and protocols across different healthcare systems and providers creates significant integration issues. According to a 2023 survey, 75% of hospitals reported difficulties in achieving seamless data exchange with other healthcare entities, directly impacting the efficiency and effectiveness of network management solutions.

These challenges are compounded by the diverse range of electronic health record (EHR) systems, which often operate on incompatible platforms. The inability to share and access comprehensive patient data across different systems hinders coordinated care efforts and increases administrative burdens. This fragmentation not only reduces operational efficiencies but also raises costs, as providers need to invest in additional interfaces and middleware to bridge the interoperability gaps.

Furthermore, the lack of interoperability can lead to data silos, where critical patient information is isolated within specific systems, preventing healthcare providers from obtaining a holistic view of patient health. This situation undermines the potential benefits of advanced HPNM solutions designed to streamline and optimize provider networks.

By Component Analysis

In 2023, Software/Platforms dominated healthcare provider network management, complemented by growing services.

In 2023, Software/Platforms held a dominant market position in the By Component segment of the Healthcare Provider Network Management Market. The comprehensive capabilities of software solutions, including automation, real-time data processing, and analytics, have proven indispensable for healthcare providers. These platforms streamline network management by enabling efficient credentialing, provider data management, and compliance tracking, which are critical for ensuring the accuracy and reliability of provider networks. Furthermore, the integration of artificial intelligence and machine learning within these platforms has enhanced predictive analytics capabilities, allowing providers to anticipate network needs and optimize resource allocation.

Concurrently, the Services segment has shown significant growth, driven by the increasing complexity of healthcare networks and the need for specialized support. Services encompass consulting, implementation, and ongoing support, which are vital for maximizing the value derived from software platforms. Service providers offer expertise in navigating regulatory requirements, optimizing network performance, and ensuring seamless integration with existing systems. As healthcare organizations strive for efficiency and compliance, the demand for robust service offerings continues to rise, complementing the software/platforms and contributing to a holistic approach to network management. This dual focus on software and services underscores the industry's commitment to innovation and excellence in healthcare provider network management.

By Delivery Mode Analysis

In 2023, On-premise Delivery dominated over Cloud-based Delivery despite growing traction.

In 2023, On-premise Delivery held a dominant market position in the By Delivery Mode segment of the Healthcare Provider Network Management Market. This segment, characterized by the deployment of network management solutions directly within the healthcare provider's IT infrastructure, offers heightened control over data security, customization, and compliance with regulatory standards. Healthcare providers favor on-premise solutions due to their ability to integrate seamlessly with existing systems and the direct oversight they provide over sensitive patient data. The robust infrastructure required for on-premise delivery also underscores its preference among large healthcare institutions with significant IT resources.

Conversely, Cloud-based Delivery has been rapidly gaining traction due to its scalability, cost-effectiveness, and ease of implementation. Cloud-based solutions eliminate the need for substantial upfront capital investment in hardware and allow for real-time updates and maintenance by the service provider, thus reducing the burden on internal IT teams. Additionally, the increasing adoption of telehealth and remote patient monitoring has further bolstered the demand for cloud-based delivery, providing healthcare providers with flexible and accessible network management capabilities. This trend reflects a broader industry shift towards digital transformation and operational agility in healthcare services.

By End User Analysis

In 2023, Payers dominated through advanced technologies and strategic initiatives.

In 2023, Payers held a dominant market position in the "By End User" segment of the Healthcare Provider Network Management Market. Payers, including private and public health insurance entities, capitalized on their extensive resources and established infrastructures to drive market growth. Private health insurance providers leveraged advanced analytics and technology platforms to enhance network efficiency, optimize cost management, and improve patient outcomes. Their ability to offer customized solutions and value-added services bolstered their competitive edge, attracting a broader customer base.

Public health insurance organizations, on the other hand, benefited from governmental support and large-scale enrollment programs, ensuring a steady influx of beneficiaries. Their focus on integrating network management systems with public health initiatives helped streamline operations and reduce administrative burdens. Additionally, public insurers played a crucial role in addressing accessibility and affordability, aligning with regulatory frameworks aimed at universal healthcare coverage.

Key Market Segments

By Component

- Software/Platforms

- Services

By Delivery Mode

- On-premise Delivery

- Cloud-based Delivery

By End User

- Payers

- Private Health Insurance

- Public Health Insurance

Growth Opportunity

AI-Powered Solutions: Transforming Efficiency and Outcomes

The integration of AI-powered solutions represents a pivotal growth opportunity in the healthcare provider network management market. AI's capabilities in data analytics, predictive modeling, and automation are transforming how healthcare networks operate. By leveraging AI, healthcare providers can optimize resource allocation, enhance patient care coordination, and streamline administrative processes. For instance, AI can predict patient admission rates, enabling better staffing and resource planning, thereby reducing operational costs and improving patient outcomes. Furthermore, AI-driven platforms can assist in identifying and mitigating fraudulent activities, thus safeguarding the financial integrity of healthcare organizations.

Strategic Partnerships with Technology Leaders: Enhancing Capabilities

Partnering with technology leaders is another significant avenue for growth. Collaborations with tech giants allow healthcare networks to integrate advanced technologies seamlessly into their operations. These partnerships can facilitate the development of robust IT infrastructures, ensuring interoperability and data security across different healthcare systems. For example, alliances with leading technology firms can enable the adoption of cloud-based solutions, enhancing data accessibility and facilitating real-time collaboration among healthcare providers. Moreover, technology partners can offer scalable solutions that accommodate the evolving needs of healthcare networks, thereby fostering innovation and continuous improvement.

Latest Trends

Growing Adoption of Cloud-Based Solutions

The healthcare provider network management market is witnessing a significant shift towards cloud-based solutions. This trend is driven by the need for scalable, cost-effective, and secure data management systems. Cloud-based solutions offer unparalleled flexibility, enabling healthcare organizations to efficiently manage vast amounts of patient data and streamline operations across multiple locations. Additionally, the cloud facilitates real-time data access and collaboration, enhancing the ability of providers to deliver coordinated care. With the increasing focus on reducing IT infrastructure costs and improving system interoperability, cloud adoption is expected to accelerate, fostering innovation and efficiency within the healthcare sector.

Integration with Electronic Health Records (EHRs)

The integration of provider network management systems with electronic health records (EHRs) is another critical trend shaping the market. EHR integration enables seamless data exchange between healthcare providers, resulting in improved patient outcomes and operational efficiencies. By incorporating network management capabilities directly into EHR platforms, healthcare organizations can streamline processes such as credentialing, provider enrollment, and compliance monitoring. This integration not only reduces administrative burdens but also ensures that providers have access to comprehensive patient information, facilitating more informed decision-making. As regulatory requirements for data interoperability continue to tighten, the demand for EHR-integrated solutions is expected to grow, driving further advancements in the healthcare provider network management market.

Regional Analysis

North America dominates the market with 40% due to advanced infrastructure.

The North America healthcare provider network management market dominates globally, accounting for 40% of the largest market share. This leadership is driven by advanced healthcare infrastructure, widespread adoption of IT solutions, and supportive government policies promoting digital health initiatives. The United States, in particular, contributes significantly due to its robust technological ecosystem and substantial healthcare expenditure, which reached $4.1 trillion in 2020.

Europe follows closely, holding around 25% of the market share. The region benefits from a well-established healthcare system, substantial investments in healthcare IT, and a growing emphasis on patient-centric care models. Germany, the UK, and France are key contributors, driven by continuous advancements in healthcare technology and regulatory support for health IT innovations.

In the Asia Pacific, the market is rapidly expanding, capturing approximately 20% of the market. This growth is propelled by increasing healthcare expenditures, large patient populations, and government initiatives aimed at modernizing healthcare systems. Countries like China, Japan, and India are at the forefront, with China’s healthcare market alone expected to surpass $1 trillion by 2025.

Middle East & Africa and Latin America are emerging markets, together contributing about 15% of the global market share. In these regions, market growth is supported by improving healthcare infrastructure, rising demand for quality healthcare, and increasing adoption of digital health solutions. Brazil, South Africa, and the UAE are notable contributors due to their ongoing healthcare reforms and investments in health IT.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Healthcare Provider Network Management (HPNM) market in 2024 is poised for substantial growth, driven by the integration of advanced technologies and the need for efficient healthcare delivery systems. Key players such as Infosys Limited, Appian, and Optum Inc. are at the forefront, leveraging their expertise in IT solutions and healthcare to streamline provider network management processes.

Infosys Limited and Mphasis Limited are leading the charge with robust IT infrastructure and innovative solutions, enhancing the efficiency and accuracy of network management. Their focus on AI and machine learning helps in predictive analytics and decision-making, essential for optimizing provider networks.

Appian and Artivatic AI are making significant strides with their low-code automation platforms and AI-driven solutions. These innovations reduce administrative burdens and improve compliance and operational efficiency, crucial for modern healthcare networks.

Major healthcare corporations like Centene Corporation and McKesson Corporation bring their extensive industry experience to the table. Centene's subsidiary, Envolve Health, and McKesson’s comprehensive healthcare services are instrumental in delivering integrated and value-based care.

Change Healthcare and Optum Inc. leverage their expansive data analytics capabilities to provide insights that drive strategic decisions in network management. Their solutions enhance interoperability and patient outcomes.

Meanwhile, companies like Atos SE (Syntel Inc.), OSPLabs, and Virtusa Corporation are focusing on digital transformation initiatives, ensuring that healthcare providers can adapt to rapidly changing market dynamics.

In summary, the competitive landscape of the HPNM market in 2024 is characterized by technological innovation and strategic partnerships, aimed at enhancing operational efficiencies, regulatory compliance, and patient care quality.

Market Key Players

- Infosys Limited

- Appian

- Artivatic AI

- Atos SE (Syntel Inc.)

- Centene Corporation (Envolve Health)

- Change Healthcare

- McKesson Corporation

- Mphasis Limited

- Optum Inc.

- OSPLabs

- RELX Group (LexisNexis Risk Solutions)

- Skygen USA LLC

- Virtusa Corporation

- Others

Recent Development

- In January 2024, Philips Healthcare announced a significant push towards digital transformation by integrating advanced AI and data analytics into their network management solutions. This initiative aims to enhance patient outcomes and streamline healthcare operations, showcasing the growing emphasis on technology in healthcare.

- In October 2023, Vestica Healthcare acquired MediSpend to enhance its payer network management offerings. This acquisition aims to expand Vestica's capabilities in network contracting, provider analytics, and payment integrity solutions.

Report Scope

Report Features Description Market Value (2023) USD 4.2 Billion Forecast Revenue (2033) USD 12.1 Billion CAGR (2024-2032) 11.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Software/Platforms and Services), By Delivery Mode (On-premise Delivery and Cloud-based Delivery), By End User (Payers, Private Health Insurance, Public Health Insurance) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Infosys Limited, Appian, Artivatic AI, Atos SE (Syntel Inc.), Centene Corporation (Envolve Health), Change Healthcare, McKesson Corporation, Mphasis Limited, Optum Inc., OSPLabs, RELX Group (LexisNexis Risk Solutions), Skygen USA LLC, Virtusa Corporation, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Infosys Limited

- Appian

- Artivatic AI

- Atos SE (Syntel Inc.)

- Centene Corporation (Envolve Health)

- Change Healthcare

- McKesson Corporation

- Mphasis Limited

- Optum Inc.

- OSPLabs

- RELX Group (LexisNexis Risk Solutions)

- Skygen USA LLC

- Virtusa Corporation

- Others

Our Clients

View Our Licence Options