Chimeric Antigen Receptor Market Report By Type (Abecma, Breyanzi, Kymriah, Tecartus, Yescarta, Others), By Application (Leukemia, Lymphoma, Multiple Myeloma, Autoimmune Disorders, Other Applications), By End User (Hospitals, Cancer Care Treatment Centers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46933

-

May 2024

-

321

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

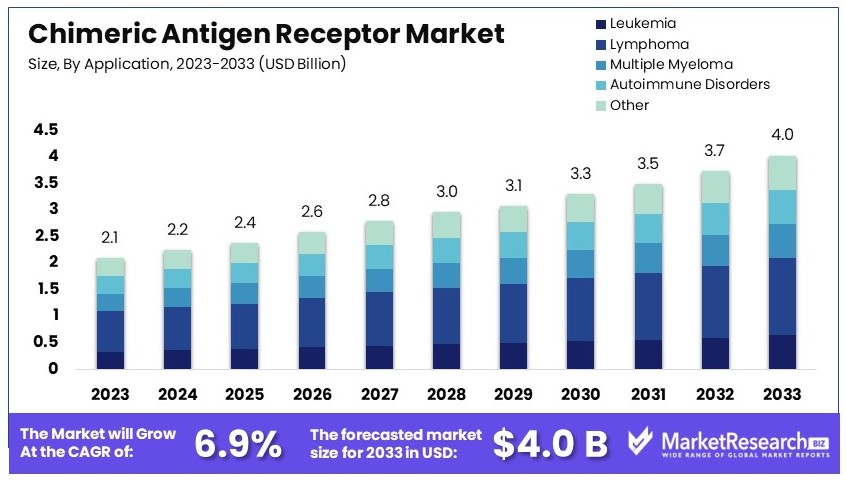

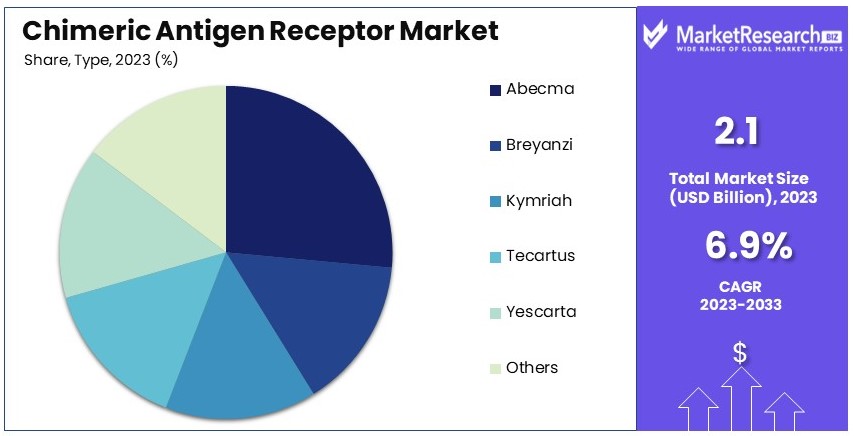

The Global Chimeric Antigen Receptor Market size is expected to be worth around USD 4.0 Billion by 2033, from USD 2.1 Billion in 2023, growing at a CAGR of 6.9% during the forecast period from 2024 to 2033.

The Chimeric Antigen Receptor (CAR) Market deals with CAR T-cell therapies. These are used to treat certain cancers. CAR T-cells are engineered to target and kill cancer cells. The market is expanding due to successful clinical trials and approvals.

Key players are investing in new CAR T-cell therapies. The market is segmented by therapy type, application, and end-user. North America leads in market share, with Europe and Asia-Pacific growing rapidly. Challenges include high treatment costs and manufacturing complexities. The market is driven by the need for effective cancer treatments and advancements in genetic engineering.

The chimeric antigen receptor (CAR) market is experiencing significant growth, driven by rising cancer incidence and advancements in cancer treatment technologies. According to the American Cancer Society, the US is projected to see 1,958,310 new cancer cases and 609,820 cancer deaths in 2023. Lung and bronchus cancer are expected to account for 21% of these deaths, while breast cancer could account for 15%. This substantial burden on healthcare systems underscores the urgent need for innovative cancer therapies.

CAR-T cell therapy represents a groundbreaking approach in immuno oncology, offering personalized cancer treatment by modifying patients' T cells to target and kill cancer cells. The market is benefiting from increased investment in research and strategic partnerships. In June 2023, Exact Sciences Corporation partnered with the Broad Institute and Baylor Scott & White to advance cancer technologies. This collaboration includes a five-year research agreement and an exclusive license for MAESTRO, a next-gen circulating tumor DNA technology. MAESTRO enables highly sensitive detection of residual disease, enhancing the scalability and effectiveness of CAR-T therapies.

These technological advancements are crucial for improving patient outcomes and reducing the healthcare burden. CAR-T therapies have shown promising results in treating hematologic cancers, and ongoing research aims to extend their application to solid tumors. The growing pipeline of CAR-T products and expanding clinical trials are expected to drive market growth.

In summary, the CAR market is poised for substantial expansion, fueled by the rising cancer burden and significant advancements in cancer treatment technologies. Strategic collaborations and innovative research are enhancing the effectiveness and scalability of CAR-T therapies, offering new hope for cancer patients.

Key Takeaways

- Market Value: Chimeric Antigen Receptor Market was valued at USD 2.1 Billion in 2023, and is expected to reach USD 4.0 Billion in 2033, at a CAGR of 6.9%

- Type Analysis: Abecma dominates with 25%; efficacy in multiple myeloma treatment.

- Application Analysis: Lymphoma dominates with 30%; high prevalence and targeted therapies.

- End User Analysis: Hospitals dominate with 52%; extensive infrastructure and patient access rises.

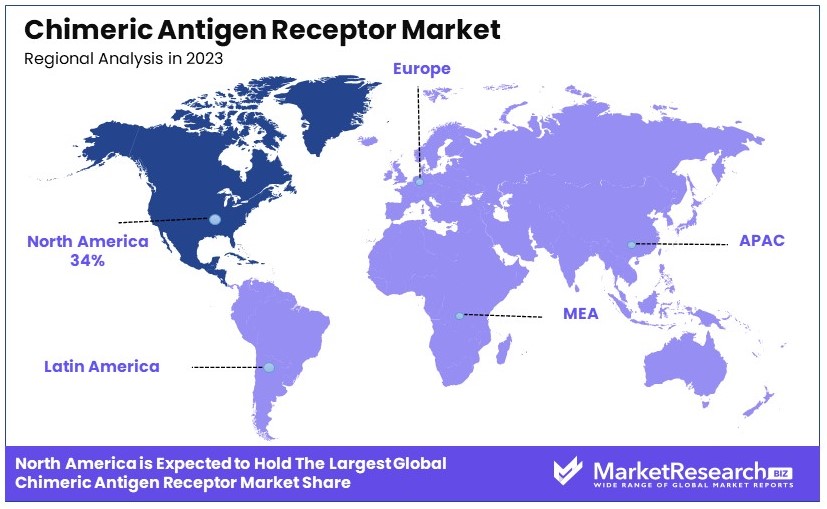

- Dominant Region: North America with 34%; advanced healthcare infrastructure and research expands.

- High Growth Region: Europe with 25%; rise in strong biotech and pharmaceutical sectors.

- Analyst Viewpoint: Market growth driven by innovative CAR-T therapies; competitive with expanding applications.

- Growth Opportunities: Development of new CAR-T therapies; expanding indications beyond oncology.

Driving Factors

Rising Incidence of Cancer and Unmet Medical Needs Drive Market Growth

The rising incidence of cancer and unmet medical needs significantly drive the growth of the Chimeric Antigen Receptor (CAR) market. The global prevalence of various cancers has surged, creating an urgent need for innovative treatments. Conventional cancer therapies often have limitations, prompting the demand for targeted approaches like CAR-T cell therapy. CAR-T therapy has shown remarkable success in treating hematological malignancies such as acute lymphoblastic leukemia (ALL) and non-Hodgkin's lymphoma (NHL). For instance, Novartis' Kymriah (tisagenlecleucel) and Gilead's Yescarta (axicabtagene ciloleucel) are approved for specific types of NHL and ALL. These therapies offer new hope to patients who have exhausted other treatment options.

The efficacy of CAR-T therapies in treating these cancers highlights their potential to address unmet medical needs. As more patients and healthcare providers recognize the benefits, the market demand for CAR-T therapies is expected to grow. This growth is further supported by ongoing clinical trials and the development of new CAR-T products targeting various cancer types. Consequently, the rising cancer incidence and the limitations of traditional treatments are key factors propelling the CAR market forward.

Advancements in Gene Editing and Cell Engineering Technologies Drive Market Growth

Advancements in gene editing and cell engineering technologies are crucial in driving the CAR market's growth. The development of tools like CRISPR-Cas9 has revolutionized the design and manufacturing of CAR-T cells. These technologies enable the creation of more potent and specific CAR-T cell constructs, enhancing their targeting capabilities and safety profiles. Companies such as Cellectis and Precision BioSciences are at the forefront, utilizing gene editing to develop next-generation CAR-T therapies with improved efficacy.

The integration of advanced gene editing techniques allows researchers to optimize CAR-T cells, making them more effective against cancer cells while minimizing adverse effects. This progress has led to a surge in the number of CAR-T cell therapies entering clinical trials and receiving regulatory approval. The ability to engineer CAR-T cells with precision ensures that they can better target cancer cells, leading to higher success rates in treatment. As a result, the continuous advancements in gene editing and cell engineering significantly contribute to the growth and expansion of the CAR market.

Expansion into Solid Tumors Drives Market Growth

The expansion of CAR-T therapy into solid tumors is a pivotal factor driving market growth. Initially, CAR-T therapy showed success primarily in hematological malignancies. However, researchers are now exploring its application in treating solid tumors, such as breast, lung, and brain cancers. Addressing the challenges of solid tumor microenvironments and identifying tumor-specific antigens are key research areas. For example, Novartis and the University of Pennsylvania are collaborating on CAR-T cell therapies for glioblastoma, an aggressive brain cancer.

The potential to expand CAR-T therapy into solid tumors opens a vast market opportunity. Solid tumors represent a significant portion of cancer diagnoses, and successful CAR-T treatments for these cancers could revolutionize cancer therapy. This expansion not only increases the market size but also drives further research and development in the field. By overcoming the barriers associated with solid tumors, CAR-T therapies can become a cornerstone treatment for various cancer types, thereby driving the market's growth and establishing CAR-T therapy as a versatile cancer treatment option.

Restraining Factors

High Manufacturing Costs and Complexity Restrain Market Growth

The high manufacturing costs and complexity significantly restrain the growth of the Chimeric Antigen Receptor (CAR) market. The manufacturing process for CAR-T cell therapies involves several intricate steps such as gene editing, cell isolation, expansion, and re-infusion into the patient. This complexity requires specialized facilities and highly trained personnel, contributing to the high costs associated with CAR-T therapies.

For instance, the list price for treatments like Kymriah and Yescarta can exceed $400,000 per treatment, making them among the most expensive therapies available. These high costs limit the accessibility of CAR-T cell therapies to a broader patient population and place a financial burden on healthcare systems. Consequently, the high manufacturing costs and complexity present significant barriers to the widespread adoption and growth of the CAR market.

Potential Severe Side Effects Restrain Market Growth

The potential severe side effects of CAR-T cell therapy restrain market growth. While CAR-T therapy has shown promising efficacy, it can lead to severe and potentially life-threatening side effects such as cytokine release syndrome (CRS) and neurotoxicity. These side effects necessitate close monitoring and specialized management strategies, increasing the overall treatment burden and costs.

For example, Kymriah's prescribing information includes a boxed warning for CRS and neurological toxicities, highlighting the need for appropriate risk evaluation and mitigation strategies. The risk of severe side effects can deter patients and healthcare providers from opting for CAR-T therapies, thereby limiting market growth. Additionally, the need for specialized care to manage these side effects further adds to the treatment costs, presenting another barrier to the widespread adoption of CAR-T cell therapies.

Type Analysis

Abecma dominates with 25% due to its efficacy in treating multiple myeloma.

The Chimeric Antigen Receptor (CAR) market is segmented by type, with Abecma, Breyanzi, Kymriah, Tecartus, Yescarta, and others as key sub-segments. Abecma, developed by Bristol-Myers Squibb and Bluebird Bio, has shown significant success in patients with relapsed or refractory multiple myeloma. Its approval by the FDA and subsequent adoption in clinical settings highlight its strong market position. Abecma's ability to offer a new treatment option for patients who have exhausted other therapies contributes to its market dominance. Additionally, its targeted mechanism of action and the clinical trial data supporting its efficacy and safety profile have driven its adoption.

Breyanzi, Kymriah, Tecartus, and Yescarta also play vital roles in the CAR market. Breyanzi, developed by Bristol-Myers Squibb, is used for treating relapsed or refractory large B-cell lymphoma. Kymriah, developed by Novartis, is approved for treating certain types of non-Hodgkin's lymphoma and acute lymphoblastic leukemia (ALL). Tecartus, by Kite Pharma (a Gilead company), is used for treating mantle cell lymphoma, while Yescarta, also by Kite Pharma, treats relapsed or refractory large B-cell lymphoma. These therapies, although significant, do not match Abecma's market share due to their specific application scopes and competitive dynamics.

The "Others" category includes emerging CAR-T therapies and those under development. These treatments expand the CAR market by targeting a broader range of cancer types and potentially other diseases. The continuous innovation and clinical trials in this segment ensure ongoing growth and diversification of the CAR market. Overall, while Abecma leads the type segment, other therapies contribute significantly to the market's breadth and potential.

Application Analysis

Lymphoma dominates with 30% due to the high prevalence and demand for targeted therapies.

The application segment of the Chimeric Antigen Receptor (CAR) market includes leukemia, lymphoma, multiple myeloma, autoimmune disorders, and other applications. CAR-T therapies like Kymriah, Yescarta, and Breyanzi have been particularly effective in treating various forms of lymphoma, including large B-cell lymphoma and mantle cell lymphoma. The success of these therapies in clinical trials and real-world settings has led to their widespread adoption, driving the dominance of the lymphoma segment. The high remission rates and durable responses observed in lymphoma patients treated with CAR-T therapies underscore their therapeutic value.

Leukemia, another significant sub-segment, includes CAR-T therapies like Kymriah, which is approved for treating acute lymphoblastic leukemia (ALL) in pediatric and young adult patients. The effectiveness of CAR-T therapy in inducing remission in patients with relapsed or refractory ALL has been well-documented, contributing to its substantial market share. Multiple myeloma, addressed by Abecma, represents a growing application area for CAR-T therapy. The success of Abecma in treating patients with advanced multiple myeloma highlights the expanding scope of CAR-T applications beyond hematologic malignancies.

Autoimmune disorders and other applications are emerging areas of interest for CAR-T therapy. Research is ongoing to explore the potential of CAR-T cells in treating autoimmune diseases and other non-cancerous conditions. The versatility of CAR-T technology and its ability to be tailored to target specific disease-causing cells make it a promising therapeutic approach for a wide range of applications. In summary, while lymphoma leads the application segment, leukemia, multiple myeloma, and emerging applications contribute to the dynamic growth of the CAR market.

End User Analysis

Hospitals dominate with 52% due to their extensive infrastructure and patient access.

The end-user segment of the Chimeric Antigen Receptor (CAR) market is divided into hospitals and cancer care treatment centers. Hospitals are the primary centers for administering CAR-T cell therapies, given their capacity to manage the complex manufacturing and administration processes involved. The presence of specialized facilities, trained medical personnel, and comprehensive patient care services make hospitals the preferred choice for CAR-T therapy treatments. Additionally, hospitals often participate in clinical trials, contributing to the development and adoption of new CAR-T therapies.

Cancer care treatment centers also play a crucial role in the CAR market. These specialized centers focus exclusively on cancer treatment and often provide advanced therapies like CAR-T. They are equipped with the necessary infrastructure and expertise to administer CAR-T therapies and manage associated side effects. While they represent a smaller market share compared to hospitals, cancer care treatment centers are essential for providing dedicated and focused care to cancer patients.

The integration of CAR-T therapy into both hospital and cancer care treatment center settings ensures broader accessibility and adoption. The collaborative efforts between hospitals and specialized treatment centers enhance the overall healthcare system's capacity to deliver CAR-T therapies to patients in need. In conclusion, while hospitals dominate the end-user segment, cancer care treatment centers contribute significantly to the market by providing specialized and focused care.

Key Market Segments

By Type

- Abecma

- Breyanzi

- Kymriah

- Tecartus

- Yescarta

- Others

By Application

- Leukemia

- Lymphoma

- Multiple Myeloma

- Autoimmune Disorders

- Other Applications

By End User

- Hospitals

- Cancer Care Treatment Centers

Growth Opportunities

Development of Next-Generation CAR-T Cell Therapies Offers Growth Opportunity

The development of next-generation CAR-T cell therapies is a key growth driver in the market. Researchers are focusing on improving safety, specificity, and durability. Advances include novel target antigens and advanced gene editing techniques.

Companies like Autolus and Poseida Therapeutics are creating CAR-T therapies with safety switches to control side effects. These innovations can reduce risks and improve patient outcomes. The market benefits from increased investment in research and development. The growing pipeline of advanced CAR-T products highlights significant market potential.

Allogeneic CAR-T Cell Therapies Offer Growth Opportunity

Allogeneic CAR-T cell therapies represent a major growth opportunity. Unlike autologous therapies, allogeneic CAR-T cells are manufactured in advance, making them more readily available and cost-effective.

Companies such as Allogene Therapeutics, Precision BioSciences, and Cellectis are at the forefront of this development. These therapies can reduce production time and costs, making treatment accessible to more patients. The ability to mass-produce CAR-T cells opens new market segments and supports scalability, driving substantial market growth.

Trending Factors

Combination Therapies and Multimodal Approaches Are Trending Factors

Combining CAR-T cell therapy with other treatments is a growing trend. Multimodal approaches aim to overcome resistance and enhance efficacy. Researchers are exploring combinations with checkpoint inhibitors like pembrolizumab and conventional chemotherapy.

This strategy can broaden the applicability of CAR-T therapy to more cancer types. The success of these combination treatments in clinical trials drives interest and investment, contributing to the market's upward trend. The potential to treat a wider range of cancers makes this a significant market trend.

Advances in Cell Manufacturing and Automation Are Trending Factors

Advances in cell manufacturing and automation are key trends in the CAR-T cell market. Improvements in manufacturing processes, including automation and scalability, streamline production and reduce costs.

Automated closed-system platforms and advanced bioreactors enhance reproducibility and consistency. These innovations can make CAR-T therapies more widely available. The focus on cost reduction and scalability supports broader market adoption. As these technologies advance, the market is poised for significant expansion.

Regional Analysis

North America Dominates with 34% Market Share

North America's dominance in the Chimeric Antigen Receptor (CAR) market is driven by advanced healthcare infrastructure, strong R&D investments, and early adoption of innovative therapies. The presence of leading biotechnology companies and supportive regulatory frameworks also contribute significantly.

The region's high market share is supported by a robust clinical trial landscape and extensive collaboration between research institutions and biotech firms. High healthcare expenditure and favorable reimbursement policies further enhance market performance.

North America's market presence is expected to grow, driven by continuous innovation and expanding clinical applications of CAR therapies. Increased funding and ongoing research will sustain its leading position.

Europe: 25% Market Share

Europe's significant market share is attributed to strong government support for healthcare innovation, established pharmaceutical industries, and a growing number of CAR therapy approvals.

Collaborative efforts between countries and high investments in biotechnological research drive market growth. Europe's regulatory landscape and focus on advanced therapies enhance its market potential.

Asia Pacific: 20% Market Share

Asia Pacific's market share is driven by rising healthcare expenditures, increasing cancer prevalence, and growing investments in biotechnology. Countries like China and Japan are leading in CAR therapy research and development.

Rapid economic growth, improving healthcare infrastructure, and favorable government policies boost market dynamics. Collaborations with global biotech firms and increasing clinical trials further enhance market growth.

Middle East & Africa: 10% Market Share

Market share in the Middle East & Africa is supported by improving healthcare systems, rising cancer incidence, and increasing government initiatives for advanced therapies.

The region's growth is driven by investments in healthcare infrastructure and growing collaborations with international biotech companies. Efforts to enhance medical research capabilities also play a role.

Latin America: 11% Market Share

Latin America's market share is influenced by rising healthcare investments, increasing cancer cases, and growing interest in innovative therapies. Countries like Brazil and Mexico are leading regional efforts in CAR therapy.

Economic development, improved healthcare access, and government initiatives support market dynamics. Collaborations with international biotech firms and expanding clinical trials drive growth.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

Impact and Strategic Positioning:

The Chimeric Antigen Receptor (CAR) market features several prominent companies, each leveraging its strengths to impact the industry. Major players like Novartis AG and Pfizer Inc. are at the forefront, driving innovation with extensive research and development efforts. Their significant investments in CAR therapy research underscore their strategic focus on advanced cancer treatments.Market Influence:

Abbott Laboratories, Baxter International Inc., and Becton, Dickinson, and Company, known for their robust portfolios in medical devices and diagnostics, contribute to the CAR market through advanced technology and manufacturing capabilities. These companies enhance the production and delivery of CAR therapies, ensuring quality and scalability.Johnson & Johnson and Medtronic PLC are leveraging their global presence and strong distribution networks to expand the reach of CAR therapies. Their strategic acquisitions and partnerships further solidify their market influence, enabling them to integrate cutting-edge technologies and improve patient access to innovative treatments.

Collaborations and Innovation:

Boston Scientific Corporation and Fresenius SE & Co. KGaA are focusing on collaborations and partnerships to enhance their CAR therapy offerings. By working with biotech firms and research institutions, they aim to accelerate the development and commercialization of CAR treatments.Endo International PLC, although smaller in scale, is making strides through niche market strategies and targeted research investments. Their focus on specific therapeutic areas helps them carve out a unique position in the competitive landscape.

Future Prospects:

The collective efforts of these companies are driving the CAR market forward. Strategic positioning, coupled with ongoing innovations and collaborations, is expected to yield significant advancements in CAR therapies. The market influence of these key players will continue to shape the future of cancer treatment, promising improved patient outcomes and expanded treatment options globally.Market Key Players

- Abbott Laboratories

- Baxter International Inc.

- Becton, Dickinson, and Company

- Boston Scientific Corporation

- Fresenius SE & Co. KGaA

- Johnson & Johnson

- Medtronic PLC

- Novartis AG

- Endo International PLC

- Pfizer Inc.

Recent Developments

- May 2024: The study on anti-CD19 chimeric antigen receptor T-cell therapy for Richter transformation was conducted as an international multicenter retrospective study. It evaluated the safety and efficacy of CAR-T cell treatment for patients with Richter transformation, who received CD19 CAR-T approved for hematologic malignancies at nine different centers.

- May 2024: Cytiva's CAR-T platform has been reported to enhance production by up to 50%. This improvement in production capacity is significant for the development and commercialization of CAR-T cell therapies.

- May 2024: The US Food and Drug Administration (FDA) has approved Bristol-Myers Squibb's Breyanzi as a new CAR-T cell therapy for relapsed or refractory mantle cell lymphoma. This approval marks a significant milestone in the treatment of this disease.

Report Scope

Report Features Description Market Value (2023) USD 2.1 Billion Forecast Revenue (2033) USD 4.0 Billion CAGR (2024-2033) 6.9% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Abecma, Breyanzi, Kymriah, Tecartus, Yescarta, Others), By Application (Leukemia, Lymphoma, Multiple Myeloma, Autoimmune Disorders, Other Applications), By End User (Hospitals, Cancer Care Treatment Centers) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Abbott Laboratories, Baxter International Inc., Becton, Dickinson, and Company, Boston Scientific Corporation, Fresenius SE & Co. KGaA, Johnson & Johnson, Medtronic PLC, Novartis AG, Endo International PLC, Pfizer Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Abbott Laboratories

- Baxter International Inc.

- Becton, Dickinson, and Company

- Boston Scientific Corporation

- Fresenius SE & Co. KGaA

- Johnson & Johnson

- Medtronic PLC

- Novartis AG

- Endo International PLC

- Pfizer Inc.

Our Clients

View Our Licence Options