Cancer Vaccines Market Report By Type (Preventive Vaccines [HPV Vaccines (for Cervical Cancer), Hepatitis B Vaccines (for Liver Cancer)], Therapeutic Vaccines [Cancer Treatment Vaccines (e.g., for Prostate Cancer, Melanoma), Personalized Cancer Vaccines], Combination Vaccines [Preventive and Therapeutic]), By Vaccine Type, By Cancer Type, By End-User, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

49712

-

July 2024

-

325

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

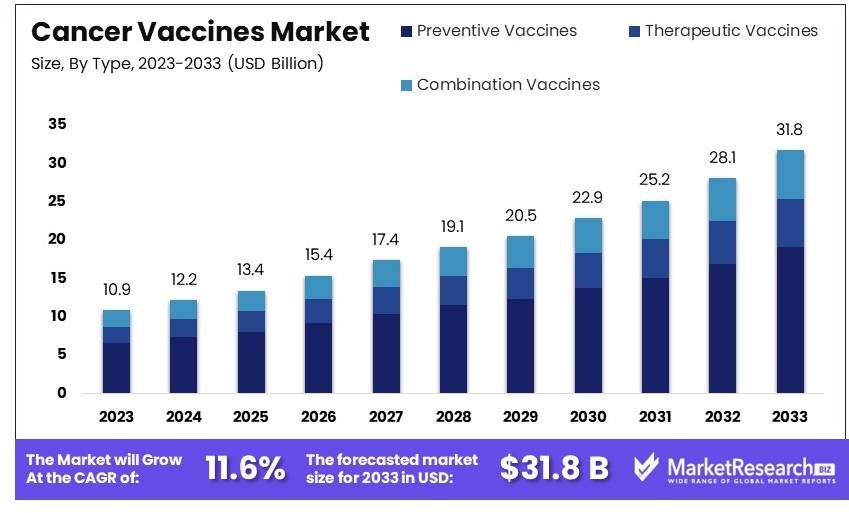

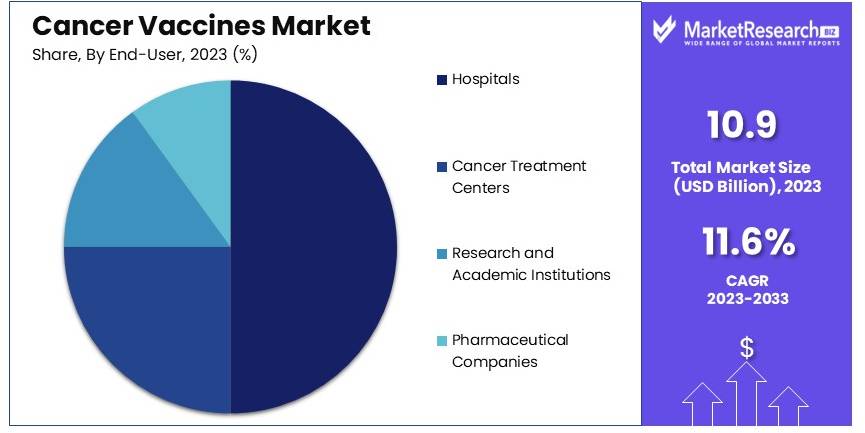

The Global Cancer Vaccines Market size is expected to be worth around USD 31.8 Billion by 2033, from USD 10.9 Billion in 2023, growing at a CAGR of 11.6% during the forecast period from 2024 to 2033.

The cancer vaccines market involves vaccines that prevent or treat various types of cancer. These vaccines stimulate the immune system to target cancer cells. Key drivers include increasing cancer prevalence, advancements in immunotherapy, and rising healthcare spending.

The market is segmented by vaccine type, indication, end-user, and region. Innovations in personalized medicine and combination therapies are influencing market trends. Major players focus on clinical trials, regulatory approvals, and strategic partnerships to bring new vaccines to market and expand their reach in oncology.

The cancer vaccines market is experiencing significant growth, driven by advancements in both preventive and therapeutic vaccines. Preventive vaccines, such as the HPV vaccine, play a crucial role in reducing cancer risk. The Centers for Disease Control and Prevention (CDC) reports that HPV vaccination can prevent over 90% of HPV-related cancers, significantly lowering the incidence of cervical cancer. Similarly, the hepatitis B vaccine is effective in preventing liver cancer, underscoring the importance of vaccines in cancer prevention.

Therapeutic cancer vaccines are also making strides. These vaccines treat existing cancer by stimulating the immune system to target and destroy cancer cells. Provenge (sipuleucel-T), an FDA-approved therapeutic vaccine for prostate cancer, has shown to improve survival rates. According to the National Cancer Institute (NCI), patients receiving Provenge had a median survival of 25.8 months compared to 21.7 months for those receiving a placebo.

The market is further bolstered by continuous research and development efforts. Advances in immunotherapy and personalized medicine are paving the way for more effective cancer vaccines. The integration of cutting-edge technologies, such as mRNA platforms, is expected to enhance vaccine efficacy and broaden their application.

However, the market faces challenges, including high development costs and complex regulatory requirements. Ensuring widespread access to these vaccines, particularly in low-resource settings, remains a critical concern.

The cancer vaccines market is poised for robust growth. Preventive vaccines like HPV and hepatitis B are essential in reducing cancer incidence, while therapeutic vaccines like Provenge offer new hope for treatment. Ongoing innovation and research will drive the market forward, addressing current challenges and expanding the impact of cancer vaccines.

Key Takeaways

- Market Value: The Cancer Vaccines Market was valued at USD 10.9 billion in 2023 and is expected to reach USD 31.8 billion by 2033, with a CAGR of 11.6%.

- Type Analysis: Preventive Vaccines dominated with 60%; essential for reducing the incidence of certain cancers.

- Vaccine Type Analysis: Monoclonal Antibodies dominated with 40%; used extensively in targeted cancer therapies.

- Cancer Type Analysis: Cervical Cancer dominated with 35%; reflecting the effectiveness of HPV vaccines.

- End-User Analysis: Hospitals dominated with 50%; primary centers for administering cancer vaccines.

- Dominant Region: North America 40%; due to advanced healthcare infrastructure and high R&D investments.

- High Growth Region: Europe; expected growth due to supportive regulatory frameworks and increasing awareness of cancer prevention.

- Analyst Viewpoint: The market is rapidly evolving with continuous advancements in immunotherapy. Future growth will be driven by personalized and combination vaccines.

- Growth Opportunities: Companies can focus on developing novel vaccines and expanding access to underserved regions to capture market share.

Driving Factors

Increasing Cancer Prevalence and Awareness Drives Market Growth

The rising incidence of various cancers globally is a significant driver for the cancer vaccines market. According to the World Health Organization, cancer is the second leading cause of death worldwide, with an estimated 19.3 million new cases in 2020. This alarming trend has led to increased awareness about cancer prevention and treatment, driving demand for innovative solutions like cancer vaccines.

For example, the success of HPV vaccines in preventing cervical cancer has heightened interest in developing vaccines for other cancer types. As more people become aware of the benefits of vaccination in cancer prevention, the demand for cancer vaccines grows. This increased awareness, combined with the urgent need to address the rising cancer cases, fuels the market for cancer vaccines.

Advancements in Immunotherapy and Personalized Medicine Drive Market Growth

The rapid progress in understanding cancer biology and the immune system has paved the way for more effective cancer vaccines. Personalized cancer vaccines, tailored to an individual's tumor mutations, are showing promising results in clinical trials.

For instance, Moderna and Merck's personalized mRNA cancer vaccine, when combined with Keytruda, has shown significant potential in treating melanoma patients. This combination demonstrated a 44% reduction in the risk of death or recurrence compared to Keytruda alone. These advancements in immunotherapy and personalized medicine are driving the development and adoption of new cancer vaccines.

The intersection of cutting-edge research and personalized treatment options enhances the effectiveness of cancer vaccines, supporting their market growth.

Increased Funding and Investment in Cancer Research Drive Market Growth

Governments, pharmaceutical companies, and private organizations are allocating substantial resources to cancer vaccine development. The Cancer Moonshot initiative in the United States, which aims to accelerate cancer research, has received a USD 1.8 billion funding boost.

This influx of capital is driving innovation and accelerating the development of novel cancer vaccines. Increased funding attracts more players to the market, fostering a competitive landscape that encourages growth. The financial support not only facilitates research but also helps bring new vaccines to market faster.

Restraining Factors

High Development Costs and Long Approval Processes Restrain Market Growth

The development of cancer vaccines is an expensive and time-consuming process, often taking over a decade and costing billions of dollars. This significant investment poses a barrier to entry for smaller biotech companies and can slow down innovation.

For instance, the development of Gardasil, an HPV vaccine that helps prevent certain types of cancer, took Merck over 15 years and cost an estimated USD 1 billion before it reached the market. These high costs and lengthy approval processes deter smaller companies from entering the market, limiting competition and slowing the pace of new vaccine development. Consequently, the overall growth of the cancer vaccines market is restrained by these substantial financial and regulatory hurdles.

Complex Manufacturing Processes and Scalability Challenges Restrain Market Growth

Cancer vaccines, especially personalized ones, require sophisticated manufacturing processes that can be difficult to scale up. This complexity can lead to production delays and higher costs, potentially limiting market growth.

An example is Dendreon's Provenge, which faced significant manufacturing challenges due to its personalized nature, contributing to the company's initial financial struggles despite the vaccine's approval. These production difficulties can delay the availability of vaccines and increase costs, making it challenging to meet market demand efficiently. As a result, the intricate manufacturing and scalability issues inherent in cancer vaccine production hinder the market's expansion.

Type Analysis

Preventive Vaccines dominate with 60% due to their effectiveness in preventing HPV and Hepatitis B-related cancers.

The Cancer Vaccines Market is segmented by type, with Preventive Vaccines leading at 60% market share. This dominance is primarily due to the effectiveness of HPV Vaccines in preventing cervical cancer and Hepatitis B Vaccines in preventing liver cancer. HPV vaccines are widely administered to young females, significantly reducing the incidence of cervical cancer. Similarly, Hepatitis B vaccines have played a crucial role in lowering liver cancer cases by preventing Hepatitis B infection, a major risk factor for liver cancer.

Therapeutic Vaccines hold a 30% market share. These vaccines are designed to treat existing cancers by stimulating the immune system to attack cancer cells. Cancer Treatment Vaccines, such as those for prostate cancer and melanoma, are part of this segment. These vaccines have shown promising results in prolonging survival and improving the quality of life for cancer patients. Personalized Cancer Vaccines, which are tailored to the individual’s specific cancer profile, represent a growing area within therapeutic vaccines, offering hope for more targeted and effective treatments.

Combination Vaccines make up the remaining 10%. These vaccines combine preventive and therapeutic approaches, aiming to provide comprehensive cancer control. Although still in early development stages, combination vaccines hold potential for providing broader protection and treatment efficacy, addressing both the prevention of cancer and the treatment of existing cancer cells.

Vaccine Type Analysis

Monoclonal Antibodies dominate with 40% due to their targeted approach and effectiveness in cancer treatment.

In the Cancer Vaccines Market segmented by vaccine type, Monoclonal Antibodies lead with a 40% share. These vaccines work by specifically targeting cancer cells and marking them for destruction by the immune system. Monoclonal antibodies are used in various cancer treatments and have shown significant success in improving patient outcomes. Their ability to target specific antigens on cancer cells while sparing normal cells makes them highly effective and reduces side effects.

Peptide-Based Vaccines hold a 20% market share. These vaccines use specific peptides to trigger an immune response against cancer cells. They are relatively easy to produce and can be tailored to different types of cancer. Peptide-based vaccines are currently being researched for their potential to treat various cancers, including melanoma and prostate cancer, with some showing promising results in clinical trials.

DNA-Based Vaccines account for 15% of the market. These vaccines use genetic material to induce an immune response against cancer cells. They are designed to provide long-lasting immunity and have shown potential in preclinical and early clinical studies. DNA-based vaccines are still in the developmental stages but are considered a promising avenue for future cancer treatments.

RNA-Based Vaccines hold a 10% share. These vaccines use messenger RNA to instruct cells to produce antigens that trigger an immune response. RNA-based vaccines gained attention with the success of COVID-19 vaccines and are now being explored for cancer treatment. Their ability to be quickly designed and manufactured makes them a flexible option for developing new cancer vaccines.

Protein Subunit Vaccines make up 10% of the market. These vaccines use specific protein fragments from cancer cells to stimulate an immune response. They are considered safe and can be produced relatively easily. Protein subunit vaccines are being researched for various cancers and have shown potential in inducing a robust immune response.

Cell-Based Vaccines account for the remaining 5%. These vaccines use whole cells, often modified to enhance their ability to stimulate the immune system, to target cancer. They are complex to produce but offer the advantage of presenting multiple antigens to the immune system, potentially improving efficacy. Cell-based vaccines are an area of active research and hold promise for future cancer therapies.

Cancer Type Analysis

Cervical Cancer dominates with 35% due to the widespread use of HPV vaccines.

In the Cancer Vaccines Market segmented by cancer type, Cervical Cancer leads with a 35% share. The widespread use of HPV vaccines has significantly reduced the incidence of cervical cancer, making it the most prominent segment. HPV vaccines are effective in preventing the types of HPV that cause most cervical cancers, leading to high vaccination rates and strong market growth in this area.

Prostate Cancer holds a 20% market share. Prostate cancer vaccines, including both therapeutic and preventive types, are used to manage and treat this common cancer in men. The demand for effective prostate cancer treatments drives this segment, with ongoing research and clinical trials aimed at improving vaccine efficacy.

Breast Cancer accounts for 15% of the market. Although there are no widely used preventive vaccines for breast cancer, therapeutic vaccines are being developed and tested. These vaccines aim to stimulate the immune system to target breast cancer cells, providing a new avenue for treatment.

Lung Cancer holds a 10% share. Lung cancer vaccines are in various stages of development, with some showing promise in clinical trials. The high incidence and mortality rates of lung cancer drive the demand for effective vaccines, making this a critical area of research and development.

Melanoma makes up 10% of the market. Melanoma vaccines, particularly those using peptide-based or cell-based approaches, are being developed to treat this aggressive form of skin cancer. Early clinical trials have shown promising results, supporting the growth of this segment.

Bladder Cancer holds 5% of the market. Bladder cancer vaccines are less common but are an area of active research. These vaccines aim to stimulate an immune response against bladder cancer cells, potentially improving treatment outcomes for patients with this type of cancer.

Other cancers, including those with lower incidence rates or those still in early stages of vaccine development, make up the remaining 5%. Research in these areas continues to explore new ways to use vaccines for cancer prevention and treatment.

End-User Analysis

Hospitals dominate with 50% due to their central role in administering cancer treatments and vaccines.

In the Cancer Vaccines Market segmented by end-user, Hospitals lead with a 50% share. Hospitals are the primary settings for administering cancer treatments and vaccines. They have the necessary infrastructure, medical expertise, and patient care capabilities to deliver complex cancer therapies. The central role of hospitals in patient treatment and care drives their dominance in this market segment.

Cancer Treatment Centers hold a 25% market share. These specialized centers focus exclusively on cancer diagnostics and treating cancer, including the administration of vaccines. They offer advanced treatment options and often participate in clinical trials for new cancer vaccines. Their specialized focus and expertise in cancer care support their significant market share.

Research and Academic Institutions account for 15% of the market. These institutions are involved in the development and testing of new cancer vaccines. They conduct clinical trials, perform basic research, and collaborate with pharmaceutical companies to bring new vaccines to market. Their contributions to vaccine development are critical to the overall growth of the cancer vaccine market.

Pharmaceutical Companies make up the remaining 10%. These companies develop, manufacture, and market cancer vaccines. They invest heavily in research and development to create new vaccines and improve existing ones. Pharmaceutical companies also conduct clinical trials and work to obtain regulatory approvals for their products. Their role in bringing new vaccines to market supports their presence in this segment.

Key Market Segments

By Type

- Preventive Vaccines

- HPV Vaccines (for Cervical Cancer)

- Hepatitis B Vaccines (for Liver Cancer)

- Therapeutic Vaccines

- Cancer Treatment Vaccines (e.g., for Prostate Cancer, Melanoma)

- Personalized Cancer Vaccines

- Combination Vaccines

- Preventive and Therapeutic

By Vaccine Type

- Monoclonal Antibodies

- Peptide-Based Vaccines

- DNA-Based Vaccines

- RNA-Based Vaccines

- Protein Subunit Vaccines

- Cell-Based Vaccines

By Cancer Type

- Breast Cancer

- Cervical Cancer

- Prostate Cancer

- Lung Cancer

- Melanoma

- Bladder Cancer

- Others

By End-User

- Hospitals

- Cancer Treatment Centers

- Research and Academic Institutions

- Pharmaceutical Companies

Growth Opportunities

Combination Therapies Offer Growth Opportunity

Combining cancer vaccines with other immunotherapies or traditional treatments offers significant potential for improved efficacy. For example, the combination of cancer vaccines with checkpoint inhibitors has shown promising results in clinical trials, as seen with Moderna and Merck's melanoma vaccine combined with Keytruda.

This approach can enhance the immune response against cancer cells, leading to better patient outcomes. By exploring combination therapies, the cancer vaccine market can expand its treatment options, improve efficacy rates, and attract investment in research and development, driving market growth.

Expansion into Preventive Vaccines for Non-Viral Cancers Offers Growth Opportunity

While HPV vaccines have been successful in preventing cervical cancer, there's an opportunity to develop preventive vaccines for non-viral cancers. Research into vaccines targeting cancer-specific antigens or mutations could lead to a new category of preventive cancer vaccines, potentially revolutionizing cancer prevention strategies.

By focusing on non-viral cancers, the market can address a broader range of cancers, offering new preventive measures and reducing cancer incidence. This expansion into preventive vaccines for non-viral cancers presents a significant opportunity to advance cancer prevention, attract funding, and drive market growth.

Trending Factors

mRNA Technology in Cancer Vaccines Are Trending Factors

The success of mRNA vaccines for COVID-19 has accelerated interest in using this technology for cancer vaccines. Companies like BioNTech and Moderna are leveraging their mRNA platforms to develop personalized cancer vaccines, with several candidates in clinical trials.

This technology allows for rapid development and customization of vaccines to target specific cancer types. By utilizing mRNA technology, the cancer vaccine market can advance personalized medicine, enhance treatment effectiveness, and drive significant growth and innovation in cancer therapies.

Artificial Intelligence in Vaccine Development Are Trending Factors

AI and machine learning are increasingly being used to accelerate cancer vaccine development. These technologies can help identify potential antigens, predict vaccine efficacy, and optimize clinical trial designs. For instance, Gritstone Oncology uses AI to identify neoantigens for its personalized cancer vaccine candidates.

The use of AI streamlines the research and development process, making it faster and more efficient. By integrating AI in vaccine development, the cancer vaccine market can improve discovery rates, reduce development costs, and bring effective cancer treatments to market more quickly, driving trends in technological advancement.

Regional Analysis

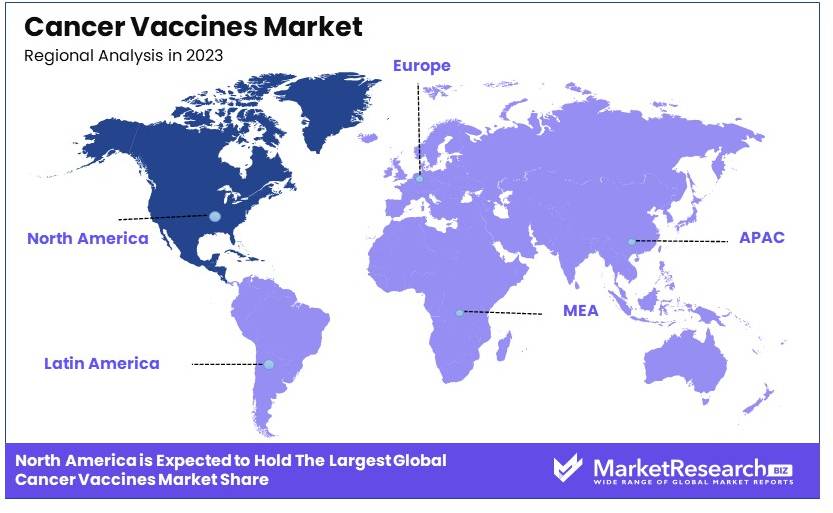

North America Dominates with 40% Market Share in the Cancer Vaccines Market

North America commands a 40% share of the global cancer vaccines market, driven by advanced biomedical research capabilities and substantial healthcare investments. The region's strong pharmaceutical industry and significant government and private funding for cancer research are pivotal. High public awareness and screening rates also accelerate the adoption of preventive and therapeutic cancer vaccines, boosting market growth.

The cancer vaccines market in North America benefits from collaborative efforts between research institutions, biotechnology firms, and pharmaceutical companies, which facilitate innovation and rapid development of new vaccines. The prevalence of cancer in the region creates a pressing demand for effective treatments, including vaccines. Furthermore, regulatory support for vaccine approval and a well-established healthcare infrastructure contribute to the vigorous market activity.

The future of the cancer vaccines market in North America appears strong, with ongoing research into novel vaccine technologies and immunotherapy treatments expected to drive growth. The rising incidence of various cancers and the aging population may further necessitate advancements in vaccine development. North America is likely to maintain or even increase its market share as it continues to lead in innovative cancer treatment solutions.

Regional Market Share and Growth Statistics

- Europe: Europe holds a 30% share of the market, supported by robust healthcare systems and increasing government funding for cancer research.

- Asia Pacific: Representing 20% of the market, Asia Pacific's growth is spurred by rising healthcare expenditures and growing awareness of cancer prevention and treatments.

- Middle East & Africa: This region accounts for 5% of the market. Growth is modest but increasing due to improving healthcare infrastructure and international collaborations in medical research.

- Latin America: With a 5% market share, Latin America is slowly expanding its focus on healthcare innovations and public health campaigns targeting cancer awareness.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The cancer vaccines market is dominated by key players with significant impact and strategic positioning. GlaxoSmithKline plc and Merck & Co., Inc. lead with their extensive research and development capabilities. Pfizer Inc. and Sanofi S.A. have strong market presence with their innovative vaccine solutions.

AstraZeneca plc and Roche Holding AG are recognized for their advanced cancer vaccine research. Moderna, Inc. and Inovio Pharmaceuticals, Inc. leverage cutting-edge technology to develop effective vaccines. Dendreon Pharmaceuticals LLC and Aduro Biotech, Inc. offer specialized cancer vaccines, enhancing their market positions.

Bavarian Nordic and Agenus Inc. focus on innovative immunotherapy solutions. OncoSec Medical Incorporated and BioNTech SE are key players with strong research and development pipelines. ImmunoCellular Therapeutics, Ltd. provides targeted cancer vaccine solutions.

These companies use advanced technologies, extensive research, and strong market presence to lead the cancer vaccines market. Their ability to innovate and develop effective vaccines ensures their continued market influence and growth.

Market Key Players

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Pfizer Inc.

- Sanofi S.A.

- AstraZeneca plc

- Roche Holding AG

- Moderna, Inc.

- Inovio Pharmaceuticals, Inc.

- Dendreon Pharmaceuticals LLC

- Aduro Biotech, Inc.

- Bavarian Nordic

- Agenus Inc.

- OncoSec Medical Incorporated

- BioNTech SE

- ImmunoCellular Therapeutics, Ltd.

Recent Developments

- Moderna has commenced phase 1/2 clinical trials for its new PD-1/IDO1 cancer vaccine, mRNA-4359. This vaccine targets advanced solid tumors by generating antibodies against PD-L1 and IDO1, with initial treatments starting at Imperial College Healthcare NHS Trust. This trial seeks to evaluate the safety and efficacy of the vaccine combined with other cancer therapies.

- BioNTech SE, in partnership with Genentech, is testing an mRNA-based colorectal cancer vaccine. The vaccine, developed by analyzing patient-specific tumor mutations, aims to prevent cancer recurrence by stimulating a targeted immune response. This trial is part of a broader effort to provide personalized immunotherapies to up to 10,000 patients by 2030.

Report Scope

Report Features Description Market Value (2023) USD 10.9 Billion Forecast Revenue (2033) USD 31.8 Billion CAGR (2024-2033) 11.6% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Preventive Vaccines [HPV Vaccines (for Cervical Cancer), Hepatitis B Vaccines (for Liver Cancer)], Therapeutic Vaccines [Cancer Treatment Vaccines (e.g., for Prostate Cancer, Melanoma), Personalized Cancer Vaccines], Combination Vaccines [Preventive and Therapeutic]), By Vaccine Type (Monoclonal Antibodies, Peptide-Based Vaccines, DNA-Based Vaccines, RNA-Based Vaccines, Protein Subunit Vaccines, Cell-Based Vaccines), By Cancer Type (Breast Cancer, Cervical Cancer, Prostate Cancer, Lung Cancer, Melanoma, Bladder Cancer, Others), By End-User (Hospitals, Cancer Treatment Centers, Research and Academic Institutions, Pharmaceutical Companies) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape GlaxoSmithKline plc, Merck & Co., Inc., Pfizer Inc., Sanofi S.A., AstraZeneca plc, Roche Holding AG, Moderna, Inc., Inovio Pharmaceuticals, Inc., Dendreon Pharmaceuticals LLC, Aduro Biotech, Inc., Bavarian Nordic, Agenus Inc., OncoSec Medical Incorporated, BioNTech SE, ImmunoCellular Therapeutics, Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Pfizer Inc.

- Sanofi S.A.

- AstraZeneca plc

- Roche Holding AG

- Moderna, Inc.

- Inovio Pharmaceuticals, Inc.

- Dendreon Pharmaceuticals LLC

- Aduro Biotech, Inc.

- Bavarian Nordic

- Agenus Inc.

- OncoSec Medical Incorporated

- BioNTech SE

- ImmunoCellular Therapeutics, Ltd.

Our Clients

View Our Licence Options