HPV Vaccines Market Report By Type of Vaccine (Bivalent HPV Vaccine (Cervarix), Quadrivalent HPV Vaccine (Gardasil), Nonavalent HPV Vaccine (Gardasil 9)), By Valency (Bivalent, Quadrivalent, Nonavalent), By Indication (Cervical Cancer Prevention, Anal Cancer Prevention, Vulvar and Vaginal Cancer Prevention, Genital Warts Prevention, Oropharyngeal and Other Head and Neck Cancers Prevention), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Public Health Clinics, Online Pharmacies, Others), By Region and Companies - Industry Segment Ou

-

47780

-

June 2024

-

291

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

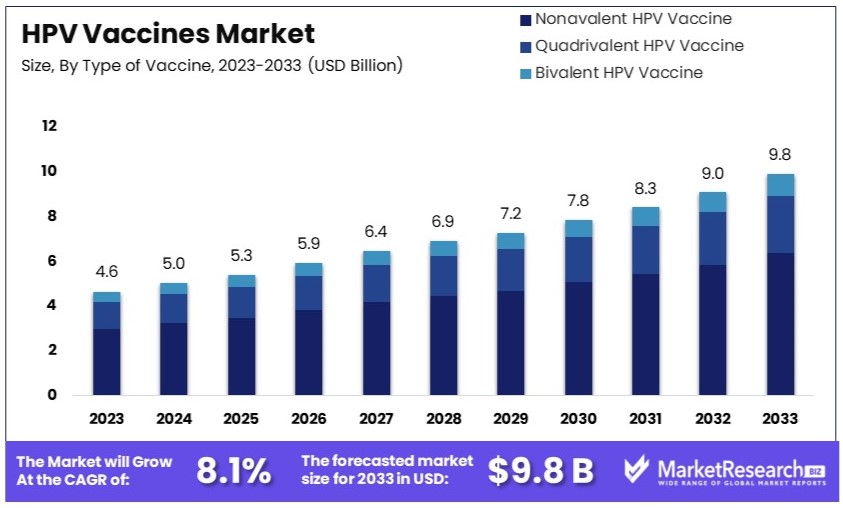

The Global HPV Vaccines Market size is expected to be worth around USD 9.8 Billion by 2033, from USD 4.6 Billion in 2023, growing at a CAGR of 8.1% during the forecast period from 2024 to 2033.

The Human Papillomavirus (HPV) Vaccines Market encompasses the development, production, and distribution of vaccines aimed at preventing infections caused by the human papillomavirus.

These vaccines are pivotal in the global health strategy to combat cervical cancer, as well as other types of cancers and genital warts associated with various strains of HPV. This market is characterized by robust participation from leading pharmaceutical companies who engage in extensive research and development to enhance vaccine efficacy and coverage.

The Human Papillomavirus (HPV) Vaccines Market is positioned at a crucial intersection of public health needs and pharmaceutical innovation. As cervical cancer remains the fourth most common cancer among women globally, the urgency for effective preventive measures is underscored by staggering statistics.

In 2022 alone, around 660,000 new cases and 350,000 deaths were recorded worldwide, predominantly in low- and middle-income countries where access to healthcare and preventive services may be limited. This highlights a significant market opportunity for HPV vaccines.

In the United States, the incidence and mortality rates stand at 7.6 and 2.2 per 100,000 women per year, respectively. These figures not only reflect the potential demand for preventive solutions in high-income countries but also underline the effectiveness of existing HPV vaccination programs. Furthermore, approximately 0.7% of women in the U.S. are likely to be diagnosed with cervical cancer at some point in their lives, presenting a persistent risk that supports ongoing vaccination efforts.

The market dynamics of the HPV vaccines are influenced by several factors: the increasing endorsement by health authorities worldwide, the integration of vaccinations into national health policies, and an enhanced awareness of the vaccines' role in cancer prevention. Pharmaceutical companies are thus motivated to innovate and expand their vaccine offerings. Additionally, new advancements in vaccine technology may increase efficacy and patient compliance, further stimulating market growth.

Given these factors, the HPV Vaccines Market is expected to witness sustained growth. Market expansion will likely be propelled by strategic alliances between global health bodies and pharmaceutical companies, aimed at increasing vaccine accessibility and affordability across diverse geographic regions. This is particularly pertinent for market strategists and health policymakers who are looking to optimize distribution channels and increase global vaccination rates to reduce the incidence of HPV-related cancers.

Key Takeaways

- Market Value: The Global HPV Vaccines Market was valued at USD 4.6 Billion in 2023, and is projected to reach USD 9.8 Billion by 2033, with a CAGR of 8.1%.

- Type of Vaccine Analysis: Nonavalent HPV Vaccine dominates with 60% due to broader coverage and high effectiveness, making it highly preferred in vaccination programs.

- Indication Analysis: Cervical Cancer Prevention dominates with 50% due to high incidence and strong prevention focus, driving the primary demand in the HPV vaccines market.

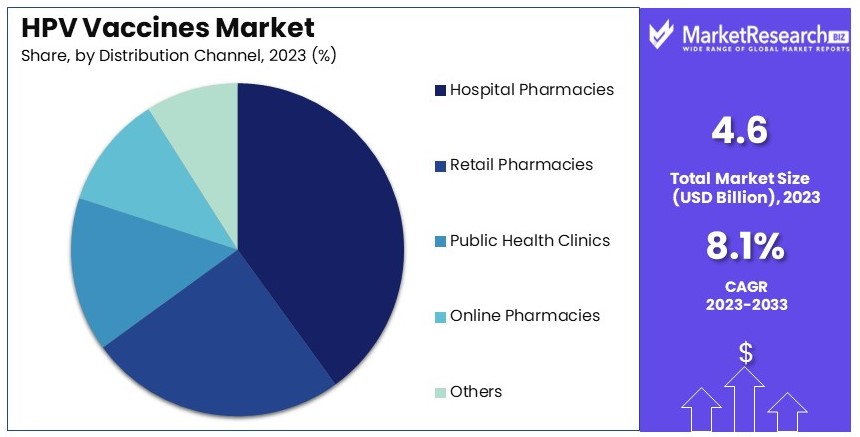

- Distribution Channel Analysis: Hospital Pharmacies dominate with 40% due to their central role in healthcare delivery and vaccination programs, facilitating access and convenience.

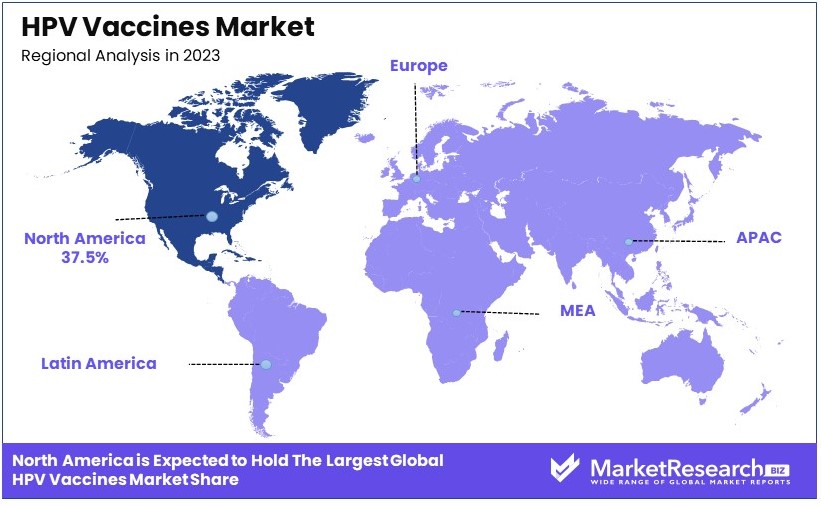

- Dominant Region: North America dominates with 37.5% market share, bolstered by high awareness, strong vaccination programs, and substantial public health support.

- High Growth Region: Asia Pacific is projected as a high growth region, currently holding 20% of the market share, with increasing awareness and healthcare improvements driving expansion.

- Analyst Viewpoint: The HPV Vaccines Market is poised for robust growth, driven by escalating public health initiatives and strategic pharmaceutical collaborations. The market's potential is amplified by ongoing advancements in vaccine technology and global health policies incorporating HPV vaccination.

- Growth Opportunities: Expanding the target population to include males and developing therapeutic HPV vaccines are pivotal areas for growth, potentially increasing market penetration and addressing unmet medical needs.

Driving Factors

Increasing Awareness and Government Initiatives Drive Market Growth

The rising awareness about the risks associated with HPV infections and the availability of effective human vaccines have significantly driven the demand for HPV vaccines. Public health campaigns have educated people on the dangers of HPV, leading to increased vaccination rates. Government initiatives have been pivotal in this growth. National immunization programs and subsidized vaccination efforts have made HPV vaccines more accessible and affordable.

For instance, Australia's National HPV Vaccination Program has led to a substantial increase in vaccination rates among eligible populations. The program's success can be attributed to government funding and widespread awareness campaigns. Additionally, similar initiatives in countries like the UK and the US have boosted market growth by reducing vaccine costs and improving distribution channels. These efforts ensure that a larger segment of the population can receive the vaccine, thereby increasing overall market demand.

Rising Incidence of HPV-related Cancers Drives Market Growth

The growing incidence of HPV-related cancers, such as cervical, anal, and oropharyngeal cancers, has underscored the importance of HPV vaccination. As research highlights the burden of these cancers, the demand for preventive measures like HPV vaccines has surged. For example, the increasing prevalence of HPV-related oropharyngeal cancers among men has led to recommendations for gender-neutral vaccination in several countries.

This shift aims to protect both males and females, recognizing that HPV affects both genders. The heightened awareness of these cancers and their association with HPV has driven a greater emphasis on vaccination, contributing to market expansion. Moreover, healthcare professionals and researchers continue to advocate for widespread vaccination to curb the rising cancer rates, further fueling market growth.

Expanding Target Population Drives Market Growth

Initially, HPV vaccines were primarily targeted at females to prevent cervical cancer. However, with increasing evidence of the vaccines' efficacy in preventing other HPV-related diseases in both genders, the target population has expanded to include males. This broader target population has significantly contributed to the market's growth.

The introduction of gender-neutral vaccination programs in countries like the United States and Canada has led to an increase in HPV vaccine uptake. These programs recognize the need to protect all individuals from HPV-related diseases, thereby broadening the market base. As more countries adopt similar strategies, the market for HPV vaccines is expected to grow further. This expansion ensures a larger and more inclusive market, driving higher demand and greater sales for vaccine manufacturers.

Restraining Factors

Vaccine Hesitancy and Concerns Restrain Market Growth

Despite the proven safety and efficacy of HPV vaccines, vaccine hesitancy has significantly hindered market growth. Concerns about potential side effects and misinformation have led to lower vaccination rates. This issue is pronounced in regions like Japan and Denmark, where public skepticism has resulted in declining HPV vaccination coverage.

Fear and mistrust of vaccines, fueled by misconceptions, reduce the willingness of people to get vaccinated. This hesitancy limits the market penetration of HPV vaccines, preventing broader public health benefits. Efforts to combat misinformation and educate the public about the benefits and safety of HPV vaccines are essential to overcoming this barrier.

Affordability and Access Issues Restrain Market Growth

The high cost of HPV vaccines and limited access to healthcare services in certain regions pose significant challenges. These issues are particularly acute in low- and middle-income countries, where financial constraints and inadequate healthcare infrastructure limit vaccine adoption. The high price of vaccines often prevents their inclusion in national immunization programs.

For instance, many developing countries struggle to afford HPV vaccines, leading to lower vaccination rates. These affordability and access barriers significantly restrict market growth, highlighting the need for global initiatives to reduce costs and improve healthcare access.

Type of Vaccine Analysis

Nonavalent HPV Vaccine dominates with 60% due to broader coverage and high effectiveness.

The HPV vaccines market is segmented by the type of vaccine into Bivalent HPV Vaccine (Cervarix), Quadrivalent HPV Vaccine (Gardasil), and Nonavalent HPV Vaccine (Gardasil 9). Among these, the Nonavalent HPV Vaccine (Gardasil 9) dominates the market due to its broader coverage against HPV strains. Gardasil 9 protects against nine HPV types, including those responsible for the majority of HPV-related cancers and genital warts.

Its comprehensive protection has made it the preferred choice in many national immunization programs. The vaccine's effectiveness in preventing various cancers and genital warts has driven its high adoption rate. The demand for Gardasil 9 is expected to continue growing, supported by recommendations from health authorities and its inclusion in public health initiatives.

The Bivalent HPV Vaccine (Cervarix) and Quadrivalent HPV Vaccine (Gardasil) also play significant roles in the market. Cervarix focuses on preventing cervical cancer caused by HPV types 16 and 18, which are responsible for the majority of cervical cancer cases. Despite its limited valency, Cervarix remains important in regions with specific public health strategies targeting cancer care.

Gardasil, the Quadrivalent vaccine, covers four HPV types, including those causing genital warts and cervical cancer. It has been widely used before the introduction of Gardasil 9 and continues to be an essential part of vaccination programs in several countries. The competition between these vaccines drives innovation and improvement, contributing to overall market growth.

Indication Analysis

Cervical Cancer Prevention dominates with 50% due to high incidence and strong prevention focus.

The market is segmented by indication into Cervical Cancer Prevention, Anal Cancer Prevention, Vulvar and Vaginal Cancer Prevention, Genital Warts Prevention, and Oropharyngeal and Other Head and Neck Cancers Prevention. Cervical Cancer Prevention is the dominant sub-segment, driven by the high incidence of cervical cancer globally and the strong focus on preventing this type of cancer through vaccination.

HPV vaccines' effectiveness in preventing cervical cancer has led to widespread adoption, making it the primary driver of the HPV vaccines market. Public health campaigns and government initiatives have further emphasized cervical cancer prevention, bolstering the demand for HPV vaccines targeting this indication.

Other indications, such as Anal Cancer Prevention, Vulvar and Vaginal Cancer Prevention, Genital Warts Prevention, and Oropharyngeal and Other Head and Neck Cancers Prevention, also contribute to market growth. The rising awareness of HPV's role in these cancers and conditions has increased the demand for comprehensive vaccination programs.

Vaccination efforts targeting these indications are growing, especially with increasing research and public health initiatives highlighting the importance of preventing a broad spectrum of HPV-related diseases. These additional indications enhance the overall value proposition of HPV vaccines, encouraging their inclusion in more extensive vaccination programs and supporting market expansion.

Distribution Channel Analysis

Hospital Pharmacies dominate with 40% due to central role in healthcare delivery and vaccination programs.

The distribution channels for HPV vaccines include Hospital Pharmacies, Retail Pharmacies, Public Health Clinics, Online Pharmacies, and Others. Hospital Pharmacies dominate the market due to their central role in healthcare delivery and vaccination programs.

Hospitals are often the primary sites for administering vaccines, especially in countries with strong public health systems. The ability to provide vaccinations during routine medical visits enhances the accessibility and convenience for patients, driving the dominance of hospital pharmacies in the distribution of HPV vaccines.

Retail Pharmacies and Public Health Clinics also play significant roles in the distribution of HPV vaccines. Retail pharmacies offer convenience and accessibility, making it easier for individuals to receive vaccinations without needing to visit a hospital.

Public Health Clinics are critical in regions with strong government-led vaccination programs, providing vaccines to underserved populations and ensuring broad coverage. Online Pharmacies are emerging as a convenient option for purchasing vaccines, particularly in areas with well-developed e-commerce infrastructure. The availability of multiple distribution channels ensures that HPV vaccines reach a wide range of populations, supporting market growth.

Key Market Segments

By Type of Vaccine

- Bivalent HPV Vaccine (Cervarix)

- Quadrivalent HPV Vaccine (Gardasil)

- Nonavalent HPV Vaccine (Gardasil 9)

By Indication

- Cervical Cancer Prevention

- Anal Cancer Prevention

- Vulvar and Vaginal Cancer Prevention

- Genital Warts Prevention

- Oropharyngeal and Other Head and Neck Cancers Prevention

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Public Health Clinics

- Online Pharmacies

- Others

Growth Opportunities

Expanding Target Population for Males Offers Growth Opportunity

Expanding the target population to include boys and men presents a significant growth opportunity in the HPV vaccines market. As awareness of the benefits of HPV vaccination for males increases, the potential for preventing HPV-related cancers and diseases in both genders is recognized.

The World Health Organization's recent recommendation to include males in HPV vaccination programs has opened new avenues for market growth. By targeting a broader population, the customer base expands, driving higher demand for vaccines. This expansion can lead to increased vaccination rates, contributing to the overall reduction of HPV-related health issues globally.

Development of Therapeutic HPV Vaccines Offers Growth Opportunity

The ongoing research and development of therapeutic HPV vaccines represent a substantial growth opportunity. Unlike prophylactic vaccines, therapeutic vaccines aim to treat existing HPV infections and associated diseases. Successful development and commercialization of these vaccines could revolutionize the market by providing treatment options for those already infected with HPV.

Several pharmaceutical companies are currently conducting clinical trials on therapeutic HPV vaccines, which could significantly expand the market. If these trials prove successful, the introduction of therapeutic vaccines would not only address existing infections but also enhance the overall market potential by offering comprehensive HPV management solutions.

Trending Factors

Increasing Adoption of Gender-Neutral Vaccination Programs Are Trending Factors

The adoption of gender-neutral HPV vaccination programs is a growing trend in the HPV vaccines market. More countries are recognizing the importance of vaccinating both males and females to prevent various cancers and diseases. This trend is driven by the benefits of achieving herd immunity and reducing the overall burden of HPV-related health issues.

Countries like Australia, Canada, and the United States have already implemented gender-neutral vaccination programs, setting a precedent for others to follow. The increased adoption of these programs highlights the expanding recognition of equal protection for both genders, further driving market growth and vaccination coverage.

Focus on Increasing Vaccination Coverage and Catch-Up Programs Are Trending Factors

Efforts to increase vaccination coverage and implement catch-up programs are trending in the HPV vaccines market. These strategies aim to ensure that individuals who missed their initial vaccinations still receive protection against HPV. By broadening the reach of vaccination programs, the overall burden of HPV-related diseases can be reduced.

Many countries have introduced catch-up vaccination programs for older age groups to improve overall vaccination rates. This focus on increasing coverage reflects the commitment to maximizing the impact of HPV vaccines and enhancing public health outcomes. Such initiatives are crucial for driving higher vaccination rates and achieving comprehensive protection within the population

Regional Analysis

North America Dominates with 37.5% Market Share

North America's dominance in the HPV vaccines market is driven by several key factors. High awareness about HPV and its associated risks, coupled with robust vaccination programs, contribute significantly. Government initiatives and funding have made HPV vaccines widely accessible and affordable. Additionally, the region benefits from advanced healthcare infrastructure and strong support from public health organizations.

Regional characteristics, such as a proactive approach to public health and extensive insurance coverage, enhance market performance. High vaccination rates in countries like the United States and Canada further bolster market growth. The presence of leading pharmaceutical companies and continuous research and development efforts also play a crucial role.

Looking ahead, North America's market presence is expected to remain strong. Continued government support, increasing awareness, and ongoing R&D investments will drive further growth. The region's commitment to public health and preventive measures ensures a sustained demand for HPV vaccines, solidifying its market dominance.

Market Share in Other Regions

In Europe, the HPV vaccines market holds a significant share at 30%. This is due to comprehensive vaccination programs, strong government support, and high awareness levels. Countries like the UK and Germany have implemented successful national immunization programs.

Asia Pacific accounts for 20% of the market share. Growing awareness, government initiatives, and improving healthcare infrastructure drive market growth in this region. Countries like Australia and Japan are at the forefront, promoting widespread HPV vaccination.

The Middle East & Africa region has a smaller market share of 8%. Limited access to healthcare and lower awareness levels are primary challenges. However, increasing efforts to improve healthcare infrastructure and government initiatives are expected to boost market growth in the future.

Latin America holds a 4.5% market share. Efforts to increase vaccination coverage and government-led immunization programs in countries like Brazil and Mexico contribute to this growth. The region is gradually overcoming barriers such as limited healthcare access and financial constraints.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The HPV vaccines market features several influential players. Merck & Co., Inc. and GlaxoSmithKline plc are market leaders, with established products such as Gardasil and Cervarix. These companies benefit from extensive global reach, strong brand recognition, and significant R&D investments, positioning them as dominant forces.

Sanofi and Johnson & Johnson Services, Inc. hold substantial market shares due to their broad pharmaceutical portfolios and advanced vaccine technologies. Their strategic partnerships and robust distribution networks enhance their market influence.

Emerging companies like Bharat Biotech and Serum Institute of India Pvt. Ltd. are notable for their contributions to affordable vaccine production. Their cost-effective solutions expand market accessibility, particularly in developing regions.

CSL Limited and Inovio Pharmaceuticals, Inc. focus on innovative vaccine technologies. Their emphasis on next-generation vaccine platforms positions them as key innovators in the market.

MedImmune, a subsidiary of AstraZeneca, leverages its parent company's resources to maintain a competitive edge. Similarly, Xiamen Innovax Biotech Co., Ltd. and Dynavax Technologies Corporation contribute through specialized vaccine research and development.

GeoVax Labs, Inc., VBI Vaccines Inc., and Profectus BioSciences, Inc. are smaller players with potential for growth due to their focus on novel vaccine candidates and strategic collaborations.

Overall, these key players shape the HPV vaccines market through a mix of established products, innovation, and strategic partnerships, ensuring ongoing market growth and development.

Market Key Players

- Merck & Co., Inc.

- GlaxoSmithKline plc

- Sanofi

- Johnson & Johnson Services, Inc.

- Bharat Biotech

- Serum Institute of India Pvt. Ltd.

- CSL Limited

- Inovio Pharmaceuticals, Inc.

- MedImmune (a subsidiary of AstraZeneca)

- Xiamen Innovax Biotech Co., Ltd.

- Dynavax Technologies Corporation

- GeoVax Labs, Inc.

- VBI Vaccines Inc.

- Profectus BioSciences, Inc.

- Other Key Players

Recent Developments

- June 2024: The HPV vaccine has been found to significantly reduce the risk of head and neck cancer in men. A recent analysis revealed that the vaccine could potentially reduce the risk of HPV-associated cancers by 56% in males and 36% in females. The vaccine can prevent over 90% of HPV-related cancers, but vaccination rates remain low, particularly among males.

- March 2024: Governments, donors, and multilateral institutions have announced new policy, programmatic, and financial commitments to eliminate cervical cancer. The commitments include nearly US$ 600 million in new funding and aim to expand vaccine coverage and strengthen screening and treatment programs. This historic step could lead to the elimination of cervical cancer for the first time.

- February 2024: SII to Boost HPV Vaccine Output in Sync with Govt's Immunization Drive Serum Institute of India (SII) plans to increase its annual production capacity of quadrivalent human papillomavirus (HPV) vaccines to around 70 million doses, starting this year. This move is in sync with the government's immunization drive, which aims to include the vaccine in the Universal Immunization Program (UIP). Discussions on pricing for the government setup are still preliminary.

- February 2024: Finance Minister Nirmala Sitharaman announced the government's intention to include the HPV vaccine in its immunization program. The vaccine will be administered to girls in the age group of 9 to 14 years for the prevention of cervical cancer. The campaign will be rolled out in three phases over three years, with the vaccine to be included in routine immunization for 9-year-old girls.

Report Scope

Report Features Description Market Value (2023) USD 4.6 Billion Forecast Revenue (2033) USD 9.8 Billion CAGR (2024-2033) 8.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type of Vaccine (Bivalent HPV Vaccine (Cervarix), Quadrivalent HPV Vaccine (Gardasil), Nonavalent HPV Vaccine (Gardasil 9)), By Valency (Bivalent, Quadrivalent, Nonavalent), By Indication (Cervical Cancer Prevention, Anal Cancer Prevention, Vulvar and Vaginal Cancer Prevention, Genital Warts Prevention, Oropharyngeal and Other Head and Neck Cancers Prevention), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Public Health Clinics, Online Pharmacies, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Merck & Co., Inc., GlaxoSmithKline plc, Sanofi, Johnson & Johnson Services, Inc., Bharat Biotech, Serum Institute of India Pvt. Ltd., CSL Limited, Inovio Pharmaceuticals, Inc., MedImmune (a subsidiary of AstraZeneca), Xiamen Innovax Biotech Co., Ltd., Dynavax Technologies Corporation, GeoVax Labs, Inc., VBI Vaccines Inc., Profectus BioSciences, Inc., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Merck & Co., Inc.

- GlaxoSmithKline plc

- Sanofi

- Johnson & Johnson Services, Inc.

- Bharat Biotech

- Serum Institute of India Pvt. Ltd.

- CSL Limited

- Inovio Pharmaceuticals, Inc.

- MedImmune (a subsidiary of AstraZeneca)

- Xiamen Innovax Biotech Co., Ltd.

- Dynavax Technologies Corporation

- GeoVax Labs, Inc.

- VBI Vaccines Inc.

- Profectus BioSciences, Inc.

- Other Key Players

Our Clients

View Our Licence Options