Autonomous Vehicles Market By Type(Passenger Vehicle, Commercial Vehicle), By Mobility Type (Shared Mobility, Personal Mobility), By Level of Autonomy (L1, L2, L3, L4, L5), By Propulsion Type (Semi-autonomous, Fully Autonomous), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast Period 2024-2033

-

51085

-

Sept 2024

-

210

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

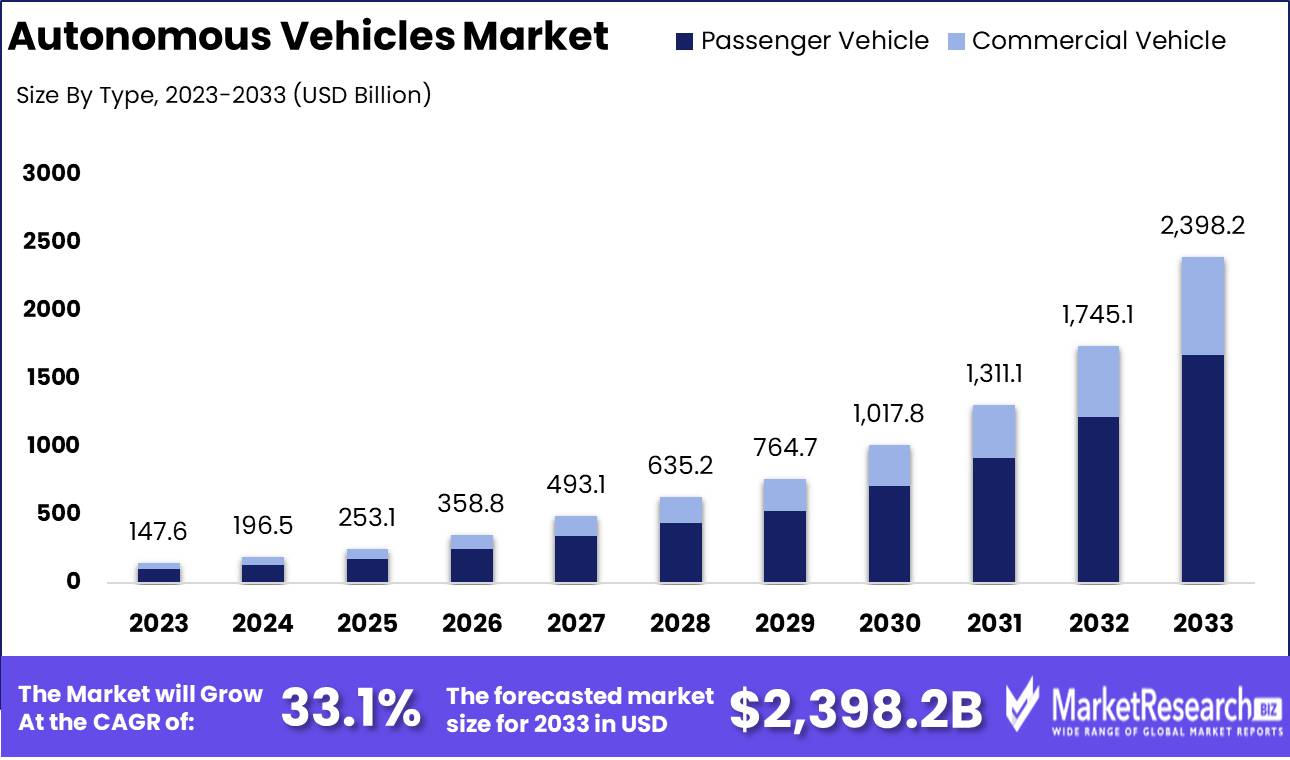

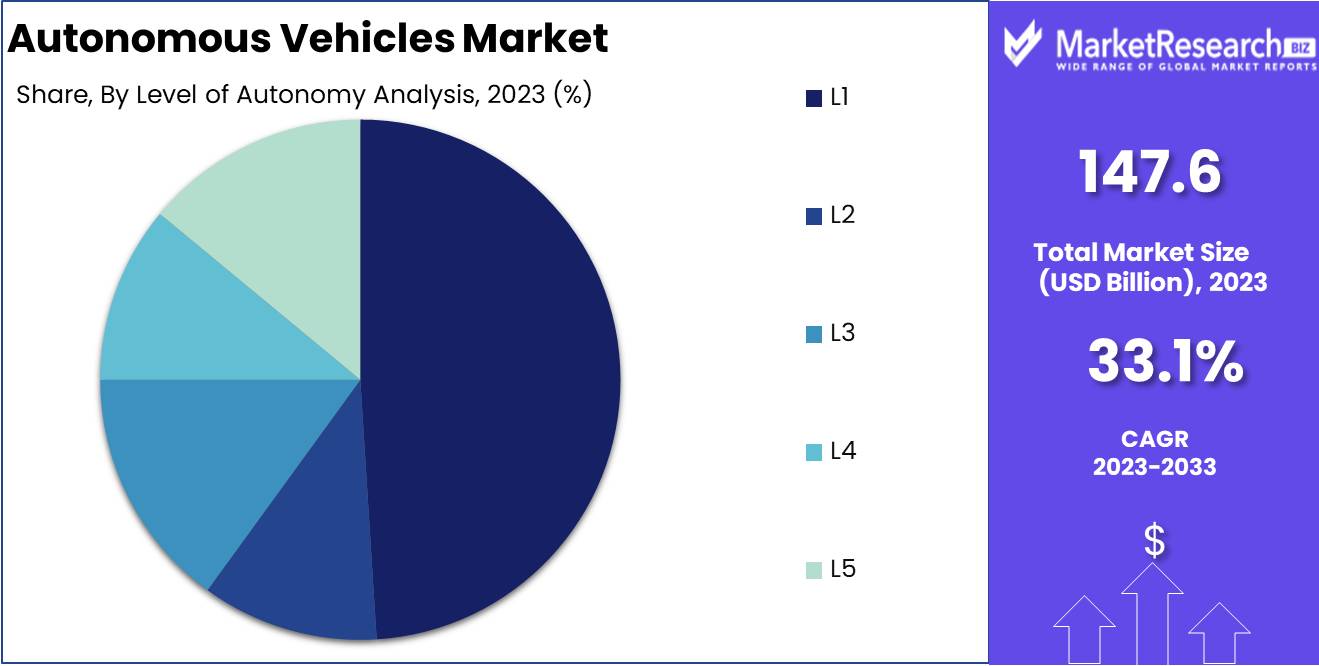

The Global Autonomous Vehicles Market was valued at USD 147.6 Billion in 2023. It is expected to reach USD 2,398.2 Billion by 2033, with a Compound annual growth rate (CAGR) of 33.1% during the forecast period from 2024 to 2033.

The Autonomous Vehicles market refers to the sector within the automotive industry focused on the development, production, and deployment of self-driving cars, also known as driverless vehicles. These vehicles utilize advanced technologies such as AI, machine learning, and sensor fusion to operate and navigate without human intervention. This market spans various sectors, including passenger vehicles, logistics, and public transportation. Key players are advancing innovations in both hardware and software, as well as shaping regulatory frameworks. As the demand for safer and more efficient transportation solutions rises, autonomous vehicles are expected to transform traditional automotive models, redefine urban mobility, and deliver significant benefits such as reduced accidents, lower operational costs, and enhanced convenience.

The Autonomous Vehicles market is evolving at a rapid pace, driven by significant advancements in AI, machine learning, and sensor technology. As companies like Waymo, Tesla, and Aurora continue to invest in AI-powered driving systems and sensor innovations, AVs are becoming more adept at handling complex driving environments. These advancements not only improve safety and efficiency but also present significant commercial opportunities, particularly in logistics and urban transportation. For instance, autonomous freight solutions have the potential to transform long-haul trucking by reducing labor costs, while ride-hailing platforms utilizing AVs can scale more effectively, offering cost-efficient and accessible mobility services.

Recent investment activity underscores the growing momentum in the AV space. In May 2024, UK-based Wayve secured $1.05 billion in Series C funding, led by SoftBank and supported by NVIDIA and Microsoft, to accelerate the development of camera- and GPS-based autonomous systems. This funding highlights the increasing interest in making AV technology more scalable and accessible. Similarly, Nuro’s $2.1 billion Series D round supports its mission of automating last-mile delivery, partnering with major brands like Walmart and Domino’s. Aurora Innovation, a leader in autonomous trucking, raised $820 million in 2023, signaling strong confidence in the future of self-driving freight technology.

The surge in capital inflow is not limited to Western markets. Indian EV startup Euler Motors raised $24 million in Series C funding in 2024, focusing on electric three-wheelers for urban logistics. Meanwhile, U.S.-based May Mobility secured $105 million in Series D, bolstering its autonomous shuttle services that have delivered over 320,000 public rides since 2019. These developments emphasize a broadening global market for AV technology, with substantial commercial applications in logistics, ride-hailing, and last-mile delivery, making it a pivotal area for investment and technological innovation.

Key Takeaways

- Growth Analysis: Autonomous Vehicles Market Size, valued at USD 147.6 billion in 2023, is projected to grow to USD 2,398.2 billion by 2033, reflecting a robust CAGR of 33.1% from 2024 to 2033.

- By Type: Passenger Vehicles held 70% of the market share in 2023, driven by demand for ADAS and autonomous features.

- By Mobility Type: Shared Mobility led with 60% market share due to increasing urbanization and demand for flexible transport.

- By Level of Autonomy: L1 Automation dominated with 49% share, attributed to consumer preference for incremental automation.

- By Propulsion Type: Semi-Autonomous Vehicles captured 45% of the market, supported by advanced driver-assistance technologies.

- Regional Growth: North America, led by the U.S., accounted for 42.4% of the market, driven by strong investments and early adoption of AV technology. Asia Pacific is expected to see rapid growth, particularly in China and Japan.

- Driving Factors: Advancements in AI and sensor technologies are enhancing AV navigation and safety, fueling market growth in logistics and ride-hailing.

- Restraining Factors: High development costs and regulatory ambiguity, especially around liability and insurance, pose barriers to wider adoption of AV technologies.

- Global Investment Surge: Major funding rounds, like Wayve’s $1.05 billion and Nuro’s $2.1 billion, underscore growing confidence in AV technologies.

- AI and Sensor Innovation: AI, machine learning, and sensor technologies are crucial drivers for enhancing AV capabilities.

Driving factors

Technological Advancements in AI and Sensors

The rapid development of artificial intelligence (AI), machine learning (ML), and sensor technologies is a cornerstone of growth in the autonomous vehicle (AV) market. These advancements drive the ability of AVs to navigate complex environments, process vast streams of real-time data, and make precise decisions—functions critical for ensuring both safety and operational efficiency. AI and ML algorithms are integral to the continuous improvement of AV systems, enabling them to learn from real-world driving conditions and adapt to varied environments. This translates directly into enhanced vehicle performance and reliability, contributing to the overall viability of autonomous solutions for both private and commercial use.

Innovations in sensor technologies—such as LiDAR, radar, and camera systems—are equally transformative. These sensors allow AVs to accurately map their surroundings and detect obstacles, pedestrians, and other vehicles. The combined improvements in AI and sensor technologies significantly reduce the risks associated with autonomous driving, increasing consumer and regulatory confidence in these systems. Companies like Waymo and Tesla are spearheading investments in these areas, with some reports indicating that over $50 billion in venture capital has been funneled into autonomous vehicle startups globally by 2023. This surge in funding underscores the industry's commitment to developing safe, scalable AV systems that can meet both current and future demands.

Commercial Opportunities in Transportation and Logistics

The autonomous vehicle market is also poised for accelerated growth due to its transformative potential in the transportation and logistics sectors. Autonomous freight and delivery systems present a compelling opportunity to reduce labor costs and increase efficiency, particularly in long-haul trucking and last-mile delivery—two areas where driver shortages and high operational costs have long posed challenges. With AV technology, logistics companies can streamline operations, optimize routes, and minimize human error, translating to faster, more reliable service delivery and reduced fuel consumption. As an example, the autonomous trucking company TuSimple has already demonstrated fuel savings of up to 10% in long-haul operations.

Ride-hailing services are another commercial area where AV technology is expected to disrupt the status quo. Autonomous ride-hailing platforms like Waymo One and Cruise offer scalable, on-demand transportation solutions that reduce the need for human drivers, thus lowering operational costs and increasing accessibility. The cost efficiencies realized through autonomous systems—combined with consumer demand for more accessible and flexible transportation options—are likely to drive further investments in this space.

Restraining Factors

High Development Costs: A Barrier to Entry but a Catalyst for Technological Excellence

The development of autonomous vehicles (AVs) requires substantial investment in R&D, sophisticated technology, and rigorous testing. Costs associated with LiDAR, radar, cameras, and advanced AI software can range into the billions for some manufacturers, creating high entry barriers for new players. For instance, Waymo, one of the market leaders, reportedly spends upwards of $1 billion annually on autonomous technology development. This level of capital outlay is beyond the reach of many potential entrants, resulting in market consolidation around a few dominant players with the resources to advance the technology.

While this high cost can deter competition and slow market expansion, it also drives innovation. Larger manufacturers, such as Tesla, Google, and traditional automakers like General Motors and Ford, are incentivized to push the boundaries of AV technology to justify their investments. The fierce competition among these major players can lead to breakthrough innovations that improve the safety, reliability, and affordability of AV systems over time.

However, high development costs also limit consumer adoption by driving up the price of AVs, particularly in the early stages of market development. This dynamic is expected to persist until economies of scale, technological maturity, and increased competition bring costs down, broadening the market's appeal.

Liability and Insurance Issues: Regulatory Ambiguity Slowing Adoption

The complexities surrounding liability and insurance represent a significant challenge in the autonomous vehicles market. In the event of an accident involving an AV, determining whether the responsibility lies with the manufacturer, software developer, or even the passenger is a contentious issue. This ambiguity has led to a cautious approach from insurers and legal bodies, creating uncertainty that hampers consumer confidence and limits the speed of market growth.

In the U.S. alone, more than 90% of accidents are currently attributed to human error, and AVs are designed to drastically reduce this number. However, the legal framework surrounding fault in AV-related incidents remains underdeveloped. This complicates insurance models, which are traditionally based on human responsibility, and could lead to costly premiums or prolonged legal battles over fault determination. Without clear regulatory guidelines, automakers and consumers alike may hesitate to fully embrace AVs, concerned about potential liabilities.

Additionally, the high-profile nature of AV accidents—such as the fatal Uber test vehicle crash in 2018—can lead to public skepticism and regulatory delays, further slowing market expansion. Manufacturers and policymakers must work together to develop a comprehensive legal framework that addresses these concerns, promoting both innovation and consumer confidence in AV technologies.

By Type Analysis

Passenger Vehicle Segment Dominated the Market with a 70.0% Largest Share in 2023

In 2023, Passenger Vehicle held a dominant market position in the By Type segment of the Autonomous Vehicles Market, capturing more than 70.0% of the total market share. This dominance can be attributed to several factors, including heightened consumer demand for advanced driver-assistance systems (ADAS) and autonomous driving features, particularly in urban and suburban environments. The rapid adoption of these technologies by automotive manufacturers, coupled with increasing government regulations aimed at improving road safety, has accelerated the integration of autonomous features in passenger vehicles. Furthermore, the development of electric and hybrid vehicles has synergized with autonomous technologies, bolstering passenger vehicles' market presence.

On the other hand, Commercial Vehicles also demonstrated significant potential within the autonomous vehicle market, albeit with a smaller share compared to passenger vehicles. The commercial vehicle segment is witnessing increasing investments, particularly in sectors like logistics, public transportation, and delivery services, where autonomous solutions can drive efficiency and reduce operational costs. However, the commercial vehicle sector faces longer development cycles and more stringent regulatory hurdles, which has contributed to its relatively lower market share when compared to passenger vehicles in 2023.

By Mobility Type Analysis

Shared Mobility Segment Dominated the Market with a 60.0% Revenue Share in 2023

In 2023, Shared Mobility held a dominant market position in the By Mobility Type segment of the Autonomous Vehicles Market, capturing more than 60.0% of the total market share. The significant growth in shared mobility services, including ride-hailing, car-sharing, and autonomous shuttle services, has been a major driver of this trend. Increasing urbanization, growing environmental concerns, and shifting consumer preferences toward cost-efficient and flexible transportation solutions have accelerated the adoption of shared autonomous vehicles. Furthermore, the rise of smart city initiatives and advancements in fleet management technologies have contributed to the dominance of shared mobility within this segment.Conversely, the Personal Mobility segment accounted for a smaller portion of the market in 2023. While personal autonomous vehicles continue to gain traction, especially among premium consumers seeking private, autonomous transport options, the higher upfront costs and slower adoption rate of fully autonomous vehicles for individual use have limited the segment’s overall market share. Despite this, personal mobility is expected to witness steady growth as technology becomes more accessible and consumer trust in autonomous vehicles increases.

By Level of Autonomy Analysis

L1 Segment Dominated the Market with a 49.0% Largest Share in 2023

In 2023, L1 held a dominant market position in the By Level of Autonomy segment of the Autonomous Vehicles Market, capturing more than 49.0% of the total market share. L1, which includes vehicles with driver assistance systems such as adaptive cruise control and lane-keeping assistance, has seen widespread adoption due to its affordability and ease of integration into existing vehicle models. The demand for enhanced safety features, along with consumer preference for incremental automation rather than fully autonomous systems, has contributed to the L1 segment’s leadership in the market.L2 and L3 levels of autonomy, which offer higher degrees of automated driving but still require driver intervention, captured smaller market shares. These levels are gaining traction, particularly in luxury and high-performance vehicle segments, as technological advancements enable greater levels of automation. However, the higher costs and regulatory challenges have slowed their broader market penetration.

Further up the spectrum, L4 and L5—which represent fully autonomous systems—accounted for minimal market shares in 2023. Despite significant technological advancements, mass adoption of fully autonomous vehicles remains hindered by regulatory, infrastructural, and safety challenges. Nevertheless, these levels hold strong growth potential in future years as technology and regulatory frameworks evolve.

By Propulsion Type Analysis

Semi-autonomous Segment Dominated the Market with a 45.0% Revenue Share in 2023

In 2023, Semi-autonomous vehicles held a dominant market position in the By Propulsion Type segment of the Autonomous Vehicles Market, capturing more than 45.0% of the total market share. This dominance is driven by the increasing integration of advanced driver-assistance systems (ADAS) in conventional vehicles, offering features such as automated braking, lane-keeping assistance, and adaptive cruise control. Semi-autonomous vehicles provide a balance between advanced technology and affordability, allowing consumers to experience partial automation while still maintaining control of the vehicle. This has led to a strong preference for semi-autonomous vehicles, especially in regions with a high focus on safety and regulatory compliance.Fully Autonomous vehicles, while gaining attention and undergoing significant development, accounted for a smaller market share in 2023. The deployment of fully autonomous vehicles faces challenges related to regulatory approval, high development costs, and public trust in driverless technology. However, ongoing advancements and investments in AI, sensors, and infrastructure suggest strong future growth potential for fully autonomous vehicles, especially in sectors like shared mobility and logistics.

Key Market Segments

By Type

- Passenger Vehicle

- Commercial Vehicle

By Mobility Type

- Shared Mobility

- Personal Mobility

By Level of Autonomy

- L1

- L2

- L3

- L4

- L5

By Propulsion Type

- Semi-autonomous

- Fully Autonomous

Growth Opportunity

Ride-Hailing and Shared Mobility

Autonomous vehicles (AVs) present immense growth potential in the ride-hailing and shared mobility sectors, offering efficiency and cost-effectiveness by eliminating the need for human drivers. This reduction in labor costs can greatly benefit ride-hailing platforms, allowing them to operate more profitably. Furthermore, AVs can provide increased accessibility, particularly for underserved communities and individuals unable to drive, thereby expanding the user base for these services. Another critical benefit is reduced congestion—autonomous vehicles can optimize routes, minimize idle time, and drive more efficiently, which is essential for urban areas struggling with traffic congestion. As cities look for sustainable solutions, AVs in shared mobility will be a critical growth driver.

Autonomous Shuttles and Public Transportation

Autonomous shuttles and other public transportation applications offer an equally significant growth opportunity. By deploying autonomous shuttles in regions with limited public transportation, AVs can enhance accessibility, connecting underserved areas to vital services. The improved efficiency of AVs in public transport stems from their ability to optimize routes and schedules in real-time, leading to faster, more reliable services. Moreover, autonomous shuttles can contribute to reduced congestion by lowering the number of personal vehicles on the road, which complements urban sustainability goals.

Latest Trends

Enhanced Sensor Technology Driving Safety and Precision

In 2024, advancements in sensor technology are at the forefront of the global autonomous vehicles market. LiDAR systems are evolving with higher resolution and extended range capabilities, significantly improving a vehicle’s ability to perceive its surroundings, even in challenging low-light or adverse weather conditions. This is complemented by progress in camera systems, where high-resolution sensors and advanced image processing algorithms allow for more accurate object detection and recognition, enhancing overall safety. Radar systems are also becoming increasingly sophisticated, offering precise measurements of an object's distance, speed, and trajectory, which are crucial for collision avoidance and navigation in complex environments. These developments collectively enhance situational awareness, contributing to safer and more reliable autonomous driving.

Advancements in Artificial Intelligence Powering Autonomous Decision-Making

Artificial Intelligence (AI) continues to be a pivotal driver in autonomous vehicle technology in 2024. Deep learning algorithms are playing a crucial role by enabling vehicles to recognize patterns and make decisions in real time, allowing them to adapt to dynamic road conditions. This technology is essential for complex decision-making processes, such as navigating through unpredictable traffic patterns. Additionally, Natural Language Processing (NLP) is being integrated into autonomous systems, allowing vehicles to understand and respond to human commands, improving user interaction and creating a more intuitive experience. These AI advancements are critical for pushing the boundaries of vehicle autonomy and ensuring a smoother, safer ride.

Regional Analysis

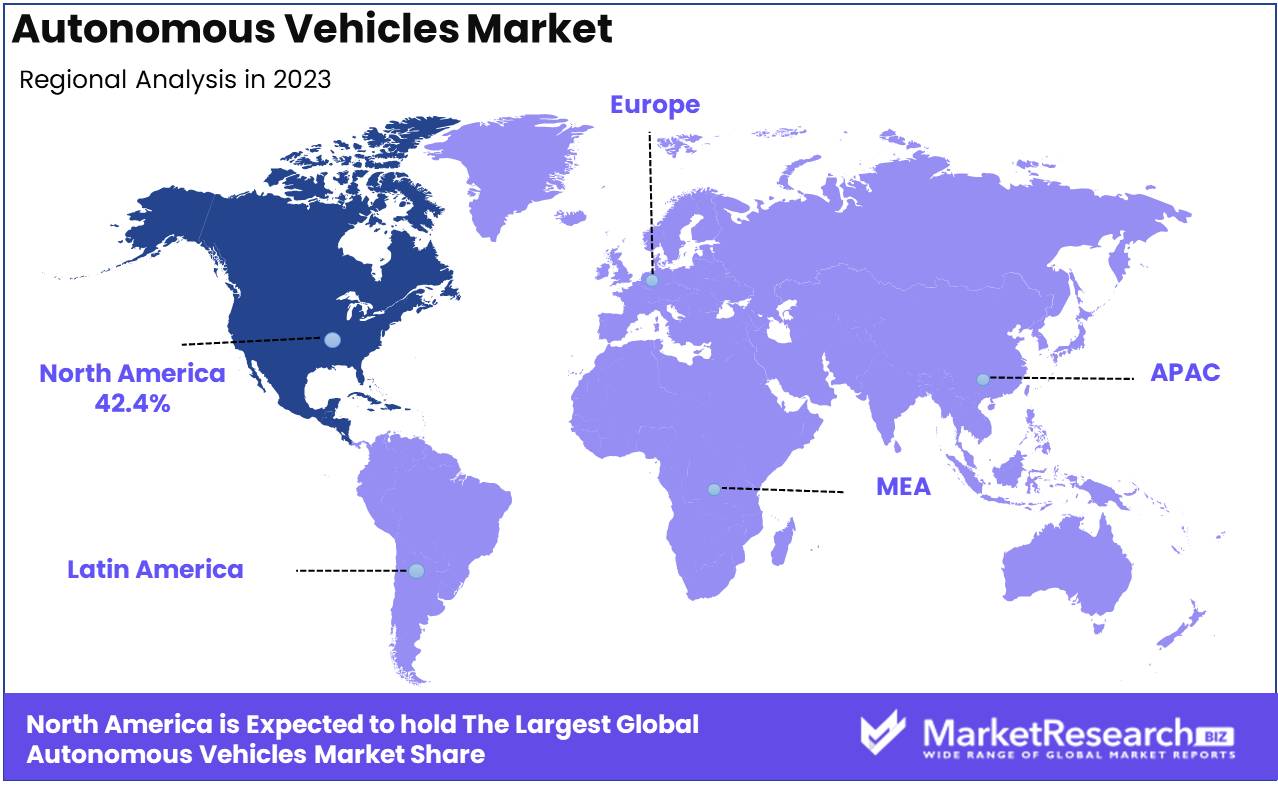

North America Leads Regional Market for Autonomous Vehicle Development, Accounting for 42.4% of Global Revenue

North America leads the regional market for autonomous vehicle development, capturing 42.4% of global revenue. The United States is a key contributor to this dominance, supported by government initiatives and significant private-sector investments in autonomous vehicle technologies. Companies like Waymo, Tesla, and GM's Cruise are at the forefront, benefiting from favorable regulations, a robust tech ecosystem, and advancements in vehicle safety. Canada also plays a critical role, focusing on integrating autonomous solutions into public transportation systems. The region’s leadership is further reinforced by high consumer awareness and adoption of advanced sensors and mobility solutions.

Europe is another influential player in autonomous vehicle development, with Germany, France, and the UK leading the charge. Germany, home to major automotive companies like BMW and Volkswagen, invests heavily in research and development for autonomous driving technologies. Similarly, the UK and France are advancing through government initiatives that promote testing on public roads and smart city infrastructure. Nations like the Netherlands and Spain are concentrating on infrastructure upgrades to support autonomous mobility.

The Asia Pacific region is poised to be the fastest-growing market for autonomous vehicles, driven by China and Japan. China’s aggressive government-backed policies aim to establish the country as a global leader in electric and autonomous vehicle development. Key players like Baidu and AutoX are making notable advancements. In Japan, automakers such as Toyota and Honda are focusing on autonomous vehicle technologies, addressing future needs like supporting an aging population.

Latin America represents an emerging market, with Mexico and Brazil leading autonomous vehicle efforts. In Mexico, the automotive manufacturing sector is increasingly embracing automation, and the government is evaluating autonomous public transportation. Brazil is showing potential despite regulatory and infrastructure challenges, driven by interest from tech and automotive companies.

The Middle East & Africa is in the nascent stage of autonomous vehicle development but holds promise, particularly in the UAE and Saudi Arabia. The UAE’s smart city initiatives position it as a future hub for autonomous mobility, with pilot projects for autonomous taxis and public transportation already underway. Saudi Arabia is investing significantly in advanced transportation technologies under its Vision 2030 initiative.

While North America currently dominates the autonomous vehicle market, Asia Pacific is expected to challenge this position as China and Japan rapidly advance their capabilities in autonomous vehicle development, particularly with innovations in vehicle safety and advanced sensors.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

The autonomous vehicles market in 2024 is defined by the rapid advancements made by several key players, each with distinct strategies and technological innovations shaping the industry's future. Tesla, Inc. remains a dominant force, leveraging its extensive electric vehicle (EV) ecosystem and advanced Full Self-Driving (FSD) capabilities, continuously improving through over-the-air updates. Cruise, backed by General Motors, is also at the forefront, particularly in deploying autonomous ride-hailing services, gaining momentum in U.S. cities.

Ford Motor Company and Nuro are emphasizing diverse applications of autonomy, with Ford focusing on logistics and commercial delivery through its partnership with Argo AI, and Nuro leading in the autonomous delivery space, especially for retail. Zoox, an Amazon subsidiary, is making headway with its purpose-built autonomous vehicle, signaling a shift toward next-generation urban mobility solutions.

European automakers such as Renault SA, Volkswagen Group, BMW, and Mercedes-Benz AG are enhancing their autonomous platforms, integrating advanced AI and sensor technologies. Toyota Motor Corporation and Hyundai Motor Group, major players from Asia, are aggressively pursuing self-driving technologies in tandem with EV development, focusing on creating scalable, mass-market autonomous solutions.

Aurora Innovation and AB Volvo stand out for their focus on commercial fleets and logistics, targeting long-haul autonomous driving and smart freight systems. Nissan continues to build on its ProPILOT system, aiming to make semi-autonomous features more accessible in consumer vehicles.

Market Key Players

- Tesla, Inc

- Cruise

- Ford Motor Company

- Nuro

- Zoox

- Renault SA

- Aurora Innovation

- Hyundai Motor Group

- Toyota Motor Corporation

- Volkswagen AG

- BMW

- Mercedes-Benz AG

- Nissan

- General Motors

- AB Volvo

Recent Developments

- In May 2024, Wayve, a UK-based autonomous vehicle startup, raised $1.05 billion in Series C funding. The round was led by SoftBank, with additional investment from NVIDIA and Microsoft. Wayve is developing self-driving technology using cameras and GPS data to make autonomous driving more accessible and affordable.

- In May 2024,Euler Motors, Indian electric vehicle startup Euler Motors raised $24 million in Series C funding. The company designs and produces electric powertrains, batteries, and charging infrastructure for electric vehicles, including three-wheelers and vans for urban logistics.

- In 2024, May Mobility, a company offering autonomous shuttle services in cities, raised $105 million in Series D funding. Since launching its services in 2019, the company has provided over 320,000 rides globally.

- In 2024, Nuro, a startup specializing in autonomous delivery vehicles, raised $2.1 billion in Series D funding. The company partners with brands like Domino's Pizza, Chipotle, Kroger, and Walmart to provide robotic delivery services.

- In July 2023, Aurora, a leader in self-driving truck technology, raised $820 million. The company, valued at $10.6 billion, has partnerships with Volvo and PACCAR, focusing on scaling autonomous trucking.

Report Scope

Report Features Description Market Value (2023) USD 147.6 Bn Forecast Revenue (2033) USD 2,398.2 Bn CAGR (2024-2032) 33.1% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type(Passenger Vehicle, Commercial Vehicle), By Mobility Type (Shared Mobility, Personal Mobility), By Level of Autonomy (L1, L2, L3, L4, L5), By Propulsion Type (Semi-autonomous, Fully Autonomous) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Tesla, Inc, Cruise, Ford Motor Company, Nuro, Zoox , Renault SA, Aurora Innovation, Hyundai Motor Group, Toyota Motor Corporation, Volkswagen Group, BMW, Mercedes-Benz AG, Nissan, General Motors, AB Volvo Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Tesla, Inc

- Cruise

- Ford Motor Company

- Nuro

- Zoox

- Renault SA

- Aurora Innovation

- Hyundai Motor Group

- Toyota Motor Corporation

- Volkswagen AG

- BMW

- Mercedes-Benz AG

- Nissan

- General Motors

- AB Volvo

Our Clients

View Our Licence Options