Artificial Intelligence Chips Market By Technology (Machine learning, Natural language processing, Context-Aware Computing, Computer Vision, Predictive Analysis), By Chip Type (GPU, ASIA, FPGA, CPU, Others), By Processing Type (Edge and Cloud), By Function (Training and Inference), By End-Users (Manufacturing, Healthcare, Automotive, Agriculture, Retail, Human Resources, Marketing, BFSI, Government, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

47870

-

June 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

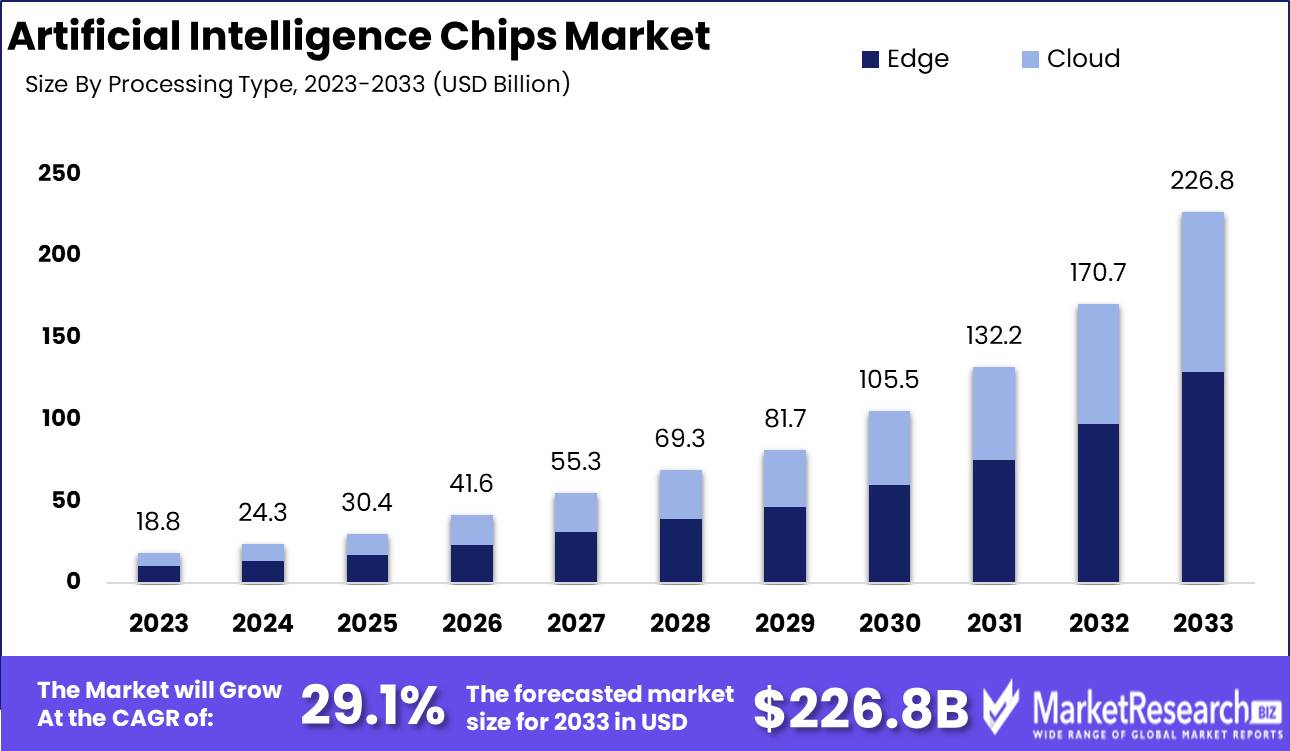

The Artificial Intelligence Chips Market was valued at USD 18.8 billion in 2023. It is expected to reach USD 226.8 billion by 2033, with a CAGR of 29.1% during the forecast period from 2024 to 2033.

The Artificial Intelligence (AI) Chips Market encompasses the development and deployment of specialized processors designed to accelerate AI workloads, such as machine learning and deep learning algorithms. These chips, including GPUs, TPUs, and custom ASICs, offer enhanced computational power and efficiency, driving advancements in AI applications across various industries. Key players invest heavily in R&D to innovate chip architectures, enhancing performance while reducing energy consumption. This market is pivotal for enabling sophisticated AI functionalities in sectors like healthcare, automotive, and finance, supporting the growing demand for intelligent systems and services, and is integral to the ongoing digital transformation across global enterprises.

The Artificial Intelligence (AI) Chips Market is poised for significant growth, driven by the increasing adoption of AI-driven smart devices and Internet of Things (IoT) technologies. This trend underscores the critical role AI chips play in enabling advanced functionalities and enhancing the performance of various applications, from autonomous vehicles to intelligent home systems. As these technologies become more integral to both consumer and industrial sectors, the demand for efficient and powerful AI chips is set to rise.

However, the market faces notable challenges, particularly for small and medium-sized enterprises (SMEs). The development and deployment of AI chips require substantial investment in R&D, specialized talent, and state-of-the-art manufacturing facilities. This high barrier to entry could limit the participation of SMEs, potentially slowing the pace of innovation and market expansion in certain segments.

Despite these challenges, continued advancements in AI chip architecture present promising opportunities. Innovations in neuromorphic computing, which mimics the neural structure of the human brain, and quantum computing, which leverages the principles of quantum mechanics, are at the forefront of this technological evolution. These cutting-edge developments are expected to drastically enhance computational capabilities and energy efficiency, propelling the AI chips market into a new era of growth. Industry leaders and startups alike are investing heavily in these technologies, anticipating their transformative impact on the market.

As a result, stakeholders must navigate a complex landscape of technological advancements, substantial investments, and competitive pressures to capitalize on the burgeoning opportunities in the AI chips market.

Key Takeaways

- Market Growth: The Artificial Intelligence Chips Market was valued at USD 18.8 billion in 2023. It is expected to reach USD 226.8 billion by 2033, with a CAGR of 29.1% during the forecast period from 2024 to 2033.

- By Technology: Machine Learning dominated Artificial Intelligence (AI) chips, driving technological innovation.

- By Chip Type: CPUs dominated the AI chips market due to versatile applications.

- By Processing Type: Edge AI Chips dominated, enhancing real-time, local processing.

- By Function: Inference Chips dominated the AI market due to widespread application.

- By End-Users: BFSI dominated AI chip use across various sectors.

- Regional Dominance: North America dominates the AI chips market with a 40% global share.

- Growth Opportunity: AI chips will see significant growth driven by edge computing, IoT applications, and advancements in autonomous vehicles and ADAS.

Driving factors

Increasing Adoption of AI Across Various Industries: A Catalyst for AI Chips Market Expansion

The rapid integration of artificial intelligence (AI) across a multitude of industries serves as a primary driver for the growth of the AI chips market. Enterprises in sectors such as healthcare, automotive, finance, and retail are increasingly implementing AI technologies to enhance efficiency, productivity, and customer experience. For instance, in healthcare, AI-driven diagnostic tools and personalized treatment plans are revolutionizing patient care. The automotive industry leverages AI for advancements in autonomous driving and smart vehicle functionalities. This surge in AI adoption necessitates the development of more sophisticated and powerful AI chips, which are essential for processing the vast amounts of data generated and for running complex algorithms efficiently.

Proliferation of Edge Computing and IoT Devices: Driving Demand for AI-Optimized Chips

The proliferation of edge computing and Internet of Things (IoT) devices is significantly boosting the demand for AI chips. Edge computing involves processing data closer to the source of generation, reducing latency, and improving real-time data analysis. IoT devices, which range from smart home appliances to industrial sensors, generate a massive amount of data that requires efficient processing. The synergy between edge computing and IoT enhances the need for AI chips that can handle data locally with minimal delay. By 2025, it is estimated that there will be over 75 billion connected IoT devices worldwide, creating a substantial market for AI chips designed for edge applications. This growth is further amplified by the demand for low-power, high-performance chips capable of supporting AI functionalities in decentralized environments.

Advancements in Semiconductor Technology: Enabling the Evolution of AI Chip Capabilities

Technological advancements in semiconductor fabrication and design are pivotal to the evolution and growth of AI chips. Innovations such as smaller node sizes, 3D stacking, and the development of specialized AI accelerators have significantly enhanced the performance and energy efficiency of AI chips. These advancements enable the production of chips that are more powerful, capable of higher throughput, and better suited for the intensive computational demands of AI applications. For example, the transition to 5nm and 3nm process nodes allows for greater transistor density, leading to improved performance and reduced power consumption. This evolution is crucial as AI applications become more complex and require higher levels of computational power. The semiconductor industry's focus on advancing AI-specific hardware, including GPUs, TPUs, and ASICs, is instrumental in meeting the growing needs of AI-driven markets.

Restraining Factors

Managing Power Consumption and Heat Dissipation: A Critical Challenge for Sustainable AI Chip Market Growth

The exponential growth in the use of artificial intelligence (AI) technologies has led to an increased demand for high-performance AI chips. However, managing power consumption and heat dissipation has emerged as a significant restraining factor. AI chips, particularly those designed for deep learning and other complex AI applications, require substantial computational power, which in turn leads to higher power consumption and heat generation. According to industry reports, high-performance AI chips can consume up to 10 times more power than traditional processors.

This increased power consumption poses several challenges. Firstly, it raises operational costs due to higher energy usage, making it less economically viable for large-scale deployment. Data centers, where AI chips are predominantly used, face substantial increases in cooling costs to manage the heat generated by these chips. Efficient thermal management systems are required to prevent overheating, which can lead to chip failure and reduced lifespan. The need for advanced cooling solutions adds to the overall cost of deploying AI chips, potentially slowing market adoption.

Furthermore, high power consumption and heat generation can limit the integration of AI chips in edge devices, such as smartphones and IoT devices, where power efficiency is crucial. The necessity to balance performance with power efficiency and thermal management creates design complexities and slows down the pace of innovation and product development. Consequently, manufacturers are compelled to invest heavily in research and development to create AI chips that are both powerful and energy-efficient, which can strain financial resources and extend time-to-market.

Data Security Concerns: A Significant Barrier to AI Chip Market Adoption

Data security concerns are increasingly becoming a pivotal issue that restrains the growth of the artificial intelligence chips market. AI applications typically involve processing large volumes of sensitive data, including personal information, financial data, and proprietary business information. As the use of AI chips in various sectors expands, so does the potential for data breaches and cyberattacks.

One of the primary concerns is the security of data during transmission and processing. AI chips often operate in environments where data is continuously transferred between devices and cloud-based platforms. This data transmission can be susceptible to interception and unauthorized access. Ensuring robust encryption and secure data handling protocols is essential but can complicate the design and functionality of AI chips, potentially affecting their performance and cost.

Moreover, the increasing deployment of AI chips in critical infrastructure, such as healthcare, finance, and national security, heightens the risk associated with data breaches. The potential for malicious exploitation of vulnerabilities in AI chip designs underscores the necessity for stringent security measures. This, in turn, requires ongoing investments in cybersecurity technologies and protocols, adding to the development costs and potentially slowing down market growth.

By Technology Analysis

In 2023, Machine Learning dominated Artificial Intelligence (AI) chips, driving technological innovation.

In 2023, Machine Learning held a dominant market position in the "By Technology" segment of the Artificial Intelligence (AI) Chips Market. This preeminence is attributable to machine learning's pervasive application across various industries, driving significant advancements in data processing and decision-making capabilities.

Natural language processing (NLP), another key segment, experienced robust growth due to its critical role in enhancing human-computer interactions, especially in customer service and virtual assistant applications. Context-aware computing, leveraging AI to provide personalized user experiences, gained traction in sectors such as retail and healthcare, where tailored services are paramount. Computer vision technology, integral to advancements in autonomous vehicles, surveillance, and industrial automation, also saw substantial adoption, underscoring its importance in interpreting and responding to visual data.

Lastly, predictive analysis, pivotal in forecasting trends and behaviors, solidified its relevance across financial services, supply chain management, and healthcare, where predictive insights are crucial for strategic planning and risk management. Collectively, these technologies underscore the multifaceted growth and integration of AI chips across diverse applications, reflecting their transformative impact on various industries.

By Chip Type Analysis

In 2023, CPUs dominated the AI chips market due to versatile applications.

In 2023, The Central Processing Unit (CPU) held a dominant market position in the Artificial Intelligence Chips Market by chip type, driven by its versatile and widespread application across various AI workloads. CPUs are integral to the computational infrastructure of AI, offering robust processing power and compatibility with a wide range of software. This dominance is primarily attributed to their ubiquity in data centers and personal computing devices, which are essential for training and inference tasks in AI applications.

Meanwhile, Graphics Processing Units (GPUs) are carving out a significant niche due to their parallel processing capabilities, which excel in deep learning and neural network tasks. The FPGA (Field-Programmable Gate Array) segment is also gaining traction, particularly in industries requiring custom, high-performance computing solutions with lower latency and power consumption.

Geographically, the Asia-Pacific region is emerging as a critical player in the AI chips market, fueled by substantial investments in AI research and development, a robust semiconductor manufacturing base, and supportive government policies.

Additionally, the "Others" category, encompassing specialized AI accelerators and neuromorphic chips, is witnessing innovation-driven growth. These emerging technologies promise to enhance AI performance through tailored architectures designed for specific AI workloads, further diversifying the competitive landscape of the AI chips market.

By Processing Type Analysis

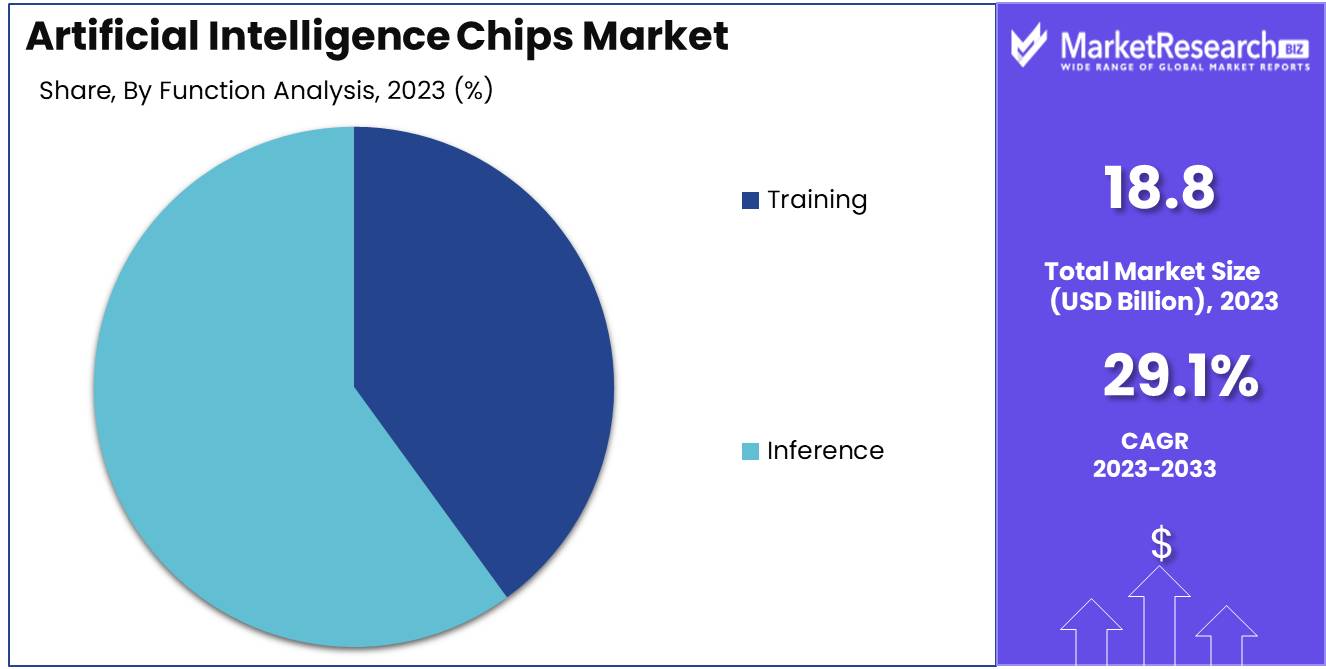

In 2023, Edge AI chips dominated, enhancing real-time, local processing.

In 2023, Edge held a dominant market position in the By Processing Type segment of the Artificial Intelligence (AI) Chips Market. Edge AI chips, designed to process data locally on devices such as smartphones, IoT gadgets, and autonomous vehicles, saw robust growth due to their ability to deliver low-latency responses and enhanced privacy. These chips alleviate the need for continuous cloud connectivity, making them highly suitable for applications requiring real-time processing and data security. The increasing proliferation of smart devices and the growing emphasis on real-time analytics have significantly bolstered the demand for Edge AI chips.

Conversely, Cloud AI chips, which are utilized in large-scale data centers, also experienced substantial growth, driven by the exponential rise in data generation and the need for high-performance computing (HPC) capabilities. Cloud AI chips excel in handling extensive datasets and complex computations, supporting advancements in fields such as natural language processing, image recognition, and predictive analytics. The scalability and robust processing power of cloud-based solutions cater to enterprises' expanding needs for big data analytics and AI-driven insights, reinforcing their crucial role in the broader AI ecosystem. Together, these segments highlight the diverse applications and growing importance of AI chips across different processing environments.

By Function Analysis

In 2023, Inference Chips dominated the AI market due to widespread application.

In 2023, The Inference segment held a dominant market position in the By Function segment of the Artificial Intelligence Chips Market. This supremacy is primarily attributed to the growing demand for real-time data processing and decision-making capabilities in various applications such as autonomous vehicles, medical diagnostics, and smart home devices. Inference chips, which are designed to deploy pre-trained AI models, have become essential for edge computing solutions where latency and power efficiency are critical. Their ability to perform complex computations on-device without relying on cloud connectivity enhances performance and security, driving their widespread adoption.

Conversely, the Training segment also plays a pivotal role in the AI Chips market, though it is characterized by its specialized usage in high-performance computing environments. Training AI models involves processing vast amounts of data to develop sophisticated algorithms, necessitating robust and powerful chips capable of handling intense computational loads. This segment sees significant investment from large tech companies and research institutions focused on advancing AI capabilities. While training chips are crucial for the development phase of AI applications, their market share remains smaller compared to inference chips, reflecting the broader application and deployment of inference-based solutions across various industries.

By End-Users Analysis

In 2023, BFSI dominated AI chip use across various sectors.

In 2023, The BFSI (Banking, Financial Services, and Insurance) sector held a dominant market position in the By End-Users segment of the Artificial Intelligence (AI) Chips Market. This dominance is attributed to several key factors. Firstly, the BFSI sector has been at the forefront of adopting AI technologies to enhance operational efficiency, security, and customer service. AI chips are integral in powering advanced analytics, fraud detection systems, and personalized banking services, which have become essential in maintaining competitive edge and regulatory compliance.

Secondly, the manufacturing sector leverages AI chips for predictive maintenance, optimizing production lines, and enhancing quality control, resulting in significant cost savings and productivity improvements. In healthcare, AI chips enable sophisticated diagnostic tools, personalized treatment plans, and efficient management of patient data, revolutionizing patient care and operational efficiencies. The automotive industry utilizes AI chips for developing autonomous vehicles, enhancing driver assistance systems, and optimizing supply chains.

In agriculture, AI chips contribute to precision farming techniques, including crop monitoring and automated harvesting, leading to increased yields and sustainability. Retailers benefit from AI chips through advanced inventory management, personalized marketing, and improved customer experiences. Human resources applications include talent acquisition, employee engagement, and workforce analytics. Marketing efforts are enhanced through AI-driven customer insights and campaign optimization. Government sectors adopt AI chips for public safety, infrastructure management, and citizen services, while various other industries utilize AI chips for bespoke applications tailored to their specific needs, showcasing the widespread impact and versatility of AI chip technology across sectors.

Key Market Segments

By Technology

- Machine learning

- Natural language processing

- Context-aware computing

- Computer vision

- Predictive analysis

By Chip Type

- GPU

- ASIA

- FPGA

- CPU

- Others

By Processing Type

- Edge

- Cloud

By Function

- Training

- Inference

By End-Users

- Manufacturing

- Healthcare

- Automotive

- Agriculture

- Retail

- Human Resources

- Marketing

- BFSI

- Government

- Others

Growth Opportunity

Expanding Edge Computing and IoT Applications

The integration of AI chips in edge computing and Internet of Things (IoT) applications presents a significant growth opportunity. The demand for real-time data processing and low-latency responses has driven the adoption of AI chips in edge devices, ranging from smart home appliances to industrial IoT solutions. These chips enable advanced data analytics directly at the source, reducing the dependency on cloud-based processing and enhancing the efficiency of IoT networks. As enterprises increasingly prioritize data security and operational efficiency, AI chip manufacturers are poised to benefit from the growing need for decentralized intelligence in edge computing environments.

Advancements in Autonomous Vehicles and ADAS

The autonomous vehicle market and Advanced Driver Assistance Systems (ADAS) are pivotal drivers for the AI chips sector. AI chips play a crucial role in processing the vast amounts of data required for real-time decision-making in autonomous vehicles. As automotive manufacturers accelerate the development of self-driving technologies, the demand for high-performance AI chips is expected to surge. Additionally, the adoption of ADAS in consumer vehicles is expanding rapidly, driven by regulatory mandates and consumer safety preferences. This trend underscores a substantial growth opportunity for AI chip providers, as they cater to the increasing computational needs of next-generation automotive systems.

Latest Trends

Continuous Advancements in Chip Architecture

The artificial intelligence (AI) chips market is set to witness significant advancements in chip architecture, driven by the relentless pursuit of performance optimization and energy efficiency. As AI applications demand increasingly complex computations, the evolution of chip designs becomes paramount. Companies are focusing on developing chips with higher transistor density, leveraging novel materials and fabrication technologies. This trend is exemplified by the integration of 3D stacking and advanced packaging techniques, which enhance processing power while minimizing footprint.

Additionally, innovations in neuromorphic computing and quantum processing units are expected to push the boundaries of traditional chip capabilities, offering unprecedented speed and efficiency in AI workloads. These architectural advancements will not only improve the performance of AI systems but also lower operational costs, making AI more accessible across various sectors.

Autonomous Vehicles and AI Integration

The integration of AI chips into autonomous vehicles is poised to be a transformative trend. As the automotive industry progresses towards higher levels of vehicle autonomy, the demand for sophisticated AI chips that can handle real-time data processing and decision-making is escalating. AI chips enable autonomous vehicles to interpret and react to their surroundings with remarkable precision, enhancing safety and operational efficiency. Key players in the market are investing heavily in developing AI chips tailored for automotive applications, emphasizing low latency, high reliability, and robust performance under diverse conditions. This integration is anticipated to accelerate the adoption of autonomous vehicles, revolutionizing transportation by reducing traffic accidents, optimizing traffic flow, and providing new mobility solutions.

The synergy between AI chip technology and autonomous vehicles will not only reshape the automotive landscape but also stimulate growth in adjacent industries such as logistics, ride-sharing, and smart city infrastructure.

Regional Analysis

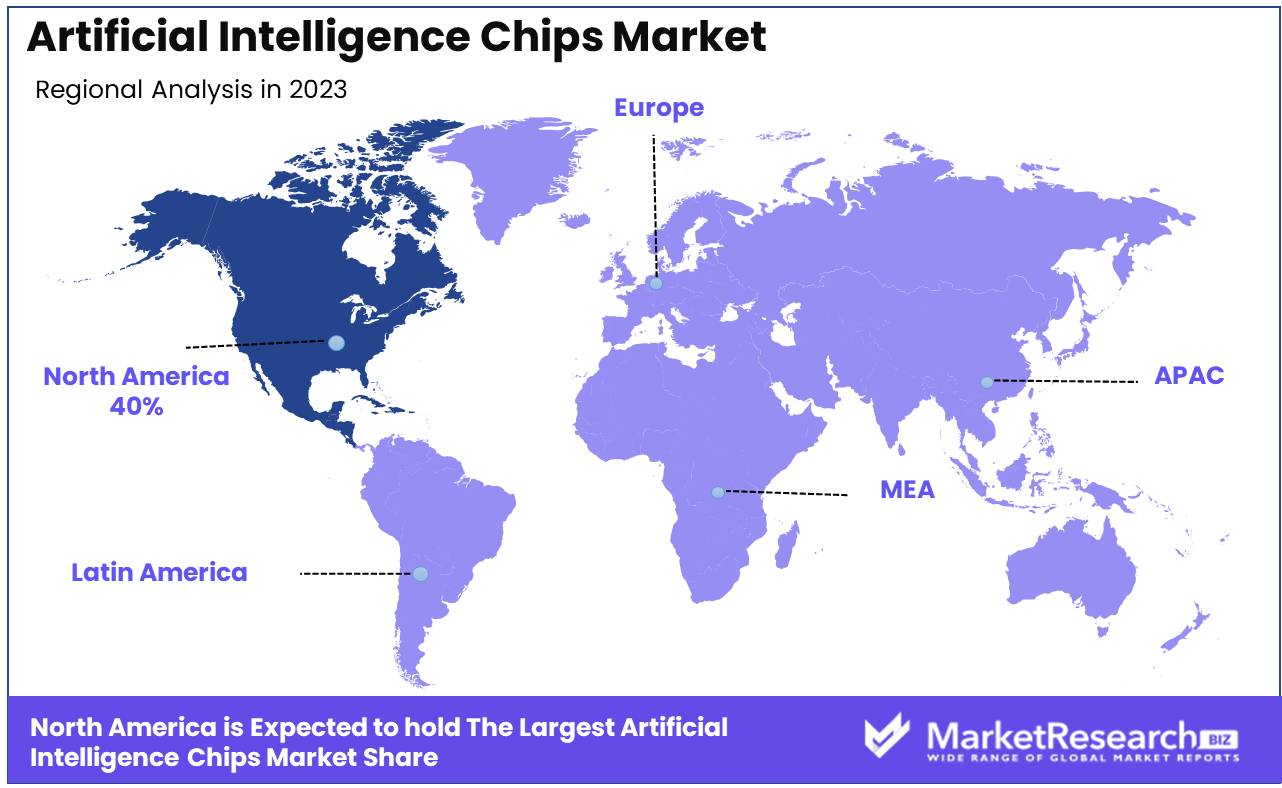

North America dominates the AI chips market with a 40% global share.

The global artificial intelligence (AI) chips market is characterized by significant regional variances, each shaped by unique economic, technological, and infrastructural factors. North America leads the market, accounting for approximately 40% of the global share, driven by robust investments in AI research and development, substantial venture capital funding, and the presence of key market players such as NVIDIA, Intel, and Google. The region's advanced technological ecosystem and high adoption rate of AI across industries like automotive, healthcare, and finance further bolster its dominance.

Europe holds a substantial share, supported by strong governmental policies promoting AI adoption and innovation. Countries like Germany, the UK, and France are at the forefront, leveraging AI in manufacturing, automotive, and healthcare sectors. The European AI market benefits from a collaborative approach between the public and private sectors, fostering an environment conducive to technological advancements.

The Asia Pacific region is experiencing rapid growth, with China, Japan, and South Korea leading the charge. China's significant investments in AI infrastructure, coupled with its strategic initiatives like the "New Generation Artificial Intelligence Development Plan," aim to make it a global AI leader. Japan and South Korea contribute through advancements in robotics and consumer electronics, enhancing regional market dynamics.

The Middle East & Africa and Latin America are emerging markets with substantial potential. In the Middle East, countries like the UAE and Saudi Arabia are investing heavily in AI as part of their economic diversification strategies. Latin America, led by Brazil and Mexico, is gradually embracing AI technologies to enhance productivity and innovation across various sectors, albeit at a slower pace compared to other regions.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Artificial Intelligence (AI) Chips market in 2024 is poised for robust growth, driven by advancements in AI applications and increased demand for high-performance computing solutions. Key players such as Intel Corporation and NVIDIA Corporation (Mellanox Technologies) continue to lead the market with their cutting-edge AI chip innovations. Intel's dominance is reinforced by its extensive R&D investments and strategic acquisitions, while NVIDIA remains a pivotal force with its powerful GPUs, essential for deep learning and AI workloads.

Qualcomm Technologies Inc. and MediaTek Inc. are leveraging their expertise in mobile technologies to develop AI chips optimized for edge computing, catering to the growing need for AI capabilities in smartphones and IoT devices. Alphabet Inc. and its subsidiaries, including Google Inc., are harnessing their vast data resources and AI research to drive forward proprietary AI chip designs, enhancing their cloud and AI services.

Samsung Electronics Co Ltd and NXP Semiconductors are expanding their AI chip portfolios to support a wide range of applications from automotive to consumer electronics, reflecting the diversification of AI applications. Advanced Micro Devices Inc. (Xilinx Inc.) and Baidu are also significant players, focusing on AI accelerators and cloud-based AI solutions.

The strategic movements of SoftBank Corp., particularly its acquisition of ARM Holdings, and Amazon Web Services' continued expansion into AI-driven cloud services, underscore the competitive dynamics of the market. Meanwhile, General Vision Inc. and Mythic are pioneering innovative AI chip technologies, aiming to carve out niche markets within the broader AI landscape.

Microsoft Corporation and Baidu are enhancing their AI capabilities, leveraging their extensive ecosystems to deliver integrated AI solutions. Collectively, these companies are driving the evolution of AI chips, setting the stage for transformative advancements across various industries.

Market Key Players

- Intel Corporation

- MediaTek Inc.

- NVIDIA Corporation (Mellanox Technologies)

- Qualcomm Technologies Inc.

- Alphabet Inc.

- NXP Semiconductors

- Mythic

- Samsung Electronics Co Ltd

- SoftBank Corp.

- Advanced Micro Devices Inc.(Xilinx Inc.)

- General Vision Inc.

- Amazon Web Services

- Google Inc.

- Microsoft Corporation

- Baidu

Recent Development

- In April 2024, AMD announced a strategic expansion of its AI chip lineup with the introduction of the Radeon Instinct M200. This new chip focuses on delivering high performance for machine learning and deep learning applications. The M200 is designed to support complex AI models, providing significant improvements in computational efficiency.

- In March 2024, Intel completed the acquisition of a promising AI chip startup, XYZ Technologies. This acquisition aims to bolster Intel's AI capabilities and expand its portfolio of AI solutions. The integration of XYZ Technologies' innovative designs is anticipated to enhance Intel's competitive edge in the AI chip market.

- In January 2024, NVIDIA announced the launch of its next-generation AI chip, the A100X. This chip is designed to significantly enhance the performance of AI workloads, offering improved energy efficiency and faster processing speeds. The A100X is expected to revolutionize data centers and AI applications across various industries.

Report Scope

Report Features Description Market Value (2023) USD 18.8 Billion Forecast Revenue (2033) USD 226.8 Billion CAGR (2024-2032) 29.1% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology (Machine learning, Natural language processing, Context-Aware Computing, Computer Vision, Predictive Analysis), By Chip Type (GPU, ASIA, FPGA, CPU, Others), By Processing Type (Edge and Cloud ), By Function (Training and Inference), By End-Users (Manufacturing, Healthcare, Automotive, Agriculture, Retail, Human Resources, Marketing, BFSI, Government, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Intel Corporation, MediaTek Inc., NVIDIA Corporation (Mellanox Technologies), Qualcomm Technologies Inc., Alphabet Inc., NXP Semiconductors, Mythic, Samsung Electronics Co Ltd, SoftBank Corp., Advanced Micro Devices Inc.(Xilinx Inc.), General Vision Inc., Amazon Web Services, Google Inc., Microsoft Corporation, Baidu Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Intel Corporation

- MediaTek Inc.

- NVIDIA Corporation (Mellanox Technologies)

- Qualcomm Technologies Inc.

- Alphabet Inc.

- NXP Semiconductors

- Mythic

- Samsung Electronics Co Ltd

- SoftBank Corp.

- Advanced Micro Devices Inc.(Xilinx Inc.)

- General Vision Inc.

- Amazon Web Services

- Google Inc.

- Microsoft Corporation

- Baidu

Our Clients

View Our Licence Options