Automotive Underbody Coatings Market Report By Type (Bitumen, Resin, Steel, Aluminum, Magnesium, Other Materials), By Material Type (Solvent-borne, Water-borne, Powder), By Application (Underbody Protection, Corrosion Protection, Noise Reduction, Heat Management, Other Applications), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

48348

-

July 2024

-

325

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

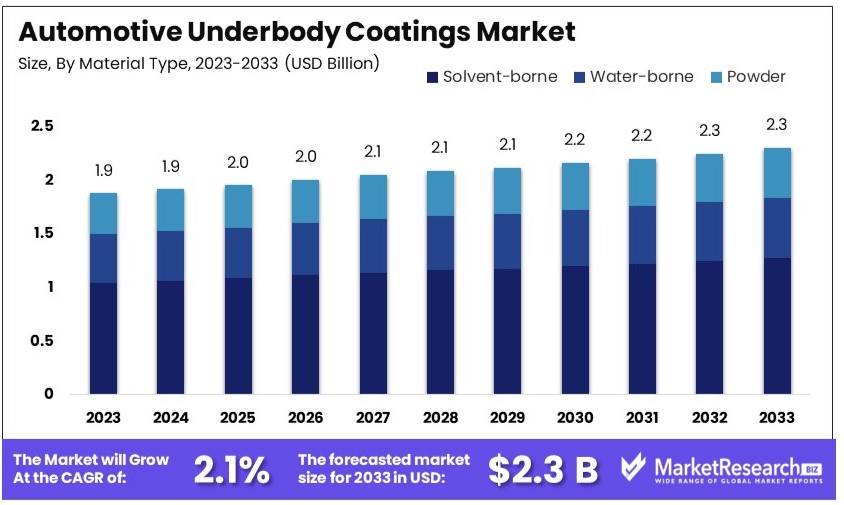

The Global Automotive Underbody Coatings Market size is expected to be worth around USD 2.3 Billion by 2033, from USD 1.9 Billion in 2023, growing at a CAGR of 2.1% during the forecast period from 2024 to 2033.

The Automotive Underbody Coatings Market deals with products used to protect the underbody parts of vehicles from corrosion, chips, and chemical abrasion. These coatings are crucial for enhancing vehicle longevity and performance. The market includes solutions like rubber-based and wax-based coatings, tailored to withstand various environmental conditions.

Driven by advancements in coating technology and increasing standards for vehicle maintenance and durability, this market serves automotive manufacturers and aftermarket services, providing essential protection solutions that meet rigorous industry standards.

The automotive underbody coatings market is experiencing significant growth, propelled by a series of strategic factors and industrial advancements. A notable driver of this market expansion is the surge in vehicle production, with a marked emphasis on electric vehicles (EVs).

These vehicles require advanced underbody coatings to ensure protection against corrosion and to extend vehicle longevity. In response to these demands, industry leaders like PPG have reported a robust increase in sales, with a 10% uptick in 2023, primarily fueled by enhanced pricing strategies and volume growth in key markets such as the U.S. and Latin America.

Investments and strategic partnerships within the private sector are further catalyzing market growth. A prime example is PPG's inauguration of a $30-million Battery Pack Application Center in Tianjin, China. This facility is dedicated to advancing coating solutions for the burgeoning EV battery market, showcasing the industry’s commitment to innovation and to meeting the rapidly evolving needs of the market.

Geographically, China continues to lead as the world’s largest vehicle producer, with production expected to reach 26.4 million units in 2024, marking a 4.2% increase year-over-year. Meanwhile, the European market is also showing signs of robust growth, with vehicle production projected to rise by 2.9% to approximately 15.1 million units in 2024. This growth is attributed to the recovery of vehicle production capacities and improvements in delivery times.

The automotive underbody coatings market is set for substantial growth, driven by increased vehicle production, innovative developments in EV technologies, and strategic global expansions. These dynamics are expected to continue driving the market forward, offering significant opportunities for stakeholders across the automotive industry.

Key Takeaways

- Market Value: The Automotive Underbody Coatings Market was valued at USD 1.9 billion in 2023 and is expected to reach USD 2.3 billion by 2033, with a CAGR of 2.1%.

- Type Analysis: Aluminum dominates with 40%, due to its lightweight properties.

- Material Type Analysis: Water-borne coatings lead with 55%, driven by environmental regulations.

- Application Analysis: Corrosion Protection dominates with 50%, essential for vehicle durability.

- Dominant Region: Asia Pacific leads with 44%, due to its automotive manufacturing base.

- Analyst Viewpoint: The market shows low saturation with steady competition, expected to grow with advancements in coating technologies.

- Growth Opportunities: Key players can capitalize on eco-friendly coatings and technological innovations to enhance market position.

Driving Factors

Increasing Demand for Vehicle Corrosion Protection Drives Market Growth

The automotive underbody coatings market is primarily driven by the need for effective corrosion protection. Underbody coatings serve as a shield against environmental elements like road salt, moisture, and debris, which are known to accelerate rusting. This need is especially pronounced in regions with severe winter conditions where road salts are commonly used.

As a result, both automobile manufacturers and owners are increasingly investing in underbody coatings to extend the longevity and maintain the value of vehicles. This growing demand significantly propels the market forward, as durable and efficient coatings become a critical requirement for vehicle maintenance and protection.

Stringent Environmental Regulations Drive Market Growth

The imposition of rigorous environmental regulations globally is a significant catalyst for the automotive underbody coatings market. These regulations demand the use of coatings that have minimal environmental impact, specifically those with low volatile organic compound (VOC) emissions.

The European Union’s End-of-Life Vehicles (ELV) Directive, for example, compels manufacturers to utilize environmentally friendly coatings. This regulatory pressure has accelerated the adoption of sustainable and compliant products, leading to innovation and expanded market opportunities in eco-friendly coatings, thereby driving market growth.

Technological Advancements Drive Market Growth

Technological innovations in the field of automotive coatings have greatly influenced the underbody coatings market. The development of coatings with superior durability, enhanced adhesion, and better corrosion resistance meets the evolving demands of the automotive industry for high-performance products.

Notably, the shift towards waterborne underbody coatings, recognized for their reduced environmental impact and superior performance characteristics compared to traditional solvent-based options, aligns with the increasing environmental concerns and regulatory standards. These advancements not only improve product offerings but also stimulate market growth by meeting both consumer preferences and regulatory requirements.

Restraining Factors

Volatility in Raw Material Prices Restrains Automotive Underbody Coatings Market Growth

Volatility in raw material prices significantly affects the automotive underbody coatings market. Key materials like resins, pigments, and additives see frequent price changes. For example, resin costs can spike with rising crude oil prices. These fluctuations increase production costs for manufacturers.

Higher costs are often passed on to consumers, making the final product more expensive. This can reduce demand for underbody coatings. Manufacturers struggle with budgeting and planning due to unpredictable material costs. The financial uncertainty can deter investment in new technologies and expansion efforts, slowing market growth.

Stringent Environmental Regulations Restrain Automotive Underbody Coatings Market Growth

Stringent environmental regulations pose challenges to the automotive underbody coatings market. Regulations like VOC emission limits and hazardous material restrictions are becoming stricter. For instance, the REACH regulation in the European Union restricts certain chemicals used in coatings.

Manufacturers must invest in developing eco-friendly alternatives to comply. This compliance can be costly and time-consuming. Failure to meet regulations can lead to penalties or market exclusion. The need to continuously adapt to changing regulations adds operational complexity. This regulatory pressure can slow innovation and production, limiting market growth.

Type Analysis

Aluminum dominates with 40% due to its lightweight properties and corrosion resistance.

In the automotive underbody coatings market, different materials such as bitumen, resin, steel, aluminum, magnesium, and other materials are used. Aluminum stands out as the leading sub-segment due to its lightweight nature and excellent corrosion resistance, which are crucial in enhancing fuel efficiency and vehicle longevity. This makes aluminum coatings particularly appealing in an industry increasingly focused on sustainability and performance.

Steel, traditionally favored for its strength and durability, remains significant but is gradually being overshadowed by aluminum billets due to weight considerations. Resin coatings are also essential, offering flexibility and protection against various environmental factors, though they are typically more prevalent in combination with other materials like aluminum for enhanced properties.

Magnesium and other innovative materials are emerging in the market, providing unique properties such as even greater weight reduction and advanced thermal management. These segments, though smaller in scale, are crucial for the development of next-generation automotive coatings.

The role of these remaining sub-segments in magnesium and innovative materials is particularly important in the growth of the market as they offer manufacturers new ways to meet stringent environmental regulations and consumer demands for higher performance and sustainability.

Material Type Analysis

Water-borne dominates with 55% due to its environmental friendliness and compliance with stringent regulations.

Material types in the automotive underbody coatings market include solvent-borne, water-borne, and powder. Water-borne coatings hold the dominant position in this segment, driven by increasing regulatory pressures worldwide to reduce volatile organic compound (VOC) emissions and their lower environmental impact. Water-borne technologies are advancing rapidly, offering comparable durability and protection as solvent-borne coatings but with a significantly reduced environmental footprint.

Solvent-borne coatings, although effective, are facing declining usage due to their higher VOC content and the stringent environmental regulations being enacted globally. However, they continue to be used in regions with less strict environmental standards or in applications where their performance advantages are indispensable.

Powder coatings are growing in popularity due to their advantages in terms of waste reduction and absence of VOC emissions. They are particularly favored in applications requiring a thick, durable finish, contributing to market growth by meeting specific performance criteria that liquid coatings might not fulfill.

The expansion of the powder segment demonstrates the industry's shift towards more sustainable and technologically advanced coating solutions, which will play a significant role in the overall market growth by offering enhanced properties such as durability and environmental sustainability.

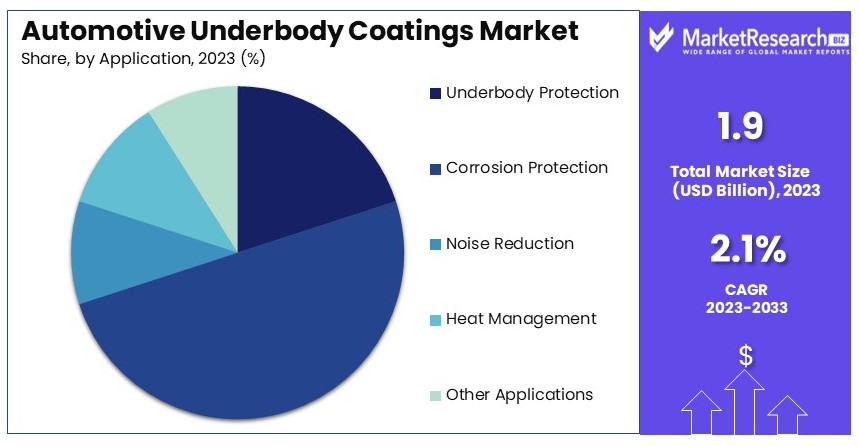

Application Analysis

Corrosion Protection dominates with 50% due to its critical role in vehicle longevity and safety.

Applications of automotive underbody coatings are categorized into underbody protection, corrosion protection, noise reduction, heat management, and other applications. Corrosion protection is the most crucial, as it directly impacts the vehicle's durability and safety. The dominance of this segment is supported by the global rise in vehicle quality standards and consumer expectations for vehicle longevity, particularly in harsh weather regions.

Underbody protection also holds a significant share, providing a barrier against physical damage from rough terrains and road debris. This application is vital for off-road and utility vehicles, emphasizing the importance of robust protective coatings.

Noise reduction coatings are increasingly being applied as consumer demand for quieter vehicle interiors grows. These coatings are applied to reduce the noise from road contact, enhancing the comfort of vehicle interiors.

Heat management coatings are vital for maintaining optimal operating temperatures and protecting sensitive vehicle components from excessive heat. This segment is becoming increasingly important with the rise of electric vehicles, which require more sophisticated thermal management solutions.

The "other applications" category includes specialized coatings designed for specific purposes such as aesthetic enhancements or additional protective features. While smaller in market size, these applications are essential for addressing niche market needs and contributing to the innovation and diversification of the underbody coatings market.

Key Market Segments

Type

- Bitumen

- Resin

- Steel

- Aluminum

- Magnesium

- Other Materials

Material Type

- Solvent-borne

- Water-borne

- Powder

Application

- Underbody Protection

- Corrosion Protection

- Noise Reduction

- Heat Management

- Other Applications

Growth Opportunities

Development of Multi-functional Coatings Offers Growth Opportunity

The trend towards multi-functional underbody coatings offers significant growth opportunities. These advanced coatings provide additional benefits such as sound dampening, vibration control, and thermal insulation, beyond just corrosion protection.

For example, sound-dampening properties can improve the driving experience by reducing road noise inside the vehicle cabin. By integrating these multiple functions, manufacturers can offer enhanced products that meet diverse consumer needs. Investing in the development of such multi-functional coatings can help companies stand out in the competitive automotive market and drive growth.

Adoption of Sustainable and Bio-based Coatings Offers Growth Opportunity

The push for sustainability in the automotive industry opens growth opportunities for bio-based and sustainable underbody coatings. These coatings, derived from renewable sources like plant-based materials, provide an eco-friendly alternative to traditional coatings.

With increasing environmental concerns and stricter regulations, the demand for sustainable solutions is rising. Manufacturers investing in research and development of these eco-friendly coatings can tap into a growing market segment. By offering products that align with sustainability goals, companies can attract environmentally conscious consumers and expand their market share.

Trending Factors

Waterborne Underbody Coatings Are Trending Factors

Waterborne underbody coatings are becoming increasingly popular due to their low VOC emissions and eco-friendly nature. These coatings use water as the primary solvent, making them more environmentally sustainable compared to traditional solvent-based coatings.

As environmental regulations tighten, the demand for waterborne coatings is expected to rise. This trend highlights the industry's shift towards greener practices. By adopting waterborne coatings, manufacturers can meet regulatory requirements and cater to the growing consumer preference for sustainable products.

Automated Application Processes Are Trending Factors

The adoption of automated application processes for underbody coatings is a key trend in the automotive industry. Automated methods, such as robotic spraying, enhance efficiency, consistency, and cost-effectiveness.

These processes ensure uniform coverage and minimize material waste, which is particularly important in high-volume production facilities. By implementing automated application systems, manufacturers can improve production quality and reduce operational costs. This trend underscores the industry's focus on innovation and efficiency, driving overall market growth and competitiveness.

Regional Analysis

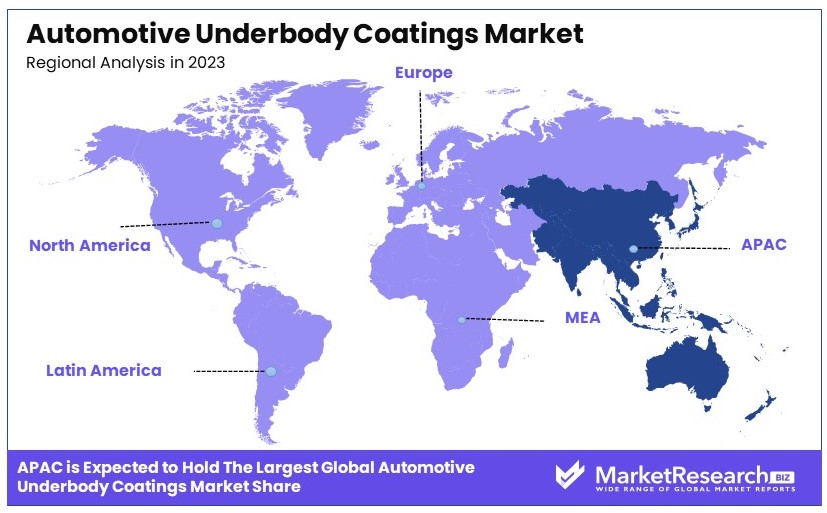

Asia Pacific Dominates with 44% Market Share in the Automotive Underbody Coatings Market

Asia Pacific's 44% share of the global automotive underbody coatings market is significantly influenced by its large automotive manufacturing base. Major automotive production countries like China, Japan, and South Korea contribute extensively to this dominance. The region's capacity for high-volume manufacturing, combined with lower production costs and abundant availability of raw materials, supports its leading position. Additionally, growing consumer demand for durable and high-quality vehicles in these populous nations further drives the market.

The automotive underbody coatings market in Asia Pacific is bolstered by rapid industrialization and increasing investments in automotive technologies. The region's emphasis on exporting automobiles to international markets also plays a crucial role. Furthermore, stringent regulations regarding vehicle safety and emissions standards in Asia Pacific countries push for advancements in coating technologies, enhancing overall market growth.

Regional Market Shares and Dynamics:

North America: North America accounts for about 25% of the market, driven by technological advancements and stringent regulations on vehicle protection and emissions. The presence of major automotive manufacturers and a focus on innovation in protective coatings support steady growth in this region.

Europe: Europe holds approximately 20% of the market share, with a strong emphasis on environmental sustainability influencing coating technologies. High standards for vehicle manufacturing and maintenance, along with a focus on luxury and performance vehicles, sustain its market position.

Middle East & Africa: This region captures around 6% of the market. Despite being smaller, there is potential growth due to increasing vehicle sales and industrial investments in countries like Saudi Arabia and the UAE.

Latin America: Latin America maintains about 5% of the market share. Growth is influenced by rising automotive production in countries like Brazil and Argentina and a growing demand for vehicle longevity and maintenance.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Automotive Underbody Coatings Market is shaped by several influential companies. BASF SE and PPG Industries, Inc. are leaders with their extensive product lines and innovative solutions. Their strong R&D capabilities and global presence give them a strategic advantage.

Axalta Coating Systems Ltd. and Akzo Nobel N.V. are notable for their advanced coating technologies and sustainable practices. They focus on providing high-performance coatings that meet environmental regulations.

Henkel AG & Co. KGaA and The Sherwin-Williams Company have a significant market influence due to their comprehensive product offerings and strong customer relationships. Their strategies include continuous innovation and expanding their market reach.

3M Company and Dow Inc. are known for their technological advancements and high-quality products. They leverage their expertise in materials science to offer durable and effective coatings.

Covestro AG and RPM International Inc. excel in specialty coatings, focusing on customized solutions for specific automotive needs. Their strategic positioning includes partnerships and collaborations to enhance their market presence.

Kansai Paint Co., Ltd. and Nippon Paint Holdings Co., Ltd. are significant players in the Asian market, leveraging their regional strengths and expanding globally. Sika AG and LORD Corporation focus on innovative bonding solutions and protective coatings, enhancing vehicle durability.

Wacker Chemie AG is noted for its silicone-based coatings, providing unique benefits in the market. The market features a blend of global leaders and specialized firms, each contributing to the market’s growth through innovation, sustainability, and strategic partnerships.

Market Key Players

- BASF SE

- PPG Industries, Inc.

- Axalta Coating Systems Ltd.

- Akzo Nobel N.V.

- Henkel AG & Co. KGaA

- The Sherwin-Williams Company

- 3M Company

- Dow Inc.

- Covestro AG

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Sika AG

- LORD Corporation

- Wacker Chemie AG

Recent Developments

- 2024: BASF has been actively involved in developing lightweight composite materials for automotive applications. Their new composite engine mounts and cross members offer a 50% weight reduction compared to traditional aluminum parts, enhancing vehicle efficiency and reducing front axle load.

- 2024: PPG Industries introduced a range of Corashield underbody coatings designed for exceptional protection against stones, road debris, and other elements. These coatings are formulated to provide long-term protection from corrosion and rust, tailored to meet the specific needs of various OEM production environments.

Report Scope

Report Features Description Market Value (2023) USD 1.9 Billion Forecast Revenue (2033) USD 2.3 Billion CAGR (2024-2033) 2.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Bitumen, Resin, Steel, Aluminum, Magnesium, Other Materials), By Material Type (Solvent-borne, Water-borne, Powder), By Application (Underbody Protection, Corrosion Protection, Noise Reduction, Heat Management, Other Applications) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape BASF SE, PPG Industries, Inc., Axalta Coating Systems Ltd., Akzo Nobel N.V., Henkel AG & Co. KGaA, The Sherwin-Williams Company, 3M Company, Dow Inc., Covestro AG, RPM International Inc., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Sika AG, LORD Corporation, Wacker Chemie AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- BASF SE

- PPG Industries, Inc.

- Axalta Coating Systems Ltd.

- Akzo Nobel N.V.

- Henkel AG & Co. KGaA

- The Sherwin-Williams Company

- 3M Company

- Dow Inc.

- Covestro AG

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Sika AG

- LORD Corporation

- Wacker Chemie AG

Our Clients

View Our Licence Options