Anastomosis Device Market By Product Type (Disposable Anastomosis Devices, Reusable Anastomosis Devices), By Application (Cardiovascular Surgery, Gastrointestinal Surgery, Others), By End-User (Hospitals, Ambulatory Care Centers), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

48969

-

July 2023

-

343

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

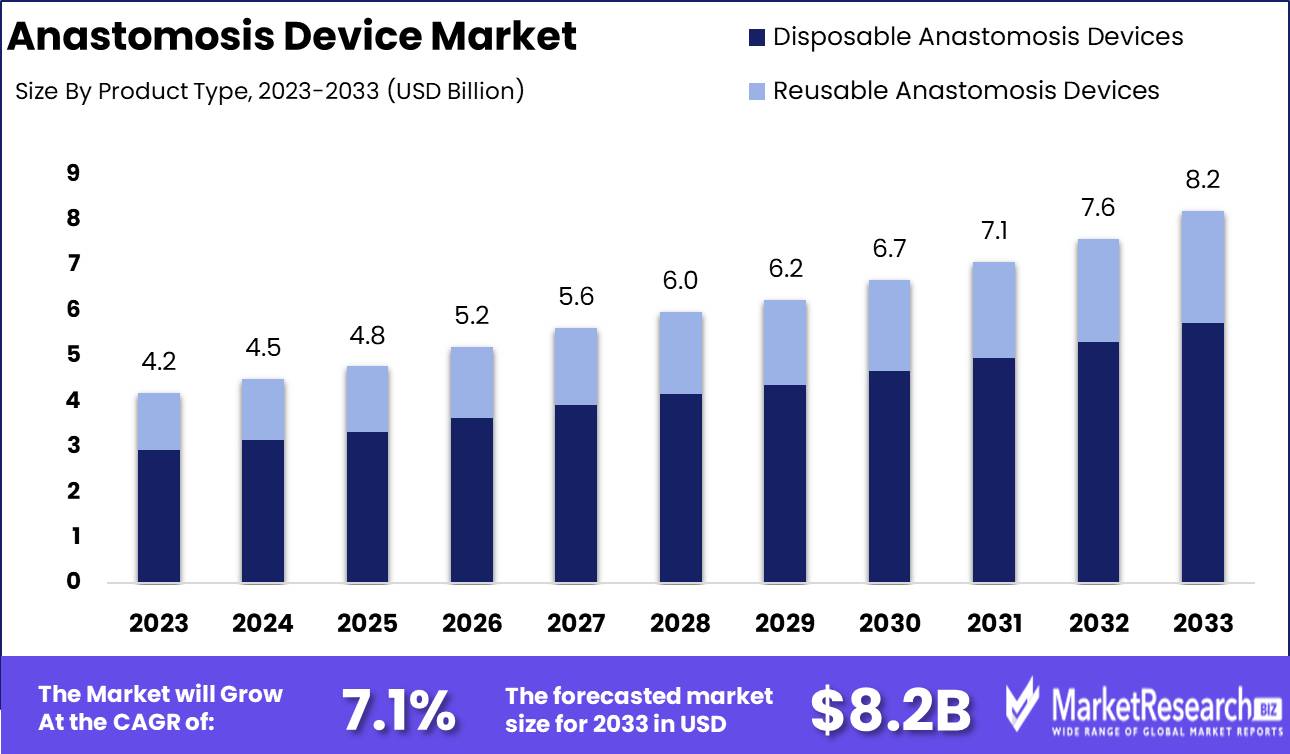

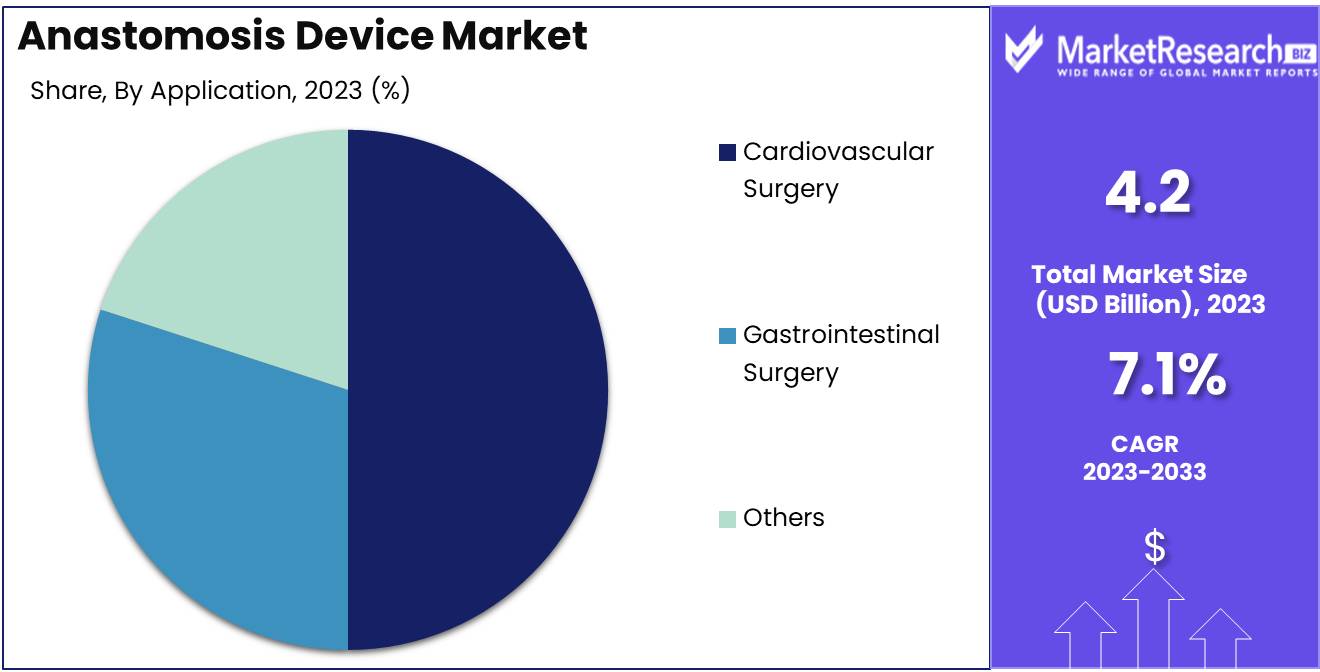

The Global Anastomosis Device Market was valued at USD 4.2 Bn in 2023. It is expected to reach USD 8.2 Bn by 2033, with a CAGR of 7.1% during the forecast period from 2024 to 2033.

The Anastomosis Device Market encompasses the development, production, and application of specialized medical devices used to connect blood vessels, intestines, or other tubular structures during surgical procedures. These devices, which include staplers, sealants, and sutures, enhance surgical outcomes by ensuring precise and reliable connections, reducing the risk of leaks and complications. Market growth is driven by the increasing prevalence of cardiovascular and gastrointestinal surgeries, technological advancements in minimally invasive procedures, and the rising demand for enhanced patient outcomes. Key players are focusing on innovative designs and materials to improve device performance and patient safety in this critical area of medical care.

The Anastomosis Device Market is experiencing significant growth, driven by the increasing demand for advanced surgical techniques and improved patient outcomes. Key factors propelling this market include the rising prevalence of cardiovascular and gastrointestinal diseases, which necessitate surgical interventions, and advancements in minimally invasive procedures. Notably, devices such as the Enclose® II have demonstrated excellent graft patency rates, averaging 96.4% at one year post-surgery across 222 proximal anastomoses in 178 patients. This device also boasts a strong safety profile, with no reported cases of aortic injury or surgical complications related to plaque microemboli.

The Anastomosis Device Market is experiencing significant growth, driven by the increasing demand for advanced surgical techniques and improved patient outcomes. Key factors propelling this market include the rising prevalence of cardiovascular and gastrointestinal diseases, which necessitate surgical interventions, and advancements in minimally invasive procedures. Notably, devices such as the Enclose® II have demonstrated excellent graft patency rates, averaging 96.4% at one year post-surgery across 222 proximal anastomoses in 178 patients. This device also boasts a strong safety profile, with no reported cases of aortic injury or surgical complications related to plaque microemboli.The market is also addressing the challenge of anastomotic leaks, a potential complication occurring in approximately 5% of cases, particularly in intestinal surgeries. This underscores the need for reliable and precise anastomosis devices that can minimize such risks. Innovations in device design and materials are enhancing the performance and safety of these devices, ensuring more successful surgical outcomes and reducing postoperative complications.

Strategically, leading companies in the anastomosis device market are focusing on research and development to introduce cutting-edge technologies that cater to the growing demands of the healthcare sector. Collaborations and partnerships are also pivotal in expanding market reach and improving product offerings. As regulatory approvals become more stringent, companies are prioritizing compliance and quality assurance to maintain a competitive edge.

Key Takeaways

- Market Value: The Global Anastomosis Device Market was valued at USD 4.2 Bn in 2023. It is expected to reach USD 8.2 Bn by 2033, with a CAGR of 7.1% during the forecast period from 2024 to 2033.

- By Product Type: Disposable Anastomosis Devices overwhelmingly lead the market, holding a commanding 70% share, reflecting their preference for ensuring sterility and reducing cross-contamination risks.

- By Application: Cardiovascular Surgery is the primary application, accounting for 50% of the market, due to the critical nature of these procedures and the need for reliable devices.

- By End-User: Hospitals are the predominant end-users, representing an extensive 75% of the market, highlighting their central role in performing complex surgical procedures.

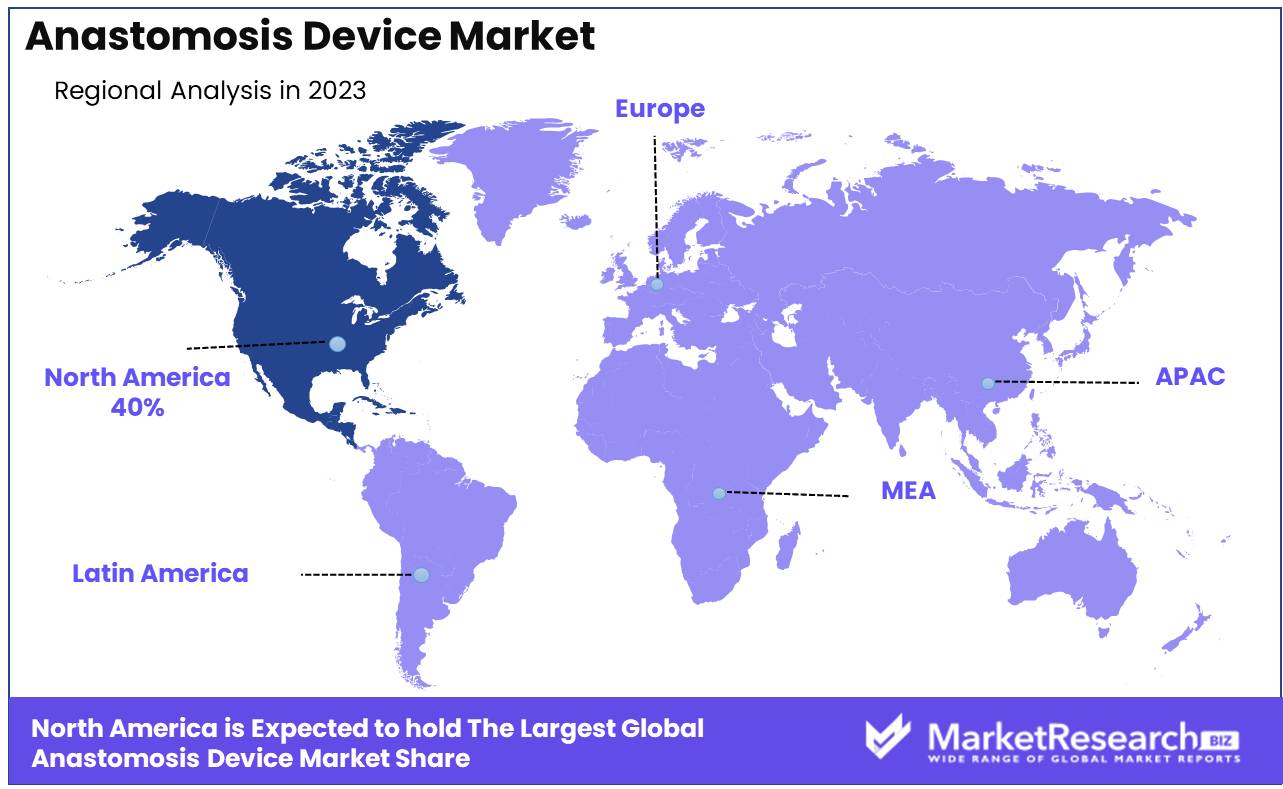

- Regional Dominance: North America dominates the market with a 40% share, driven by advanced healthcare infrastructure and a high volume of cardiovascular surgeries.

Driving factors

Growing Prevalence of Chronic Diseases

The rising prevalence of chronic diseases is a significant driver of the anastomosis device market. Conditions such as cardiovascular diseases, gastrointestinal disorders, and cancer often necessitate surgical interventions that require the use of anastomosis devices. For instance, cardiovascular diseases, which remain the leading cause of death globally, frequently require procedures such as coronary artery bypass grafting (CABG), where anastomosis devices play a crucial role.

The increasing incidence of these chronic diseases directly correlates with a higher demand for surgical procedures, thus driving the growth of the anastomosis device market. The World Health Organization (WHO) estimates that chronic diseases will account for nearly 73% of all deaths by 2025, highlighting the expanding market need for these devices.

Increasing Number of Surgical Procedures

The growing number of surgical procedures globally is another key factor fueling the anastomosis device market. Advances in medical technology and improved access to healthcare have led to an increase in surgical interventions. According to the Global Surgery report, approximately 313 million surgical procedures are performed each year worldwide. This rise is driven by the increasing aging population, which is more prone to chronic conditions requiring surgical treatment.

The demand for efficient and reliable anastomosis devices is therefore rising, as they are essential for ensuring successful outcomes in surgeries involving tissue connection. This trend is expected to continue, further propelling the market growth.

Technological Advancements in Surgical Devices

Technological advancements in surgical devices have significantly impacted the anastomosis device market. Innovations such as minimally invasive surgical techniques, robotic-assisted surgeries, and enhanced anastomosis device designs have improved surgical outcomes and reduced recovery times. The development of bioabsorbable anastomosis devices, which dissolve in the body after serving their purpose, reduces the need for additional surgical interventions.

These technological improvements make surgical procedures safer and more effective, increasing the adoption of anastomosis devices. The continuous evolution of surgical technology, including improved precision and reduced complication rates, is expected to drive the market growth substantially.

Restraining Factors

High Cost of Anastomosis Devices

The high cost of anastomosis devices presents a significant challenge to the market's growth. These devices are often expensive due to the advanced materials and technologies used in their manufacture. The high price can be prohibitive for many healthcare facilities, particularly in low- and middle-income countries, where budget constraints are more pronounced. The cost can be a barrier for patients, especially those without comprehensive insurance coverage.

This financial barrier limits the widespread adoption of these devices, slowing market expansion. To mitigate this issue, manufacturers need to explore cost-reduction strategies, such as optimizing production processes and increasing competition through market entry of new players.

Stringent Regulatory Requirements

Stringent regulatory requirements also pose a significant hurdle for the anastomosis device market. These devices must undergo rigorous testing and approval processes to ensure they meet safety and efficacy standards set by regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Compliance with these regulations involves substantial time and financial investment, potentially delaying the introduction of new products to the market.

Differing regulatory standards across regions can complicate the global distribution of these devices. Manufacturers must navigate these complex regulatory landscapes, which can be resource-intensive and slow market entry and growth.

By Product Type Analysis

Disposable Anastomosis Devices dominated the By Product Type segment of the Anastomosis Device Market in 2023, capturing more than a 70% share.

In 2023, Disposable Anastomosis Devices held a dominant market position in the By Product Type segment of the Anastomosis Device Market, capturing more than a 70% share. This significant market share is driven by the advantages of single-use devices, including reduced risk of cross-contamination, no need for sterilization, and enhanced convenience for healthcare providers. The increasing emphasis on infection control and patient safety in surgical procedures further supports the preference for disposable devices.

Reusable Anastomosis Devices offer the benefits of cost savings over multiple uses and are designed for durability and repeated sterilization. However, the need for rigorous cleaning and sterilization processes to prevent infection risks can be resource-intensive. Despite their initial higher cost-effectiveness, the market share of reusable devices is limited by these additional operational challenges and the growing preference for the convenience and safety provided by disposable options.

By Application Analysis

Cardiovascular Surgery dominated the By Application segment of the Anastomosis Device Market in 2023, capturing more than a 50% share.

In 2023, Cardiovascular Surgery held a dominant market position in the By Application segment of the Anastomosis Device Market, capturing more than a 50% share. This leadership is driven by the high prevalence of cardiovascular diseases and the increasing number of coronary artery bypass graft (CABG) surgeries and other cardiovascular procedures requiring precise and reliable anastomosis. The critical nature of cardiovascular surgeries necessitates the use of advanced anastomosis devices to ensure successful outcomes and reduce complications.

Gastrointestinal Surgery also represents a significant segment within the anastomosis device market. Procedures such as colorectal surgeries, gastric bypass, and other digestive tract surgeries frequently require anastomosis devices to reconnect tissues. Although the market share of gastrointestinal surgery is substantial, it remains smaller compared to cardiovascular surgery due to the relatively lower volume of procedures and different clinical demands.

Others encompass various surgical fields, including urology devices, neurology, and gynecology, where anastomosis devices are utilized. These areas, while important, contribute less to the overall market share compared to cardiovascular and gastrointestinal surgeries due to their specific and varied application requirements.

By End-User Analysis

Hospitals dominated the By End-User segment of the Anastomosis Device Market in 2023, capturing more than a 75% share.

In 2023, Hospitals held a dominant market position in the By End-User segment of the Anastomosis Device Market, capturing more than a 75% share. This significant market share is attributed to the high volume of complex surgical procedures performed in hospital settings, where anastomosis devices are critical for surgeries such as cardiovascular, gastrointestinal, and other major operations. Hospitals' access to advanced surgical technologies, skilled healthcare professionals, and comprehensive patient care facilities supports their leading role in the adoption and utilization of anastomosis devices.

Ambulatory Care Centers also play a vital role in the anastomosis device market, particularly for outpatient surgeries and less complex procedures. These centers offer convenience, reduced hospital stays, and lower costs, making them an attractive option for certain surgical interventions. However, the scope of procedures performed in ambulatory care centers is generally narrower compared to hospitals, limiting their market share.

Key Market Segments

By Product Type

- Disposable Anastomosis Devices

- Reusable Anastomosis Devices

By Application

- Cardiovascular Surgery

- Gastrointestinal Surgery

- Others

By End-User

- Hospitals

- Ambulatory Care Centers

Growth Opportunity

Expansion in Emerging Markets

The global anastomosis device market in 2024 presents substantial opportunities for expansion in emerging markets. Regions such as Asia-Pacific, Latin America, and parts of Africa are witnessing significant improvements in healthcare infrastructure and rising investments in medical technology. These areas have large populations with increasing incidences of chronic diseases and a growing demand for advanced surgical procedures. By entering these markets, companies can tap into a vast and underserved customer base.

Strategic initiatives such as forming partnerships with local healthcare providers, offering competitive pricing, and investing in education and training programs can facilitate market entry and growth. This expansion is expected to drive substantial revenue growth and increase market share for anastomosis device manufacturers.

Development of Minimally Invasive Anastomosis Devices

Innovation in the development of minimally invasive anastomosis devices represents another critical opportunity for market growth in 2024. Minimally invasive surgical techniques offer numerous advantages, including reduced recovery times, lower risk of complications, and shorter hospital stays. These benefits are driving the adoption of minimally invasive procedures across the globe. Anastomosis devices designed for these techniques, such as endoscopic and laparoscopic anastomosis devices, are becoming increasingly popular.

Companies that focus on developing and refining these advanced devices can meet the evolving needs of modern surgical practices, attracting a broader customer base. Additionally, these innovative products can command premium pricing, thereby increasing profitability. The continuous development of minimally invasive anastomosis devices will drive market differentiation and provide a competitive edge.

Latest Trends

Adoption of Robotic-Assisted Surgeries

One of the most significant trends in the anastomosis device market for 2024 is the increasing adoption of robotic-assisted surgeries. Healthcare service robots or Robotic-assisted surgical systems provide greater precision, flexibility, and control than traditional surgical methods. These systems enable surgeons to perform complex procedures with enhanced accuracy and minimal invasiveness. The growing utilization of robotic-assisted surgeries is driving demand for specialized anastomosis devices that are compatible with these advanced systems.

This trend is expected to enhance surgical outcomes, reduce recovery times, and minimize complications, thereby increasing the appeal and adoption of anastomosis devices designed for robotic-assisted applications. As hospitals and surgical centers continue to invest in robotic technologies, the market for compatible anastomosis devices is poised for substantial growth.

Advances in Biocompatible Materials for Devices

Advances in biocompatible materials represent another critical trend shaping the anastomosis device market in 2024. The development of new materials that are more compatible with human tissues and less likely to cause adverse reactions is improving the safety and efficacy of anastomosis devices. Innovations in biocompatible materials, such as biodegradable polymers and bioactive coatings, enhance the integration of devices with the body and reduce the risk of post-surgical complications.

These materials can also promote healing and reduce the need for additional surgeries. Companies that focus on incorporating these advanced materials into their anastomosis devices will be better positioned to meet the stringent safety standards and clinical demands, driving market growth and differentiation.

Regional Analysis

The Anastomosis Device Market is dominated by North America, which holds a significant 40% share of the global market.

The Anastomosis Device Market demonstrates varied regional dynamics and growth drivers. In North America, which leads the market with a substantial 40% share, the growth is primarily driven by advanced healthcare infrastructure, high adoption rates of innovative surgical technologies, and a large number of surgical procedures performed annually. The United States, in particular, is a key contributor due to its well-established healthcare system and significant investments in medical research and development.

In Europe, the market is propelled by the increasing prevalence of chronic diseases requiring surgical intervention and the strong presence of key market players. Countries such as Germany, France, and the UK are leading markets within the region, supported by robust healthcare systems and a growing focus on minimally invasive surgical procedures.

The Asia Pacific region is experiencing rapid growth in the anastomosis device market, driven by increasing healthcare expenditure, improving healthcare infrastructure, and rising awareness about advanced surgical techniques. Major contributors include China, Japan, and India, where the expanding medical tourism industry and growing patient population necessitate the adoption of smart medical devices.

In the Middle East & Africa, the market is growing steadily, supported by investments in healthcare infrastructure and an increasing number of surgical procedures. The market in this region is particularly strong in countries like Saudi Arabia, the UAE, and South Africa, where there is a focus on enhancing healthcare services and adopting modern medical technologies.

Latin America also shows promising growth in the anastomosis device market, driven by improving healthcare systems and rising demand for advanced surgical solutions. Brazil and Mexico are key markets within this region, exhibiting significant potential due to increasing healthcare investments and a growing patient base.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The global anastomosis device market is projected to witness significant growth in 2024, fueled by advancements in minimally invasive surgical techniques and the rising prevalence of chronic diseases requiring surgical interventions. Key players in this market are poised to capitalize on these trends through innovation, strategic collaborations, and robust distribution networks.

Becton, Dickinson and Company stands out with its comprehensive portfolio of medical devices and strong R&D capabilities. Their continuous innovation in anastomosis technologies ensures they remain a dominant force, catering to a broad range of surgical needs.

Intuitive Surgical Inc., renowned for its pioneering da Vinci robotic surgical system, leverages its expertise in robotic-assisted surgery to enhance the precision and efficacy of anastomosis procedures. Their technological advancements provide significant competitive advantages in the market.

CONMED Corporation and Johnson & Johnson are key players with extensive experience in surgical devices. Johnson & Johnson, through its Ethicon division, offers advanced stapling technologies that improve surgical outcomes, while CONMED’s focus on minimally invasive solutions positions it well to meet the growing demand for less invasive surgical options.

Smith & Nephew Plc and B. Braun Melsungen bring a wealth of experience in wound management and surgical instruments. Their innovations in anastomosis devices emphasize patient safety and recovery, aligning with the market's move towards enhanced patient care.

Advanced Medical Solutions Group Plc and Teleflex contribute with specialized solutions that address specific surgical challenges. Their focus on niche areas within anastomosis technology allows them to cater to unique surgical requirements effectively.

Artivion, Inc. and Surgical Specialties Corporation are noted for their commitment to quality and precision in surgical devices. Their products support complex surgical procedures, providing reliability and effectiveness critical to successful anastomosis.

Baxter International, Inc. offers a diverse range of healthcare products, including innovative anastomosis devices. Their global presence and strong market reach enable them to serve a wide customer base, ensuring accessibility to cutting-edge surgical solutions.

Market Key Players

- Becton, Dickinson and Company

- Intuitive Surgical Inc.

- CONMED Corporation

- Johnson & Johnson

- Smith & Nephew Plc

- B. Braun Melsungen

- Advanced Medical Solutions Group Plc

- Teleflex

- Artivion, Inc.

- Surgical Specialties Corporation

- Baxter International, Inc.

Recent Development

- In March 2024, MedTech Innovations introduced bioabsorbable anastomosis devices to reduce post-surgical complications and improve recovery times.

- In January 2024, BioSuture Inc.developed an advanced suture-based anastomosis device with enhanced knot security for cardiovascular procedures.

Report Scope

Report Features Description Market Value (2023) USD 4.2 Bn Forecast Revenue (2033) USD 8.2 Bn CAGR (2024-2033) 7.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Disposable Anastomosis Devices, Reusable Anastomosis Devices), By Application (Cardiovascular Surgery, Gastrointestinal Surgery, Others), By End-User (Hospitals, Ambulatory Care Centers) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Becton, Dickinson and Company, Intuitive Surgical Inc., CONMED Corporation, Johnson & Johnson, Smith & Nephew Plc, B. Braun Melsungen, Advanced Medical Solutions Group Plc, Teleflex, Artivion, Inc., Surgical Specialties Corporation, Baxter International, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Becton, Dickinson and Company

- Intuitive Surgical Inc.

- CONMED Corporation

- Johnson & Johnson

- Smith & Nephew Plc

- B. Braun Melsungen

- Advanced Medical Solutions Group Plc

- Teleflex

- Artivion, Inc.

- Surgical Specialties Corporation

- Baxter International, Inc.

Our Clients

View Our Licence Options