Healthcare Service Robots Market By Offering (Orthopedic Surgery, Cardiology, Neurosurgery), By Deployment (Laparoscopy, Pharmacy Applications, Orthopedic Surgery, and Other), By Application (Disinfection Robots, e-Assistance, Medical TRobotic Nurselepresence Robots, Delivery Robots, Dispensing Robots, Others), By End-Users (Hospitals, Rehabilit and Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48457

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

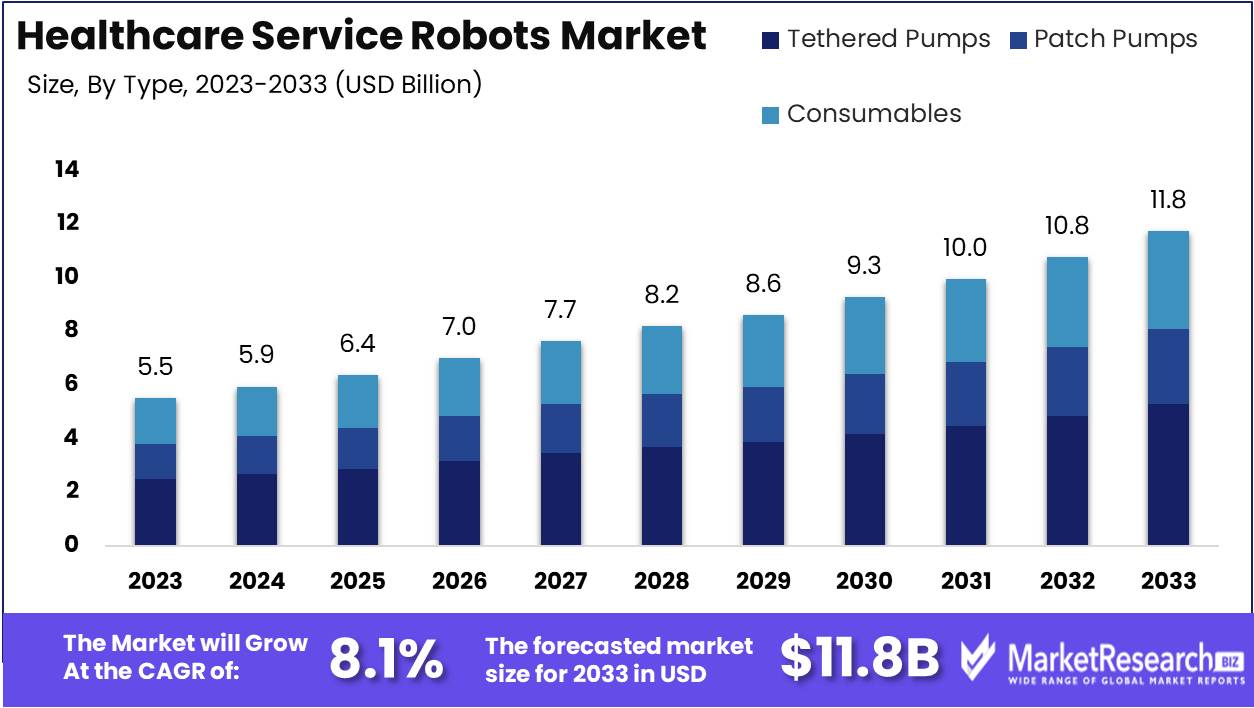

The Healthcare Service Robots Market was valued at USD 5.5 billion in 2023. It is expected to reach USD 11.8 billion by 2033, with a CAGR of 8.1% during the forecast period from 2024 to 2033.

The Healthcare Service Robots Market encompasses the development and deployment of robotic systems designed to support medical and caregiving tasks within healthcare settings. These robots enhance operational efficiency, patient care, and safety by performing a range of functions such as surgery assistance, patient monitoring, drug delivery, and sanitation. This market is driven by technological advancements, aging populations, and a growing demand for precision in medical procedures.

The healthcare service robots market is poised for significant growth, driven by several critical factors that are reshaping the industry landscape. Foremost among these is the aging global population, which is escalating the demand for advanced surgical and rehabilitation robots. As the geriatric demographic expands, the need for efficient and precise medical interventions becomes paramount, positioning healthcare robots as indispensable tools in modern medical practice. Furthermore, continuous technological advancements in robotics and artificial intelligence are catalyzing this market's expansion. Innovations are not only enhancing the functionality and effectiveness of these robots but also paving the way for new applications, thus broadening their adoption across diverse healthcare settings.

However, despite these promising trends, the market faces notable challenges that could impede its growth. Chief among these is the high initial investment and maintenance costs associated with healthcare robots. This financial barrier is particularly pronounced for smaller healthcare facilities, which may struggle to justify the substantial capital expenditure without clear, immediate returns. Consequently, while larger, well-funded institutions are likely to continue driving adoption, a concerted effort to reduce costs and demonstrate the long-term economic benefits of healthcare robots will be crucial for broader market penetration. Addressing these financial constraints, alongside continued technological progress and demographic shifts, will be essential for sustaining and accelerating growth in the healthcare service robots market.

Key Takeaways

- Market Growth: The Healthcare Service Robots Market was valued at USD 5.5 billion in 2023. It is expected to reach USD 10.1 billion by 2033, with a CAGR of 8.1% during the forecast period from 2024 to 2033.

- By Offering: Orthopedic Surgery dominated, driving healthcare service robot's precision and growth.

- By Deployment: Laparoscopy dominated Healthcare Service Robots with precision advancements.

- By Application: Disinfection robots dominated the healthcare service robots market.

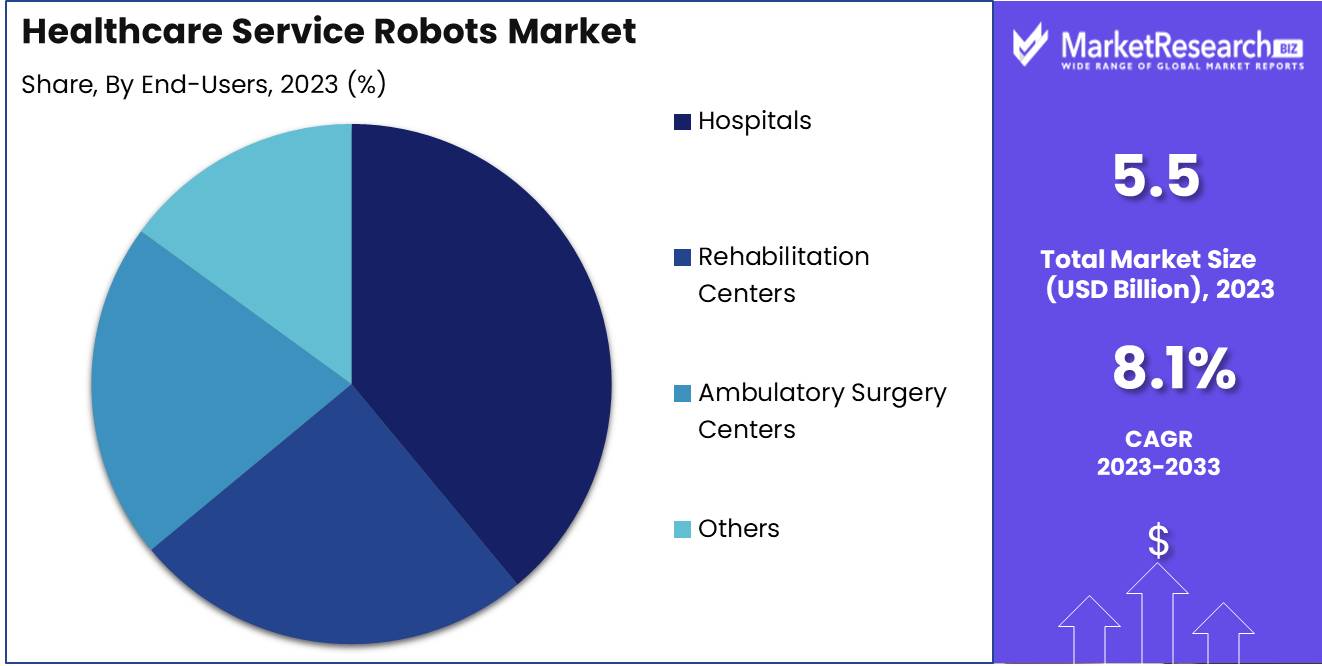

- By End-Users: Hospitals dominated healthcare service robots, enhancing surgical precision and efficiency.

- Regional Dominance: North America dominates the healthcare service robots market with a 40% largest share.

- Growth Opportunity: The global healthcare service robots market is set for growth, driven by AI, machine learning, and collaborative robots.

Driving factors

Technological Innovations in Cognition, Interaction, and Manipulation of Service Robotics: Revolutionizing Healthcare Service Delivery

Technological advancements in the cognition, interaction, and manipulation capabilities of service robots have significantly transformed the healthcare sector. These innovations have led to the development of more sophisticated and intuitive robots capable of performing complex tasks with greater precision and efficiency. For instance, cognitive improvements allow robots to better understand and respond to human needs, enhancing patient care through personalized interactions. Enhanced interaction capabilities enable robots to assist healthcare professionals more effectively, streamlining workflows and reducing the likelihood of human error.

Additionally, advancements in manipulation technology allow service robots to perform intricate procedures, such as minimally invasive surgeries, with remarkable accuracy. These combined technological innovations have made healthcare service robots indispensable tools in medical facilities, driving market growth by increasing their adoption and expanding their application scope.

Increasing Adoption of Surgical Robots: Pioneering Precision and Efficiency in Surgery

The increasing adoption of surgical robots represents a significant growth driver for the healthcare service robots market. Surgical robots, such as the da Vinci Surgical System, have gained widespread acceptance due to their ability to perform precise and minimally invasive procedures. According to recent statistics, the adoption rate of surgical robots has surged by approximately 12% annually over the past five years, reflecting their growing popularity among healthcare providers. This rise is attributed to the robots' ability to enhance surgical outcomes, reduce recovery times, and minimize the risks associated with traditional surgery.

Moreover, the integration of advanced imaging and real-time data analytics within these robots allows for better decision-making during surgeries, further cementing their value. As more hospitals and clinics invest in surgical robots to improve patient outcomes and operational efficiency, the market for healthcare service robots is poised for substantial growth.

Rising Advantages of Robotic-Assisted Surgery: Enhancing Patient Outcomes and Operational Efficiency

Robotic-assisted surgery offers numerous advantages that are propelling its adoption and, consequently, the growth of the healthcare service robots market. These advantages include greater precision, reduced trauma to the patient, and faster recovery times. For instance, robotic-assisted surgeries typically result in smaller incisions, which reduce the risk of infection and shorten hospital stays. A study found that patients undergoing robotic-assisted prostatectomy had a 20% lower risk of complications compared to those undergoing traditional surgery.

Furthermore, these procedures often involve less blood loss and pain, enhancing the overall patient experience. From an operational standpoint, robotic-assisted surgeries can lead to higher throughput in surgical departments, as reduced recovery times allow for more procedures to be scheduled. This increased efficiency not only boosts hospital revenue but also alleviates the burden on healthcare systems. The compelling advantages of robotic-assisted surgery are therefore driving both demand and innovation in the healthcare service robots market.

Restraining Factors

High Costs of Robotic Systems: A Major Barrier to Market Expansion

The high costs associated with the acquisition, implementation, and maintenance of healthcare service robots represent a significant barrier to the growth of this market. Advanced robotic systems, integral to modern healthcare, often come with a price tag that is prohibitive for many healthcare facilities, particularly smaller hospitals and clinics with limited budgets. For instance, the average cost of a surgical robot can range from $1 million to $2.5 million, excluding additional expenses for maintenance, training, and software upgrades.

This financial burden is further exacerbated by the need for specialized infrastructure to support these robots, such as dedicated operating rooms and advanced IT systems. As a result, the adoption of healthcare service robots is largely confined to well-funded institutions, creating a disparity in technological access and hindering widespread market penetration.

Additionally, the high upfront costs deter potential investors and healthcare administrators who may be wary of the long-term return on investment (ROI). This skepticism is compounded by the rapid pace of technological advancements, which can render expensive systems obsolete within a few years, further complicating the decision-making process for healthcare providers.

Lack of Reimbursement and Insurance Coverage: Limiting Adoption and Utilization

The absence of comprehensive reimbursement and insurance coverage for robotic-assisted procedures significantly stifles the growth of the healthcare service robots market. Reimbursement policies play a crucial role in the adoption of new medical technologies by offsetting costs for healthcare providers and patients. However, many insurance companies and public health systems have been slow to update their policies to include robotic procedures, often due to insufficient long-term data on cost-effectiveness and patient outcomes.

For example, while robotic-assisted surgeries can offer benefits such as reduced recovery times and lower risk of complications, these advantages are not always reflected in current reimbursement models. Consequently, hospitals and clinics are less inclined to invest in robotic systems if they cannot guarantee that the costs will be partially or fully reimbursed.

This coverage gap not only affects the financial viability of adopting robotic systems but also influences the perceived value of these technologies. Without insurance support, patients may be unable or unwilling to opt for robotic-assisted procedures, leading to underutilization of existing robotic systems and slowing the overall growth of the market.

By Offering Analysis

Orthopedic Surgery dominated, driving healthcare service robots' precision and growth.

In 2023, Orthopedic Surgery held a dominant market position in the By Offering segment of the Healthcare Service Robots Market, underscoring its significant impact and growth potential. This segment's prominence is driven by the increasing adoption of robotic-assisted surgical systems that enhance precision, reduce recovery times, and improve patient outcomes. The integration of advanced technologies such as AI and machine learning into orthopedic surgical robots has further propelled their utilization, catering to the rising demand for minimally invasive procedures.

Cardiology, another vital segment, is experiencing robust growth due to the escalating prevalence of cardiovascular diseases and the need for precise and efficient surgical interventions. Robotic systems in cardiology enable enhanced visualization and control, leading to improved surgical accuracy and patient safety.

Neurosurgery, while trailing behind orthopedic surgery and cardiology, is witnessing steady advancements. The intricate nature of neurosurgical procedures benefits greatly from robotic assistance, which offers unparalleled precision and dexterity. Innovations in this segment are poised to drive future growth, supported by increasing investments in healthcare robotics and the continuous development of sophisticated robotic platforms. Overall, the diverse applications across these segments illustrate the expansive potential and transformative impact of healthcare service robots.

By Deployment Analysis

In 2023, Laparoscopy dominated Healthcare Service Robots with precision advancements.

In 2023, Laparoscopy held a dominant market position in the By Deployment segment of the Healthcare Service Robots Market. This segment's prominence is attributed to the rising adoption of minimally invasive surgical procedures, which enhance patient recovery times and reduce hospital stays. Healthcare facilities increasingly invest in robotic-assisted laparoscopy to improve precision, reduce surgical errors, and enhance overall patient outcomes.

Pharmacy Applications are also gaining traction, driven by the need for automation in medication dispensing, which improves efficiency and accuracy in hospitals and pharmacies. Orthopedic Surgery benefits significantly from robotic assistance, which provides superior precision in complex procedures, leading to better patient outcomes and shorter rehabilitation periods.

External Beam Radiation Therapy robots are crucial in oncology for their precision in targeting cancerous tissues while sparing healthy cells, thus enhancing treatment efficacy. In Physical Rehabilitation, robotic systems offer personalized therapy, improve patient mobility, and track progress with high accuracy, contributing to better recovery rates.

Neurosurgery robots aid in highly delicate brain and spinal procedures, offering unparalleled precision and reducing the risk of complications. Lastly, the Other category, encompassing diverse applications such as dental surgery and diagnostic robots, continues to expand as technological advancements drive broader adoption across various medical fields. The overarching trend underscores a significant shift towards automation and precision in healthcare, positioning robotic deployment as a cornerstone of modern medical practice.

By Application Analysis

In 2023, Disinfection Robots dominated the healthcare service robots market.

In 2023, Disinfection Robots held a dominant market position in the "By Application" segment of the healthcare service robots market. Disinfection robots have become essential in healthcare settings due to their efficacy in reducing the spread of infections, especially during the COVID-19 pandemic. These robots utilize advanced UV-C light and hydrogen peroxide vapor to sterilize surfaces, offering a high level of precision and consistency that manual cleaning cannot achieve.

E-Assistance robots, meanwhile, are revolutionizing patient care by providing support to the elderly and disabled, enhancing their independence and quality of life through interactive and responsive technologies. Medical telepresence robots are facilitating remote consultations, allowing healthcare providers to interact with patients in real time without physical presence, thereby improving access to care in remote areas.

Delivery robots are optimizing logistical operations within hospitals by transporting medications, lab samples, and other medical supplies, thus freeing up healthcare workers to focus on patient care. Dispensing robots, on the other hand, ensure accurate and efficient medication dispensing, reducing errors and enhancing patient safety.

Other emerging categories, such as rehabilitation robots and surgical assistance robots, are also gaining traction, demonstrating significant potential to further augment the capabilities of healthcare professionals and improve patient outcomes. Collectively, these applications underscore the critical role of robotics in advancing healthcare efficiency, safety, and accessibility.

By End-Users Analysis

In 2023, Hospitals dominated healthcare service robots, enhancing surgical precision and efficiency.

In 2023, Hospitals held a dominant market position in the "By End-Users" segment of the healthcare service robots market. This preeminence is driven by the extensive adoption of robotic technologies to enhance surgical precision, improve patient care, and streamline operational efficiencies. Hospitals are increasingly investing in advanced robotic systems, such as surgical robots for minimally invasive procedures, robotic-assisted imaging devices, and automated medication dispensers. These technologies not only reduce the risk of human error but also significantly enhance patient outcomes and recovery times, thus solidifying hospitals' leading role in the market.

Rehabilitation centers also represent a significant segment, leveraging robotic systems for patient rehabilitation therapies. Robots aid in physical therapy by providing consistent, repeatable, and precise movements, which are crucial for patient recovery. The integration of robotics in rehabilitation centers helps improve patient mobility and accelerate recovery times, contributing to the segment's robust growth.

Ambulatory surgery centers (ASCs) are emerging as key players by adopting robotic systems to perform outpatient surgeries with higher efficiency and safety. The portability and precision of robotic surgical systems are particularly advantageous in ASCs, where space and time are critical constraints.

The "Others" category, encompassing nursing homes, diagnostic centers, and home care settings, is gaining traction as these entities adopt robotic solutions for tasks ranging from diagnostics to patient monitoring and daily care assistance. Collectively, these subsegments reflect the broadening scope and growing reliance on robotics across various healthcare settings, with hospitals leading the charge.

Key Market Segments

By Offering

- Orthopedic Surgery

- Cardiology

- Neurosurgery

By Deployment

- Laparoscopy

- Pharmacy Applications

- Orthopedic Surgery

- External Beam Radiation Therapy

- Physical Rehabilitation

- Neurosurgery

- Other

By Application

- Disinfection Robots

- E-Assistance

- Medical TRobotic Nurselepresence Robots

- Delivery Robots

- Dispensing Robots

- Others

By End-Users

- Hospitals

- Rehabilitation Centers

- Ambulatory Surgery Centers

- Others

Growth Opportunity

Integration of AI and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) into healthcare service robots represents a significant growth opportunity. AI and ML enhance the capabilities of robots, enabling them to perform complex tasks with greater accuracy and efficiency. For instance, AI-driven robots can assist in diagnostics by analyzing medical images and patient data to identify patterns and anomalies that might be missed by human eyes. Additionally, machine learning algorithms allow these robots to learn and improve from their interactions, leading to continuous performance enhancements. This technological synergy not only improves patient outcomes but also reduces the workload on healthcare professionals, allowing for more personalized and timely patient care.

Collaborative Robots (Cobots) for Safer Human-Robot Interaction

The advent of collaborative robots, or cobots, designed for safe human-robot interaction, is another key opportunity in the healthcare service robots market. Cobots are engineered to work alongside healthcare staff, assisting with tasks such as lifting patients, dispensing medication, or even performing minimally invasive surgeries. Their design prioritizes safety features, such as force limitation and real-time response to human presence, minimizing the risk of injury. The use of cobots can significantly enhance operational efficiency in healthcare settings, reduce the physical strain on medical staff, and improve patient care quality. By taking over repetitive and physically demanding tasks, cobots free up healthcare professionals to focus on more critical, patient-centered activities.

Latest Trends

Orthopedic Surgery Opportunities

The healthcare service robots market is poised to see significant advancements in orthopedic surgery. Robotics in this sector promises increased precision and improved outcomes, addressing the complex needs of orthopedic procedures. These robots enhance the capabilities of surgeons by providing tools that ensure greater accuracy in bone alignment and placement of implants. The integration of artificial intelligence and machine learning with robotic systems enables real-time data analysis, enhancing decision-making during surgeries. As the global population ages and the incidence of musculoskeletal disorders rises, the demand for orthopedic surgical robots is expected to surge. Hospitals and surgical centers are likely to invest heavily in this technology, driven by the need to improve patient outcomes and reduce recovery times.

Advantages of Robotic-Assisted Surgery

Robotic-assisted surgery continues to revolutionize the healthcare sector by offering several compelling advantages. Firstly, it provides unparalleled precision, reducing the risk of human error and enhancing the accuracy of surgical procedures. This is particularly crucial in delicate operations where even minor deviations can lead to significant complications. Secondly, robotic systems facilitate minimally invasive surgeries, which translate to smaller incisions, reduced blood loss, and quicker recovery times for patients.

Additionally, the consistency and reliability of robotic systems ensure that surgical procedures are performed with the same high standards every time, regardless of surgeon fatigue or other human factors. Furthermore, the integration of advanced imaging and navigation technologies allows for better visualization and manipulation of surgical sites, leading to improved surgical outcomes. These advantages not only enhance patient safety but also contribute to overall cost savings for healthcare providers by reducing the length of hospital stays and minimizing postoperative complications.

Regional Analysis

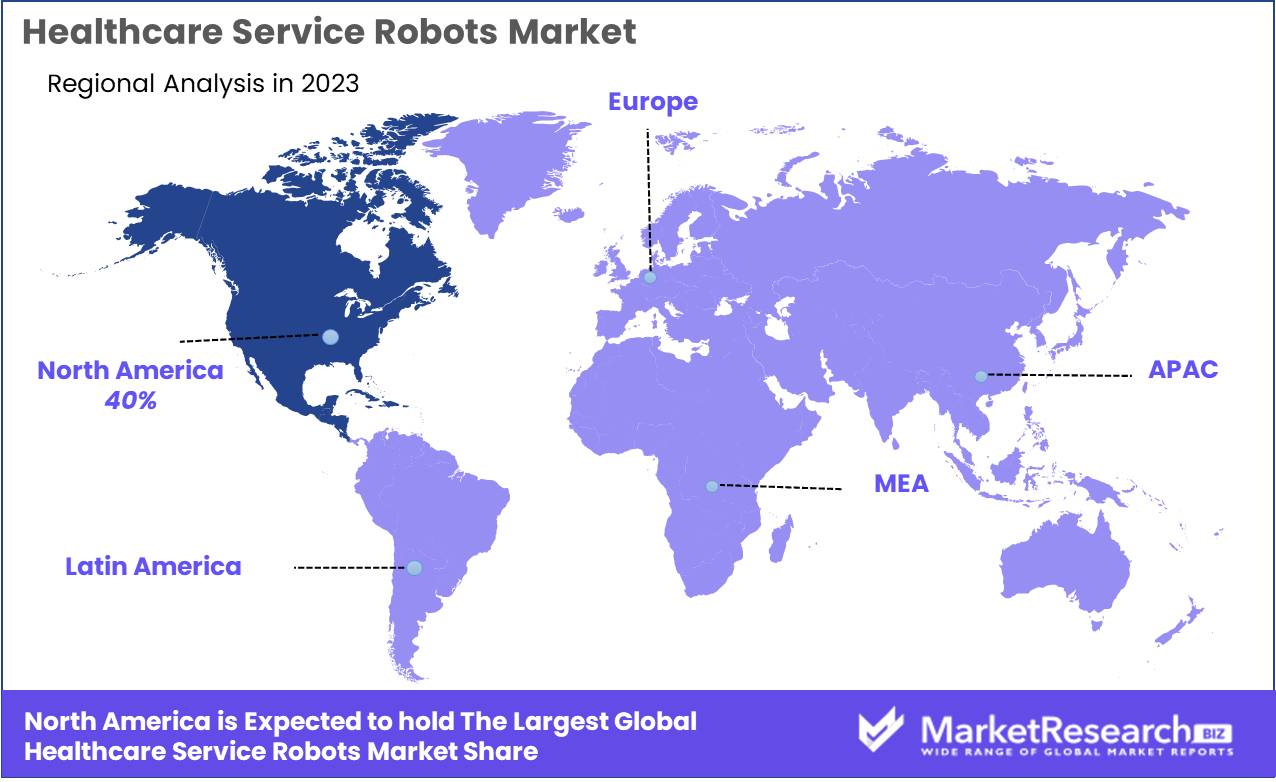

North America dominates the healthcare service robots market with a 40% largest share.

The global healthcare service robots market is experiencing significant growth, driven by advancements in robotics and increasing demand for automation in healthcare settings. Regionally, North America dominates the market, accounting for approximately 40% of the global market share. This dominance is attributed to the region's robust healthcare infrastructure, high adoption rate of advanced technologies, and substantial investments in R&D. The presence of leading market players further consolidates North America's leadership position.

Europe holds the second-largest market share, driven by increasing government initiatives and funding for healthcare innovation, alongside a growing elderly population requiring advanced care solutions. Key countries such as Germany, the UK, and France are at the forefront of this regional growth.

The Asia Pacific region is witnessing the fastest growth, with countries like China, Japan, and South Korea spearheading advancements in robotics technology. Rapid urbanization, rising healthcare expenditure, and a growing focus on improving healthcare services contribute to this region's expanding market presence.

In the Middle East & Africa, the market is gradually emerging, supported by increasing investments in healthcare infrastructure and a growing awareness of robotic solutions in medical applications. Meanwhile, Latin America shows moderate growth, primarily driven by Brazil and Mexico, where healthcare modernization efforts are gaining traction. Each region's unique economic and demographic factors play a critical role in shaping the healthcare service robots market's landscape.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global healthcare service robots market in 2024 is set for substantial growth, driven by innovations in robotic technology and increasing demand for automation in medical services. Key players in this market are poised to leverage their technological expertise and market presence to capitalize on emerging opportunities.

iRobot Corporation, traditionally known for consumer robots, is diversifying into healthcare, bringing its robust engineering capabilities to medical applications. Medrobotics Corporation and Titan Medical Inc. are at the forefront of minimally invasive surgical robots, enhancing precision and reducing recovery times for patients.

Renishaw Plc, renowned for its engineering and scientific technology, is innovating in neurosurgical robots, providing advanced solutions for complex brain surgeries. Health Robotics SLR and OR Productivity plc are enhancing pharmaceutical automation, and improving efficiency in drug dispensing and management.

Intuitive Surgical, a leader with its da Vinci Surgical System, continues to dominate the market with continuous upgrades and a strong focus on R&D. Mako Surgical Corp., now part of Stryker, specializes in orthopedic surgical robots, delivering customized joint replacement solutions.

Varian Medical Systems is a key player in radiation therapy, integrating robotics for precise cancer treatments. Stereotaxis Inc. focuses on robotic navigation systems for cardiology, enhancing the safety and efficacy of cardiac procedures. Mazor Robotics, also under Medtronic, provides innovative spine surgery solutions.

Stryker Corporation and Zimmer Biomet, established leaders in medical technology, are investing heavily in robotics to maintain their competitive edge. Overall, these companies are driving significant advancements, ensuring robust growth and transformative impacts in the healthcare service robots market.

Market Key Players

- iRobot Corporation

- Medrobotics Corporation

- Titan Medical Inc.

- Renishaw Plc

- Health Robotics SLR

- OR Productivity plc

- Intuitive Surgical

- Mako Surgical Corp.

- Varian Medical Systems

- Stereotaxis Inc.

- Mazor Robotics

- Medtronic

- Stryker Corporation

- Zimmer Biomet

- Other Key Players

Recent Development

- In April 2024, ABB introduced a new line of healthcare robots specifically designed for elderly care facilities. These robots are equipped with advanced sensors and AI to provide companionship, monitor vital signs, and assist with mobility and daily activities. ABB's initiative addresses the growing need for elder care solutions amidst an aging global population, aiming to improve the quality of life for seniors.

- In March 2024, Intuitive Surgical unveiled its latest AI-enhanced surgical robot, the da Vinci X2, designed to improve precision in minimally invasive surgeries. The new model incorporates advanced machine learning algorithms to assist surgeons in planning and executing complex procedures, thus increasing safety and outcomes for patients. This launch marks a significant advancement in robotic-assisted surgery technology.

- In February 2024, Boston Dynamics announced a strategic partnership with Mayo Clinic to deploy their Spot robots for hospital logistics. These robots will assist in delivering medications, medical supplies, and other critical items across the Mayo Clinic’s facilities. The initiative aims to enhance operational efficiency and reduce the workload on healthcare staff, allowing them to focus more on patient care.

Report Scope

Report Features Description Market Value (2023) USD 5.5 Billion Forecast Revenue (2033) USD 10.1 Billion CAGR (2024-2032) 8.1% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Offering (Orthopedic Surgery, Cardiology, Neurosurgery), By Deployment (Laparoscopy, Pharmacy Applications, Orthopedic Surgery, External Beam Radiation Therapy, Physical Rehabilitation, Neurosurgery, Other), By Application (Disinfection Robots, e-Assistance, Medical TRobotic Nurselepresence Robots, Delivery Robots, Dispensing Robots, Others), By Component (Security Systems, Locomotive Systems, Interface Applications, Software Platforms, Power Resources and Visualization Systems), By End-Users (Hospitals, Rehabilitation Centers, Ambulatory Surgery Centers, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape iRobot Corporation, Medrobotics Corporation, Titan Medical Inc., Renishaw Plc, Health Robotics SLR, OR Productivity plc, Intuitive Surgical, Mako Surgical Corp., Varian Medical Systems, Stereotaxis Inc., Mazor Robotics, Medtronic, Stryker Corporation, Zimmer Biomet, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- iRobot Corporation

- Medrobotics Corporation

- Titan Medical Inc.

- Renishaw Plc

- Health Robotics SLR

- OR Productivity plc

- Intuitive Surgical

- Mako Surgical Corp.

- Varian Medical Systems

- Stereotaxis Inc.

- Mazor Robotics

- Medtronic

- Stryker Corporation

- Zimmer Biomet

- Other Key Players

Our Clients

View Our Licence Options