Global Zeolite Market By Product(Natural, Synthetic), By Application(Catalysts, Adsorbents, Detergent Builders, Cement, Animal Feed, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

6365

-

July 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

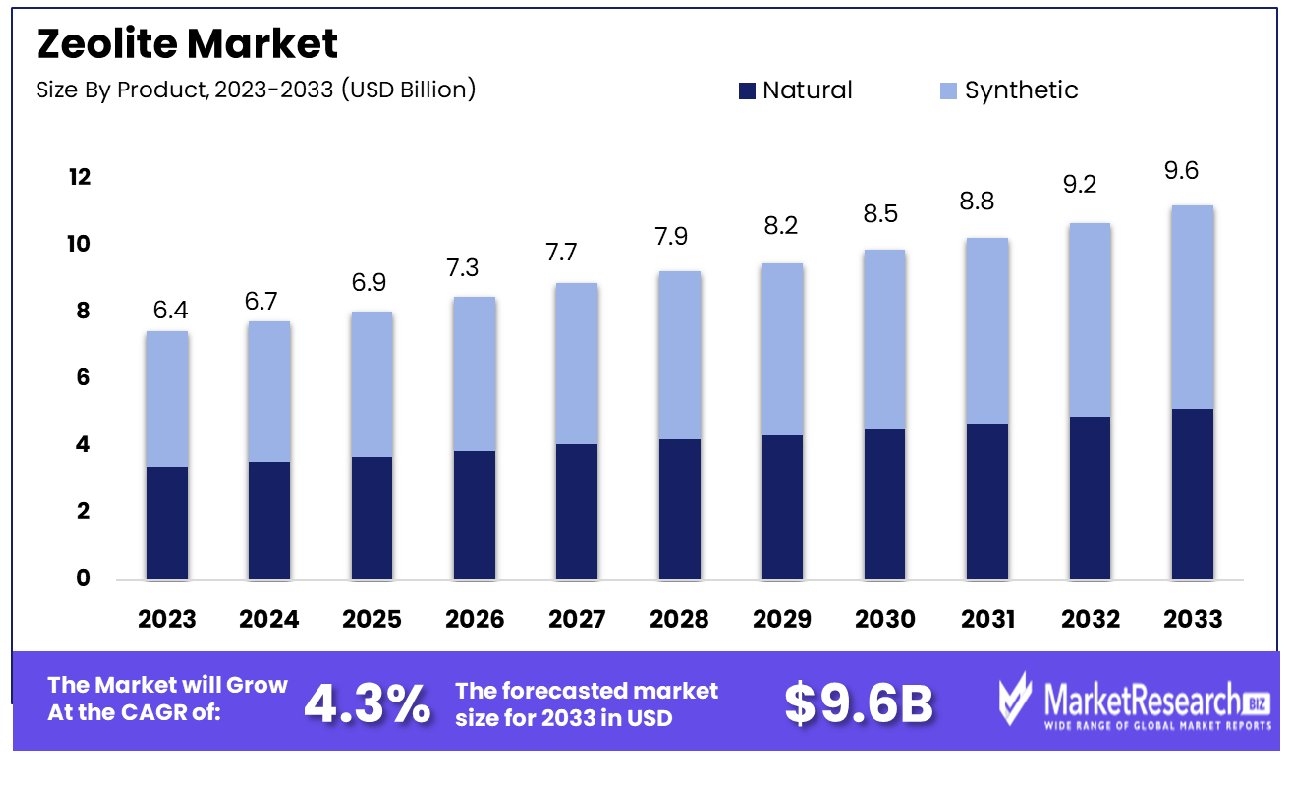

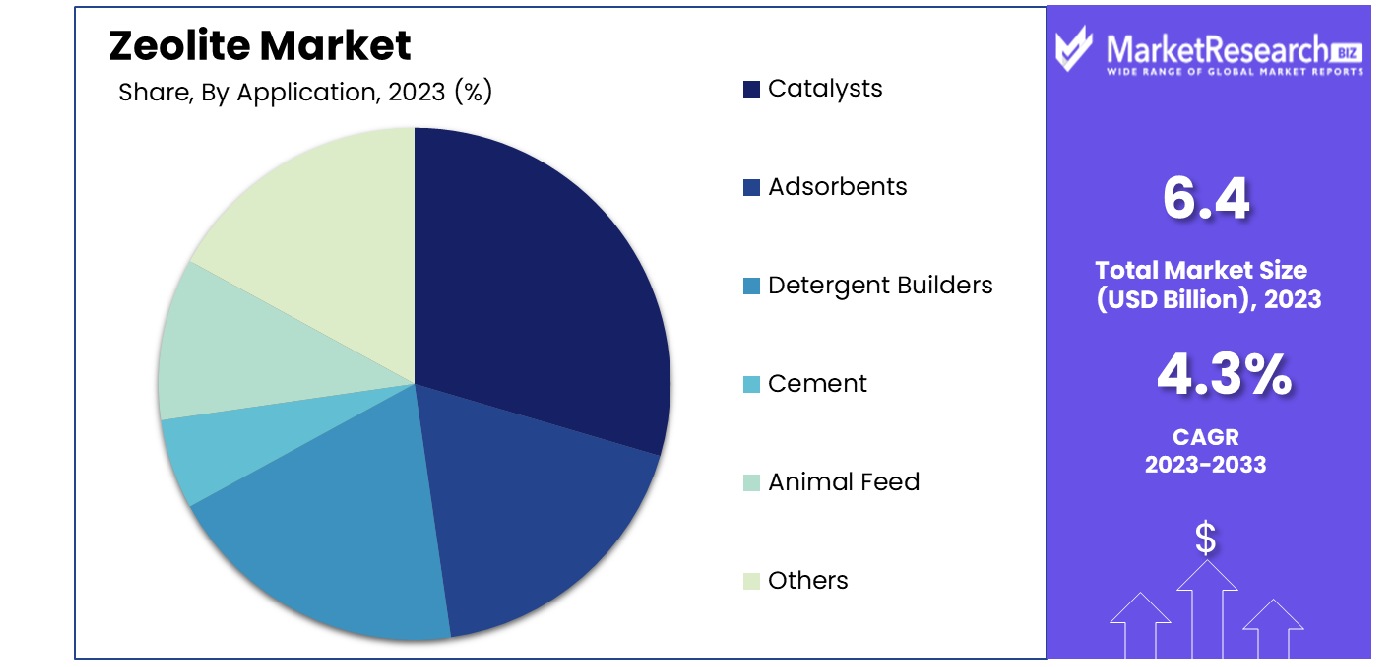

The Global Zeolite Market was valued at USD 6.4 billion in 2023. It is expected to reach USD 9.6 billion by 2033, with a CAGR of 4.3% during the forecast period from 2024 to 2033.

The zeolite market encompasses the global production and distribution of zeolite minerals, which are microporous, aluminosilicate minerals extensively utilized in various industrial, commercial, and consumer applications. These applications range from water purification and air filtration to catalysts in petrochemical refining. Zeolites are valued for their unique ability to exchange cations, making them highly effective for adsorption and separation processes.

The market is driven by demands in industries such as agriculture, detergents, and environmental protection. Strategic developments, including advancements in synthetic zeolite production, are poised to expand applications and drive market growth, catering to an increasing demand for sustainable and efficient materials.

The Zeolite Market presents a dynamic landscape characterized by significant production and application across diverse industries. Globally, the annual production of natural zeolite stands at approximately 3 million tonnes, with major contributions from countries such as China, South Korea, and Japan.

China, leading with 2 million tonnes produced in 2010, exemplifies the market's concentrated production capabilities. This is followed by South Korea (210,000 tonnes), Japan (150,000 tonnes), and other notable producers like Jordan, Turkey, Slovakia, and the United States. These figures underscore the strategic positioning of these nations in leveraging their natural reserves towards industrial applications.

From a market growth perspective, the increasing demand for eco-friendly and efficient materials has propelled the usage of zeolites in applications such as water purification, gas separation, and catalysts in the petrochemical industry. The properties of zeolites, including high surface area and the ability to undergo ion exchange, make them indispensable in environmental and agricultural solutions. Furthermore, advancements in synthetic zeolites are expected to broaden their applicability and enhance market penetration.

Key Takeaways

- Market Growth: The Global Zeolite Market was valued at USD 6.4 billion in 2023. It is expected to reach USD 9.6 billion by 2033, with a CAGR of 4.3% during the forecast period from 2024 to 2033.

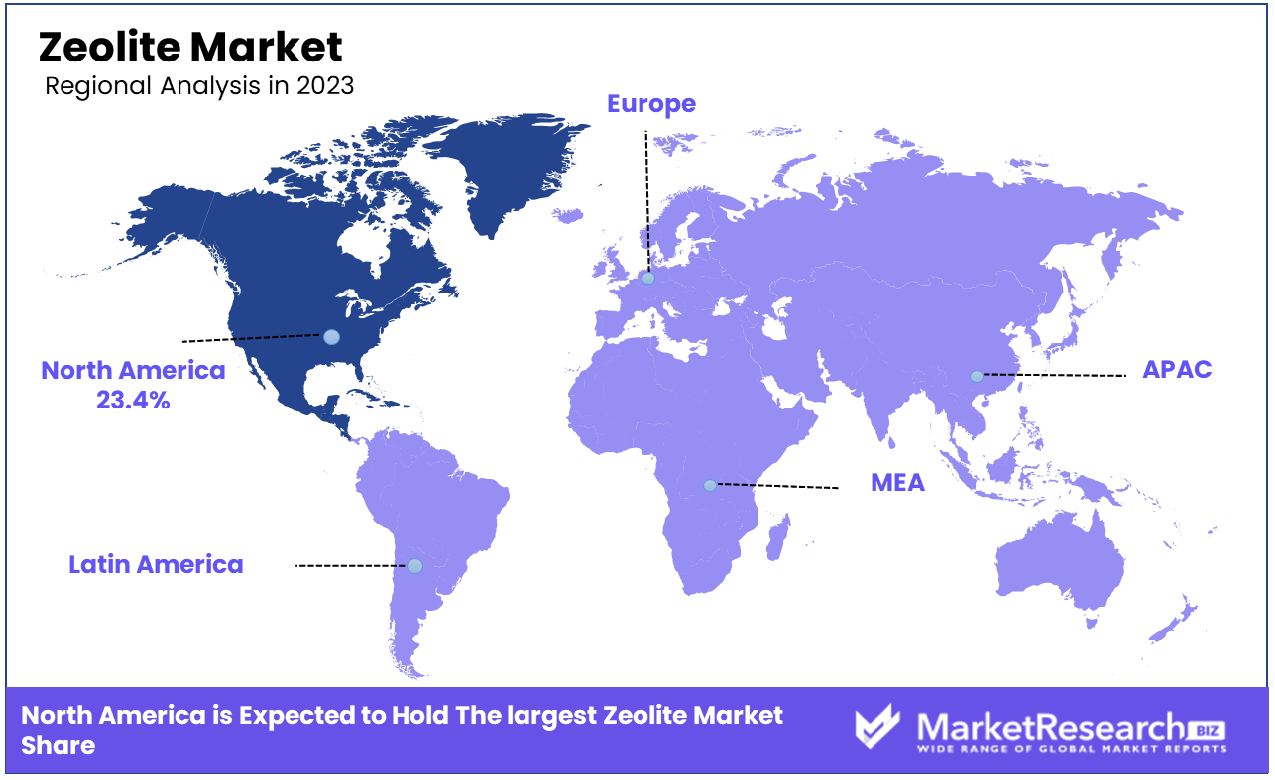

- Regional Dominance: The North American Zeolite Market holds a significant 23.4% share.

- By Product: Synthetic zeolites dominated the market with an 87.0% share.

- By Application: Zeolites are primarily used as catalysts, holding a 47.0% dominance.

Driving factors

Impact of Global Population Growth on Zeolite Demand for Detergents

The burgeoning global population, which is projected to reach approximately 9.7 billion by 2050, significantly enhances the demand for consumer products, particularly detergents. Zeolites, due to their ion-exchange properties, are extensively utilized in detergent formulations to soften water and enhance cleaning efficiency.

This growing demand directly correlates with the increased need for household cleaning products in burgeoning urban environments and developing regions. The expanding consumer base is likely to maintain a steady demand trajectory for zeolites in the laundry detergent industry, further propelled by innovations in detergent formulations that emphasize environmental sustainability and efficiency.

Zeolite Market Expansion Driven by the Petrochemical Industry

The expansion of the petrochemical sector, especially in emerging economies, plays a pivotal role in driving the demand for zeolites. Used primarily as catalysts in fluid catalytic cracking processes, zeolites enhance the efficiency and selectivity of chemical reactions essential for producing petrochemical derivatives like plastics, fibers, and rubbers.

The growth of industries such as automotive, construction, and packaging indirectly stimulates the demand for zeolites. As global economic conditions improve and consumption patterns rise, the petrochemical industry's expansion is expected to continue, thereby sustaining the growth momentum of the zeolite market.

Environmental Regulations Boosting Zeolite Utilization in Water Treatment

Rising environmental concerns have led to stringent regulations regarding water purity standards, which in turn have heightened the demand for effective water treatment solutions. Zeolites, with their natural ability to remove contaminants such as heavy metals and ammonia from water, are increasingly employed in both municipal and industrial water treatment facilities.

This surge in usage is supported by global efforts to improve water quality and the growing industrial emphasis on sustainable practices. The dual pressure of regulatory compliance and corporate sustainability initiatives is likely to further augment the demand for zeolites in the water treatment sector, contributing to overall market growth.

Restraining Factors

Market Challenges Posed by Alternatives to Zeolites

The availability of alternatives like silica gel and activated carbon poses significant challenges to the zeolite market. These materials are often favored in various applications such as adsorption and catalysis due to their comparable or superior performance characteristics in specific contexts.

Silica gel, for instance, is preferred for its higher pore volume in applications requiring intense moisture control, while activated carbon is renowned for its efficacy in removing a broader range of organic compounds from air and water. This competition can restrain the growth of the zeolite market as end-users opt for materials that best meet their specific functional requirements. Market differentiation and the development of high-performance zeolite variants are essential strategies for countering these alternatives.

Impact of Raw Material Supply Fluctuations on Zeolite Production Costs

Fluctuations in the supply of raw materials necessary for zeolite production significantly impact the market by increasing production costs. Zeolites are primarily manufactured from aluminosilicate minerals, which are subject to volatile pricing and availability due to geopolitical and economic factors. For instance, disruptions in mining activities or changes in export policies in key supplier countries can create supply shortages, driving up raw material costs.

These increased costs are often passed on to the end consumer, potentially making zeolites less competitive compared to their alternatives. Integrating these supply chain vulnerabilities into strategic planning is crucial for maintaining market stability and growth, despite these challenges.

By Product Analysis

Synthetic zeolites dominated the market by product, accounting for 87.0% due to their versatile industrial applications.

In 2023, Synthetic held a dominant market position in the by-product segment of the Zeolite Market, capturing more than an 87.0% share. This segment outperformed its counterpart, Natural, which constituted the remaining portion of the market. The substantial lead of synthetic zeolites can be attributed to their enhanced performance characteristics, uniformity in structure, and extensive application across diverse industries.

Synthetic zeolites are primarily favored for their high thermal stability and tailored pore sizes, which are crucial for applications in petrochemical cracking, gas separation, and ion exchange. The production of synthetic zeolites involves controlled processes that allow for the customization of properties to meet specific industrial needs, thereby broadening their utility.

The market dynamics of synthetic zeolites are influenced by the growing demand in the refining industry, where they are used as catalysts to improve yield and operational efficiencies. Additionally, the wastewater treatment sector increasingly relies on synthetic zeolites for removing contaminants due to their high ion exchange capacities.

Despite the smaller market share, natural zeolites also present significant opportunities. They are often marketed as eco-friendly alternatives due to their lower processing requirements and minimal environmental impact. The market for natural zeolites is expected to grow, driven by their applications in agriculture and construction, where they are used for soil remediation and as lightweight aggregate materials, respectively.

Overall, the zeolite market is expected to expand, with synthetic varieties continuing to lead due to their versatile applications and ability to meet stringent industrial specifications. Meanwhile, natural zeolites are likely to witness growth in niche markets, focusing on sustainable and environmentally friendly applications.

By Applications Analysis

Catalysts led with a 47.0% share, essential in chemical reactions and pollution control.

In 2023, Catalysts held a dominant market position in the By Application segment of the Zeolite Market, capturing more than a 47.0% share. Other significant applications included Adsorbents, Detergent Builders, Cement, Animal Feed, and Others. The prominence of catalysts in the market is primarily driven by their essential role in the refining and petrochemical industries, where they are used to enhance reaction efficiencies and selectivity.

The utilization of zeolites as catalysts offers substantial benefits, including improved product yield and the ability to operate at lower temperatures and pressures, thereby reducing energy consumption and operational costs. This application leverages the unique molecular sieve properties of zeolites, which are critical for processes such as fluid catalytic cracking (FCC) and hydrocracking.

Adsorbents formed the second largest category, driven by the demand for zeolites in applications requiring high surface area and specific pore size, such as gas purification and water treatment. Detergent builders also constituted a significant share, attributed to the phosphate-free formulation demands, enhancing the environmental sustainability of household and industrial cleaning products.

Further applications such as in cement as a pozzolanic material, in animal feed as a dietary supplement, and various niche markets underscore the versatility of zeolites. The cement industry utilizes natural zeolites to improve the mechanical properties and durability of concrete, while the animal feed industry benefits from their ability to bind toxins and improve nutrient absorption.

Overall, the zeolite market is set to grow, with catalysts maintaining their lead due to critical industrial applications, while emerging uses in eco-friendly products and processes are expected to drive further diversification and expansion of the market.

Key Market Segments

By Product

- Natural

- Synthetic

By Application

- Catalysts

- Adsorbents

- Detergent Builders

- Cement

- Animal Feed

- Others

Growth Opportunity

Potential of Synthetic Zeolites in Specialized Industrial Applications

The development of synthetic zeolites presents substantial opportunities for the zeolite market in 2023. These engineered counterparts to natural zeolites offer tailored pore sizes and structures, making them highly effective for specific industrial applications that demand precision, such as advanced catalysis in chemical manufacturing, pollution control, and gas separation.

The ability to design synthetic zeolites for particular functions allows them to meet stringent industry specifications, providing a competitive edge over natural zeolites and other alternative materials. This adaptability not only broadens the application scope of zeolites but also enhances their market penetration in industries seeking innovative solutions to complex challenges.

Expansion into Agricultural Applications

Increasing the use of zeolites in agricultural applications also heralds significant market opportunities. Zeolites' natural ion-exchange properties and water retention capabilities make them valuable for soil amendment purposes, improving water efficiency and nutrient retention in arid and semiarid regions. Additionally, their ability to slowly release nutrients helps in reducing the leaching of fertilizers into groundwater, aligning with sustainable agricultural practices.

As global focus intensifies on food security and sustainable farming practices, zeolites are poised to play a crucial role in agriculture by enhancing productivity and environmental sustainability. The integration of zeolites into agricultural products is expected to unlock new market segments and drive growth through 2023, leveraging their environmental benefits and functional versatility.

Latest Trends

Innovation in Zeolite Frameworks for Carbon Capture and Storage

A key trend in the 2023 zeolite market is the innovation in zeolite frameworks specifically designed for carbon capture and storage (CCS) applications. As global industries strive to meet stringent carbon emission targets, the demand for effective CCS technologies is surging. Zeolites, with their high surface area and stability under various conditions, are being engineered to improve their efficiency in capturing carbon dioxide from industrial emissions.

Advances in material science have led to the development of zeolites with modified pore structures and enhanced adsorption capacities, making them more suitable for capturing larger volumes of CO2. This trend not only supports global efforts to reduce greenhouse gas emissions but also opens new commercial avenues for zeolites in environmental management industries.

Enhanced Focus on Lightweight and High-Strength Zeolite Materials for Automotive Emissions Control

Another significant trend is the enhanced focus on developing lightweight and high-strength zeolite materials for automotive emissions control. The automotive industry is under continuous pressure to comply with evolving emissions regulations, which has spurred the development of advanced zeolite-based catalysts. These catalysts are designed to efficiently reduce harmful emissions such as NOx (nitrogen oxides) in vehicle exhaust systems.

The development of lighter and more robust zeolite materials contributes to overall vehicle weight reduction, which enhances fuel efficiency and lowers emissions further. This focus not only aligns with the automotive sector's goals to meet environmental standards but also enhances the performance and longevity of emissions control systems, positioning zeolites as an indispensable component in modern automotive engineering.

Regional Analysis

The North American Zeolite Market commands a substantial 23.4% share of the global market.

North America, holding a dominant market share of 23.4%, continues to lead due to substantial investments in environmentally friendly technologies, especially in the areas of industrial emissions control and wastewater treatment. The U.S. drives regional growth, leveraging its advanced petrochemical and automotive sectors, which extensively utilize zeolites for catalysis and emissions reduction.

Europe follows closely, with a strong emphasis on sustainability and stringent environmental regulations that bolster the demand for zeolites in water treatment and clean energy applications. The region's focus on reducing carbon footprints and enhancing green manufacturing processes has led to increased adoption of zeolites in chemical industries and agricultural applications, particularly in Germany and the UK.

Asia Pacific is identified as the fastest-growing region, fueled by rapid industrialization and urbanization, especially in China and India. The expansion of manufacturing, agriculture, and automotive sectors in these economies drives the demand for zeolites. The region's growth is further supported by governmental initiatives toward water purification and environmental conservation, making substantial use of zeolite-based solutions.

Middle East & Africa show promising growth, primarily due to the expanding petrochemical sector. The region utilizes zeolites in oil refining and gas processing applications, with Saudi Arabia and UAE leading in market penetration due to their substantial oil and gas reserves.

Latin America, though smaller in comparison, is gradually adopting zeolite technology, particularly in Brazil and Mexico, where there is growing awareness about sustainable agricultural practices and water treatment needs.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Zeolite market is significantly influenced by the strategic activities of leading companies such as Albemarle Corporation, BASF, Clariant, KMI Zeolite, Zeolite, and Zeolyst International. Each company contributes uniquely to the industry's landscape through innovation, geographic expansion, and application development.

Albemarle Corporation has positioned itself as a leader in high-purity zeolite synthesis, focusing on tailored solutions for the refining and petrochemical industries. Their commitment to research and development is evident in their production of specialized zeolites that enhance catalytic performance, driving cleaner production processes.

BASF stands out with its broad portfolio of zeolite-based catalysts, which are critical in environmental applications. Their products are pivotal in reducing emissions from industrial and automotive sources, aligning with global regulatory demands for environmental sustainability.

Clariant excels in the innovation of zeolites used in chemical synthesis and pollution control. Their focus on sustainable practices and eco-friendly materials resonates well with industries aiming to improve their environmental footprint through advanced material solutions.

KMI Zeolite primarily focuses on naturally occurring zeolites and capitalizes on their environmentally benign properties. Their product offerings are extensively utilized in agriculture and water purification, demonstrating a strong commitment to sustainable resource management.

Zeolyst International has carved a niche in the development of custom zeolite formulations. Their products are designed to meet specific client requirements in a variety of market segments, including healthcare, environmental, and industrial applications.

Market Key Players

- Albemarle Corporation

- BASF

- Clariant

- KMI Zeolite

- Zeolite

- Zeolyst International

Recent Development

- In June 2024, KMI Zeolite announced a partnership with a major water treatment company to supply zeolites for water purification systems. This partnership aims to enhance the efficiency of removing contaminants from water supplies.

- In March 2024, Albemarle Corporation launched a new high-purity zeolite product tailored for the petrochemical industry. This product aims to improve the efficiency of catalysts used in oil refining processes.

Report Scope

Report Features Description Market Value (2023) USD 6.4 Billion Forecast Revenue (2033) USD 9.6 Billion CAGR (2024-2032) 4.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Natural, Synthetic), By Application(Catalysts, Adsorbents, Detergent Builders, Cement, Animal Feed, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Albemarle Corporation, BASF, Clariant, KMI Zeolite, Zeolite, Zeolyst International Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Albemarle Corporation

- BASF

- Clariant

- KMI Zeolite

- Zeolite

- Zeolyst International

Our Clients

View Our Licence Options