Workwear Uniforms Market By Type (General Workwear, Corporate Workwear and Uniform), By Distribution Channel (Direct, Retail and E-Commerce), By Purpose (Rental, Purchase), By Demography (Men, Women), By End-User Industry (Manufacturing, Mining, Agriculture and Forestry Industry, Service, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

23905

-

August 2024

-

300

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

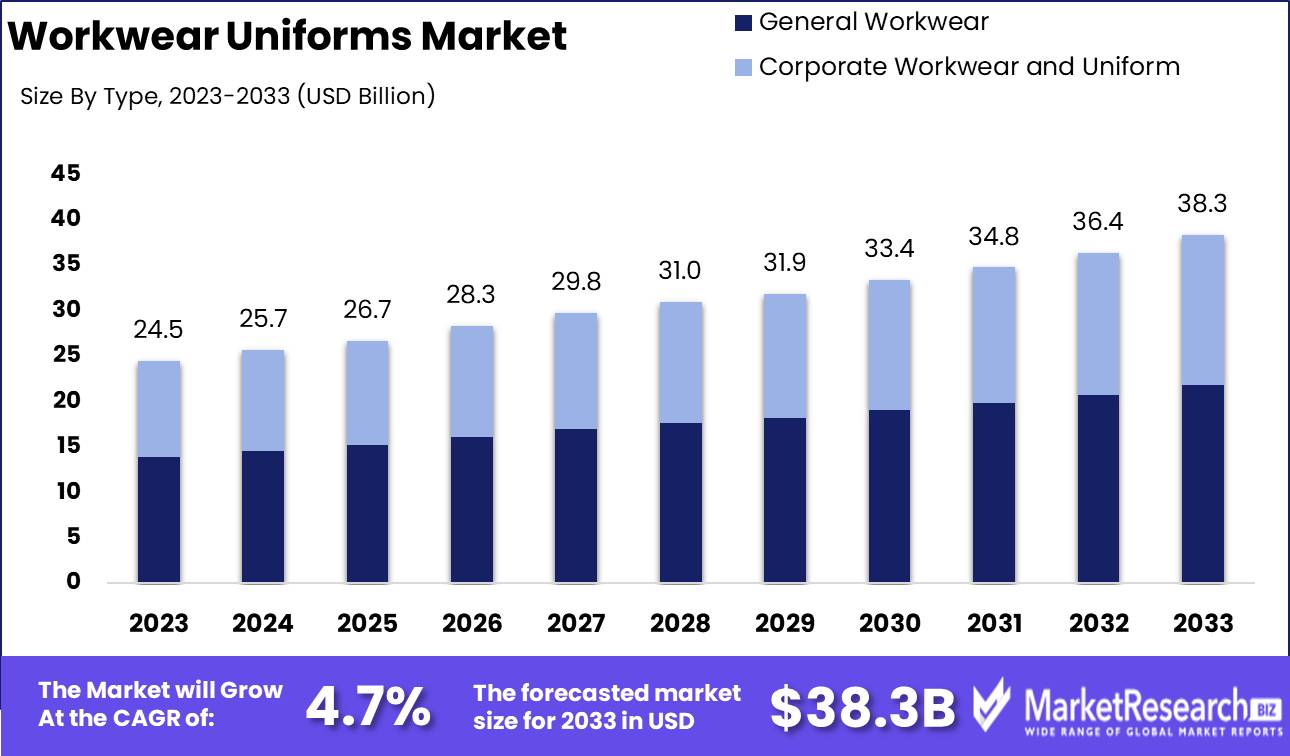

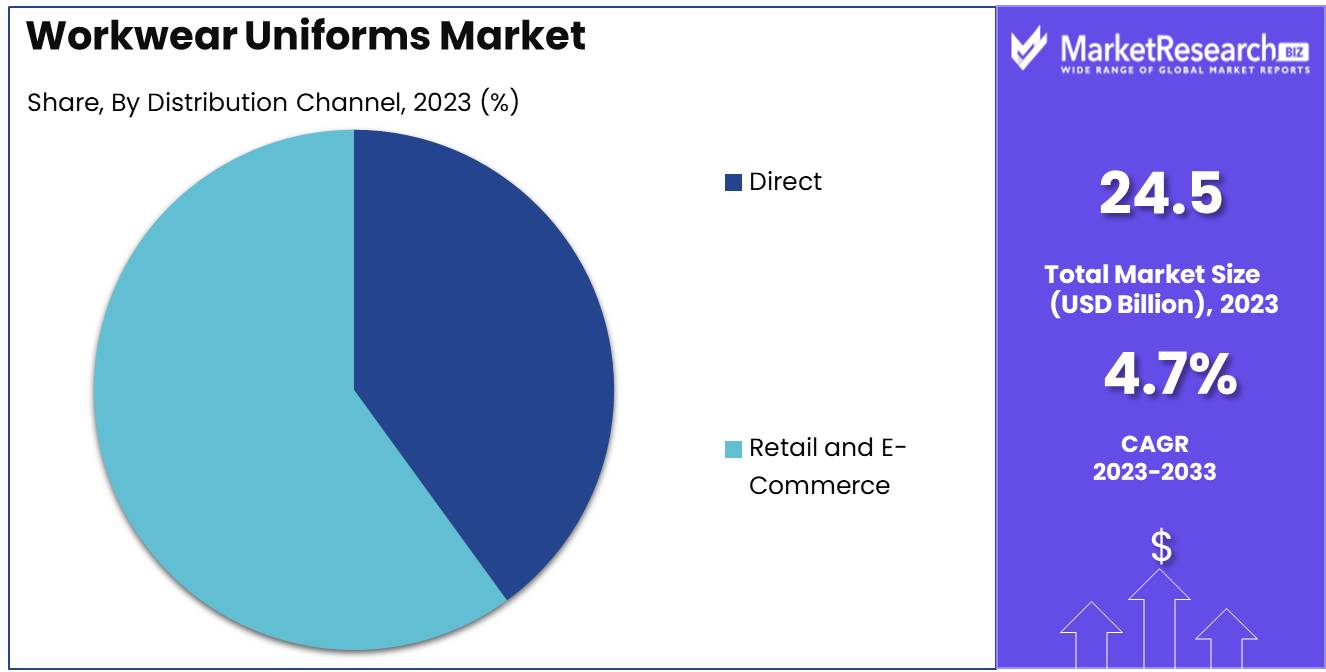

The Workwear Uniforms Market was valued at USD 24.5 billion in 2023. It is expected to reach USD 38.3 billion by 2033, with a CAGR of 4.7% during the forecast period from 2024 to 2033.

The Workwear Uniforms Market encompasses the segment of the apparel industry dedicated to uniforms designed for occupational use across various sectors. This market includes products such as corporate uniforms, industrial workwear, safety garments, and healthcare attire. Driven by evolving safety regulations, corporate branding needs, and technological advancements in fabric materials, the market has seen significant growth.

The Workwear Uniforms Market is experiencing significant transformation driven by evolving safety regulations, technological advancements, and shifting consumer preferences. Increasing safety regulations and standards across industries are propelling the demand for workwear that not only meets compliance but also enhances worker protection. Technological advancements in fabric and design are pivotal, as they facilitate the development of uniforms with superior durability, comfort, and functionality. This is complemented by the growing demand for customized and branded workwear, which reflects a broader trend towards personalized solutions in various sectors.

Additionally, the introduction of smart fabrics and wearables is revolutionizing the market, offering features such as real-time monitoring and environmental responsiveness. The integration of eco-friendly materials aligns with the rising emphasis on sustainability, further enhancing the appeal of workwear uniforms. These innovations are positioning the market to cater to a more diverse set of requirements, from enhanced durability to advanced functionality, reflecting a broader shift towards technology-driven and environmentally conscious product offerings. As such, the Workwear Uniforms Market is set to evolve rapidly, driven by these dynamic factors and the ongoing need for robust, adaptive solutions in the workplace.

Key Takeaways

- Market Growth: The Workwear Uniforms Market was valued at USD 24.5 billion in 2023. It is expected to reach USD 38.3 billion by 2033, with a CAGR of 4.7% during the forecast period from 2024 to 2033.

- By Type: General Workwear dominated the Workwear/Uniforms market due to versatility.

- By Distribution Channel: Retail dominated the Workwear/Uniforms Market, leading in reach.

- By Purpose: The Purchase segment dominates due to cost efficiency and customization benefits.

- By Demography: Men's workwear dominated due to high industrial sector demand.

- By End-User Industry: Manufacturing led the Workwear/Uniforms Market due to extensive needs.

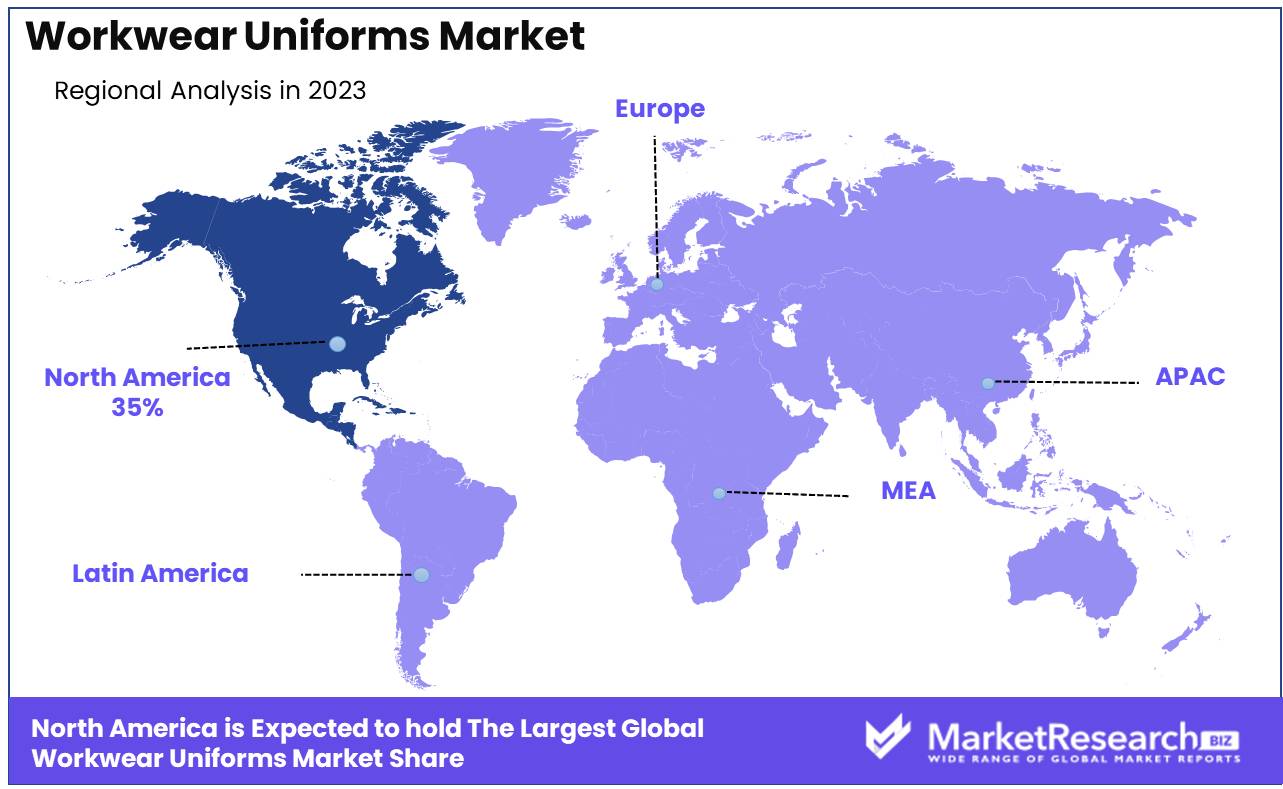

- Regional Dominance: North America dominates the workwear uniforms market with a 40% largest share.

- Growth Opportunity: Expanding workforce and stricter safety regulations drive growth in the global Workwear Uniforms Market, offering significant opportunities

Driving factors

Expanding Workforce and Industrialization

The growth of the workwear/uniforms market is significantly driven by the expanding workforce and rapid industrialization. As economies develop, there is a corresponding increase in the number of industrial and manufacturing units. This expansion necessitates a larger workforce, particularly in sectors like construction, manufacturing, and mining, where safety and operational efficiency are paramount. For instance, in 2023, global industrial employment saw an increase of approximately 3.5%, directly translating to higher demand for workwear.

Additionally, emerging markets in Asia Pacific and Latin America are witnessing unprecedented industrial growth, further propelling the need for specialized workwear to ensure worker safety and compliance with industry standards.

Strict Safety Regulations and Concerns

The implementation of stringent safety regulations and heightened awareness of worker safety are critical factors driving the demand for workwear and uniforms. Regulatory bodies such as OSHA (Occupational Safety and Health Administration) in the United States and the European Agency for Safety and Health at Work have mandated the use of specific workwear to reduce workplace injuries and fatalities. Compliance with these regulations is non-negotiable for companies, leading to a substantial and consistent demand for certified protective clothing.

For example, in 2022, the global market for high-visibility clothing grew by 6%, reflecting the direct impact of safety regulations on market expansion. The focus on safety not only protects employees but also mitigates legal risks and enhances corporate reputation.

Corporate Branding and Image Enhancement

The role of workwear in corporate branding and image enhancement cannot be understated. Companies increasingly recognize the value of a consistent and professional appearance, which workwear and uniforms provide. This trend is particularly prominent in service-oriented sectors such as hospitality, healthcare, and retail, where customer perception directly influences business success. Branded uniforms contribute to a cohesive corporate identity, instill a sense of belonging among employees, and promote brand recognition. For instance, a survey conducted in 2023 revealed that 68% of customers perceive uniformed employees as more professional and trustworthy. Consequently, businesses are investing more in high-quality, branded workwear, driving the market growth.

Restraining Factors

Impact of Fluctuations in Raw Material Prices on Workwear/Uniforms Market Growth

Fluctuations in raw material prices significantly impact the growth trajectory of the Workwear/Uniforms Market. Raw materials such as cotton, polyester, and specialized fabrics are essential in the production of workwear and uniforms. Volatility in the prices of these materials can lead to increased production costs, which in turn affects the overall pricing structure of workwear products.

For instance, recent data indicates that cotton prices have experienced considerable fluctuations due to supply chain disruptions and climatic conditions affecting global production. This volatility leads to unpredictable cost structures for manufacturers, compelling them to either absorb the increased costs or pass them on to consumers. The latter option can lead to higher prices for end-users, potentially reducing demand, particularly in cost-sensitive segments of the market.

Additionally, fluctuations in the prices of synthetic fibers and specialized fabrics used in high-performance workwear, such as flame-resistant or anti-static uniforms, further contribute to market instability. As manufacturers face higher costs, their ability to offer competitively priced products diminishes, which can restrict market growth and slow down the adoption of advanced workwear solutions.

Influence of the Availability of Many Substitutes on Workwear/Uniforms Market Growth

The availability of numerous substitutes for traditional workwear and uniforms poses a significant challenge to market growth. Substitutes in this context include alternative types of clothing and gear that serve similar functions but may offer different benefits or cost advantages. For example, the rise of casual or "smart casual" dress codes in various industries has led to an increased acceptance of non-traditional workwear options.

Moreover, technological advancements have led to the development of multifunctional clothing that combines the features of workwear with casual attire. This trend has introduced a broader range of alternatives, further fragmenting the market and increasing competition.

The proliferation of substitute products often results in price pressure and reduced market share for traditional workwear manufacturers. As consumers and businesses explore more versatile or cost-effective options, the demand for conventional workwear may decrease. This shift in consumer preference can slow market growth by diverting potential revenue streams away from traditional workwear products.

By Type Analysis

In 2023, General Workwear dominated the Workwear/Uniforms market due to versatility.

In 2023, General Workwear held a dominant market position in the Workwear/Uniforms market's By Type segment. General Workwear includes apparel designed for a variety of industries, including manufacturing, construction, and logistics, where practicality and durability are paramount. This segment has seen robust demand due to the increasing emphasis on workplace safety and the need for protective clothing that meets industry standards. The versatility of General Workwear, combined with advancements in materials technology that enhance comfort and functionality, has contributed to its substantial market share.

In contrast, Corporate Workwear and Uniforms cater to specific sectors such as hospitality, healthcare, and retail, where a more formal or brand-consistent appearance is required. This segment also holds a significant position, driven by the growing focus on brand identity and professional appearance. Corporate Workwear and Uniforms often incorporate design elements that promote brand recognition and align with corporate standards.

By Distribution Channel Analysis

In 2023, Retail dominated the Workwear/Uniforms Market, leading in reach.

In 2023, The Retail segment held a dominant market position in the Workwear/Uniforms Market, reflecting its significant influence on market dynamics. The Retail sector's strong performance can be attributed to its extensive reach and established presence in both physical and online stores. Retail channels offer direct access to consumers, enabling them to view and purchase workwear and uniforms conveniently. This direct interaction between retailers and customers facilitates immediate feedback and personalized service, driving consumer satisfaction and repeat purchases. Retailers also benefit from established brand recognition and loyalty, further consolidating their position in the market.

Conversely, The E-Commerce segment has been experiencing rapid growth, driven by the increasing preference for online shopping due to its convenience and accessibility. E-commerce platforms provide a wide range of workwear and uniforms, often accompanied by detailed product descriptions and customer reviews, enhancing the shopping experience. The rise of mobile commerce and advancements in online payment systems have further fueled the growth of the E-commerce segment. Both Retail and E-Commerce play crucial roles in shaping the workwear/uniforms market, catering to diverse consumer preferences and contributing to overall market expansion.

By Purpose Analysis

The Purchase segment dominates due to cost efficiency and customization benefits.

In 2023, The Purchase segment held a dominant market position in the Workwear/Uniforms Market by Purpose segment. The preference for purchasing workwear is driven by several factors, including long-term cost efficiency and the desire for tailored, company-specific uniforms that enhance brand identity. Organizations across industries such as healthcare, hospitality, and manufacturing invest significantly in custom uniforms to ensure brand consistency and employee satisfaction. The increased focus on quality and durability, combined with advancements in fabric technology, has also encouraged companies to opt for purchase over rental.

Conversely, the Rental segment continues to gain traction due to its flexibility and cost-effective nature, particularly appealing to small and medium-sized enterprises (SMEs). Rental services offer a hassle-free solution for companies needing uniforms for seasonal or temporary staff, avoiding the upfront costs and inventory management associated with purchasing. The rental model also includes maintenance services, such as cleaning and repairs, which reduce the operational burden on businesses. This segment is bolstered by the trend towards sustainable practices, as rental services often promote the reuse and recycling of garments.

By Demography Analysis

In 2023, Men's workwear dominated due to high industrial sector demand.

In 2023, Men held a dominant market position in the "By Demography" segment of the Workwear/Uniforms market. This prominence is largely driven by the higher representation of men in industrial sectors such as construction, manufacturing, and logistics, where durable and functional workwear is essential. The demand for men's workwear is bolstered by stringent safety regulations and the necessity for specialized clothing that ensures protection and compliance with industry standards.

Women also emerged as a significant demographic in the Workwear/Uniforms market. This growth is attributed to the increasing participation of women in various industries, including healthcare, hospitality, and corporate sectors, where professional attire and uniforms are critical. The evolving corporate culture and the push for gender diversity in workplaces have led to a heightened demand for women's workwear that combines style, comfort, and practicality. Manufacturers are responding with tailored solutions that address the specific needs of female professionals, such as better fit, flexibility, and fabric choices.

By End-User Industry Analysis

In 2023, Manufacturing led the Workwear/Uniforms Market due to extensive needs.

In 2023, The Manufacturing sector held a dominant market position in the Workwear/Uniforms Market. This dominance is attributable to the sector's extensive requirement for protective and specialized clothing due to the nature of its operations. Workwear in manufacturing environments is essential for ensuring safety, compliance with health regulations, and enhancing operational efficiency. The demand for durable and functional workwear is driven by the need to protect workers from hazardous conditions, including exposure to chemicals, high temperatures, and mechanical injuries.

In comparison, the Mining sector also maintained a significant presence within the Workwear/Uniforms Market, due to its rigorous safety requirements and challenging working conditions. Workwear in mining includes flame-resistant and high-visibility garments designed to withstand extreme environments and ensure worker safety.

The Agriculture and Forestry Industry contributed to the market with a steady demand for rugged, durable workwear suitable for outdoor and often harsh conditions. Service industries, while smaller in comparison, also drove demand for uniforms reflecting professionalism and branding. The "Others" category encompassed diverse sectors, each contributing to the overall market with specific workwear needs, but without the significant impact seen in the primary sectors.

Key Market Segments

By Type

- General Workwear

- Corporate Workwear and Uniform

By Distribution Channel

- Direct

- Retail and E-Commerce

By Purpose

- Rental

- Purchase

By Demography

- Men

- Women

By End-User Industry

- Manufacturing

- Mining

- Agriculture and Forestry Industry

- Service

- Others

Growth Opportunity

Expanding Workforce and Industrialization

The global Workwear Uniforms Market is poised for substantial growth, driven by the expanding workforce and accelerating industrialization. As economies continue to develop and sectors such as manufacturing, construction, and healthcare expand, the demand for workwear uniforms is increasing. This trend is particularly evident in emerging markets, where industrial activities are surging and new businesses are being established. The requirement for standardized and protective workwear is becoming crucial, not only for compliance but also for enhancing worker efficiency and safety. Companies are investing in high-quality, durable uniforms that cater to the specific needs of various industries, creating a significant growth opportunity for market players.

Increased Safety Regulations

Another key driver for the market's expansion is the rise in safety regulations across different industries. Governments and regulatory bodies worldwide are implementing stricter safety standards to protect workers and reduce workplace accidents. These regulations often mandate the use of specific types of workwear that meet certain safety criteria. As a result, businesses are increasingly upgrading their workwear uniforms to comply with these regulations, thereby driving market demand. The emphasis on safety has led to innovations in workwear materials and designs, enhancing functionality and protection. Companies that can provide compliant and advanced workwear solutions are likely to gain a competitive edge in this growing market.

Latest Trends

Rising Demand for Safety Gear

The Workwear Uniforms Market is witnessing a marked increase in the demand for safety gear. This trend is driven by heightened awareness of workplace safety regulations and the need to protect employees in high-risk industries such as construction, manufacturing, and chemical processing. Organizations are investing in advanced safety uniforms that incorporate features such as flame resistance, high visibility, and ergonomic designs to enhance worker safety and compliance with stringent regulations. This growing focus on safety is also being influenced by the increasing number of safety-related incidents and the push for improved safety standards globally.

Focus on Professionalism and Branding

Simultaneously, there is a strong emphasis on professionalism and branding within the workwear segment. Companies are recognizing the role of uniforms in promoting their brand identity and enhancing the professional image of their workforce. Workwear is no longer viewed merely as functional attire but as a strategic tool for brand differentiation and employee morale. Organizations are opting for customized uniforms that reflect their brand colors, logos, and values, thereby reinforcing corporate identity and fostering a sense of unity among employees. This trend is also supported by the increasing demand for workwear that combines style with functionality, catering to both professional appearance and practical needs.

Regional Analysis

North America dominates the workwear uniforms market with a 40% largest share.

North America dominates the global workwear uniforms market, holding a substantial market share of approximately 35%. The region's leadership is driven by stringent safety regulations and a high demand for specialized workwear across various industries, including construction, manufacturing, and healthcare. The U.S. is the primary contributor, with significant investments in technological advancements and innovation in workwear materials. Canada also contributes to the regional market, driven by its robust industrial sector and increasing adoption of advanced workwear solutions.

Europe holds a significant share of around 30%, with major markets including Germany, the UK, and France. The region benefits from a well-established industrial base and regulatory frameworks that emphasize worker safety and compliance. The growing emphasis on sustainability and eco-friendly materials is shaping the market dynamics, with increased demand for environmentally responsible workwear options.

Asia Pacific is witnessing rapid growth, with a market share of approximately 25%. The expansion is fueled by industrialization, particularly in countries like China and India, where increasing manufacturing and construction activities drive the demand for workwear. Additionally, the rising focus on occupational safety and protective clothing contributes to the region’s growth.

Middle East & Africa and Latin America hold smaller shares of around 5% and 10%, respectively. The market in these regions is emerging, with growth driven by infrastructural developments and industrial activities. However, the relatively smaller market size compared to North America and Europe reflects ongoing economic and industrial development stages.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Workwear Uniforms market remains highly competitive, with several prominent players shaping the industry landscape. Key companies such as Dickies, Carhartt, and Red Kap from the U.S. continue to dominate the market with their extensive product lines and strong brand recognition. Dickies, known for its durable and high-quality workwear, maintains a significant market share through its broad distribution network and continuous innovation. Similarly, Carhartt leverages its reputation for rugged work apparel to capture substantial market interest.

European players also hold notable positions, with Alsico Group and Delta Plus Group leading in the Belgian and French markets, respectively. Alsico’s commitment to ergonomic design and Delta Plus’s focus on safety and protection bolster their competitive edge. Additionally, Fristads Kansas Group from Sweden and Engelbert Strauss GmbH & Co. KG from Germany are recognized for their high-performance workwear, contributing to their strong market presence.

VF Corporation and Williamson-Dickie Manufacturing Company from the U.S. continue to expand their global reach through strategic acquisitions and product diversification. Other significant players include Cintas Corporation and Aramark, which offer comprehensive workwear solutions and uniform services, catering to diverse industry needs.

Overall, the market is characterized by robust competition, driven by innovation, quality, and strategic global expansion, positioning these key players as leaders in the workwear uniforms sector.

Market Key Players

- Dickies (U.S.)

- Carhartt (U.S.)

- Red Kap (U.S.)

- Alsico Group (Belgium)

- Delta Plus Group (France)

- Williamson-Dickie Manufacturing Company (U.S.)

- VF Corporation (U.S.)

- Fristads Kansas Group (Sweden)

- Engelbert Strauss GmbH & Co. KG (Germany)

- Alsico NV (Belgium)

- Adolphe Lafont (France)

- Mascot International A/S (Denmark)

- Aramark (The U.S)

- Cintas Corporation (The U.S)

- Liberty Work and Leisure Wear Limited (UK)

- The Uniform House (The U.S)

- Landau Uniforms (The U.S)

- Superior Group of Companies (The U.S)

- Johnsons Apparelmaster Limited (UK)

- MARTIN & LEVESQUE (Canada)

Recent Development

- In July 2024, Cintas Corporation launched a new line of eco-friendly workwear uniforms designed to improve sustainability in the industry. These uniforms are made from recycled materials and feature improved durability and comfort.

- In June 2024, Aramark introduced a new digital uniform management system that allows clients to manage their workwear inventory and employee orders through a streamlined online platform.

- In May 2024, G&K Services expanded its product offerings by incorporating advanced antimicrobial fabric technology into its workwear uniforms, aimed at enhancing employee hygiene and safety in high-risk environments.

Report Scope

Report Features Description Market Value (2023) USD 24.5 Billion Forecast Revenue (2033) USD 38.3 Billion CAGR (2024-2032) 4.7% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (General Workwear, Corporate Workwear, and Uniform), By Distribution Channel (Direct, Retail, and E-Commerce), By Purpose (Rental, Purchase), By Demography (Men, Women), By End-User Industry (Manufacturing, Mining, Agriculture, and Forestry Industry, Service, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Dickies (U.S.), Carhartt (U.S.), Red Kap (U.S.), Alsico Group (Belgium), Delta Plus Group (France), Williamson-Dickie Manufacturing Company (U.S.), VF Corporation (U.S.), Fristads Kansas Group (Sweden), Engelbert Strauss GmbH & Co. KG (Germany), Alsico NV (Belgium), Adolphe Lafont (France), Mascot International A/S (Denmark), Aramark (The U.S), Cintas Corporation (The U.S), Liberty Work and Leisure Wear Limited (UK), The Uniform House (The U.S), Landau Uniforms (The U.S), Superior Group of Companies (The U.S), Johnsons Apparelmaster Limited (UK), MARTIN & LEVESQUE (Canada) Customization Scope Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Dickies (U.S.)

- Carhartt (U.S.)

- Red Kap (U.S.)

- Alsico Group (Belgium)

- Delta Plus Group (France)

- Williamson-Dickie Manufacturing Company (U.S.)

- VF Corporation (U.S.)

- Fristads Kansas Group (Sweden)

- Engelbert Strauss GmbH & Co. KG (Germany)

- Alsico NV (Belgium)

- Adolphe Lafont (France)

- Mascot International A/S (Denmark)

- Aramark (The U.S)

- Cintas Corporation (The U.S)

- Liberty Work and Leisure Wear Limited (UK)

- The Uniform House (The U.S)

- Landau Uniforms (The U.S)

- Superior Group of Companies (The U.S)

- Johnsons Apparelmaster Limited (UK)

- MARTIN & LEVESQUE (Canada)

Our Clients

View Our Licence Options