Retail Industry Market By Product (Pharmaceuticals, Luxury Goods, Electronic and Household Appliances, Furniture, Toys, Others), By Distribution Channel (Hypermarkets, E-Commerce, Convivence Stores, Department Stores, Specialty Stores, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

47504

-

June 2024

-

300

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

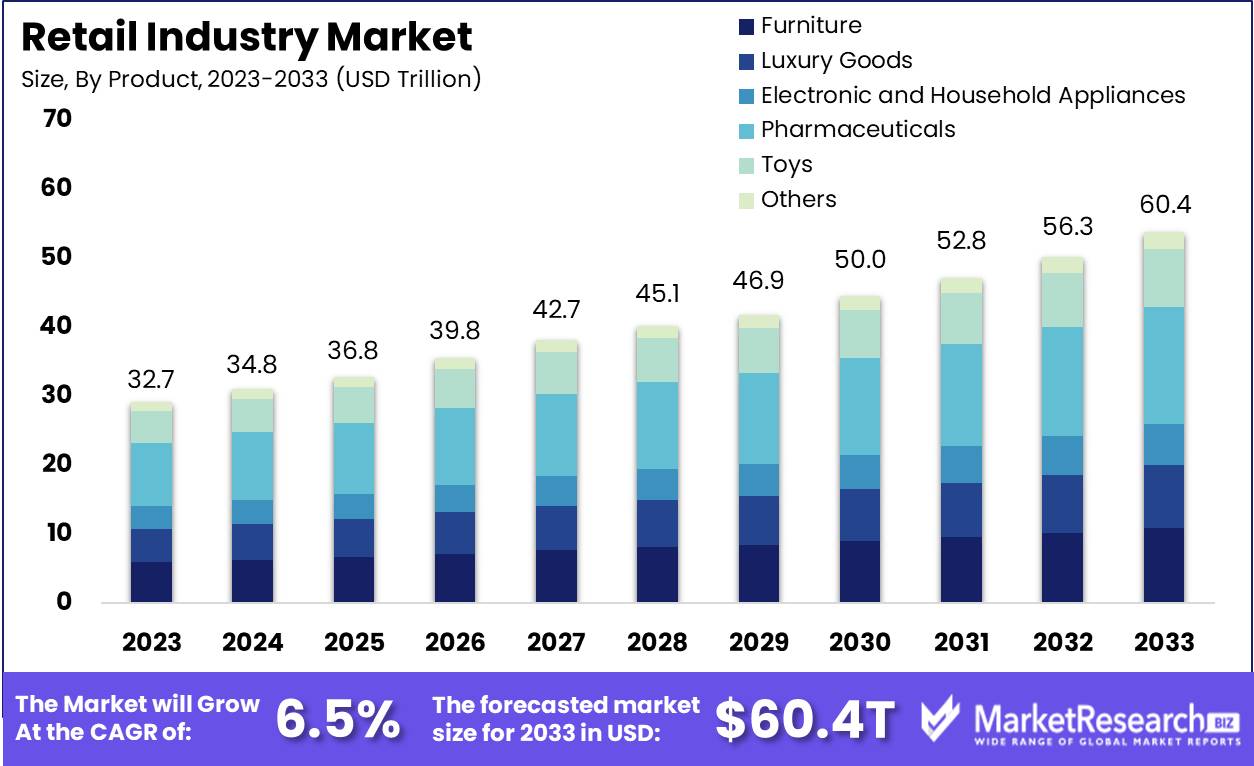

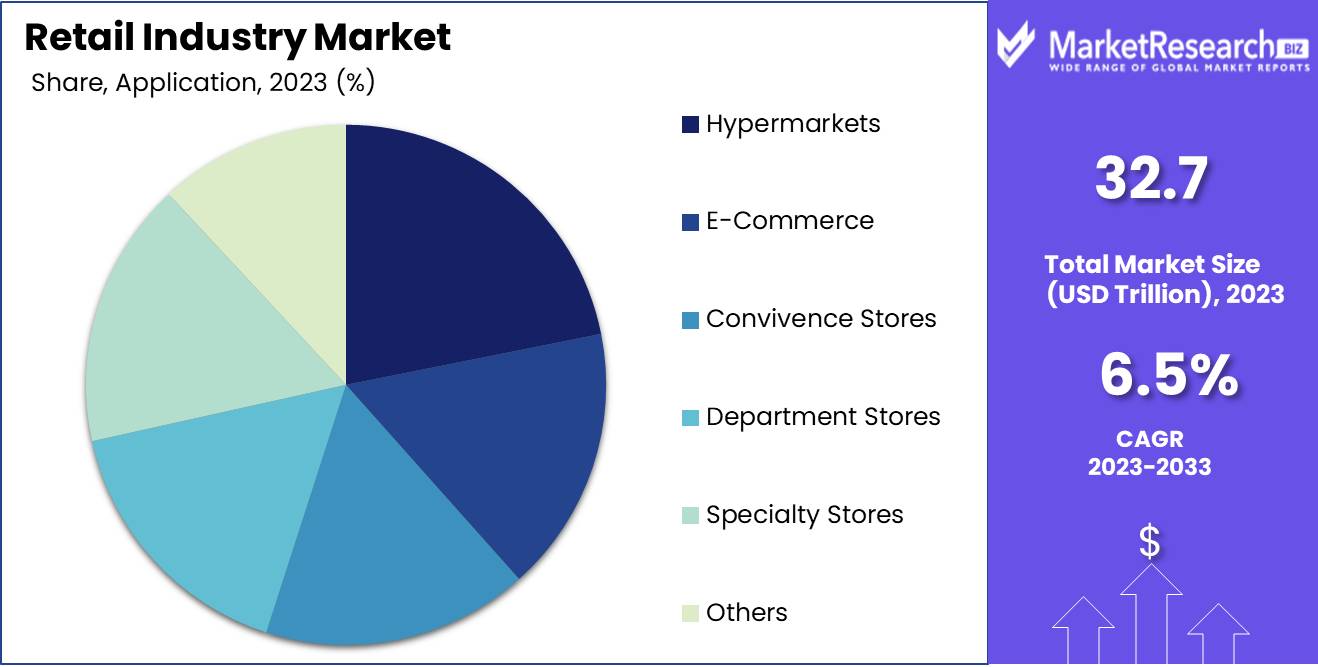

The Retail Industry Market was valued at USD 32.7 Trillion in 2023. It is expected to reach USD 60.4 Trillion by 2033, with a CAGR of 6.5% during the forecast period from 2024 to 2033.

The retail industry market encompasses the businesses and entities involved in the selling of goods and services directly to consumers. This sector includes a broad array of formats, from brick-and-mortar stores to e-commerce platforms, and covers various segments such as food and beverages, apparel, electronics, and household goods.

The retail market is characterized by its dynamic nature, driven by evolving consumer preferences, technological advancements, and shifting economic conditions. Strategic trends within this market include omnichannel retailing, personalized customer experiences, and sustainability initiatives, all aimed at enhancing competitive advantage and fostering long-term growth.

The retail industry is undergoing a profound transformation driven by technological advancements and shifting consumer behaviors. A significant trend is the increased investment in AI and automation, which is yielding remarkable outcomes. Retailers leveraging these technologies are reporting up to a 30% rise in operational efficiency and enhanced customer satisfaction. This surge in productivity is critical as the sector grapples with persistent supply chain disruptions, which continue to pose significant challenges; 55% of retailers have reported substantial operational impacts due to these disruptions. Consequently, there is a heightened emphasis on resilience and adaptability within the supply chain networks to mitigate these issues.

Digital transformation remains at the forefront of strategic initiatives in the retail sector. Global spending on digital transformation is projected to reach an astounding $1.1 trillion by 2024, underscoring the industry's commitment to integrating advanced digital solutions. This investment is crucial for maintaining competitive advantage and meeting the evolving demands of tech-savvy consumers. Retailers are focusing on enhancing their digital capabilities, from e-commerce platforms to personalized customer experiences, aiming to foster deeper customer engagement and loyalty. As these trends converge, the retail landscape is poised for a dynamic evolution, characterized by increased efficiency, resilience, and customer-centricity, ultimately driving sustainable growth and profitability in a highly competitive market.

Key Takeaways

- Market Growth: The Retail Industry Market was valued at USD 32.7 Trillion in 2023. It is expected to reach USD 60.4 Trillion by 2033, with a CAGR of 6.5% during the forecast period from 2024 to 2033.

- By Product: Pharmaceuticals dominated the retail market, driven by increased healthcare demand.

- By Distribution Channel: Hypermarkets dominated the retail market through extensive product variety.

- Regional Dominance: North America dominates retail with a 35% global market share, driving innovation.

- Growth Opportunity: Strategic geographic expansion and robust omnichannel strategies in emerging markets drive retail growth through localized offerings and integrated sales channels.

Driving factors

Economic Growth: A Catalyst for Retail Expansion

Economic growth is a fundamental driver of the retail industry market, acting as a catalyst for increased consumer spending and market expansion. As economies grow, typically measured by GDP growth, disposable incomes rise, leading to higher consumer confidence and spending power. This increased purchasing capability directly translates to higher demand for retail goods and services. Moreover, sustained economic growth often encourages investment in retail infrastructure, enhancing the shopping experience and attracting more customers.

Demographics: Shaping Retail Demand

Demographic changes significantly influence the retail market by altering consumer behavior and preferences. Key demographic factors include age distribution, population growth, and income levels. For example, the growing purchasing power of Millennials and Generation Z, who are known for their preference for online shopping and demand for sustainable products, is reshaping the retail landscape. This shift necessitates retailers to adapt their strategies to cater to these tech-savvy and environmentally conscious consumers.

Urbanization: Driving Retail Infrastructure Development

Urbanization plays a crucial role in the expansion of the retail market by concentrating populations in urban areas, thereby creating larger markets and more opportunities for retail businesses. The United Nations reports that by 2050, 68% of the world’s population will reside in urban areas, up from 55% in 2018. This migration trend drives the development of retail infrastructure, including shopping malls, retail parks, and enhanced logistics networks, facilitating greater market penetration and access to a larger customer base. Urbanization also fosters innovation in retail formats, such as the emergence of convenience stores and urban shopping centers that cater to the fast-paced lifestyle of city dwellers.

Restraining Factors

High Inflation: Eroding Consumer Purchasing Power and Margin Pressures

High inflation significantly impacts the retail industry by eroding consumer purchasing power, which directly affects consumer spending habits. When the prices of goods and services rise, consumers tend to reduce their discretionary spending, focusing primarily on essential items. This shift in spending patterns can lead to a decline in sales volumes for retailers, particularly those in non-essential or luxury segments. For instance, according to a recent survey, a 1% increase in inflation can lead to an estimated 0.5% decrease in consumer spending on non-essential goods.

Moreover, high inflation increases the cost of goods sold (COGS) for retailers due to higher prices for raw materials, production, and transportation. These increased costs can compress profit margins, especially if retailers are unable to pass on the full extent of these costs to consumers without risking further reductions in sales. This margin pressure necessitates a strategic response from retailers, such as optimizing supply chains, renegotiating supplier contracts, and enhancing operational efficiencies to maintain profitability.

Rising Interest Rates: Higher Costs of Capital and Consumer Credit Constraints

Rising interest rates have a multifaceted impact on the retail industry, primarily through increased borrowing costs and constrained consumer credit. For retailers, higher interest rates mean that the cost of financing operations, expansions, or inventory increases. This can lead to higher debt servicing costs, reducing the available capital for investment in growth initiatives such as new store openings, technological upgrades, or marketing campaigns. Data shows that a 1% increase in interest rates can raise a retailer's annual debt servicing costs by approximately 2-3%, depending on their leverage ratio.

From the consumer perspective, higher interest rates increase the cost of credit, including mortgages, car loans, and credit card debt. This can reduce disposable income and curtail spending on retail goods. The retail sectors that rely heavily on consumer financing, such as home furnishings, electronics, and automotive, are particularly vulnerable. A study highlighted that a 1% rise in interest rates could decrease consumer spending on financed goods by 3-5%.

By Product Analysis

In 2023, Pharmaceuticals dominated the retail market, driven by increased healthcare demand.

In 2023, Pharmaceuticals held a dominant market position in the by-product segment of the Retail Industry Market. This dominance is attributable to several factors. Firstly, the global healthcare landscape has seen a significant rise in the demand for medications and health supplements, driven by an aging population and increased awareness of health and wellness. The COVID-19 pandemic further accentuated the importance of pharmaceuticals, resulting in heightened consumer spending in this category. Advanced drug development technologies and the expansion of e-pharmacies have also facilitated easier access to pharmaceutical products, boosting sales.

Luxury Goods also maintained a strong presence, propelled by affluent consumers seeking high-end fashion, accessories, and personal care items. Electronic and Household Appliances witnessed steady growth, fueled by rapid technological advancements and the burgeoning trend of smart homes. The Furniture segment benefited from increased home renovation projects as remote working became more commonplace. Toys continued to capture a significant share, driven by innovative products and the growing influence of digital and educational toys. Lastly, the Others category, encompassing diverse products, showed resilient performance, adapting to changing consumer preferences and market dynamics.

By Distribution Channel Analysis

In 2023, Hypermarkets dominated the retail market through extensive product variety.

In 2023, Hypermarkets held a dominant market position in the By Distribution Channel segment of the Retail Industry Market. This supremacy is attributable to their extensive product range, competitive pricing, and the convenience of a one-stop shopping experience, which resonates strongly with consumers seeking value and variety. Hypermarkets' strategic locations in urban and suburban areas further bolster their appeal by offering easy accessibility.

Conversely, E-Commerce has emerged as a formidable contender, driven by the exponential growth of online shopping, enhanced logistics, and personalized customer experiences. Convenience Stores, valued for their proximity and extended operating hours, cater to immediate consumer needs, fostering loyalty through ease of access.

Department Stores, traditionally known for their wide array of merchandise, face challenges but remain relevant through brand differentiation and exclusive product offerings. Specialty Stores focus on niche markets, providing tailored experiences and expert knowledge that attract dedicated customer bases.

Lastly, the Others category, encompassing various retail formats, continues to innovate, integrating technology and unique value propositions to capture diverse consumer segments. Together, these channels contribute to a dynamic retail landscape, each playing a pivotal role in shaping consumer behavior and market trends.

Key Market Segments

By Product

- Pharmaceuticals

- Luxury Goods

- Electronic and Household Appliances

- Furniture

- Toys

- Others

By Distribution Channel

- Hypermarkets

- E-Commerce

- Convivence Stores

- Department Stores

- Specialty Stores

- Others

Growth Opportunity

Expanding to New Locations

The global retail industry is poised for significant growth, driven largely by strategic geographic expansion. As mature markets saturate, retailers are increasingly turning their attention to emerging economies. Regions such as Southeast Asia, Sub-Saharan Africa, and parts of Latin America offer untapped potential due to rising disposable incomes and a burgeoning middle class. According to recent studies, these areas are expected to see retail sales growth of 6-8% annually, outpacing the global average. By establishing a presence in these markets, retailers can capitalize on the demographic dividend and lower competitive intensity.

A successful expansion strategy necessitates a nuanced understanding of local consumer behaviors and preferences. Customizing product offerings to meet regional tastes, investing in local supply chains, and forging strategic partnerships with local businesses are essential steps. Moreover, adapting to varying regulatory environments and navigating logistical challenges will be crucial for sustained success.

Selling on Multiple Channels

The retail industry's shift towards omnichannel strategies continues to accelerate, with significant growth opportunities arising from the integration of physical and digital sales channels. Consumers increasingly expect a seamless shopping experience that transcends the boundaries between online and offline platforms. Retailers adopting a robust omnichannel approach can enhance customer engagement, increase brand loyalty, and drive sales growth.

Data shows that omnichannel customers have a 30% higher lifetime value compared to single-channel shoppers. By leveraging technologies such as AI and data analytics, retailers can gain deeper insights into consumer behavior, personalize marketing efforts, and optimize inventory management across channels. Additionally, the integration of mobile commerce, social media shopping, and click-and-collect services is becoming imperative.

Latest Trends

Hybrid Shopping: Seamless Integration of Online and Offline Channels

The retail industry is witnessing a significant evolution with the rise of hybrid shopping. This model combines the convenience of online shopping with the tactile experience of physical stores, creating a seamless customer journey. Retailers are increasingly leveraging technology to blur the lines between digital and brick-and-mortar environments. Innovations such as buy-online-pickup-in-store (BOPIS), curbside pickups, and integrated mobile apps are becoming standard. These hybrid solutions not only enhance customer convenience but also drive foot traffic to physical stores, fostering a holistic retail ecosystem. Retailers adopting these practices are better positioned to meet the dynamic needs of modern consumers, who demand flexibility and efficiency in their shopping experiences.

AI and Personalization: Tailoring Experiences Through Advanced Analytics

Artificial intelligence (AI) is revolutionizing the retail sector by enabling unprecedented levels of personalization. AI-driven personalization is not just an add-on but a core component of retail strategies. Retailers are using AI to analyze vast amounts of data, from purchase history to browsing behavior, to deliver highly customized experiences. Personalized recommendations, dynamic pricing, and targeted marketing campaigns are some of the ways AI is enhancing customer engagement. This tailored approach not only improves customer satisfaction but also boosts sales and loyalty. Retailers who invest in AI technologies can offer more relevant product suggestions, streamline operations, and create a competitive edge in an increasingly crowded market.

Regional Analysis

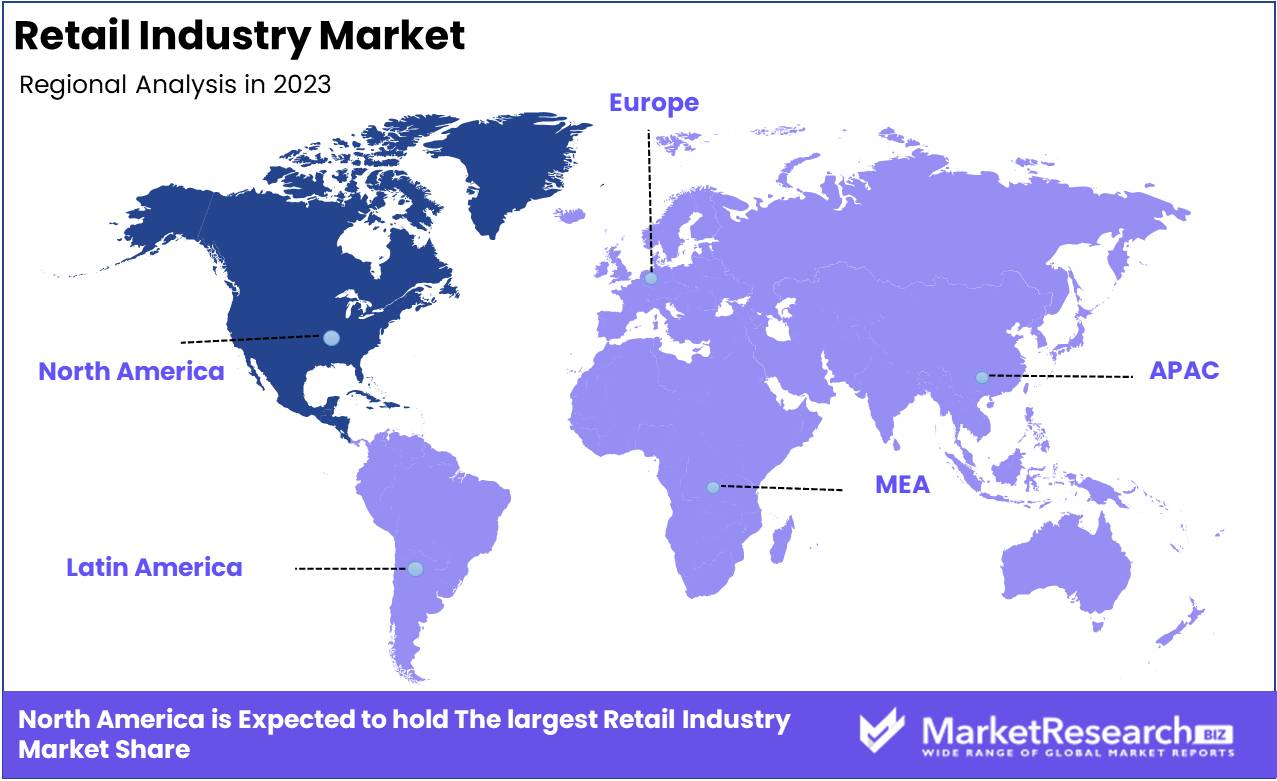

North America dominates retail with a 35% global market share, driving innovation.

The global retail industry showcases distinct regional dynamics shaped by varying economic landscapes, consumer behaviors, and technological advancements. North America, dominated by the United States, leads the market with a robust retail infrastructure and advanced e-commerce penetration, accounting for approximately 35% of the global retail market share. The region's retail sales exceeded $5.5 trillion in 2023, driven by strong consumer spending and digital transformation initiatives.

Europe, comprising major economies like Germany, the UK, and France, represents around 25% of the global market. The region's retail sector is characterized by a mix of traditional brick-and-mortar stores and a rapidly growing online retail segment, with e-commerce accounting for over 15% of total retail sales in 2023.

The Asia Pacific region, led by China, Japan, and India, holds a significant 30% share of the global market. China's retail sales alone surpassed $6 trillion in 2023, propelled by urbanization, rising disposable incomes, and a burgeoning middle class. E-commerce growth is particularly noteworthy, with platforms like Alibaba and JD.com driving substantial sales volumes.

The Middle East & Africa region, while smaller in comparison, is experiencing rapid growth, particularly in the Gulf Cooperation Council (GCC) countries. The region's retail market is valued at over $1 trillion, with increasing investments in retail infrastructure and a youthful, tech-savvy population contributing to growth.

Latin America, with Brazil and Mexico at the forefront, holds around 10% of the global market share. The region is witnessing a steady increase in retail sales, driven by economic stabilization efforts and a growing e-commerce sector. Brazil's retail market alone was valued at approximately $600 billion in 2023, reflecting positive consumer sentiment and market expansion.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global retail industry market is expected to be shaped by the strategic maneuvers and competitive dynamics among key players such as Best Buy Co. Inc., Walmart Inc., Metro Group AG, Carrefour SA, The Kroger Company, The Home Depot Inc., Tesco, Alibaba Group Holding Limited, Amazon.com Inc., Costco Wholesale Corporation, Inter Ikea Systems BV, and Target Corporation.

Walmart Inc. and Amazon.com Inc. continue to dominate the market, leveraging their extensive logistics networks and innovative technology solutions to enhance customer experience and streamline operations. Walmart's strategic investments in omnichannel capabilities and Amazon's continued expansion into grocery and physical retail exemplify their aggressive market positioning.

Alibaba Group Holding Limited remains a formidable player in the Asian markets, with its robust e-commerce ecosystem and integration of offline and online retail channels. The company's focus on artificial intelligence and big data analytics provides a competitive edge in personalizing consumer experiences.

Costco Wholesale Corporation and The Home Depot Inc. exemplify strength in niche markets, with Costco's membership-based model fostering customer loyalty and The Home Depot's emphasis on home improvement catering to a growing DIY market.

European giants such as Tesco and Carrefour SA are focusing on sustainability and local market adaptation to maintain their market share, while Best Buy Co. Inc. and Target Corporation emphasize personalized customer service and in-store experiences.

Market Key Players

- Best Buy Co. Inc.

- Walmart Inc.

- Metro Group AG

- Carrefour SA

- The Kroger Company

- The Home Depot Inc.

- Tesco

- Alibaba Group Holding Limited

- Amazon.Com Inc.

- Costco Wholesale Corporation

- Inter Ikea Systems BV

- Target Corporation

- others

Recent Development

- In April 2024, Walmart unveiled a major investment in AI and automation technologies to streamline its supply chain and improve in-store operations. This includes deploying more AI-driven inventory management systems and increasing the use of autonomous delivery vehicles, reflecting Walmart's commitment to leveraging technology to maintain competitive advantage.

- In March 2024, Amazon announced the opening of several new Amazon Fresh grocery stores across the United States, expanding its footprint in the physical retail space. This move aims to blend their digital expertise with in-person shopping experiences, leveraging their advanced technology to enhance customer convenience and operational efficiency.

- In February 2024, Target expanded its same-day delivery service, partnering with Shipt and introducing new delivery hubs in key metropolitan areas. This initiative aims to cater to the growing consumer demand for rapid delivery, enhancing customer satisfaction and loyalty through improved service efficiency.

Report Scope

Report Features Description Market Value (2023) USD 32.7 Trillion Forecast Revenue (2033) USD 60.4 Trillion CAGR (2024-2032) 6.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Pharmaceuticals, Luxury Goods, Electronic and Household Appliances, Furniture, Toys, Others), By Distribution Channel (Hypermarkets, E-Commerce, Convivence Stores, Department Stores, Specialty Stores, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Best Buy Co. Inc., Walmart Inc., Metro Group AG, Carrefour SA, The Kroger Company, The Home Depot Inc., Tesco, Alibaba Group Holding Limited, Amazon.Com Inc., Costco Wholesale Corporation, Inter Ikea Systems BV, Target Corporation, others Customization Scope Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Best Buy Co. Inc.

- Walmart Inc.

- Metro Group AG

- Carrefour SA

- The Kroger Company

- The Home Depot Inc.

- Tesco

- Alibaba Group Holding Limited

- Amazon.Com Inc.

- Costco Wholesale Corporation

- Inter Ikea Systems BV

- Target Corporation

- others

Our Clients

View Our Licence Options