Global Virtual Reality (VR) In Healthcare Market Size, Share, Growth, And Industry Analysis By Application (Medical Training and Education, and others), Technology (Augmented Reality (AR), Virtual Reality (VR)), And By Region Forecast - 2023-2032

-

41141

-

Sep 2023

-

150

-

-

This report was compiled by Correspondence Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

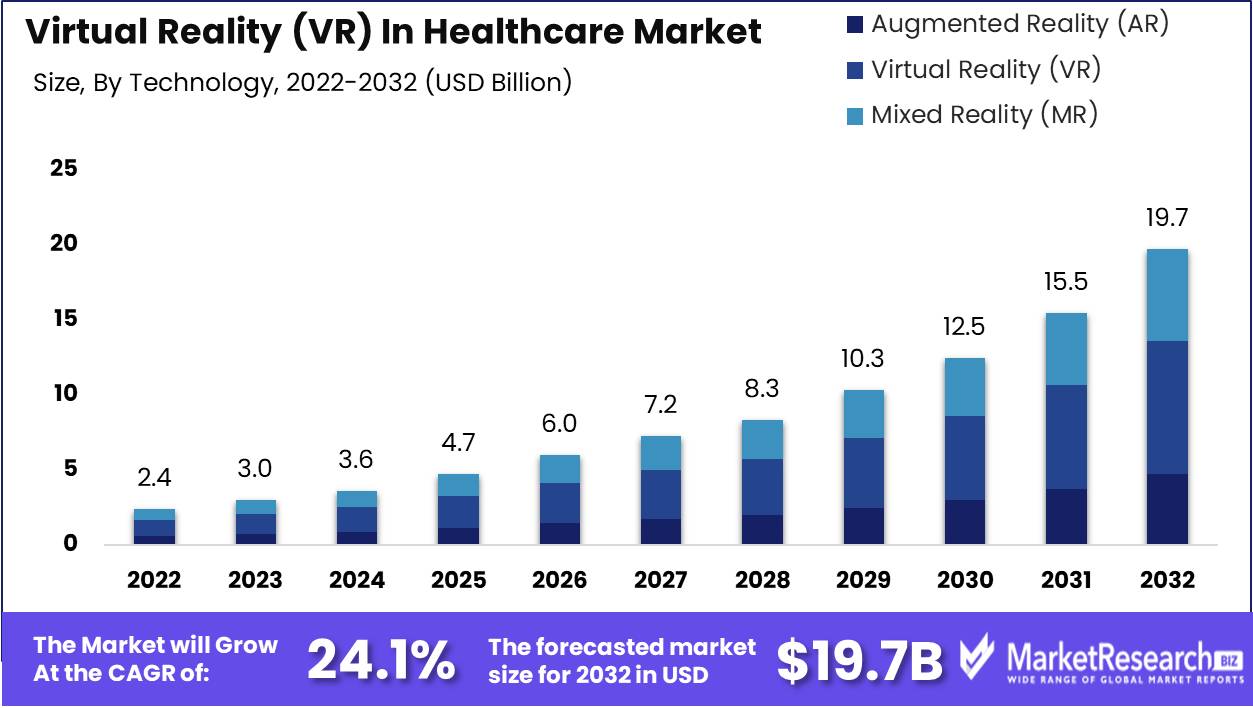

The global Virtual Reality (VR) in healthcare market revenue is expected to increase to USD 19.7 Bn in 2032 from USD 2.4 Bn in 2022, and register a revenue CAGR of 24.1% during the forecast period (2023 to 2032).

Some Key Takeaways

- The global Virtual Reality (VR) in healthcare market is registering a substantially rapid growth rate and was valued at approximately USD 2.4 billion in 2022. Revenue is projected to exceed USD 4.7 billion by the end of 2025, and the market is expected to register a robust Compound Annual Growth Rate (CAGR) of around 24.1% over the forecast period.

- North America continues to account for dominant revenue contribution to the global Virtual Reality (VR) In Healthcare Market and is expected to register a revenue CAGR of around 28.7% over the forecast period.

- Asia Pacific market is expected to retain dominance for fastest revenue growth rate over the forecast period, which can be attributed to the large population and a growing base of healthcare providers and consumers seeking to modernize healthcare offerings and integrate more advanced technologies.

- In 2022, a remarkable 45% increase in utilization of AI-powered diagnostic tools was noted and this is attributed to continuous evolution of VR technology, including advancements in AI diagnostics, telehealth platforms, and remote monitoring devices.

- According to survey findings in 2022, around 58% of healthcare professionals preferred VR-based simulations for medical training and surgical planning due to their effectiveness and immersive nature.

- VR in healthcare has significantly improved access to medical care. In 2023, more than 50% of telehealth consultations took place in underserved rural areas, demonstrating its potential to bridge healthcare disparities and bring quality healthcare to remote regions.

Market Overview

Virtual Reality (VR) has been gaining significant traction within the healthcare sector, and the technology enables further development of an expanding range of innovative solutions for use for education in the medical field, treatment of patients, and for improved diagnostic processes. VR, immersive VR, Augmented Reality (AR), and Mixed Reality (MR) have been gaining wide popularity and rising preference in applications such as medical training, surgical planning and preparation, and also in patient therapy. VR has been playing a major role in healthcare services and is applied to surgical simulations, patient rehabilitation, mental health therapy, and remote consultations, among others.

The global Virtual Reality (VR) In Healthcare Market is expected to continue to account for a significantly rapid revenue growth rate of over 30% over the forecast period. Some key drivers include high demand for immersive training experiences for medical professionals, patient engagement through VR therapy, and the need for remote consultations, especially post-pandemic.

Consumption trends indicate a rising preference for VR-based surgical simulations, pain management, and therapy solutions. Advances in VR technology such as haptic feedback and 3D visualization are serving to enhance user experience, and this coupled with various initiatives to promote adoption of VR in healthcare applications and government and private organizations investing in research and development are other key factors.

The advantages of VR in healthcare encompass improved training, reduced anxiety in patients, and enhanced diagnostics. Detailed analysis and insights highlight a promising future for this transformative technology in the healthcare sector.

Driving Factors

Increased Adoption of Telemedicine

Growing acceptance of telemedicine, especially post-COVID-19 pandemic, is driving demand for VR in healthcare. VR technology facilitates immersive remote consultations, thereby improving patient engagement and expanding revenue potential for players operating in the market.

Enhanced Medical Training and Education

VR offers realistic surgical simulations and interactive educational tools, enabling healthcare professionals to hone their skills and knowledge. This also enables development of a better-trained workforce, ultimately leading to improved patient care and increased revenue.

Rising Prevalence of Chronic Diseases

Global incline in prevalence of chronic diseases is necessitating development and use of more innovative treatment approaches. VR-based therapies and pain management solutions continue to gain traction, owing to results such as leading to improved patient outcomes.

Investments in R&D

Ongoing investments by both public and private sectors in VR technology is a major factor driving advancements in VR technology and expanding end-uses and applications. Also, development of more sophisticated VR hardware and software tailored to the healthcare sector is expected to support market growth to a major extent.

Patient-Centric Approach

VR is proving to be game-changer in healthcare applications and enhances patient experience by reducing anxiety during some procedures and providing non-pharmacological pain management. Such as patient-centric focus improves outcomes, as well as has an overly positive impact on preference among patients and healthcare providers and experts in medical fields, and this is another key factor supporting revenue growth.

Restraining Factors

High Initial Costs

key factor expected to restrain revenue growth of the market is the substantial initial investment required for VR hardware and software implementation in healthcare facilities. This factor can limit budget constrained healthcare providers from adopting VR technology, thereby restraining potential market revenue.

Regulatory Hurdles

Need for stringent compliance and presence of norms and regulations in the healthcare industry, and navigating these regulations for VR applications can be complex and time-consuming. Compliance with stringent data privacy and patient safety standards can also delay adoption of VR solutions, and have a negative impact on market revenue growth.

Limited Content Development

The scarcity of high-quality, medically validated VR content hinders wider adoption of VR in healthcare. Developing accurate and effective VR simulations and therapies is time consuming, critical, and takes up resources. This is another major factor causing sluggish market expansion and revenue growth.

Opportunities

Content Development Services

Offering of specialized content development services for VR applications in healthcare is a strategy that can open up revenue opportunities for companies operating in the market. Development of high-quality, medically accurate simulations, training modules, and therapy programs can also create lucrative revenue streams as healthcare providers seek customized VR content to enhance patient care and medical training.

Telehealth Integration Solutions

Rising demand for telemedicine presents significant opportunity for companies to develop VR solutions that seamlessly integrate with telehealth platforms. This can enhance the virtual healthcare experience, and provide added value to offerings of healthcare providers.

Hardware and Software Sales

Hardware costs can be a major barrier to entry, so companies can generate revenue by developing and offering VR hardware and software tailored specifically for healthcare settings and applications. Innovations in VR headset technology and medical-grade software can serve to leverage substantial increase in market share as healthcare facilities upgrade equipment and infrastructure, and the modernization trend continues to remain at the forefront of patient care and education in a number of developed and developing economies.

Segment Analysis

By Application

The medical training and education segment accounted for a substantially large revenue share in the global Virtual Reality (VR) In Healthcare Market in 2022. Some key factors driving growth of this segment are increasing demand for immersive and realistic training experiences for medical professionals and continuous advancements in VR technology.

An increasing number of healthcare institutions and medical schools are steadily adopting VR-based simulations and interactive modules for surgical and diagnostic training, thus reducing the need for physical cadavers and offering a safe, cost-effective, and repeatable training environment. As VR technology evolves with haptic feedback and real-time feedback mechanisms, it further enhances the effectiveness of medical training, and such advancements are contributing significantly to revenue growth.

By Technology

Virtual reality segment among the technology segments accounted for a significantly large revenue share in 2022. Growing adoption of VR in telemedicine and the development of VR content tailored to healthcare needs, coupled with increasing number of telemedicine providers integrating VR into their platforms to offer immersive remote consultations and therapy sessions, particularly in mental health, are driving market revenue growth. Also, the creation of medically validated VR content, such as 3D anatomical models and surgical simulations, is driving demand. These factors, coupled with increasing affordability and accessibility of VR hardware, are contributing to high revenue share of the VR segment.

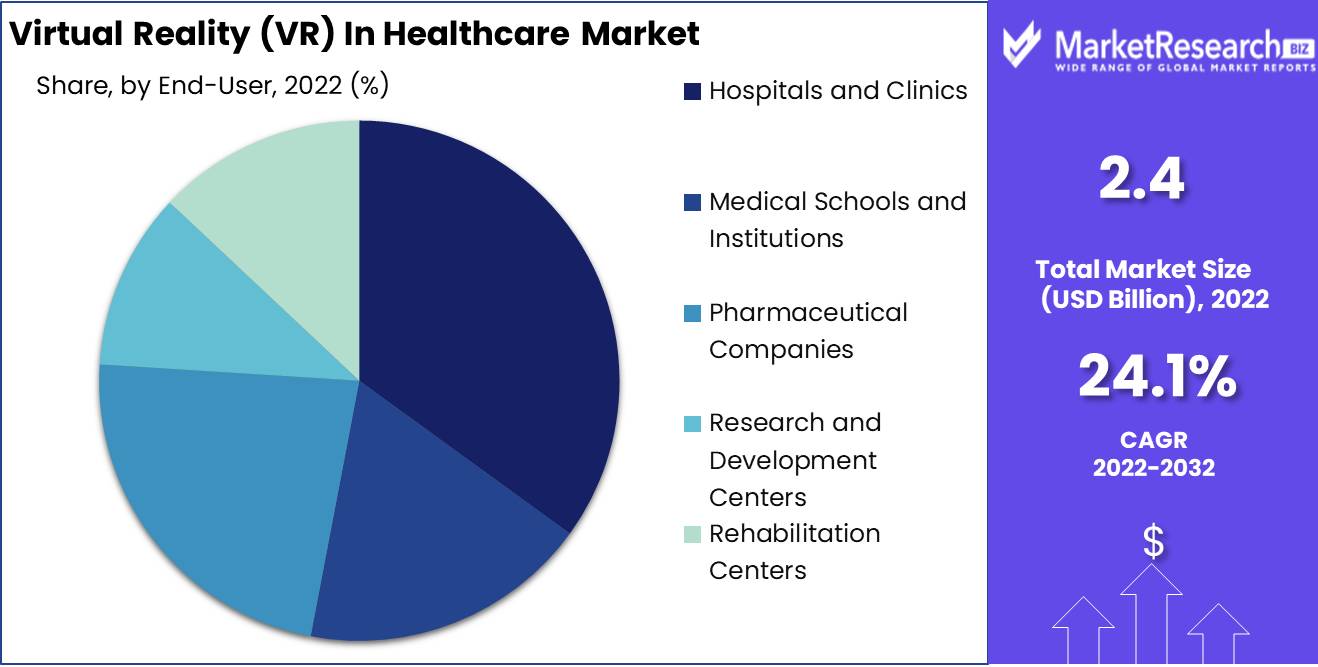

End-User

Among the end-user segments the hospitals and clinics segment accounted for largest share of revenue. Increasing utilization of VR for surgical planning and simulations within hospital settings, and rising demand for VR-based patient therapies, are primary factors driving revenue growth of this segment. Surgical teams are adopting VR for preoperative planning, reducing errors and enhancing patient outcomes. Moreover, VR therapies for pain management and rehabilitation are becoming more prevalent in clinical settings, improving patient satisfaction and recovery rates.

Market Segmentation

By Application

- Medical Training and Education

- Pain Management and Therapy

- Surgical Simulations

- Patient Rehabilitation

- Cognitive Rehabilitation

Technology

- Augmented Reality (AR)

- Virtual Reality (VR)

- Mixed Reality (MR)

End-User

- Hospitals and Clinics

- Medical Schools and Institutions

- Pharmaceutical Companies

- Research and Development Centers

- Rehabilitation Centers

Content Type

- 3D Models and Anatomy Visualization

- Interactive Modules and Simulations

- Therapeutic VR Programs

- Diagnostic VR Tools

- Training and Procedure Walkthroughs

Component

- Hardware

- VR Headsets

- Haptic Devices

- Software

- VR Applications

- Simulation Software

- Services

- Content Development

- Consulting

- Accessories

- Controllers

- Sensors

- Maintenance and Support

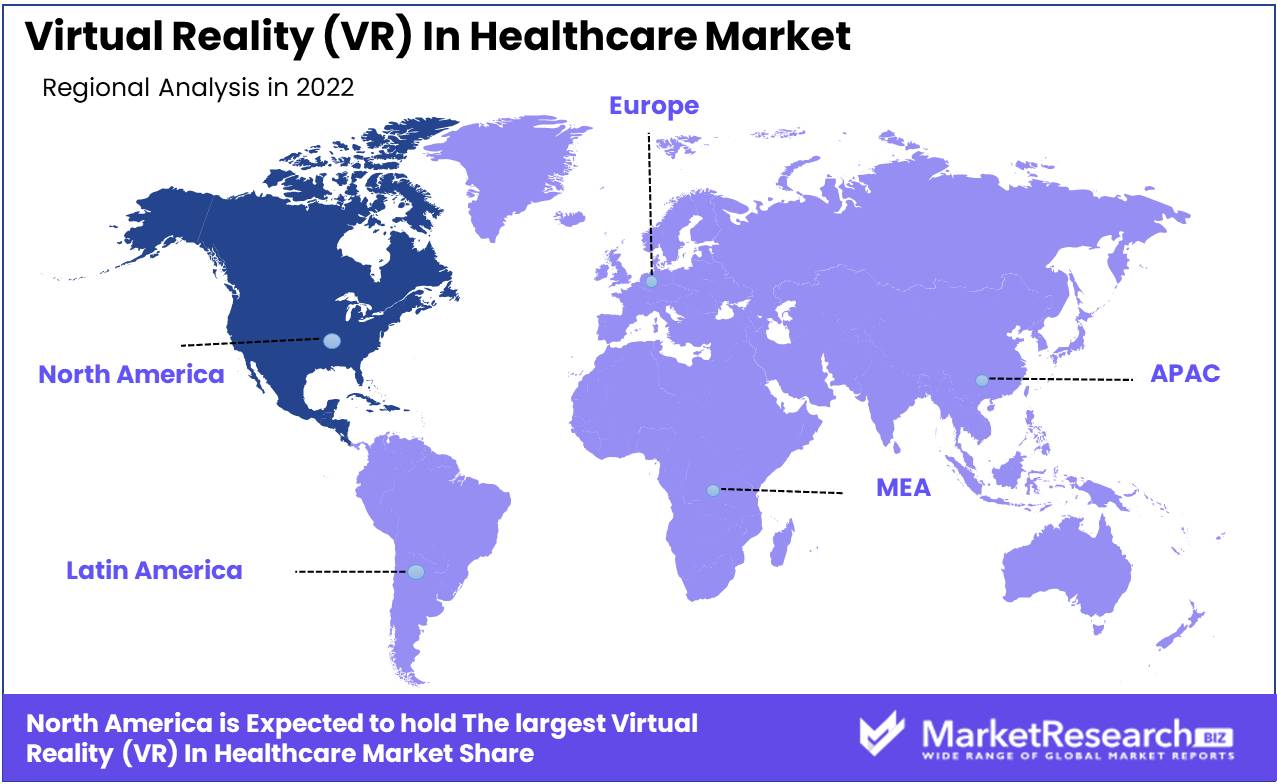

Regional Analysis

North America

North America accounted for largest market share in the global Virtual Reality (VR) In Healthcare Market in 2022, and this can be attributed to presence of advanced healthcare infrastructure and robust adoption of advanced technologies and solutions in countries in the region. Increasing investments in VR for medical training, telemedicine integration, and pain management, and technological advancements on development of more advanced VR headsets and software are other key factors expected to continue to drive market revenue growth. Initiatives such as public-private partnerships and funding for VR research are also supporting revenue growth, with the U.S. accounting for substantially larger revenue share among the countries.

Europe

Europe follows closely behind North America in terms of market share and revenue potential. The region is witnessing steady industry growth as VR makes major headway into the healthcare sector and are being considered crucial for surgical simulations, telehealth applications, and patient rehabilitation. Technological advancements in VR content and hardware are also factors supporting market revenue growth. Government initiatives, particularly in countries such as the UK and Germany, are driving investments in healthcare VR, and creating a conducive environment for revenue growth.

Asia-Pacific

Asia-Pacific represents a rapidly expanding market for VR in healthcare, with significant revenue growth potential. The region is registering a rapid market revenue growth rate, driven by robust industry expansion and modernization, rising healthcare investments, and increasing awareness of VR benefits. Technological advancements are being driven by companies in countries such as China, Japan, and South Korea. Government initiatives to improve healthcare infrastructure and technology adoption are further supporting revenue growth.

Latin America

Latin America is emerging as a lucrative market for VR in healthcare, with untapped potential to be addressed. Steady growth can be expected as healthcare providers recognize the value of VR for medical education and patient therapy. Technological advancements in VR content creation are contributing to market expansion. Initiatives aimed at improving healthcare access and quality in the region are expected to create lucrative revenue growth opportunities.

Middle East & Africa

Interest in VR for healthcare applications are gaining traction across the sector in the Middle East and Africa. Industry growth potential is significant, especially as VR becomes more integrated into medical training and telemedicine. Technological developments in VR hardware are driving market expansion. Initiatives to enhance healthcare services, including telehealth programs, in untapped regions is expected to support revenue growth.

Segmentation By Region

North America

- United States

- Canada

Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- Association of Southeast Asian Nations (ASEAN)

- Rest of Asia Pacific

Europe

- Germany

- The U.K.

- France

- Spain

- Italy

- Russia

- Poland

- BENELUX (Belgium, the Netherlands, Luxembourg)

- NORDIC (Norway, Sweden, Finland, Denmark)

- Rest of Europe

Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Israel

- Rest of MEA (Middle East & Africa)

Competitive Landscape

The landscape in the global VR in healthcare market is highly competitive and characterized by a mix of established tech giants, innovative startups, and specialized service providers. These companies are focused on leveraging majority market share and deploying various strategies and approaches to remain ahead in the rapidly growing market.

Companies are entering into strategic agreements, leveraging each other’s technology and hardware to maintain a robust presence in the market, and creating much-needed content for pain management applications and therapeutics to drive sales and revenues.

For instance, Oculus VR (a subsidiary of Meta Platforms, Inc.), remains a major player, and offers VR hardware and software solutions for healthcare applications. The company has the backing of Meta Platforms (formerly Facebook), and Oculus also has a strong market presence and extensive resources to develop VR technologies for healthcare.

Also, HTC Corporation, known for its Vive VR headset, has been actively engaged in the healthcare VR market. The company has entered into partnerships with various healthcare institutions to provide VR solutions for medical training and patient therapy. Providing the necessary needs for training in the healthcare sector is another major strategy being adopted by companies.

For example, Medtronic plc, which is a global leader in medical technology, has been leveraging VR for surgical training and healthcare simulations. The company’s commitment to enhancing medical education through VR positions it as a key player.

In addition, AppliedVR, Inc. specializes in creating VR content and platforms for pain management and therapeutic purposes. The company has gained recognition for immersive VR solutions aimed at alleviating chronic pain and reducing the need for pharmaceutical interventions. Other companies are focused intently on developing and offering telehealth services, providing VR-based therapy and remote patient monitoring.

Furthermore, Surgical Theater, LLC. specializes in surgical simulations and 360-degree virtual reality for preoperative planning. The company’s immersive VR technology assists surgeons in better understanding and preparing for complex procedures.

Company List

- Oculus VR

- HTC Corporation

- Sony Corporation

- Samsung Electronics Co., Ltd.

- Google LLC

- Medtronic plc

- AppliedVR, Inc.

- Osso VR, Inc.

- ImmersiveTouch Inc.

- Surgical Theater, LLC

- VirtaMed AG

- Psious

- Oculus Surgical

- MindMaze

- Firsthand Technology

- Touch Surgery

- FundamentalVR

- XRHealth

- Embodied Labs

- Vicarious Surgical

Recent Developments

- In May 2022, PrecisionOS announced teaming up with Medtronic Saudi Arabia and expanding its VR training offerings into general surgery. The company is a leading provider of surgeon education, and offers training for complex soft tissue surgery on a portable VR solution, the Meta Quest.

- Medtronic unveiled a virtual reality surgical training program designed to enhance the skills of medical professionals. It provides realistic simulations for practicing complex surgical procedures.

- Oculus, which is a subsidiary of Meta Platforms, has recently introduced ‘Oculus for Healthcare’. This new product is a suite of VR solutions specifically designed for medical and healthcare applications and includes VR tools for training, therapy, and patient engagement.

- In November 2021, XRHealth, which is a leader in the extended reality telehealth therapeutic market, announced the launch of a crowdfunding campaign offering stock in its pioneering Virtual Clinics. Through these clinics, the company provides at-home medical treatments through VR/AR and digital health technologies. The platform serves to integrate licensed clinicians and allows access to advanced data analytics.

- In 2020, AppliedVR introduced a virtual reality-based pain management platform that offers personalized therapy for chronic pain sufferers. It utilizes immersive VR experiences to help patients manage pain effectively.

Report Scope

Report Features Description Market Value (2022) USD 2.4 Bn Forecast Revenue (2032) USD 19.7 Bn CAGR (2023-2032) 24.1% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Application (Medical Training and Education, Pain Management and Therapy, Surgical Simulations, Patient Rehabilitation, Cognitive Rehabilitation), Technology (Augmented Reality [AR], Virtual Reality [VR], Mixed Reality [MR]), End-User (Hospitals and Clinics, Medical Schools and Institutions, Pharmaceutical Companies, Research and Development Centers, Rehabilitation Centers), Content Type (3D Models and Anatomy Visualization, Interactive Modules and Simulations, Therapeutic VR Programs, Diagnostic VR Tools, Training and Procedure Walkthroughs), Component (Hardware, Software, Services, Accessories, Maintenance and Support) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Oculus VR, HTC Corporation, Sony Corporation, Samsung Electronics Co., Ltd., Google LLC, Medtronic plc, AppliedVR, Inc., Osso VR, Inc., ImmersiveTouch Inc., Surgical Theater, LLC, VirtaMed AG, Psious, Oculus Surgical, MindMaze, Firsthand Technology, Touch Surgery, FundamentalVR, XRHealth, Embodied Labs, Vicarious Surgical Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Oculus VR

- HTC Corporation

- Sony Corporation

- Samsung Electronics Co., Ltd.

- Google LLC

- Medtronic plc

- AppliedVR, Inc.

- Osso VR, Inc.

- ImmersiveTouch Inc.

- Surgical Theater, LLC

- VirtaMed AG

- Psious

- Oculus Surgical

- MindMaze

- Firsthand Technology

- Touch Surgery

- FundamentalVR

- XRHealth

- Embodied Labs

- Vicarious Surgical

Our Clients

View Our Licence Options