Sterile Injectable Drugs Market By Type (Small Molecule, Large Molecule), By Therapeutic Application (Cancer, Diabetes, Cardiovascular Diseases, Infectious Disorders, Central Nervous Systems, Musculoskeletal, Anti-Viral, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

47392

-

June 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

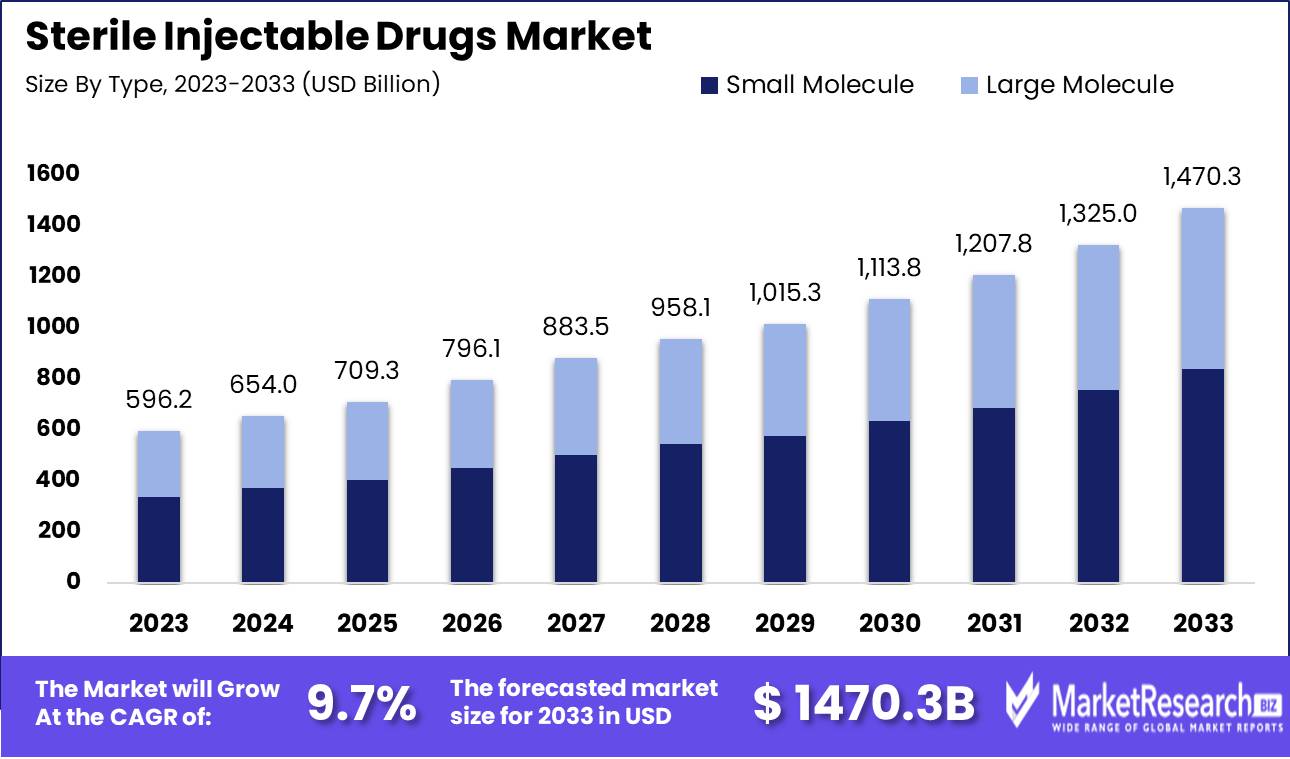

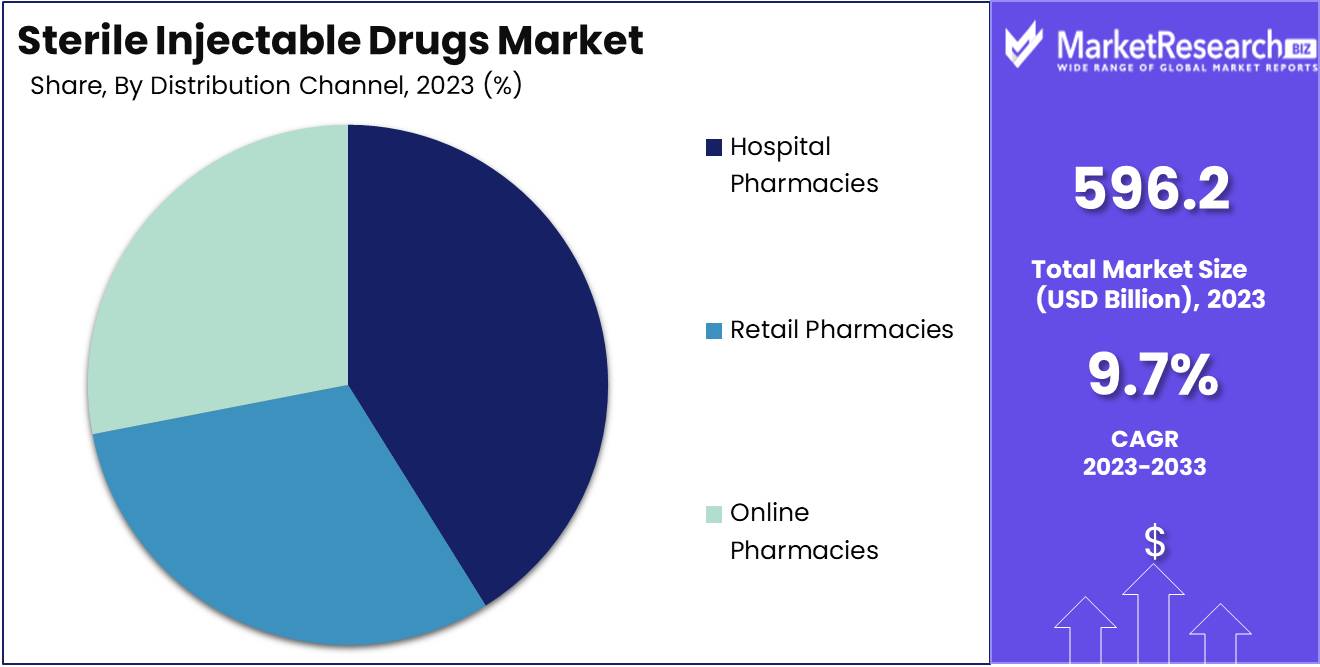

The Sterile Injectable Drugs Market was valued at USD 596.2 billion in 2023. It is expected to reach USD 1470.3 billion by 2033, with a CAGR of 9.7% during the forecast period from 2024 to 2033.

The Sterile Injectable Drugs Market encompasses the development, production, and distribution of injectable medications that are free from microbial contaminants, ensuring patient safety and therapeutic efficacy. These drugs are critical for treating various medical conditions, including chronic diseases, cancers, and infections, due to their rapid onset of action and high bioavailability.

The market is driven by advancements in biologics, the increasing prevalence of chronic diseases, and the growing demand for personalized medicine. Regulatory standards and technological innovations in manufacturing processes are pivotal in maintaining sterility and quality, ensuring the safe administration of these essential therapeutics.

The sterile injectable drugs market is experiencing significant growth, driven by several key factors that align with broader trends in healthcare and pharmaceutical innovation. As the prevalence of chronic diseases such as cancer, diabetes, and cardiovascular conditions continues to rise globally, the demand for effective and reliable injectable treatments has surged. These diseases often require long-term management and targeted therapies, making sterile injectables an essential component of modern medical practice. Furthermore, the market is benefiting from the emergence of advanced drug delivery systems, such as pre-filled syringes and auto-injectors, which offer enhanced convenience, improved patient compliance, and reduced risk of contamination. These innovations are particularly important in the context of biologics, where precision and sterility are paramount.

In addition to these drivers, the continued innovation and advancements in biologics are poised to propel the market further. Biologics represent a significant segment of the pharmaceutical industry, characterized by complex molecules that are often sensitive to environmental conditions. The sterile injectable format is ideal for these drugs, ensuring their stability and efficacy. As research and development in this field advance, we can expect a steady stream of new biologic therapies entering the market, each requiring sterile injectable solutions. This trend underscores the critical role of technological advancements and the ongoing evolution of pharmaceutical manufacturing processes.

In summary, the sterile injectable drugs market is on a robust growth trajectory, supported by increasing chronic disease prevalence, technological innovations in drug delivery, and the dynamic progress in biologic therapies. This confluence of factors suggests a vibrant future for stakeholders within this sector, necessitating strategic investments in R&D and production capabilities to meet the rising demand.

Key Takeaways

- Market Growth: The Sterile Injectable Drugs Market was valued at USD 596.2 billion in 2023. It is expected to reach USD 1470.3 billion by 2033, with a CAGR of 9.7% during the forecast period from 2024 to 2033.

- By Type: Small Molecule dominated the Sterile Injectable Drugs Market.

- By Therapeutic Application: Cardiovascular Diseases dominated the Sterile Injectable Drugs Market.

- By Distribution Channel: Hospital Pharmacies dominated sterile injectable drug distribution channels.

- Regional Dominance: Asia Pacific leads the sterile injectable drugs market with a 35% share.

- Growth Opportunity: The sterile injectable drugs market will grow due to biotech advancements and expanded healthcare infrastructure.

Driving factors

Rising Prevalence of Chronic Diseases Fuels Demand for Sterile Injectable Drugs

The global increase in chronic diseases such as diabetes, cancer, and cardiovascular diseases is a significant driver for the sterile injectable drugs market. According to the World Health Organization (WHO), chronic diseases are the leading cause of death and disability worldwide, accounting for approximately 71% of all deaths globally. This rise in chronic conditions necessitates long-term treatment regimens, often involving sterile injectable drugs, which are crucial for delivering precise dosages and maintaining efficacy over extended periods. The increased need for effective management of chronic diseases, coupled with a growing aging population susceptible to these conditions, directly propels the demand for sterile injectable therapeutics, ensuring steady market growth.

Growing Demand for Biologics Accelerates Market Expansion

Biologics, which include a wide range of products such as vaccines, blood components, and gene therapies, represent a rapidly expanding segment of the pharmaceutical industry. The preference for biologics is driven by their efficacy in treating complex conditions that traditional small-molecule drugs cannot address effectively. The global biologics market was valued at approximately $375 billion in 2020 and is expected to grow at a compound annual growth rate (CAGR) of 8-9% through 2027. This surge in demand for biologics directly impacts the sterile injectable drugs market, as these products require sterile formulations to ensure safety and effectiveness. Biologics' growth not only enhances the market for sterile injectables but also drives innovation and development in drug delivery systems, further bolstering market expansion.

Increased Outsourcing Activities Optimize Production and Distribution

Pharmaceutical companies are increasingly outsourcing the manufacturing of sterile injectable drugs to specialized contract manufacturing organizations (CMOs). This trend is driven by the need to reduce operational costs, access advanced technologies, and meet stringent regulatory requirements. According to industry reports, the global pharmaceutical contract manufacturing market is expected to grow from $103.1 billion in 2021 to $168.2 billion by 2026, at a CAGR of 10%. Outsourcing enables pharmaceutical companies to leverage the expertise of CMOs in sterile manufacturing, ensuring high-quality production while focusing on core competencies such as research and development. The increased reliance on CMOs enhances the scalability and efficiency of sterile injectable drug production, facilitating timely market entry and meeting the growing global demand.

Restraining Factors

Regulatory Hurdles and Quality Control Measures Impede Market Expansion

Stringent regulations and quality control measures are pivotal in ensuring the safety and efficacy of sterile injectable drugs. However, these stringent requirements pose significant challenges for market growth. The complex and rigorous approval processes mandated by regulatory bodies like the FDA (Food and Drug Administration) and EMA (European Medicines Agency) demand extensive documentation, prolonged testing phases, and adherence to high standards of manufacturing practices. This often results in substantial delays in product approvals and market entry.

Moreover, maintaining compliance with these regulations incurs continuous costs related to monitoring, audits, and potential modifications in manufacturing processes. For instance, any deviation or quality lapse can lead to product recalls, legal liabilities, and loss of market trust, thereby exacerbating financial burdens. As a result, smaller pharmaceutical companies might struggle to meet these requirements, limiting their ability to compete and innovate in the market. This regulatory environment, while critical for patient safety, inadvertently restrains the pace of market growth by imposing heavy operational constraints on market participants.

Elevated Development Costs Stifle Market Innovation

The high costs associated with the development of sterile injectable drugs present another substantial barrier to market growth. Developing these drugs involves a series of intricate and resource-intensive steps, including initial research, clinical trials, manufacturing, and distribution. According to industry reports, the development cost for bringing a new injectable drug to market can exceed $2.6 billion, encompassing expenses related to R&D, regulatory compliance, and post-marketing surveillance.

These financial demands are particularly challenging for smaller biotech firms and startups, which often rely on external funding to sustain their operations. The substantial investment required not only limits the entry of new players into the market but also hinders the ability of existing companies to diversify their product portfolios.

By Type Analysis

In 2023, Small Molecule dominated the Sterile Injectable Drugs Market.

In 2023, Small Molecule held a dominant market position in the By Type segment of the Sterile Injectable Drugs Market. This leadership is attributed to the extensive utilization of small molecule injectables in treating a broad range of diseases, including cardiovascular, oncological, and infectious diseases. Their well-established efficacy, affordability, and simpler manufacturing processes compared to large molecules have solidified their market dominance. Furthermore, the rapid approval rates for small molecule drugs by regulatory authorities have facilitated their swift market penetration.

Conversely, the Large Molecule segment is witnessing significant growth, driven by advancements in biotechnology and the increasing prevalence of chronic diseases like diabetes and autoimmune disorders. Large molecules, or biologics, offer targeted therapeutic effects, which are particularly beneficial in personalized medicine. Despite their higher costs and complex manufacturing processes, their potential for high specificity and efficacy in treatment provides substantial value. As biopharmaceutical innovations continue to evolve, large molecules are poised to capture an increasing share of the market, complementing the established presence of small molecules and enhancing the overall therapeutic landscape of sterile injectable drugs.

By Therapeutic Application Analysis

In 2023, Cardiovascular Diseases dominated the Sterile Injectable Drugs Market.

In 2023, Cardiovascular Diseases held a dominant market position in the By Therapeutic Application segment of the Sterile Injectable Drugs Market. This preeminence is driven by the high prevalence and chronic nature of cardiovascular conditions, necessitating frequent and ongoing medical intervention. Cancer treatment also represented a significant share, propelled by advances in targeted therapies and the rising incidence of oncology cases.

Diabetes management, though robust, faced stiff competition from cardiovascular therapeutics but remained a critical segment due to the chronic nature of the disease and the necessity for continuous treatment. Infectious Disorders saw strong demand, especially with the global focus on combating emergent pathogens and antibiotic resistance. The Central Nervous System category benefitted from innovations in treating neurological disorders, while Musculoskeletal applications gained traction due to an aging population and increasing instances of osteoarthritis and related conditions.

Anti-viral treatments continued to grow, spurred by ongoing research and development in response to viral outbreaks. Lastly, the 'Others' category encompassed a diverse range of treatments addressing niche therapeutic needs, contributing to the overall robustness of the sterile injectable drugs market. This diverse segmentation underscores the market’s responsiveness to varied and evolving healthcare challenges.

By Distribution Channel Analysis

In 2023, Hospital Pharmacies dominated sterile injectable drug distribution channels.

In 2023, Hospital Pharmacies held a dominant market position in the by-distribution channel segment of the sterile injectable drugs market. This leadership is attributable to several critical factors. First, the intricate nature and administration requirements of sterile injectables often necessitate a controlled environment, sophisticated storage solutions, and professional healthcare administration, all of which are standard in hospital settings. Hospital pharmacies are equipped with the necessary infrastructure and trained personnel to manage these complex requirements effectively.

Retail pharmacies, while also significant, play a complementary role, particularly in follow-up treatments and chronic condition management where patients may require ongoing access to sterile injectables outside the hospital setting. Their growth is supported by the increasing prevalence of outpatient care and the rising incidence of chronic diseases requiring regular medication.

Online pharmacies represent a rapidly emerging distribution channel, driven by the convenience and expanding reach of e-commerce platforms. However, their market share remains comparatively smaller due to regulatory hurdles, cold chain logistics challenges, and patient trust issues. Nonetheless, advancements in telemedicine and digital health are likely to bolster their role shortly, potentially reshaping the competitive landscape of the sterile injectable drugs market.

Key Market Segments

By Type

- Small Molecule

- Large Molecule

By Therapeutic Application

- Cancer

- Diabetes

- Cardiovascular Diseases

- Infectious Disorders

- Central Nervous Systems

- Musculoskeletal

- Anti-Viral

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Growth Opportunity

Advancements in Biotechnology-Engineered Anti-Cancer Drugs

The global sterile injectable drugs market is poised for significant growth, driven primarily by advancements in biotechnology, particularly in the development of engineered anti-cancer drugs. The biotechnology sector has been instrumental in producing innovative therapies that offer higher efficacy and safety profiles. Engineered anti-cancer drugs, such as monoclonal antibodies and cell-based therapies, have shown remarkable success in clinical trials, promising enhanced treatment outcomes for patients. These advancements are expected to propel the demand for sterile injectable drugs as they require precise manufacturing processes to maintain sterility and efficacy. The continuous pipeline of biotechnological innovations and the increasing incidence of cancer globally underline a robust growth trajectory for this market segment.

Expansion of Healthcare Infrastructure and Access to Injectable Treatments

Another pivotal factor driving market growth is the expansion of healthcare infrastructure globally, especially in emerging economies. Governments and private sectors are investing heavily in upgrading healthcare facilities and making advanced treatments more accessible. This expansion increases the availability and administration of injectable treatments, including vaccines, antibiotics, and chronic disease therapies. Enhanced healthcare access leads to higher demand for sterile injectable drugs, which are often preferred due to their rapid onset of action and improved bioavailability. Furthermore, global health initiatives aimed at eradicating infectious diseases and improving chronic disease management are likely to bolster the sterile injectable drugs market.

Latest Trends

Rise in Cancer Cases and Demand for Cancer Treatments

The global incidence of cancer is projected to continue its upward trajectory, driving significant demand for sterile injectable drugs. This surge is attributed to various factors, including aging populations, increased exposure to carcinogens, and improved diagnostic capabilities. Sterile injectables, being a critical component of cancer treatment protocols, are expected to see heightened demand. These drugs offer precise delivery mechanisms essential for chemotherapy, immunotherapy, and targeted therapies. Pharmaceutical companies are increasingly investing in the development and production of advanced sterile injectables to meet the growing needs of oncology patients, resulting in robust market expansion.

Rise of E-commerce and Online Distribution Channels

The advent and acceleration of e-commerce are reshaping the distribution landscape for sterile injectable drugs. The shift towards online platforms is anticipated to gain momentum, influenced by the broader trend of digital transformation in the healthcare sector. E-commerce offers several advantages, including enhanced accessibility, streamlined logistics, and improved patient adherence through convenient delivery options. Pharmaceutical companies and distributors are capitalizing on these benefits by establishing robust online presence and direct-to-patient distribution models. This transition not only improves supply chain efficiency but also enhances the reach of sterile injectable drugs to remote and underserved areas, potentially increasing market penetration and sales volume.

Regional Analysis

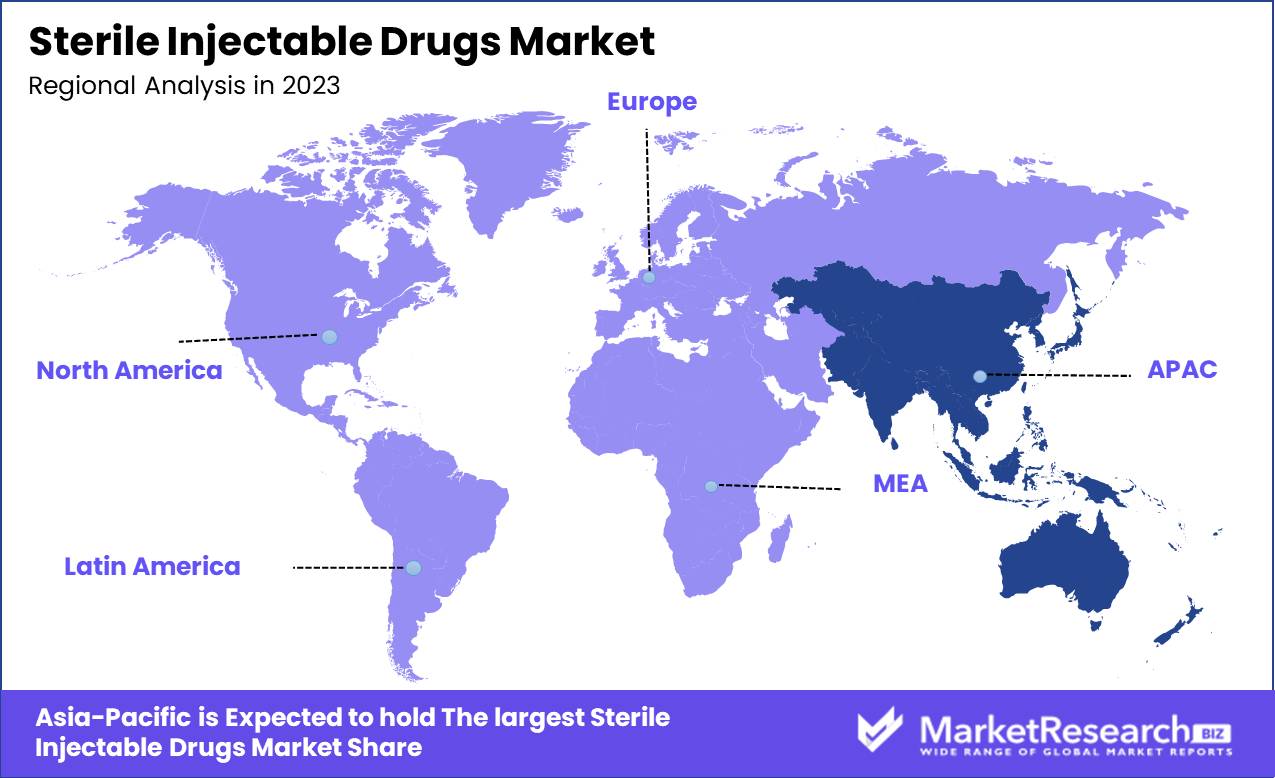

Asia Pacific leads the sterile injectable drugs market with a 35% share.

The Sterile Injectable Drugs market exhibits distinct regional dynamics, driven by varying levels of healthcare infrastructure, regulatory environments, and market demand. In North America, robust healthcare systems, high R&D investments, and the presence of major pharmaceutical companies contribute to significant market share. The U.S. leads this region with substantial FDA-approved sterile injectable products. Europe follows, characterized by stringent regulatory standards and a strong focus on biosimilars, particularly in countries like Germany, France, and the U.K. where healthcare spending is high.

Asia Pacific stands out as the dominant region, accounting for approximately 35% of the global market share, fueled by expanding healthcare infrastructure, rising prevalence of chronic diseases, and increasing investments in pharmaceutical manufacturing, notably in China and India. The Middle East & Africa region is experiencing gradual growth, propelled by improving healthcare access and increasing government initiatives, although market penetration remains lower compared to other regions. Latin America shows steady market development, with Brazil and Mexico being key contributors due to their large patient populations and ongoing healthcare reforms. Overall, the global sterile injectable drugs market is heavily influenced by the rapid growth in Asia Pacific, which is poised to continue leading due to its favorable demographic trends and significant industry investments.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global sterile injectable drugs market in 2024 is poised for significant growth, driven by advancements in biologics, increasing prevalence of chronic diseases, and heightened demand for vaccines and biosimilars. Key players like GlaxoSmithKline PLC, AstraZeneca, and Johnson & Johnson Services, Inc. are at the forefront of this expansion, leveraging their extensive R&D capabilities and robust portfolios to meet the rising global demand.

GlaxoSmithKline PLC and AstraZeneca are anticipated to capitalize on their strong pipelines of novel therapeutics and vaccines, bolstering their market positions. Johnson & Johnson Services, Inc., renowned for its diversified pharmaceutical products, continues to innovate in oncology and immunology, driving growth and competitive differentiation.

Sanofi and Merck & Co., Inc. are expected to benefit from their focus on specialty care and biosimilars, addressing critical needs in oncology and autoimmune disorders. Baxter International Inc. and Gilead Sciences Inc. are likely to see growth through strategic expansions and enhancements in their biologics and antiviral drug offerings.

Pfizer Inc. and Novartis AG remain influential with their expansive portfolios and strategic investments in biotechnology, while Nova Nordisk A/S is set to drive significant advancements in diabetes care. Amgen, Inc. continues to strengthen its market position through innovation in oncology and inflammation treatments.

In summary, these key players are strategically positioned to harness growth opportunities in the sterile injectable drugs market, driven by their robust R&D efforts, diverse portfolios, and strategic market expansions.

Market Key Players

- GlaxoSmithKline PLC

- Baxter International Inc.

- AstraZeneca

- Johnson & Johnson Services, Inc.

- Sanofi

- Merck & Co., Inc.

- Gilead Sciences Inc.

- Pfizer Inc.

- Novartis AG

- Nova Nordisk A/S

- Amgen, Inc.

Recent Development

- In May 2024, Baxter International announced a strategic partnership with Moderna, Inc. to develop and commercialize next-generation sterile injectable formulations of mRNA-based therapies. This collaboration focuses on leveraging Baxter's extensive manufacturing capabilities to produce Moderna's advanced therapeutic solutions.

- In April 2024, Merck completed the acquisition of Themis Bioscience, a company specializing in vaccine development and immune-modulatory therapies. The acquisition is poised to bolster Merck’s portfolio in the sterile injectables segment, particularly for novel vaccines and immune-modulating treatments.

- In February 2024, Pfizer announced the expansion of its sterile injectable manufacturing capabilities with a $500 million investment in their Kalamazoo, Michigan facility. This investment aims to enhance production capacity and modernize facilities to meet the growing demand for sterile injectables, especially in critical care and chronic disease management.

Report Scope

Report Features Description Market Value (2023) USD 596.2 Billion Forecast Revenue (2033) USD 1470.3 Billion CAGR (2024-2032) 9.7% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Small Molecule, Large Molecule), By Therapeutic Application (Cancer, Diabetes, Cardiovascular Diseases, Infectious Disorders, Central Nervous Systems, Musculoskeletal, Anti-Viral, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape GlaxoSmithKline PLC, AstraZeneca, Johnson & Johnson Services, Inc., Sanofi, Merck & Co., Inc., Baxter International Inc., Gilead Sciences Inc., Pfizer Inc., Novartis AG, Nova Nordisk A/S, Amgen, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- GlaxoSmithKline PLC

- Baxter International Inc.

- AstraZeneca

- Johnson & Johnson Services, Inc.

- Sanofi

- Merck & Co., Inc.

- Gilead Sciences Inc.

- Pfizer Inc.

- Novartis AG

- Nova Nordisk A/S

- Amgen, Inc.

Our Clients

View Our Licence Options