Serverless Computing Market By Service (Professional, Managed), By Type (Hybrid, Multi-Cloud), By End-user Industry (IT & Telecommunication, BFSI, Retail, Government, Industrial), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

51333

-

September 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

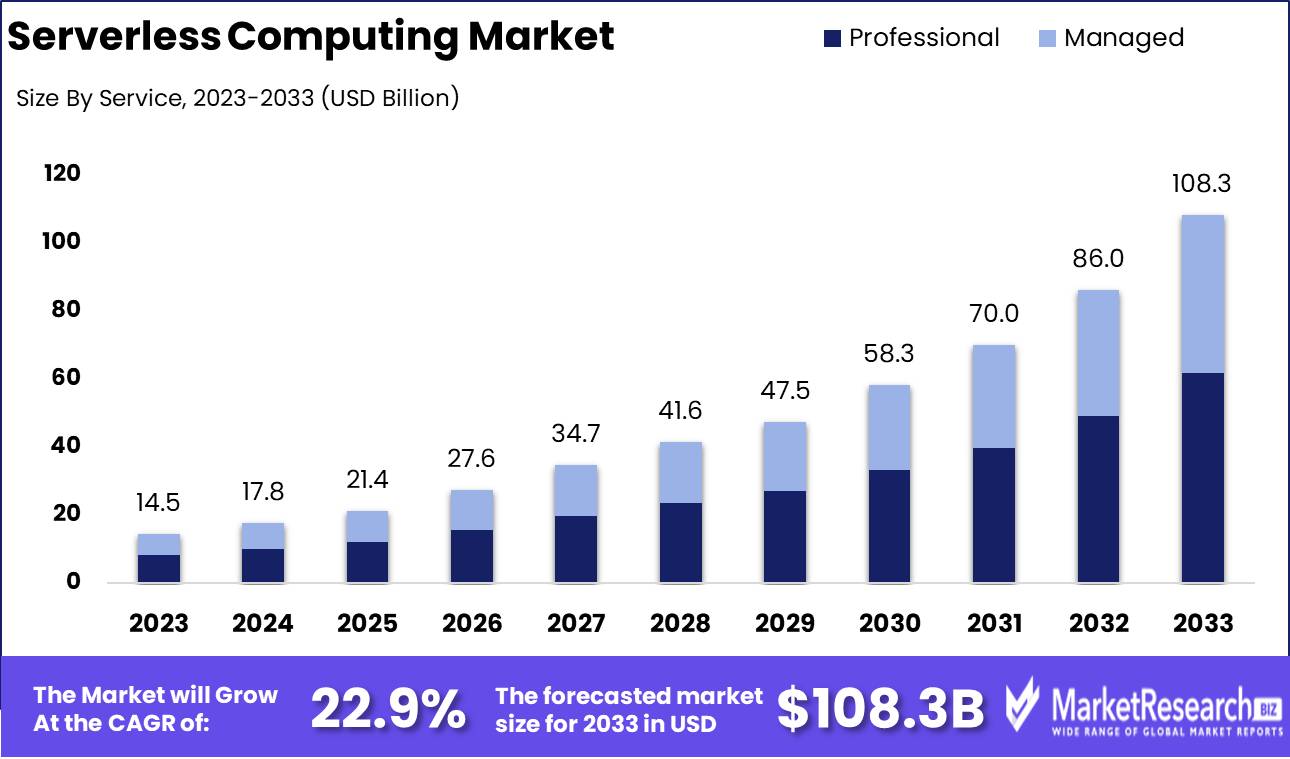

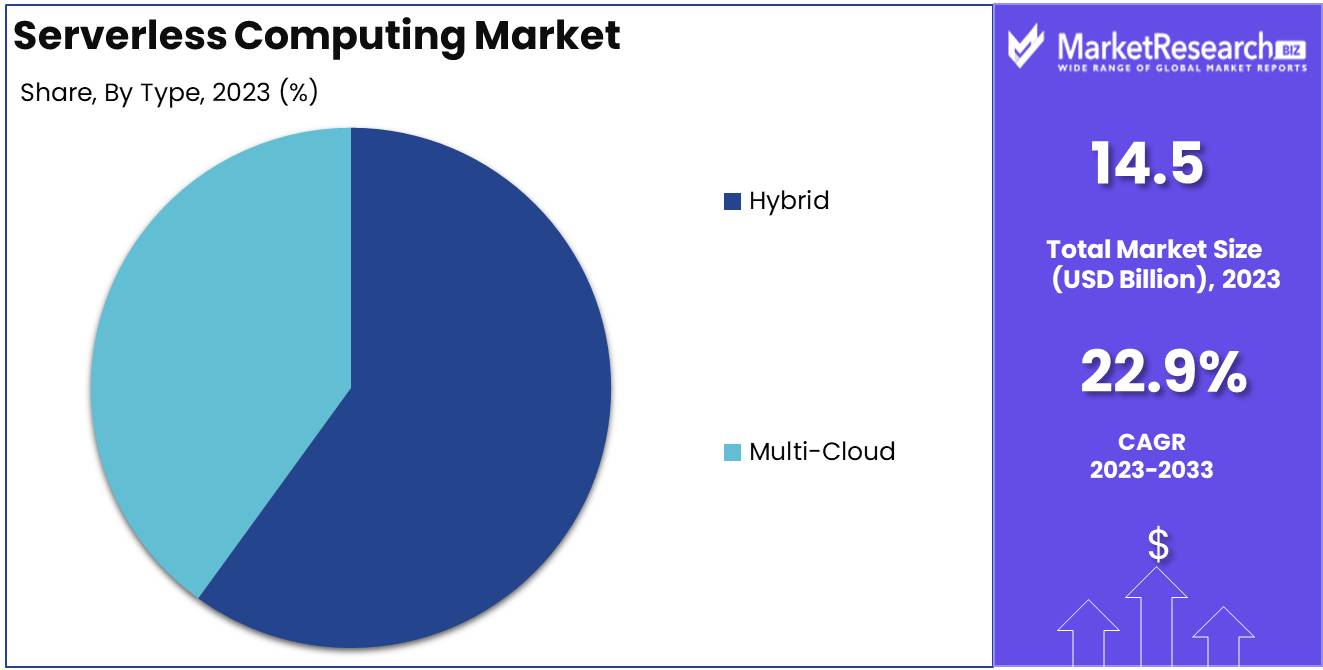

The Serverless Computing Market was valued at USD 14.5 billion in 2023. It is expected to reach USD 108.3 billion by 2033, with a CAGR of 22.9% during the forecast period from 2024 to 2033.

Serverless computing is a cloud computing model where developers can build and run applications without managing the underlying infrastructure. In this model, cloud providers handle server management, scaling, and maintenance, allowing organizations to focus on writing code and deploying applications. Serverless computing automatically scales based on demand and charges users only for actual resource consumption, improving cost efficiency.

The serverless computing market is poised for substantial growth, driven by the increasing demand for cost-efficient, scalable, and flexible solutions across industries. Organizations are shifting towards serverless architecture as it eliminates the need for managing infrastructure, significantly reducing operational costs. This cost-efficiency is further enhanced by the pay-per-use pricing model, which aligns well with businesses looking to optimize resources and control IT expenditure. Scalability, a key feature of serverless computing, allows companies to seamlessly manage varying workloads without the need for manual intervention, ensuring operational efficiency and performance consistency. Additionally, the flexibility of serverless solutions enables faster deployment and iteration, making them ideal for businesses focusing on rapid innovation.

Security and compliance, once a challenge in serverless environments, have seen notable improvements, with cloud service providers introducing advanced security protocols and compliance certifications to mitigate risks. Furthermore, the integration of AI and machine learning into serverless platforms is transforming business processes by automating tasks and enhancing decision-making capabilities. The ongoing innovation in developer tools is also contributing to market expansion, as improved debugging, monitoring, and development environments are making serverless computing more accessible and efficient for developers. These factors collectively indicate a robust upward trajectory for the serverless computing market, positioning it as a key enabler of digital transformation across multiple sectors. This growth is expected to accelerate as enterprises increasingly leverage serverless solutions to enhance agility, reduce costs, and innovate at scale.

Key Takeaways

- Market Growth: The Serverless Computing Market was valued at USD 14.5 billion in 2023. It is expected to reach USD 108.3 billion by 2033, with a CAGR of 22.9% during the forecast period from 2024 to 2033.

- By Service: Professional Services dominated serverless computing's service segment growth.

- By Type: Hybrid dominated the serverless computing market by type.

- By End-user Industry: IT & Telecommunication dominated the serverless computing market growth.

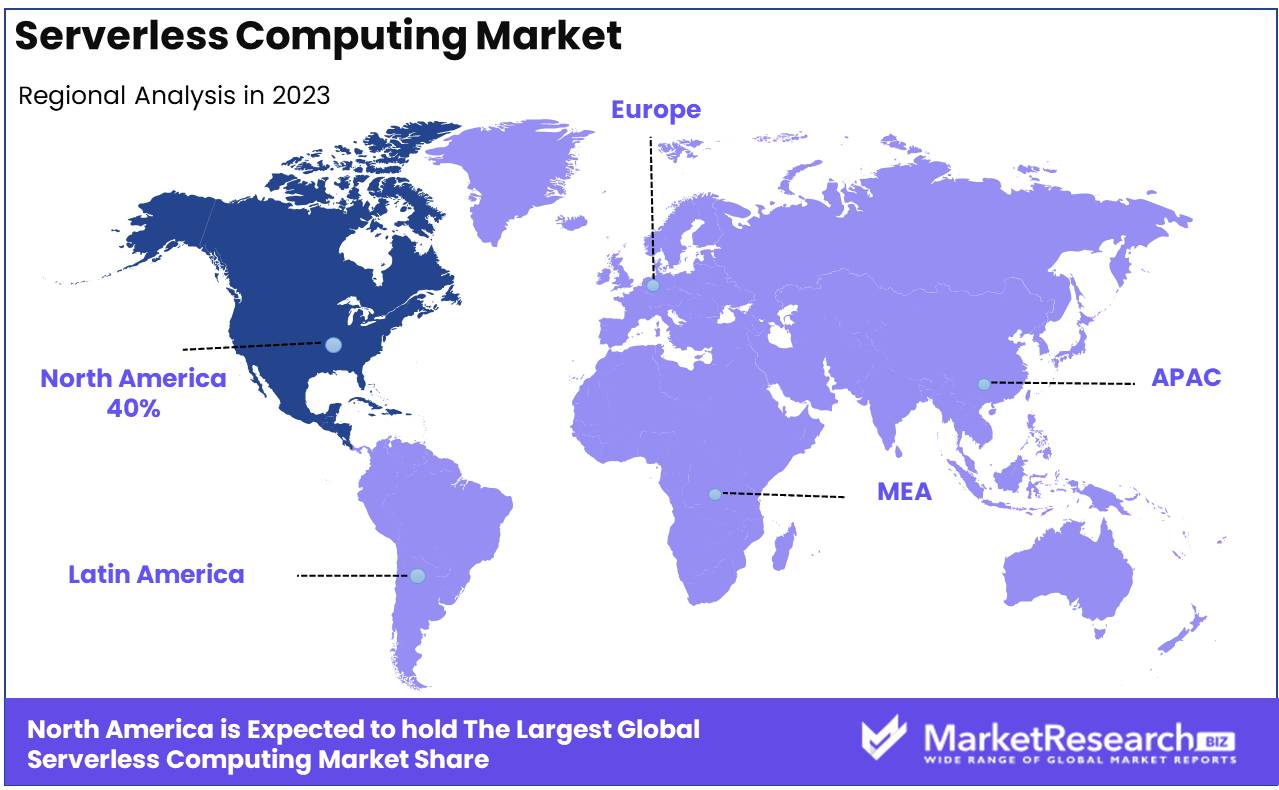

- Regional Dominance: North America dominates the serverless computing market with a 40% largest share.

- Growth Opportunity: The serverless computing market will witness significant growth, driven by increased digital transformation and AI/ML integration, enhancing agility, scalability, and cost-efficiency across industries.

Driving factors

Increased Demand for Cloud Automation Drives Scalability and Cost-Efficiency

The increased demand for cloud automation is a significant driving factor behind the growth of the serverless computing market. As businesses shift from traditional on-premises infrastructure to the cloud, the need for automated solutions to manage workloads, provisioning, and scaling becomes critical. Serverless computing enables companies to dynamically allocate resources based on demand, thus reducing the need for manual intervention in infrastructure management.

This automation allows organizations to achieve better cost-efficiency by paying only for the computing power they use. For instance, serverless platforms like AWS Lambda and Google Cloud Functions automatically scale resources during traffic spikes and reduce idle costs during periods of low demand. This has led to wider adoption across industries looking to optimize operational efficiency. According to industry reports, the global cloud automation market is expected to grow at a CAGR of 18.5% from 2021 to 2026, further fueling the serverless computing market.

Moreover, cloud automation enhances the agility of businesses by simplifying the deployment of applications, enabling faster go-to-market strategies. This flexibility and cost control, coupled with reduced operational overhead, directly contribute to the expansion of the serverless computing market, especially for SMEs and startups that may lack extensive IT resources.

Focus on Core Business Functions Shifts Operational Burden to Cloud Providers

The focus on core business functions is another pivotal factor driving the growth of the serverless computing market. Enterprises are increasingly seeking to offload the complexities of infrastructure management to third-party cloud providers, allowing their internal teams to concentrate on strategic initiatives and innovation rather than routine server management.

Serverless computing platforms handle backend infrastructure, including server maintenance, scaling, and security, thus freeing developers and IT teams to focus on building and improving applications. This shift enables businesses to allocate more resources to innovation and competitive differentiation, which enhances overall productivity. As the need for operational efficiency grows, serverless architectures are becoming increasingly attractive, especially for organizations that prioritize agility and scalability.

Additionally, the reduction in infrastructure overhead can also translate into financial savings. With no servers to manage and reduced infrastructure costs, businesses experience increased profitability while maintaining optimal performance. This has led to higher adoption rates across sectors such as retail, healthcare, and finance, where the emphasis on customer-facing applications requires a consistent focus on business objectives and less on IT maintenance.

The proliferation of Microservices Architecture Fosters Modular and Agile Application Development

The proliferation of microservices architecture plays a critical role in the growth of the serverless computing market. Microservices break down complex applications into smaller, independent services that can be developed, deployed, and scaled individually. This modular approach aligns seamlessly with serverless computing, where individual functions can be executed and scaled independently, reducing resource consumption and improving overall system resilience.

Microservices, when combined with serverless computing, offer enhanced flexibility, enabling developers to deploy services without worrying about the underlying infrastructure. This increases the speed of development cycles and simplifies the integration of new features or updates. The convergence of these architectures is particularly beneficial in industries that require rapid innovation and frequent deployment of new services, such as e-commerce, banking, and entertainment.

As organizations increasingly adopt microservices for their software development processes, serverless computing becomes the preferred choice due to its ability to scale specific functions in response to microservice demands. According to industry trends, the microservices architecture market is projected to grow at a CAGR of 18.6% between 2021 and 2026. This expansion will further drive the adoption of serverless computing as businesses seek efficient ways to manage the complexity of microservices without being burdened by infrastructure concerns.

Restraining Factors

Complexity in Monitoring and Debugging: A Barrier to Efficient Operations in Serverless Computing

The complexity associated with monitoring and debugging serverless architectures presents a significant restraining factor in the growth of the serverless computing market. In traditional computing environments, developers and IT teams have direct control over the infrastructure, allowing them to track and debug applications more effectively. However, serverless architectures abstract much of this infrastructure management, making it difficult to monitor various aspects such as performance metrics, error tracing, and log management across distributed systems.

The lack of visibility into the underlying systems complicates root-cause analysis during failures or performance bottlenecks, often resulting in increased operational overhead. This complexity leads to longer resolution times and higher maintenance costs, deterring businesses from adopting serverless models, particularly for critical applications where uptime and performance are paramount. According to industry reports, the need for enhanced tools that can simplify monitoring and debugging in serverless environments has been a key factor limiting the broader adoption of serverless solutions.

Compliance and Regulatory Issues: A Major Concern for Serverless Adoption in Regulated Industries

Compliance and regulatory issues also contribute to slowing down the adoption of serverless computing, particularly in industries like finance, healthcare, and government, where stringent data security and privacy regulations must be adhered to. In serverless computing environments, data may be processed across various regions and cloud providers, introducing complications in meeting local and international regulatory standards, such as GDPR, HIPAA, or PCI DSS.

A lack of control over where and how data is stored or processed increases the risks associated with compliance violations. Additionally, serverless environments rely on third-party cloud providers, complicating the ability of businesses to ensure data governance and compliance reporting, further raising concerns about accountability and risk management. Businesses, especially those handling sensitive information, may hesitate to fully embrace serverless computing due to these concerns, restricting the market's growth potential in regulated sectors.

The intersection of these regulatory concerns and the complexity in monitoring demonstrates a cumulative effect, wherein both issues contribute to operational inefficiencies and increased risk, making it less attractive for businesses that prioritize security, control, and regulatory compliance.

By Service Analysis

In 2023, Professional Services dominated serverless computing's service segment growth.

In 2023, Professional Services held a dominant market position in the by-service segment of the Serverless Computing Market. This can be attributed to the increasing demand for expertise in the development, deployment, and management of serverless infrastructure. Enterprises are increasingly relying on professional service providers to guide the transition from traditional cloud computing models to serverless architectures, driven by the need for customized solutions, best practices implementation, and reduced operational complexity. Professional services, including consulting, training, and integration, play a crucial role in helping organizations maximize the benefits of serverless computing, such as cost efficiency and scalability.

Meanwhile, Managed Services are also experiencing significant growth within the same segment, driven by businesses looking to outsource the management and maintenance of serverless infrastructure. These services provide continuous monitoring, optimization, and support, ensuring seamless operation and freeing internal IT teams from the burdens of infrastructure management. The expansion of managed services reflects the growing demand for scalability and flexibility in application deployment, particularly among small and medium-sized enterprises (SMEs) seeking to enhance operational agility while maintaining cost control.

By Type Analysis

In 2023, Hybrid dominated the serverless computing market by type.

In 2023, Hybrid held a dominant market position in the By Type segment of the Serverless Computing Market, followed by Multi-Cloud. The Hybrid approach allows enterprises to balance their workloads between on-premises and cloud environments, providing increased flexibility and control over data management and security. This flexibility is critical for industries with strict regulatory requirements, such as healthcare and finance, where sensitive data must remain within certain geographic or organizational boundaries. Hybrid serverless computing also enables businesses to optimize costs by leveraging their existing infrastructure while scaling with cloud resources during peak demands.

Meanwhile, Multi-Cloud adoption continues to grow, offering organizations a diversified approach that reduces dependency on a single cloud provider, improving redundancy and service reliability. This approach supports risk mitigation by distributing workloads across multiple cloud environments, offering higher availability, and preventing vendor lock-in. Both Hybrid and Multi-Cloud solutions are projected to drive significant growth in the serverless computing market, as enterprises prioritize scalability, cost efficiency, and security in their digital transformation initiatives.

By End-user Industry Analysis

In 2023, IT & Telecommunication dominated the serverless computing market growth.

In 2023, IT & Telecommunication held a dominant market position in the By End-user Industry segment of the Serverless Computing Market. The demand for scalable, cost-effective cloud solutions in IT and telecommunication services significantly contributed to the adoption of serverless computing models. Rapid digital transformation, increased demand for high-speed internet, and the expansion of 5G networks further accelerated this growth.

The BFSI sector also experienced substantial growth, leveraging serverless computing to streamline operations, improve data processing speeds, and enhance cybersecurity. The adoption of serverless architecture enabled BFSI firms to handle the vast amounts of data generated by financial transactions efficiently.

The Retail industry witnessed a growing implementation of serverless computing due to the increased reliance on e-commerce platforms and omnichannel strategies. Serverless models allowed for seamless scaling during peak demand periods, optimizing customer experiences.

In the Government sector, serverless computing gained traction for public administration, where scalability, security, and cost-efficiency were essential for managing large data repositories and digital service delivery.

The Industrial segment adopted serverless computing solutions to facilitate IoT integration, automation, and smart manufacturing. The ability to process real-time data with minimal infrastructure costs positioned serverless computing as an ideal solution for industries seeking agile and flexible digital operations.

Key Market Segments

By Service

- Professional

- Managed

By Type

- Hybrid

- Multi-Cloud

By End-user Industry

- IT & Telecommunication

- BFSI

- Retail

- Government

- Industrial

Growth Opportunity

Increased Demand for Digital Transformation

The global serverless computing market is poised for significant growth, driven primarily by the rising demand for digital transformation across industries. Businesses are increasingly prioritizing agility and scalability in their IT infrastructure, seeking to reduce operational complexities and overhead costs. Serverless architecture, which allows companies to run applications without managing underlying servers, aligns perfectly with this trend. As organizations continue to modernize their IT ecosystems, the adoption of serverless models is expected to accelerate, providing a flexible and cost-effective solution for handling dynamic workloads and application scaling. This trend will particularly benefit sectors like e-commerce, healthcare, and financial services, where the demand for real-time processing is surging.

Integration of AI and Machine Learning

AI and machine learning (ML) integration into serverless computing environments is another key growth driver. The convergence of these technologies is anticipated to create new opportunities for businesses seeking to leverage advanced data analytics and automation. Serverless platforms provide the ideal framework for executing AI/ML workloads by offering event-driven, scalable computing resources that automatically adjust to demand. As more enterprises integrate AI/ML models into their applications for tasks like predictive analytics and personalized user experiences, serverless infrastructure will be increasingly adopted. This will not only streamline AI/ML development but also enhance operational efficiency, reducing time-to-market for new applications.

Latest Trends

Growing Need for Real-Time Data Processing

The serverless computing market is set to experience significant growth, driven by the increasing demand for real-time data processing. Enterprises are shifting from batch-processing methods to serverless architectures, which offer faster and more efficient data-handling capabilities. As businesses rely on real-time analytics for decision-making, serverless computing will play a critical role in delivering low-latency processing and reducing infrastructure overhead. This demand is particularly strong in sectors such as financial services, e-commerce, and IoT, where immediate data insights are paramount for operational efficiency.

Support for Multiple Programming Languages

Another key trend in the serverless computing market is the growing support for multiple programming languages. Vendors are expanding their platforms to accommodate a wider range of languages, making it easier for developers from diverse technical backgrounds to adopt serverless solutions. This trend reflects the broader movement towards polyglot programming, where developers leverage the strengths of different languages for specific tasks. Serverless platforms that support languages such as Python, Node.js, Java, Go, and .NET are expected to see increased adoption as they enable more flexible and customized application development.

Regional Analysis

North America dominates the serverless computing market with a 40% largest share.

The global serverless computing market exhibits varied growth across regions, driven by the increasing adoption of cloud-native applications and the need for agile computing solutions. North America dominates the serverless computing market, accounting for approximately 40% of the global market share. This dominance is largely attributed to the presence of major cloud service providers such as AWS, Microsoft Azure, and Google Cloud, coupled with the region's advanced technological infrastructure. The high adoption of cloud solutions across industries, particularly in the United States, drives the growth in this region.

Europe holds a significant market share, with countries like Germany, the UK, and France leading the adoption of serverless computing, contributing to approximately 25% of the market. Regulatory frameworks surrounding data privacy and cloud computing, such as GDPR, influence the growth in this region, driving demand for secure and scalable cloud services.

The Asia Pacific region is expected to witness the fastest growth, with a compound annual growth rate (CAGR) exceeding 25% during the forecast period. Rapid digital transformation, particularly in China and India, the increasing penetration of cloud services, and a rising number of startups are key growth drivers.

In the Middle East & Africa and Latin America, the market is growing steadily, driven by increasing cloud adoption across various sectors. However, these regions collectively account for a smaller share of the global market, with a growth rate anticipated to increase as cloud infrastructure matures and digitalization initiatives expand. North America remains the dominant region, given its robust cloud ecosystem and early adoption trends.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global serverless computing market is projected to experience substantial growth, driven by key players offering advanced serverless architectures and cloud-native solutions. Notable companies such as Microsoft Corporation, Amazon Web Services (AWS), and Google LLC continue to dominate the landscape due to their extensive infrastructure capabilities and cloud ecosystems. AWS Lambda remains a significant driver, allowing seamless integration of cloud services and enhancing scalability.

Microsoft Azure Functions is gaining traction by leveraging its strong enterprise relationships, while Google Cloud Functions appeals to developers due to its integration with Google’s broader cloud offerings. Additionally, Firebase, a Google subsidiary, strengthens Google’s position with serverless backend solutions that target mobile and web developers.

Alibaba Group, IBM Corporation, and Oracle Corporation are expanding their cloud platforms with serverless capabilities, particularly in Asia-Pacific markets, where cloud adoption is accelerating. Platform9 Systems, Inc., Rackspace Inc., and NTT Data also contribute with hybrid cloud solutions, catering to businesses seeking more flexible deployment options.

Innovators like Syncano, Joyent, Iron.io, and Realm are fostering serverless innovation by offering lightweight, developer-friendly platforms, focusing on real-time data processing and microservices. Companies like Dynatrace and Snyk add value by addressing security and performance monitoring challenges within serverless architectures, which are increasingly critical in highly distributed systems.

Emerging players such as Galactic Fog Ip Inc., Modubiz, and Tarams Software Technologies emphasize platform customization and specific-use cases, signaling a diversification of offerings in the serverless computing ecosystem, and positioning these players for growth in specialized markets.

Market Key Players

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC.

- Firebase

- Alibaba Group

- IBM Corporation

- Oracle Corporation

- Platform9 Systems, Inc.

- Rackspace Inc.

- CA Technologies

- Tibco Software

- Syncano

- NTT Data

- Joyent

- Iron.io

- Stdlib

- Realm

- Galactic Fog Ip Inc

- Modubiz

- Tarams Software Technologies,

- Snyk

- Dynatrace

- Fior

Recent Development

- In July 2024, Amazon Web Services (AWS) introduced significant updates to its Lambda function in July 2024. The new features focus on enhanced scalability and performance, specifically to support workloads driven by generative AI (GenAI). These updates include the ability to run more complex, fine-tuned machine learning models, and aligning serverless computing with AI workloads that have become increasingly important. AWS remains the market leader, holding a significant share of the global serverless market.

- In June 2024, GCP advanced its serverless architecture by integrating edge computing in June 2024. This integration allows serverless functions to operate closer to the data source, improving real-time data processing, especially for IoT and 5G-enabled applications. This development is a key step in reducing latency and addressing the needs of industries requiring real-time analytics.

- In January 2024, PwC Consulting emphasized the growing role of Generative AI (GenAI) in serverless computing. Developers can now integrate AI and machine learning models into serverless environments more easily, significantly accelerating development cycles and enhancing performance. GenAI helps automate and optimize functions in real-time, improving scalability and reducing manual intervention, which makes AI-driven serverless solutions more attractive for various industries.

Report Scope

Report Features Description Market Value (2023) USD 14.5 Billion Forecast Revenue (2033) USD 108.3 Billion CAGR (2024-2032) 22.9% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Service (Professional, Managed), By Type (Hybrid, Multi-Cloud), By End-user Industry (IT & Telecommunication, BFSI, Retail, Government, Industrial) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Microsoft Corporation, Amazon Web Services, Inc., Google LLC., Firebase, Alibaba Group, IBM Corporation, Oracle Corporation, Platform9 Systems, Inc., Rackspace Inc., CA Technologies, Tibco Software, Syncano, NTT Data, Joyent, Iron.io, Stdlib, Realm, Galactic Fog Ip Inc, Modubiz, Tarams Software Technologies, Snyk, Dynatrace, Fior Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC.

- Firebase

- Alibaba Group

- IBM Corporation

- Oracle Corporation

- Platform9 Systems, Inc.

- Rackspace Inc.

- CA Technologies

- Tibco Software

- Syncano

- NTT Data

- Joyent

- Iron.io

- Stdlib

- Realm

- Galactic Fog Ip Inc

- Modubiz

- Tarams Software Technologies,

- Snyk

- Dynatrace

- Fior

Our Clients

View Our Licence Options