Global Sanitary Ware Market By Technology(Spangles, Slip Casting, Pressure Coating, Jiggering, Isostatic Casting, Others), By Product Type(Urinals, Washbasins & Kitchen Sinks, Bidets, Water Closets, Faucets, Others), By Distribution Channel(Online, Offline), By End-User(Commercial, Residential, Personal), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

5335

-

August 2024

-

300

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

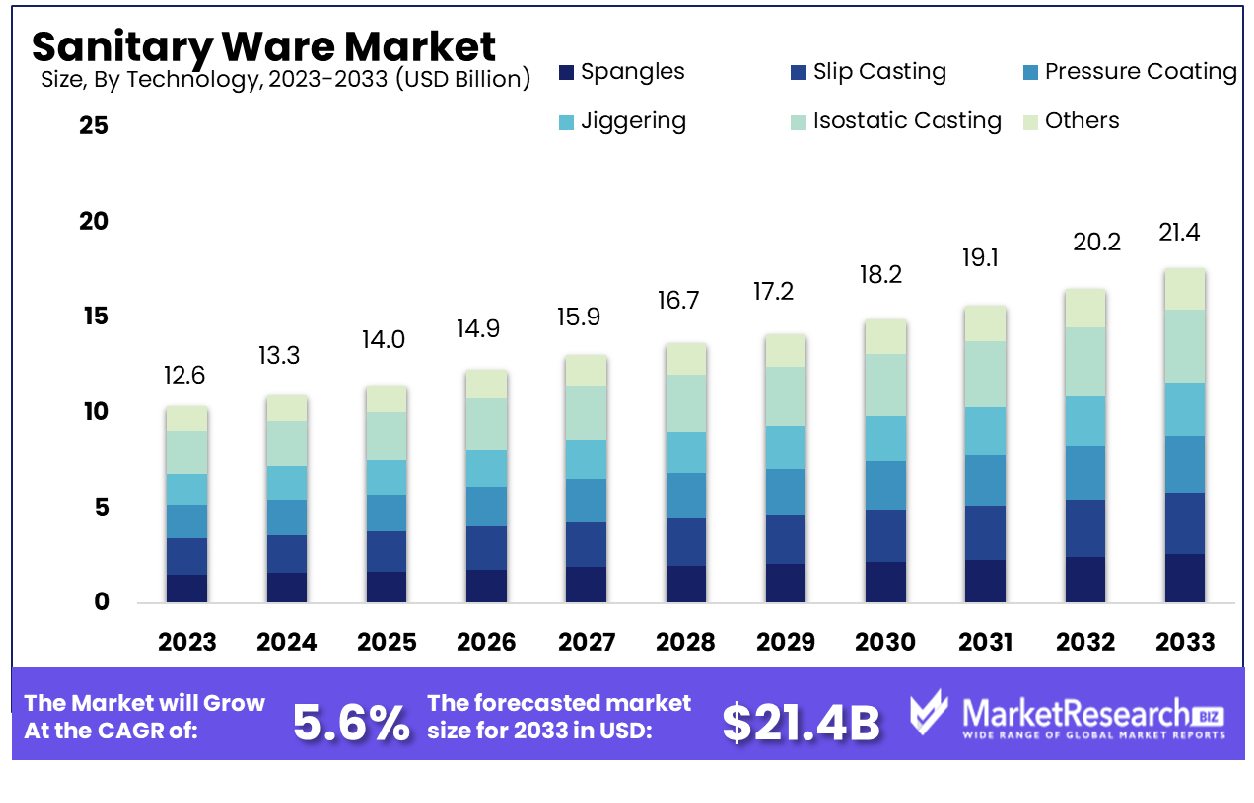

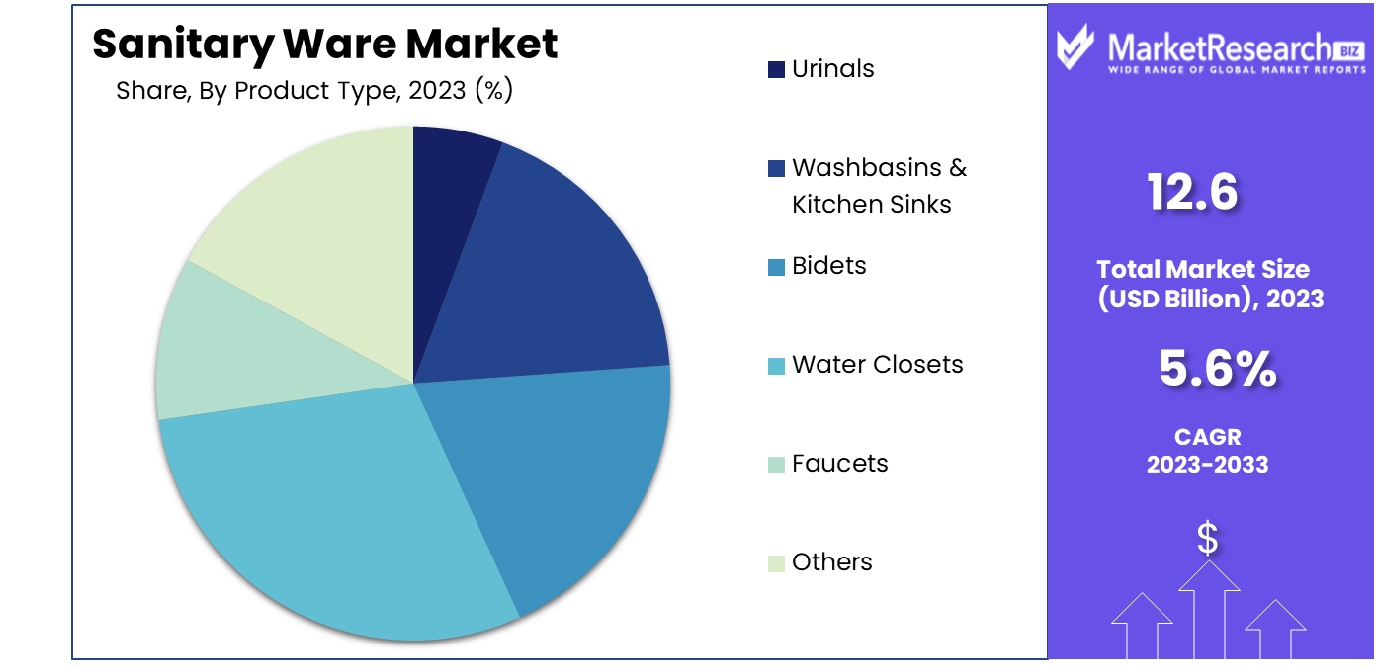

The Global Sanitary Ware Market was valued at USD 12.6 billion in 2023. It is expected to reach USD 21.4 billion by 2033, with a CAGR of 5.6% during the forecast period from 2024 to 2033.

The Sanitary Ware Market encompasses a diverse range of products designed for hygiene and sanitation purposes within residential, commercial, and industrial settings. This market primarily includes fixtures such as toilets, washbasins, urinals, and bidets, along with ancillary products like bathroom accessories and fittings.

Integral to building and renovation projects, the market's growth is propelled by advancements in materials technology, design innovation, and increasing emphasis on sustainable solutions. Strategic leaders such as product managers focus on market trends, consumer preferences, and regulatory impacts to drive competitive advantage and meet evolving consumer expectations in the global marketplace.

The sanitary ware market in India has witnessed a notable contraction in export values in the year 2023. The exports of commodity group 7324, which includes sanitary ware and parts thereof made of iron or steel, totaled $12.2 million, marking a decline of 15.3% compared to the previous year. This downturn follows a peak in 2022, where exports reached $14.4 million. The data points to volatility in the market over the past decade, with figures oscillating and hitting a low of $8.3 million in 2012.

Such fluctuations suggest a market influenced by varying factors including economic conditions, international demand, and competitive dynamics. The recent decline could be attributed to a range of factors such as changes in global market demand, increased competition from other countries, or shifts in production costs. As such, stakeholders in the industry should consider these elements in strategic planning and positioning to better navigate the uncertainties of the market.

Key Takeaways

- Market Growth: The Global Sanitary Ware Market was valued at USD 12.6 billion in 2023. It is expected to reach USD 21.4 billion by 2033, with a CAGR of 5.6% during the forecast period from 2024 to 2033.

- Regional Dominance: Asia Pacific dominates the sanitary ware market with a 40.2% share.

- By Technology: Isostatic casting technology dominates 25% of the market by technology.

- By Product Type: Water closets lead product types, holding a 35% market share.

- By Distribution Channel: Online distribution channels overwhelmingly lead with a 70% dominance.

- By End-User: Commercial end-users represent half of the market at 50%.

Driving factors

Increasing Urbanization and Housing Construction

The surge in urbanization globally, coupled with increasing housing construction, acts as a pivotal driver for the sanitary ware market. Urbanization leads to higher population densities in cities, necessitating the development of residential and commercial infrastructure. This development inherently increases demand for bathroom fixtures and fittings, which are integral components of new buildings.

Statistically, global urbanization has reached over 55%, with projections suggesting further growth, which aligns with increasing investments in construction sectors across emerging economies. This trend not only supports market expansion through heightened demand but also by fostering innovations tailored to urban living environments.

Rising Focus on Hygiene and Sanitation

Heightened awareness and rising standards of hygiene and sanitation globally have significantly influenced the sanitary ware market. Recent global health crises have underscored the importance of hygiene practices, leading to more stringent sanitation requirements in both public and private spaces.

This shift has catalyzed demand for modern and efficient sanitary ware solutions that offer enhanced cleanliness and reduce the spread of pathogens. Governments and health organizations' increasing emphasis on sanitary regulations has propelled the adoption of advanced sanitary installations, driving market growth from a regulatory and consumer behavior perspective.

Growing Preference for Luxury Sanitary Ware Products

The luxury segment of the sanitary ware market is witnessing robust growth, driven by rising disposable incomes and the aspirational lifestyles of the middle and upper economic classes. Consumers are increasingly seeking bespoke and high-end bathroom aesthetics, which include premium fixtures that offer superior functionality and design.

This demand for luxury sanitary products is not only prevalent in new residential developments but also in renovations and upgrades of existing properties. The luxury market's expansion is further supported by innovations in product design, such as smart toilets and sensor-based faucets, which combine luxury with technology to enhance user experience and convenience.

Restraining Factors

High Cost of Premium and Designer Sanitary Ware

The high cost of premium and designer sanitary ware products significantly restrains market growth, particularly in cost-sensitive markets. These premium products often feature cutting-edge design and technology, which while appealing, come with a price tag that can be prohibitive for a large segment of consumers.

This pricing barrier limits the accessibility of luxury sanitary ware to a niche market, primarily affluent consumers and high-end commercial projects. The limited consumer base can stifle the overall growth potential of the sanitary ware market, as manufacturers may struggle to achieve economies of scale in the production and distribution of these high-cost items.

Fluctuations in Raw Material Prices

Fluctuations in the prices of raw materials, such as ceramics, metals, and plastics, pose a significant challenge to the sanitary ware market. These materials are essential for manufacturing sanitary products, and price volatility can directly impact production costs.

For instance, a rise in the cost of ceramic might lead to higher prices for ceramic basins and toilets, which in turn could reduce consumer demand and affect market growth negatively. Such fluctuations can also lead to inconsistent product pricing, complicating budgeting and financial planning for manufacturers and potentially leading to decreased investment in new product development.

By Technology Analysis

Isostatic casting technology dominates 25% of the market, favored for its uniformity and strength in products.

In 2023, Isostatic Casting held a dominant market position in the By Technology segment of the Sanitary Ware Market, capturing more than a 25% share. This method surpassed other technologies such as Spangles, Slip Casting, Pressure Coating, Jiggering, and Others in market adoption, owing to its superior precision and uniformity in product density and strength, which are critical in high-quality sanitary ware manufacturing.

The breakdown of market share by technology in the sanitary ware industry reveals that following Isostatic Casting, Slip Casting also maintained a significant presence, accounting for approximately 20% of the market. This method is favored for its cost-effectiveness and flexibility in shaping intricate designs. Jiggering, which allows for the efficient production of symmetrical forms, captured around 15% of the market. Meanwhile, Pressure Coating and Spangles collectively held around 20%, with each bringing unique aesthetic and functional benefits to sanitary ware.

The remaining market share was distributed among other emerging technologies, which collectively accounted for the remaining 20%. These are gaining traction as manufacturers explore new materials and innovative manufacturing techniques to enhance the aesthetic appeal and functional capabilities of sanitary ware.

The preference for Isostatic Casting is largely attributed to its ability to produce high-strength, flawless products that meet the rigorous standards of modern infrastructure needs. Its dominance is supported by advancements in automation and pressing technology, which have significantly reduced manufacturing times and costs, thus driving its adoption across major markets. The continued growth in this segment is indicative of a broader trend toward adopting high-efficiency, cost-effective technologies in the sanitary ware industry.

By Product Type Analysis

Water closets lead in product type, holding a 35% share, indicating strong consumer preference and widespread usage.

In 2023, Water Closets held a dominant market position in the By Product Type segment of the Sanitary Ware Market, capturing more than a 35% share. This category outperformed other segments including Urinals, Washbasins & Kitchen Sinks, Bidets, Faucets, and Others, due to its essential role in residential and commercial buildings globally.

Following Water Closets, the Washbasins & Kitchen Sinks segment also secured a robust market share, accounting for approximately 25%. This segment benefits from the increasing trend towards modern and more functional kitchens and bathrooms. Faucets, integral to both cost-effective renovations and luxury designs, claimed about 15% of the market, driven by innovations in water-saving technologies and aesthetic design.

Urinals and Bidets collectively accounted for 15% of the market. Urinals have seen moderate growth, particularly in commercial and institutional sectors driven by a growing emphasis on water conservation. Bidets, though less common in some regions, are gaining popularity due to increasing awareness of hygiene and the rise in health-conscious consumers.

The remaining market share, representing 10%, is distributed among other miscellaneous sanitary ware products which include specialty items and innovative designs that cater to niche markets.

The dominance of Water Closets is primarily attributed to the increasing construction activities worldwide, coupled with rising demands for sanitary products that promote water efficiency. The ongoing urbanization and upgrades in sanitary standards globally further catalyze this segment’s growth, making it a critical area for manufacturers in the sanitary ware industry.

By Distribution Channel Analysis

Online distribution channels command a 70% market share, reflecting consumer shifts towards digital shopping experiences.

In 2023, Online held a dominant market position in the By Distribution Channel segment of the Sanitary Ware Market, capturing more than a 70% share. This overwhelming preference for online channels starkly contrasts with the Offline segment, which accounted for the remaining 30% of the market.

The ascendancy of the Online distribution channel can be primarily attributed to the convenience and wide range of options it offers consumers. Factors such as ease of access to detailed product information, user reviews, and competitive pricing have significantly contributed to the preference for purchasing sanitary ware online. Additionally, the growth of e-commerce platforms and digital marketing strategies has enhanced consumer reach and engagement, further propelling online sales.

Offline channels, including brick-and-mortar stores and showrooms, continue to play a crucial role, particularly in offering consumers tactile experiences and immediate purchases. However, the shift towards digitalization and the impact of the COVID-19 pandemic have accelerated the adoption of online shopping, diminishing the market share held by traditional retail outlets.

Despite the substantial lead of online channels, there is an ongoing effort within the offline segment to regain market relevance through experiential retailing and personalized customer service, which are difficult to replicate online. Moreover, some consumers still prefer the in-store experience for high-value items like luxury sanitary ware, indicating that offline channels retain significant potential for targeted growth strategies.

Overall, the dominance of the online segment underscores a broader shift in consumer behavior and market dynamics within the sanitary ware industry, highlighting the need for manufacturers and retailers to adapt to an increasingly digital marketplace.

By End-User Analysis

The commercial sector is the largest end-user, dominating 50% of the market, driven by extensive facility upgrades.

In 2023, Commercial held a dominant market position in the By End-User segment of the Sanitary Ware Market, capturing more than a 50% share. This segment outstripped the Residential and Personal segments, which collectively accounted for the remaining market share, demonstrating a significant inclination towards commercial applications.

The substantial lead of the Commercial segment is primarily driven by extensive infrastructural developments, including new commercial buildings and renovations of existing facilities such as hotels, office spaces, shopping centers, and educational institutions. The growth in this segment is further fueled by increased investments in commercial real estate and urban development projects across the globe.

Residential follows, with a substantial share, reflecting ongoing housing developments and the rising demand for improved sanitation facilities in homes. This segment benefits from the growing trend towards modern and luxurious bathroom fittings, driven by rising disposable incomes and the increasing importance of comfort and aesthetics in residential design.

The Personal segment, while smaller in comparison, is gradually expanding as individual consumers show heightened interest in upgrading their personal sanitary facilities, influenced by health and hygiene awareness heightened by recent global health events.

Overall, the dominance of the Commercial segment underscores the critical role of economic growth, urbanization, and infrastructural investment in driving the sanitary ware market. The focus on sustainability and hygiene standards in commercial settings further supports the sustained demand in this segment, highlighting its pivotal role in the overall market dynamics of the sanitary ware industry.

Key Market Segments

By Technology

- Spangles

- Slip Casting

- Pressure Coating

- Jiggering

- Isostatic Casting

- Others

By Product Type

- Urinals

- Washbasins & Kitchen Sinks

- Bidets

- Water Closets

- Faucets

- Others

By Distribution Channel

- Online

- Offline

By End-User

- Commercial

- Residential

- Personal

Growth Opportunity

Technological Advancements in Eco-Friendly Products

In 2023, the global sanitary ware market is poised to capitalize significantly on technological advancements in eco-friendly products. Environmental concerns and stringent regulations on water usage are driving the development and adoption of sustainable sanitary solutions. Innovations such as low-flow toilets and waterless urinals are not only aligning with global sustainability goals but are also offering long-term cost savings to consumers through reduced water bills.

These advancements present a substantial opportunity for market growth, as eco-conscious consumers and green building certifications increasingly influence buying decisions. Companies that are at the forefront of integrating these green technologies into their product offerings are likely to gain a competitive edge and capture a growing segment of environmentally aware customers.

Expansion in Emerging Markets

Emerging markets represent a significant growth opportunity for the sanitary ware industry in 2023. Rapid urbanization, increasing disposable incomes, and expanding middle classes in regions such as Asia, Africa, and Latin America are creating new demand for modern sanitary facilities. As these economies grow, there is a heightened focus on improving infrastructure, which includes upgrading public and private sanitation facilities.

The expansion into these markets is facilitated by the local government's initiatives to enhance living standards and promote hygiene practices, offering substantial market potential for sanitary ware manufacturers. By tapping into these emerging markets, companies can diversify their revenue streams and offset potential slowdowns in more mature markets, thus sustaining their overall market growth in the face of global economic fluctuations.

Latest Trends

Integration of Smart Technology in Sanitary Products

The integration of smart technology into sanitary products is a defining trend in the 2023 global sanitary ware market, reflecting a broader shift towards connected, intelligent home environments. Smart sanitary products, which include toilets with built-in health monitoring, touchless faucets, and shower systems that can be controlled via smartphones, are gaining traction among tech-savvy consumers.

These innovations not only enhance user convenience and hygiene but also align with the increasing consumer preference for home automation systems. The ability of these products to integrate seamlessly with other smart home system devices offers significant growth potential for the industry. Manufacturers investing in these technologies are likely to see increased market share as they cater to the modern consumer’s desire for convenience, customization, and advanced functionality.

Increasing Demand for Water-Efficient Products

Amid growing environmental concerns and rising water scarcity, the demand for water-efficient sanitary products is escalating. In 2023, this trend is especially prominent, driven by both regulatory pressures and consumer awareness around sustainable living. Products that conserve water, such as high-efficiency toilets (HETs), low-flow showerheads, and faucets with aerators, are becoming the standard in new residential and commercial constructions.

This demand for water-efficient products is not only a response to environmental sustainability but also a cost-saving measure for consumers looking to reduce their water bills. The industry's response to this demand is critical, as offering a range of water-efficient products can be a decisive factor for companies aiming to enhance their brand image and market position in a competitive landscape.

Regional Analysis

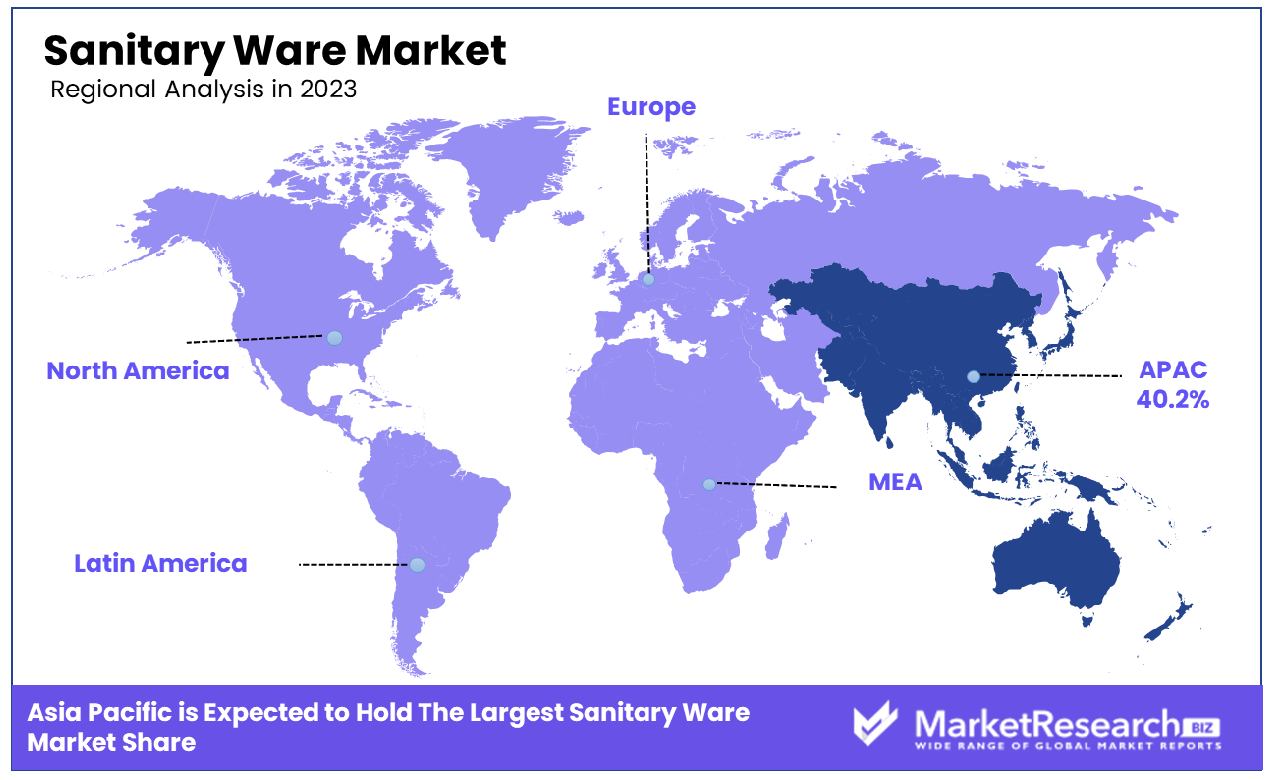

The Asia Pacific leads the sanitary ware market, holding a substantial 40.2% of the global share.

The global sanitary ware market is segmented across several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each presenting unique growth dynamics and opportunities.

Asia Pacific is the dominant region in the sanitary ware market, accounting for 40.2% of the global market share. This region's dominance is driven by rapid urbanization, increasing population, and significant investments in infrastructure development across major economies such as China and India. The demand in Asia Pacific is further bolstered by the expanding middle class and increasing emphasis on sanitation and hygiene, stimulated by government initiatives aimed at improving public health facilities.

In North America, the market is characterized by a preference for high-end, technologically advanced sanitary ware products, reflecting the region’s strong focus on innovation and quality. This market benefits from the established infrastructure and consumer preference for eco-friendly and water-efficient products, aligning with stringent environmental regulations.

Europe mirrors North America in its demand for eco-friendly products but adds a strong emphasis on aesthetic and design, driven by its rich history in craftsmanship and luxury goods. European consumers highly value sustainability, which influences their purchasing decisions towards sanitary ware products that combine functionality with minimal environmental impact.

The Middle East & Africa region is experiencing growth due to increased construction activities in the residential and commercial sectors, particularly in the Gulf Cooperation Council (GCC) countries, driven by economic diversification efforts away from oil.

Latin America, though smaller in market size compared to Asia Pacific, shows potential due to urbanization and improving economic conditions, which are gradually enhancing consumer spending on home improvements, including bathroom renovations.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global sanitary ware market is characterized by the presence of several key players that contribute to the industry's competitive dynamics and innovation. Among these, companies like CERA Sanitaryware Limited, Cersanit, and Duravit AG are recognized for their strong market presence, particularly in regional markets. For instance, CERA Sanitaryware Limited leverages its extensive distribution network in India to capture a significant share of the burgeoning market in Asia Pacific.

Geberit AG and Toto Ltd stand out for their commitment to technological innovation, especially in the development of water-efficient and smart sanitary products. Geberit’s dominance in the European market is augmented by its advanced flushing systems and water-saving technologies, which align well with the region’s stringent environmental regulations. Similarly, Toto Ltd is a leader in the Japanese market, renowned for its high-tech toilet systems that incorporate comfort and hygiene innovations.

Companies like Jaquar Group and Kohler Co. have expanded their global footprint by focusing on luxury and designer sanitary ware products that offer both aesthetic appeal and functional superiority. Kohler, in particular, is noted for its innovative designs and smart home integration, making it a strong competitor in North America and Europe.

Smaller regional players like Lecico Egypt and Saudi Ceramics cater to the Middle East & Africa markets, where there is increasing demand for both standard and high-end products due to ongoing infrastructure and residential development.

Market Key Players

- CERA Sanitaryware Limited

- Cersanit

- Duravit AG

- Geberit AG

- H & R Johnson

- Hindware Homes

- Jaquar Group

- Kohler Co.

- Lecico Egypt

- Roca Sanitario S.A.

- Saudi Ceramics

- Toto Ltd

- Villeroy & Boch

Recent Development

- In May 2024, H & R Johnson launched an eco-friendly sanitary ware line in May 2024, made from recycled ceramics. This initiative is part of their sustainability strategy, expected to reduce their carbon footprint by 30% and attract environmentally conscious consumers.

- In April 2024, Geberit AG secured a $50 million investment to enhance its manufacturing facilities. This funding will be used to adopt advanced manufacturing technologies, aiming to improve product quality and reduce production costs by 15%.

- In March 2024, CERA Sanitaryware Limited launched a new range of water-efficient toilets designed to reduce water usage by up to 40%. This product line aims to cater to the increasing consumer demand for environmentally friendly home products.

Report Scope

Report Features Description Market Value (2023) USD 12.6 Billion Forecast Revenue (2033) USD 21.4 Billion CAGR (2024-2032) 5.6% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology(Spangles, Slip Casting, Pressure Coating, Jiggering, Isostatic Casting, Others), By Product Type(Urinals, Washbasins & Kitchen Sinks, Bidets, Water Closets, Faucets, Others), By Distribution Channel(Online, Offline), By End-User(Commercial, Residential, Personal) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape CERA Sanitaryware Limited, Cersanit, Duravit AG, Geberit AG, H & R Johnson, Hindware Homes, Jaquar Group, Kohler Co., Lecico Egypt, Roca Sanitario S.A., Saudi Ceramics, Toto Ltd, Villeroy & Boch Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- CERA Sanitaryware Limited

- Cersanit

- Duravit AG

- Geberit AG

- H & R Johnson

- Hindware Homes

- Jaquar Group

- Kohler Co.

- Lecico Egypt

- Roca Sanitario S.A.

- Saudi Ceramics

- Toto Ltd

- Villeroy & Boch

Our Clients

View Our Licence Options