Global Protective Textiles Market By Material(Aramid & Blends, Polyamide, Laminated Polyesters, Cotton Fibers, Polyolefin & Blends, Others), By Application(Mechanical, Thermal, Electrical, Chemical, Radiation, Others), By End-Use(Defence, Manufacturing and Construction, Mining, Oil and Gas, Space Exploration, Healthcare, Emergency Services, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

7585

-

June 2024

-

300

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

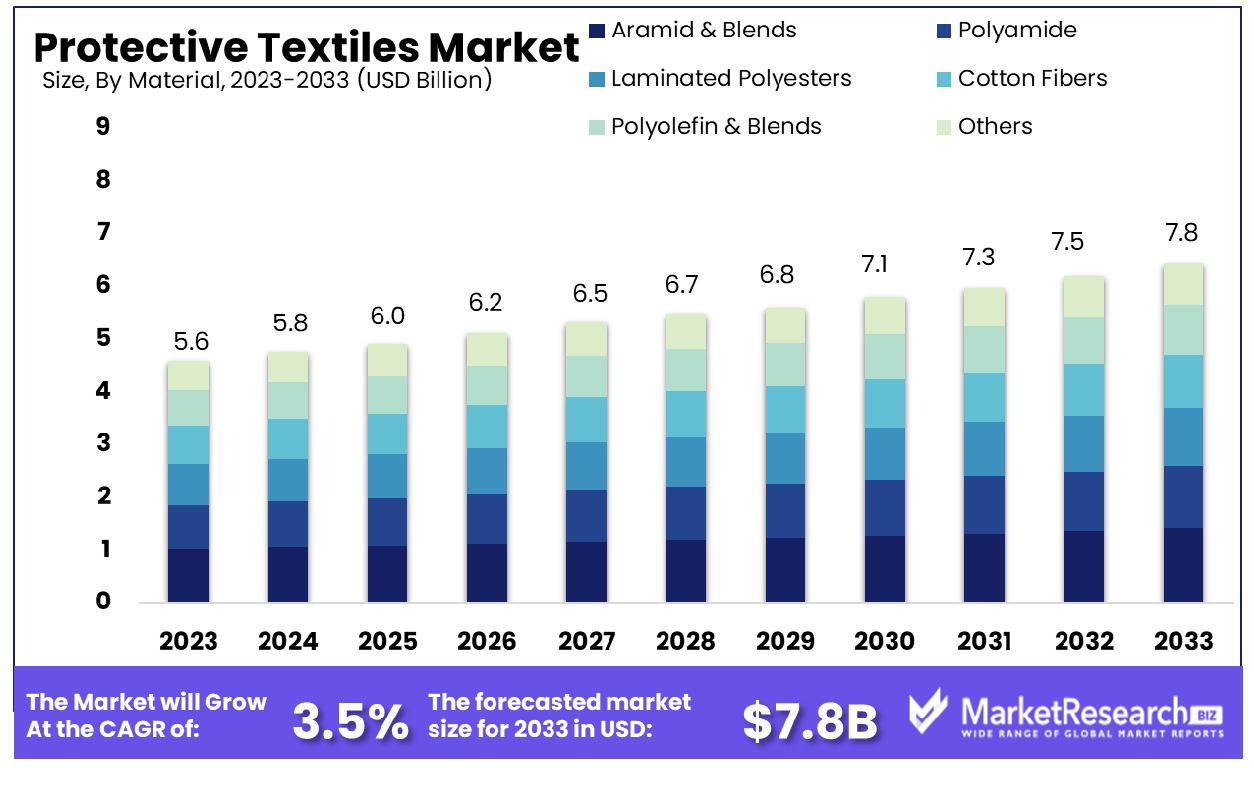

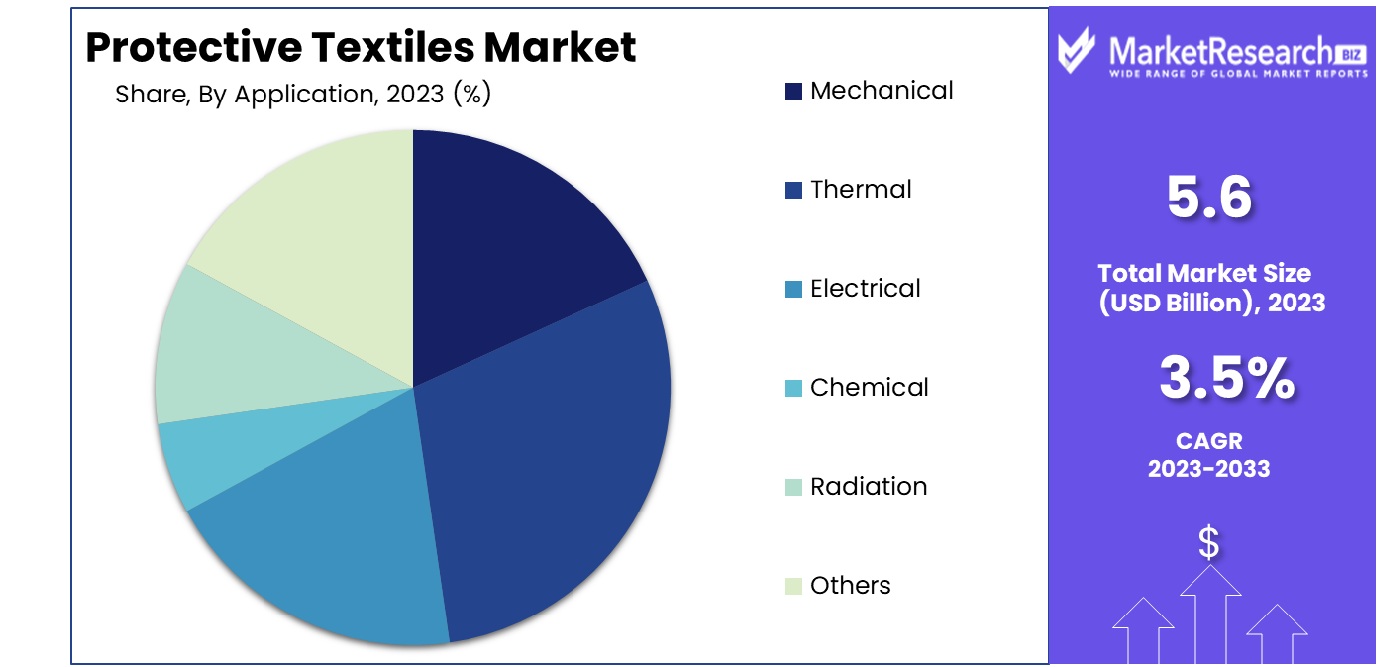

The Global Protective Textiles Market was valued at USD 5.6 billion in 2023. It is expected to reach USD 7.8 billion by 2033, with a CAGR of 3.5% during the forecast period from 2024 to 2033.

The Protective Textiles Market encompasses advanced fabric technologies designed to safeguard individuals from environmental hazards, including extreme temperatures, chemical exposures, and physical injuries. These textiles are integral to sectors such as defense, firefighting, healthcare, and construction, where safety is paramount. The market’s offerings include fire-resistant clothing, chemical-defensive gear, and ballistic protection, tailored to meet stringent safety standards.

As industries prioritize worker safety and regulatory compliance, the demand for these specialized textiles grows, presenting significant opportunities for innovation and market expansion. This market's evolution is crucial for companies looking to enhance occupational safety and reduce liability.

The Protective Textiles Market is positioned for substantial growth, driven by increasing demand across various industrial sectors prioritizing safety and regulatory compliance. As of 2020, the market was valued at approximately $16 billion and is anticipated to expand at a compound annual growth rate (CAGR) of 12-14%. By 2024, it is projected to reach a valuation of $20-23 billion. This growth trajectory is supported by technological advancements in material science, which enhance the protective capabilities of textiles used in hazardous environments.

Key sectors fueling this demand include construction, healthcare, defense, and firefighting. Companies operating in these industries seek innovative textile solutions that offer superior protection against a broad spectrum of threats, ranging from fire and chemicals to biological hazards and ballistic impacts. As these textiles evolve to meet stringent safety standards globally, they also open new avenues for market participants to innovate and capture emerging opportunities. Thus, stakeholders in the Protective Textiles Market must focus on scaling up production capabilities, enhancing material properties, and expanding their product offerings to leverage the growth potential fully.

Key Takeaways

- Market Growth: The Global Protective Textiles Market was valued at USD 5.6 billion in 2023. It is expected to reach USD 7.8 billion by 2033, with a CAGR of 3.5% during the forecast period from 2024 to 2033.

- Regional Dominance: Asia Pacific holds 45.2% of the global protective textiles market.

- By Material: Aramid & Blends dominated, holding a 40% market share in materials.

- By Application: Thermal application leads with 35% dominance in market usage.

- By End-Use: Manufacturing and construction lead, occupying 30% of market end-use share.

Driving factors

Increasing Safety Regulations and Standards in Industries

The enforcement of stringent safety regulations and standards across various industries fundamentally drives the demand for protective textiles. As governments globally intensify their focus on worker safety to mitigate occupational hazards, the market for protective textiles is experiencing substantial growth. For instance, regulations such as OSHA (Occupational Safety and Health Administration) in the United States mandate the use of protective clothing in several high-risk industries including construction, chemical, and oil and gas.

These regulations ensure a steady demand for protective textiles designed to shield workers from chemical exposure, extreme temperatures, and mechanical risks. This regulatory push is not only enhancing worker safety but also propelling the expansion of the protective textiles market.

Growing Demand from the Military and Defense Sector

The military and defense sector represents a significant driver of growth for the protective textiles market. With increasing geopolitical tensions and a heightened focus on personnel safety, there is a robust demand for advanced protective gear. Protective textiles are integral in manufacturing uniforms that offer ballistic protection, flame resistance, and chemical and biological hazard resistance.

The ongoing innovations and investments in military gear, aimed at improving the comfort and effectiveness of protective clothing, further stimulate market growth. The defense sector's stringent requirements for durable and technologically advanced textiles underscore its pivotal role in expanding the protective textiles market.

Technological Advancements in Textile Materials

Technological advancements in textile materials are revolutionizing the protective textiles market, enhancing both the functionality and appeal of these products. Innovations such as nanotechnology, which involves the manipulation of fibers at the molecular level, result in textiles that are lighter, stronger, and more adaptable to various environmental conditions.

For instance, the development of textiles that can change their properties in response to temperature fluctuations or exposure to hazardous chemicals is increasing their applicability across diverse industries. This technological progression not only meets the evolving demands of end-users but also opens new avenues for market growth by expanding the applications of protective textiles in emerging sectors like extreme sports and space exploration.

Restraining Factors

Impact of High Costs on Market Expansion for Protective Textiles

The high cost of advanced protective fabrics significantly influences the market dynamics of protective textiles. These textiles often incorporate specialized materials and technologies designed to ensure high performance in extreme conditions, such as resistance to chemicals, fire, and abrasion. The development and integration of these advanced features involve substantial research and development expenditures, alongside the use of costly raw materials.

Consequently, the final products are priced higher, potentially limiting their accessibility and adoption across various sectors, especially in cost-sensitive markets such as developing countries. This cost barrier can restrain market growth as potential buyers opt for less expensive, albeit less effective, alternatives. Therefore, managing and reducing production costs without compromising quality is pivotal for expanding market reach and enhancing the adoption rate of high-performance protective textiles.

Challenges in Recycling and Environmental Concerns

The environmental impact associated with synthetic protective textiles presents a significant challenge for the market. These materials are often non-biodegradable and complex to recycle, leading to considerable waste management issues. As environmental regulations become stricter and societal awareness increases, the demand for sustainable production practices and eco-friendly materials in the textile industry has surged. This shift is prompting companies to innovate in the areas of material sustainability and recycling technologies.

However, the transition involves complex technological upgrades and can be cost-intensive. The inability to effectively address these environmental concerns could hinder market growth, as consumers and regulatory bodies increasingly favor environmentally sustainable products. Conversely, addressing these challenges effectively can open new growth avenues through the adoption of green technologies and by meeting the rising demand for sustainable protective solutions.

By Material Analysis

Aramid & Blends dominated the material segment with a substantial 40% share in the market.

In 2023, Aramid & Blends held a dominant market position in the By Material segment of the Protective Textiles Market, capturing more than a 40% share. This prominence is attributed to the superior strength, durability, and resistance to high temperatures and chemicals offered by aramid fibers, making them ideal for applications in industries such as firefighting, military, and automotive.

Following Aramid & Blends, Polyamide accounted for approximately 25% of the market share. Specialty polyamide materials are favored for their excellent abrasion resistance and flexibility, which are essential for protective apparel in the construction and manufacturing sectors.

Laminated Polyesters have also carved a significant niche, securing about 15% of the market. These materials are primarily utilized for their waterproof and windproof properties in outdoor and weather-exposed environments.

Cotton Fibers, known for their comfort and breathability, maintained a 10% share of the market. Despite lower durability, their demand persists in less hazardous environments where comfort is prioritized.

Polyolefin & Blends, comprising around 7% of the market, are selected for their lightweight and non-conductive properties, particularly in electric hazard applications.

The remaining 3% is distributed among other materials, which include newer, innovative fabrics that are gaining traction for specific niche applications that require unique protective properties.

The dominance of Aramid & Blends in the market is reinforced by ongoing technological advancements and product innovations aimed at enhancing the performance characteristics of protective textiles. As industries continue to enforce stringent safety standards, the demand for advanced protective materials is expected to grow, further influencing market dynamics and investment trends in this sector.

By Application Analysis

In applications, thermal protective textiles led, accounting for 35% of the market dominance.

In 2023, the Protective Textiles Market was segmented by application into Mechanical, Thermal, Electrical, Chemical, Radiation, and Others. Among these, the Thermal segment held a dominant market position, capturing more than a 35% share. This significant market share can be attributed to the increasing demand for thermal protective clothing across various industries including firefighting, oil and gas, and construction, where protection against extreme heat and flames is critical.

The prominence of the Thermal segment is driven by technological advancements in material science that enhance the thermal resistance of fabrics while maintaining comfort and durability. Innovations such as the integration of nanotechnology and the development of hybrid materials have further boosted the efficacy and attractiveness of thermal protective textiles.

Meanwhile, the Mechanical segment also showed considerable growth, driven by the need for protection against mechanical hazards like abrasions, punctures, and cuts in sectors such as automotive, manufacturing, and construction. Electrical protective textiles are increasingly in demand due to the rising focus on safety standards in electrical and utility industries. Chemical and Radiation protective textiles are similarly advancing, with improvements in chemical resistance and the incorporation of materials that provide safety from hazardous exposures and radiological threats.

The segment labeled 'Others,' which includes applications such as biological protection and UV resistance, is growing as well, spurred by rising awareness of workplace safety and the diverse requirements of various industries. Each segment’s growth is supported by regulatory standards mandating higher safety measures, which influence the development and adoption of advanced protective textiles across the globe.

By End-Use Analysis

Manufacturing and construction emerged as the top end-use category, dominating 30% of the market.

In 2023, Manufacturing and Construction held a dominant market position in the By End-Use segment of the Protective Textiles Market, capturing more than a 30% share. This sector's significant share is primarily driven by the heightened need for protective apparel that shields against mechanical, chemical, and thermal hazards prevalent in these industries.

Defence followed, accounting for approximately 20% of the market. The demand in this sector is fueled by the critical need for ballistic protection, fire resistance, and chemical defense in military applications.

The Oil and Gas industry secured around 15% of the market share, where the requirement for protective clothing is essential to safeguard workers from oil-based hazards, fires, and extreme environmental conditions.

Mining industry contributions stood at 10%, driven by the necessity for durable and robust protective gear that offers high levels of safety against underground hazards, including falling objects and moisture.

Healthcare, which includes protective garments for biological and chemical protection, captured about 8% of the market, a figure that has been influenced by global health dynamics and heightened awareness of personal protective equipment.

Emergency Services accounted for 7% of the market, emphasizing the critical need for fire-resistant and waterproof materials in rescue and firefighting operations.

Space Exploration and Others, although smaller in their market share contributions at around 5% each, highlight niche areas with specialized requirements for high-tech protective solutions designed to withstand extreme conditions and provide maximum safety.

The dominance of the Manufacturing and Construction sector is likely to persist as technological advancements continue to introduce more durable, flexible, and safer materials, catering to stringent workplace safety regulations and evolving industry requirements.

Key Market Segments

By Material

- Aramid & Blends

- Polyamide

- Laminated Polyesters

- Cotton Fibers

- Polyolefin & Blends

- Others

By Application

- Mechanical

- Thermal

- Electrical

- Chemical

- Radiation

- Others

By End-Use

- Defence

- Manufacturing and Construction

- Mining

- Oil and Gas

- Space Exploration

- Healthcare

- Emergency Services

- Others

Growth Opportunity

Development of Lightweight and More Comfortable Protective Clothing

The global Protective Textiles Market stands at the cusp of transformation in 2023, largely propelled by the development of lightweight and more comfortable protective clothing. This evolution is not just a trend but a significant growth opportunity, as comfort and wearability directly influence user compliance and market penetration. Innovations that reduce the weight of protective garments while maintaining or enhancing their protective features cater to a broader range of industries, from healthcare to construction and beyond.

This shift towards more ergonomic protective solutions is likely to attract a wider demographic, including sectors that have traditionally hesitated to adopt standard protective gear due to discomfort and mobility restrictions. The strategic focus on lightweight materials could be particularly instrumental in boosting product adoption rates and expanding the market's footprint.

Expansion into Emerging Markets with Growing Industrial Sectors

2023 presents a substantial growth avenue for the Protective Textiles Market through expansion into emerging markets, which are witnessing rapid industrialization. Regions such as Asia-Pacific, Latin America, and parts of Africa are seeing an influx of industrial investments and a corresponding rise in labor-intensive industries. These markets offer untapped potential due to lower penetration of protective textiles and burgeoning awareness of worker safety norms.

Capitalizing on this opportunity involves navigating diverse regulatory landscapes and establishing robust distribution channels. However, the long-term benefits include establishing early dominance in these markets, fostering brand loyalty, and driving volume growth. As these emerging markets continue to develop their infrastructure and industrial capabilities, the demand for protective textiles is expected to surge, providing a sustained growth trajectory for the industry.

Latest Trends

Nanotechnology's Role in Enhancing Protective Textiles

In 2023, the incorporation of nanotechnology in protective textiles signifies a groundbreaking trend, transforming market prospects dramatically. Nanotechnology involves manipulating materials at an atomic or molecular scale to imbue textiles with enhanced properties such as increased strength, chemical resistance, and durability. These nano-enhanced fabrics are pivotal in sectors requiring high-performance gear, including military, firefighting, and healthcare.

By integrating nanotechnology, manufacturers are able to offer products that not only provide superior protection but also improve comfort and functionality, which is crucial for user acceptance and satisfaction. The adoption of this technology is poised to drive significant growth within the protective textiles market by fulfilling stringent safety standards and adapting to evolving industry requirements. This trend is expected to garner substantial investment as companies strive to innovate and capture market share in an increasingly competitive landscape.

Expansion Through Smart Textiles with Integrated Sensors

The rise in the adoption of smart textiles equipped with integrated sensors marks another prominent trend shaping the protective textiles market in 2023. These textiles are embedded with sensors that monitor various health and environmental parameters, offering real-time data to enhance safety and performance. Applications range from monitoring vital signs in healthcare settings to tracking hazardous exposures in industrial environments.

The integration of these technologies addresses the growing demand for interconnected, intelligent safety solutions, particularly in industries where real-time data can significantly impact safety outcomes and operational efficiency. As businesses increasingly prioritize worker safety and regulatory compliance, the market for smart protective textiles is expected to witness robust growth. This trend also aligns with the broader movement towards the Internet of Things (IoT), positioning smart textiles at the forefront of technological integration in protective gear.

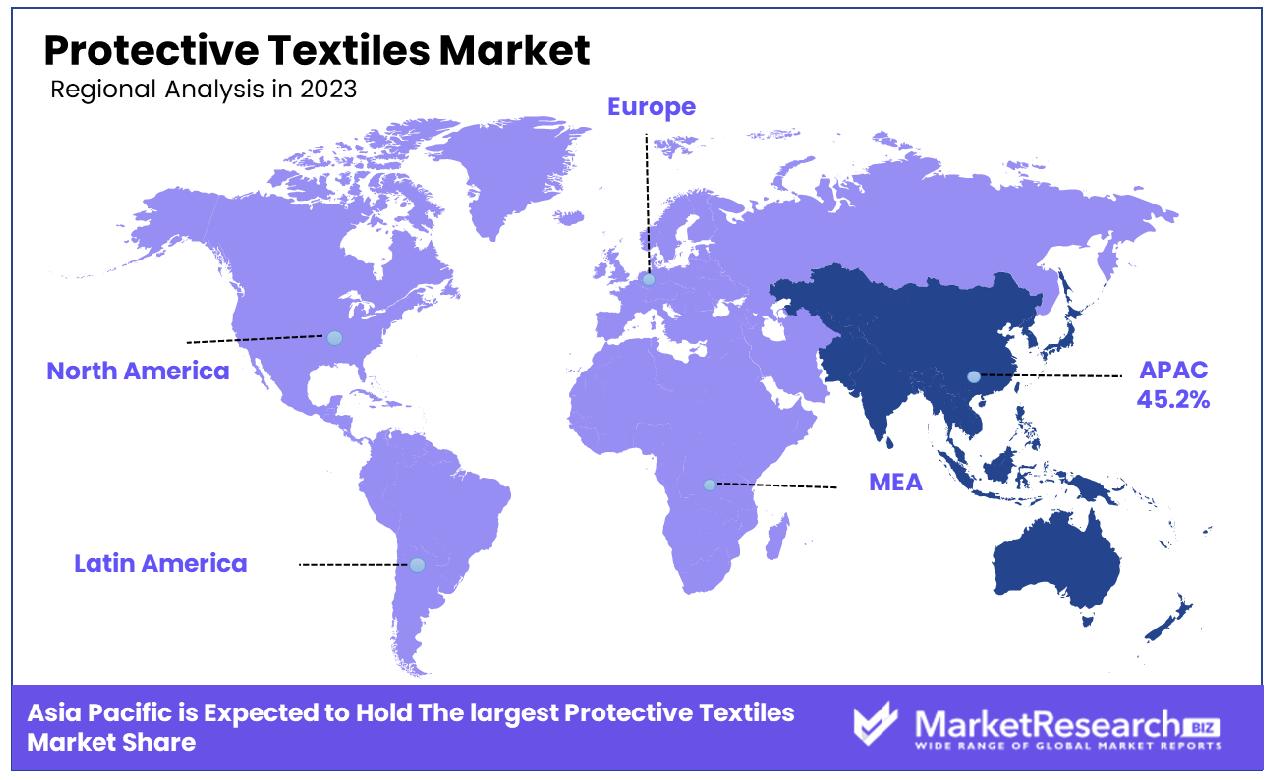

Regional Analysis

In 2023, the Asia Pacific region held a 45.2% share of the global protective textiles market.

In North America, the market is characterized by a well-established industrial sector and stringent safety regulations which drive the demand for high-standard protective clothing. Advanced manufacturing techniques and the presence of leading market players also contribute to the robust market size in this region.

Europe follows closely, with a strong emphasis on safety standards and worker protection, especially in the industrial and chemical sectors. The European market benefits from proactive government policies that enforce strict safety and health protocols, fostering growth in the protective textiles sector.

Asia Pacific stands as the dominating region in the protective textiles market, holding a substantial 45.2% market share. This dominance is driven by rapid industrialization in emerging economies like China and India, coupled with increasing awareness regarding worker safety. The region's competitive manufacturing capabilities and expanding industrial workforce provide a fertile ground for the protective textiles market to thrive.

The Middle East & Africa and Latin America regions, though smaller in market size compared to others, are witnessing growth due to developing industrial sectors and rising standards for workplace safety. These regions present significant growth opportunities, driven by urbanization and governmental initiatives to enhance industrial safety standards.

Collectively, these regional markets underscore the global reach and diverse application spectrum of the Protective Textiles Market, each contributing uniquely to the industry's growth trajectory with Asia Pacific leading the charge due to its expansive industrial activities and escalating safety requirements.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global protective textiles market will be influenced significantly by the activities and innovations of several key companies. DuPont, a leader in this sector, continues to drive advancements with its cutting-edge materials science expertise, enhancing the performance and durability of protective fabrics. Royal Ten Cate NV leverages its broad portfolio to cater to diverse industries, reinforcing its presence in global markets through strategic innovations and collaborations.

W. L. Gore & Associates, Inc. remains pivotal in shaping the market through their proprietary technologies in waterproof and breathable barriers, which are critical in protective clothing for extreme environments. Meanwhile, Kusumgar Corporates and DyStar Group are expanding their footprint by focusing on compliance with stringent environmental standards and enhancing the functional aspects of protective textiles.

Schoeller Textil AG stands out for its commitment to sustainability and technological integration, developing fabrics that offer both protection and comfort without compromising on environmental values. In contrast, ARGAR S.r.l specializes in technical knitted fabrics, providing tailored solutions that meet the specific needs of their clients, demonstrating flexibility and innovation in design.

Madhuram Fabrics Pvt. Ltd. and Teijin Limited are also noteworthy for their contributions to the market, with Teijin focusing on the integration of high-performance fibers to create advanced protective solutions. PBI Performance Products, Inc. emphasizes the development of high-heat-resistant fabrics, crucial for firefighting and industrial applications.

These companies collectively drive the protective textiles market forward through a blend of innovative material technologies, strategic market expansions, and a strong focus on sustainability and customer-specific solutions. Their efforts are set to not only lead but also transform the market landscape in 2023 and beyond.

Market Key Players

- DuPont

- Royal Ten Cate NV

- W. L. Gore & Associates, Inc.

- Kusumgar Corporates

- DyStar Group

- Schoeller Textil AG

- ARGAR S.r.l

- Madhuram Fabrics Pvt. Ltd.

- Teijin Limited

- PBI Performance Products, Inc., and more.

Recent Development

- In March 2024, Kusumgar Corporates received a $30 million investment in March 2024 to enhance their manufacturing facilities. This investment is aimed at boosting production capabilities for high-tech protective textiles used in military and aerospace applications.

- In February 2024, DuPont introduced a new line of fire-resistant fabrics under their renowned Nomex brand. This line enhances protection for workers in hazardous environments and represents a significant advancement in their protective textile offerings.

- In January 2024, DyStar Group announced in January 2024 the acquisition of a smaller chemical producer that specializes in environmentally friendly dyes for protective textiles. This acquisition is part of their strategy to offer more sustainable options in their product line.

Report Scope

Report Features Description Market Value (2023) USD 5.6 Billion Forecast Revenue (2033) USD 7.8 Billion CAGR (2024-2032) 3.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Material(Aramid & Blends, Polyamide, Laminated Polyesters, Cotton Fibers, Polyolefin & Blends, Others), By Application(Mechanical, Thermal, Electrical, Chemical, Radiation, Others), By End-Use(Defence, Manufacturing and Construction, Mining, Oil and Gas, Space Exploration, Healthcare, Emergency Services, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape DuPont, Royal Ten Cate NV, W. L. Gore & Associates, Inc., Kusumgar Corporates, DyStar Group, Schoeller Textil AG, ARGAR S.r.l, Madhuram Fabrics Pvt. Ltd., Teijin Limited, PBI Performance Products, Inc., and more. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- DuPont

- Royal Ten Cate NV

- W. L. Gore & Associates, Inc.

- Kusumgar Corporates

- DyStar Group

- Schoeller Textil AG

- ARGAR S.r.l

- Madhuram Fabrics Pvt. Ltd.

- Teijin Limited

- PBI Performance Products, Inc., and more.

Our Clients

View Our Licence Options