Global Professional Service Automation Software Market By Component(Solutions, Services), By Solutions(Project Management, Project Accounting, Billing & Invoice Management, Project Analytics), By Services(System Integration Services, Consulting, Training and Support), By Deployment(Cloud, On-premise), By Enterprise Size(Large Enterprises, Small & Medium Enterprises), By Application(Consulting Firms, Technology Companies), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

49395

-

July 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

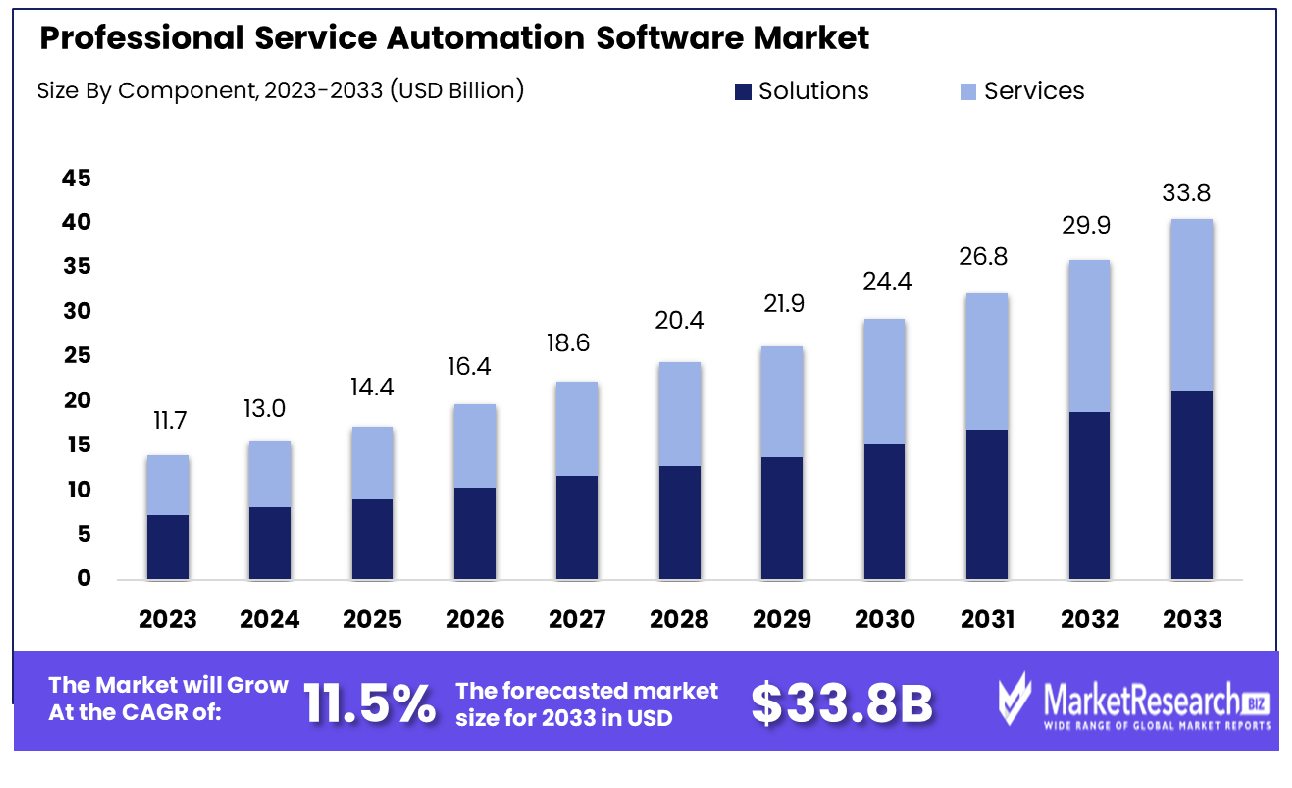

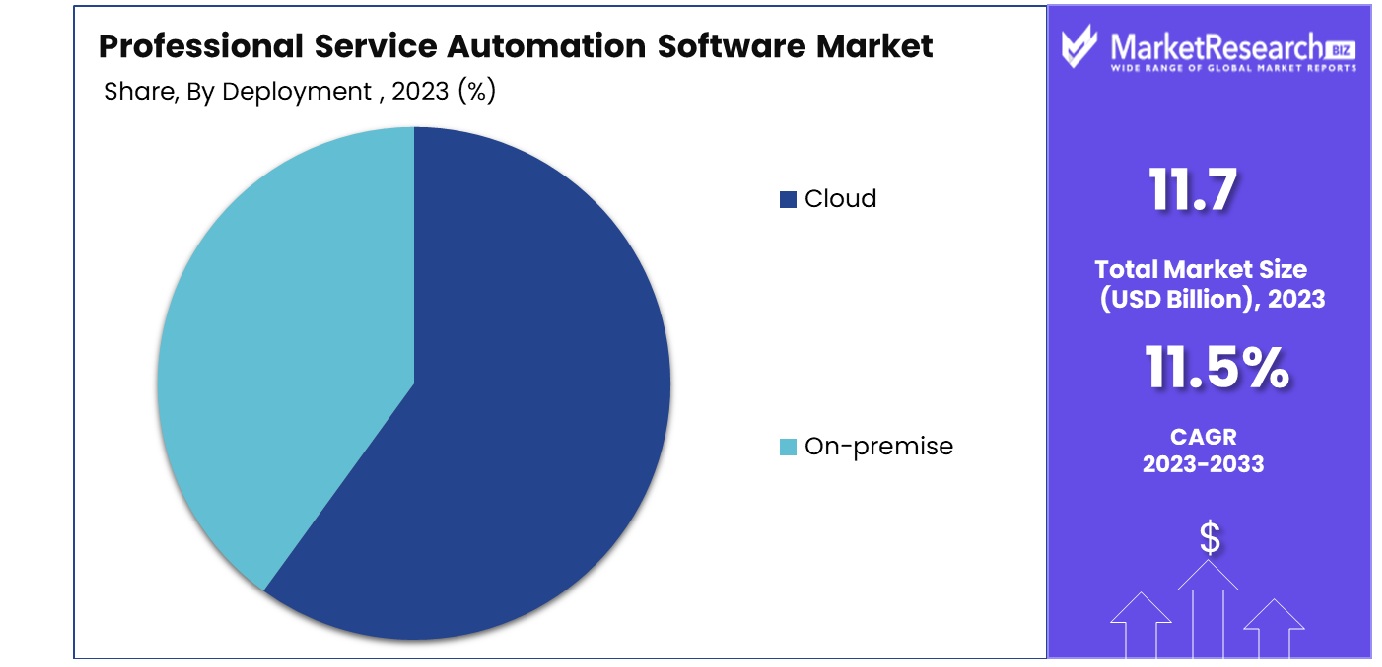

The Global Professional Service Automation Software Market was valued at USD 11.7 billion in 2023. It is expected to reach USD 33.8 billion by 2033, with a CAGR of 11.5% during the forecast period from 2024 to 2033.

The Professional Service Automation (PSA) Software Market encompasses a suite of tools designed to optimize the management of project-based operations within professional service firms. These solutions facilitate core functions such as project management, resource allocation, time tracking, and billing, integrating these components to enhance operational efficiency and profitability.

Tailored for decision-makers such as Product Managers, PSA software provides crucial insights into project performance, financial health, and resource utilization, enabling informed strategic decisions and improved client delivery. As businesses seek greater transparency and efficiency, the demand for such integrated solutions is rapidly expanding within the professional services sector.

The Professional Service Automation (PSA) Software Market is witnessing a robust growth trajectory, with projections indicating an escalation from $3.6 billion in 2022 to $5.2 billion by 2027, translating to a compound annual growth rate (CAGR) of 7.6%. This significant expansion underscores the critical role that PSA software plays in enhancing operational efficiencies within professional services firms. Currently, approximately 50% of these firms have integrated PSA solutions into their operational frameworks, signaling a shift towards more structured and efficient project management practices.

Key drivers catalyzing the adoption of PSA software include the imperative to improve resource utilization, which 54% of service providers identify as a primary motivator. Furthermore, 48% of firms seek to enhance project visibility, while 47% aim to streamline processes related to billing and invoicing. These factors collectively foster a conducive environment for the adoption of PSA tools, as firms strive to optimize both internal processes and client-facing outcomes.

From a strategic standpoint, the increasing reliance on PSA software is indicative of a broader trend toward digitization and automation in professional services. The integration of these systems enables firms to attain a holistic view of project metrics and financials, thereby facilitating informed decision-making and improved operational agility. As the market matures, the adoption of PSA software is expected to permeate deeper within the industry, driven by the growing recognition of its strategic benefits in maintaining competitiveness and enhancing service delivery.

Key Takeaways

- Market Growth: The Global Professional Service Automation Software Market was valued at USD 11.7 billion in 2023. It is expected to reach USD 33.8 billion by 2033, with a CAGR of 11.5% during the forecast period from 2024 to 2033.

- North America dominates with 44.1% of the Professional Service Automation market.

- By Component: The Solutions component dominates, holding a 70% share of the market.

- By Solutions: Project Management leads the solutions segment with a 30% market share.

- By Services: Consulting services dominate, capturing 40% of the services segment.

- By Deployment: Cloud deployment is predominant, securing 65% of the market.

- By Enterprise Size: Large enterprises lead, representing 55% of the enterprise segment.

- By Application: Technology companies are the top application, holding a 35% share.

Driving factors

Enhanced Operational Efficiency in Service Organizations

The Professional Service Automation (PSA) Software Market is significantly driven by the increasing need for enhanced operational efficiency in service organizations. PSA software streamlines various aspects of project management, resource allocation, and billing, which are critical for optimizing operations and improving service delivery.

This integration facilitates the effective management of project timelines and budgets, reduces overhead costs, and enhances workforce productivity. As organizations strive to maximize their output with minimal resources, the demand for solutions that can automate routine tasks and consolidate project data increases, thus propelling the growth of the PSA software market.

Adoption of Cloud-Based Solutions

The growth of the PSA software market is further catalyzed by the growing adoption of cloud-based solutions. Cloud-based PSA software offers several advantages, including scalability, remote accessibility, and reduced IT overhead. This makes it particularly attractive to businesses looking to expand their operations without substantial upfront investments in infrastructure.

According to industry statistics, cloud deployment in the PSA sector has seen a significant uptick, with enterprises increasingly preferring cloud configurations due to their cost-effectiveness and ease of integration with existing systems. This shift not only widens the market for PSA software but also enhances its adaptability across various business scales and geographies.

Automation of Business Processes

Lastly, the rise in demand for automation of business processes stands as a crucial factor boosting the PSA software market. Automation within PSA tools helps eliminate manual errors, speeds up data processing, and ensures compliance with regulatory standards, all of which are vital for maintaining competitive advantage.

As businesses increasingly focus on data-driven decision-making, the integration of automation technologies in PSA solutions enables real-time insights and analytics, leading to more informed strategic planning and execution. This growing dependency on automated systems to maintain efficiency and competitiveness in service delivery directly impacts the expansion and innovation within the PSA software market.

Restraining Factors

High Implementation Costs

A significant restraining factor in the Professional Service Automation (PSA) Software Market is the high implementation costs associated with these systems. Deploying PSA software often involves substantial initial investments in software licensing, system customization, and integration with existing IT infrastructure. For many small and medium-sized enterprises (SMEs), these costs can be prohibitive, limiting the market's expansion primarily to larger organizations that can afford such capital outlays.

Moreover, ongoing maintenance and upgrade expenses further add to the total cost of ownership, deterring budget-conscious businesses from adopting these advanced solutions. This financial barrier not only restricts the immediate uptake of PSA software but also impacts the pace at which the technology could be universally adopted across industries.

Resistance to Change from Traditional Project Management Methods

Resistance to change from traditional project management methods also poses a considerable challenge to the growth of the PSA software market. Many organizations are accustomed to conventional project management tools and methods, and shifting to a new, automated system can be met with skepticism and reluctance from both management and staff. This resistance is often rooted in the fear of the unknown, potential job displacements, and the perceived complexity of new software systems.

Overcoming these cultural and behavioral barriers requires significant change management efforts, which can slow down the adoption process and subsequently dampen the market growth rate. Integrating PSA software effectively into businesses thus involves not only technological upgrades but also a transformation in organizational culture and attitudes toward technology-driven management.

By Component

The Solutions component dominates the market, commanding a substantial 70% share of the total market.

In 2023, Solutions held a dominant market position in the By Component segment of the Professional Service Automation Software Market, capturing more than a 70% share. The significant dominance of Solutions within this market can be attributed to their critical role in integrating various functionalities that streamline project management, resource allocation, and billing operations for professional services. This sector, complemented by Services, which accounted for the remaining market share, emphasizes a comprehensive approach to improving operational efficiency and client satisfaction in professional settings.

The Solutions segment has been instrumental in offering robust platforms that enhance decision-making processes and improve the overall productivity of service-oriented organizations. As businesses increasingly rely on data-driven strategies to optimize service delivery, the demand for sophisticated solutions that provide detailed analytics and real-time insights has surged. This trend is expected to sustain the growth trajectory of the Solutions segment in the forthcoming years.

Conversely, the Services component, though smaller in market share, plays a vital role in supporting the deployment, maintenance, and customization of these software solutions. Services ensure that the software is tailored to the unique needs of each business, providing the necessary training and support to maximize the functionality and impact of the Solutions deployed.

Overall, the Professional Service Automation Software Market is poised for continued growth, with a significant push from the increasing need for streamlined project and resource management across various industries. This market dynamic underscores the importance of integrated Solutions in maintaining competitive advantage and driving business success in the professional services sector.

By Solutions

Within the Solutions category, Project Management stands out, capturing 30% of the segment's overall dominance.

In 2023, Project Management held a dominant market position in the By Solutions segment of the Professional Service Automation Software Market, capturing more than a 30% share. This segment, which outperforms other categories such as Project Accounting, Billing & Invoice Management, Resource Management, Timesheet & Expense Management, Project Analytics, Opportunity Management, Contract Management, and others (including Knowledge Management), underscores the critical need for robust project oversight tools within professional services.

Project Management solutions are integral to the efficient orchestration of project timelines, budgets, and resource allocations, making them indispensable in sectors where precision and optimal resource utilization dictate success. Their ability to provide a centralized platform for tracking project progress, identifying bottlenecks, and facilitating communication has driven their adoption across various industries.

Meanwhile, other segments like Billing & Invoice Management and Resource Management also contribute significantly to the market, though none have reached the penetration of Project Management. Billing & Invoice Management solutions streamline financial transactions and enhance fiscal accuracy, whereas Resource Management tools help in optimizing staff deployment and reducing overhead costs.

The overall market landscape for Professional Service Automation Software is characterized by a growing emphasis on integration and automation, with firms increasingly seeking comprehensive solutions that can reduce manual effort and error, thereby enhancing productivity and profitability. As businesses continue to evolve and face new operational challenges, the demand for advanced, multi-functional software solutions, particularly in project management, is expected to grow, further cementing its status as a market leader in this space.

By Services

In the Services sector, Consulting services take the lead, accounting for 40% of the market share.

In 2023, Consulting held a dominant market position in the By Services segment of the Professional Service Automation Software Market, capturing more than a 40% share. This category surpasses others within the segment, including System Integration Services and Training and Support, highlighting its pivotal role in facilitating effective software utilization across various industries.

The prominence of Consulting services can be attributed to the increasing complexity of professional service automation software systems and the need for specialized expertise to tailor these solutions to specific business requirements. Consultants play a critical role in aligning software capabilities with organizational goals, ensuring that the implementation process adds strategic value and enhances operational efficiencies.

Moreover, as businesses continue to face dynamic market conditions and evolving technological landscapes, the demand for consulting services that offer strategic guidance and expert insights into best practices for software utilization remains high. These services not only help organizations maximize their investment in professional service automation software but also equip them with the tools to adapt to changes and scale operations effectively.

While System Integration Services and Training and Support also contribute to the market, their roles are more focused on the technical implementation and user competency aspects, respectively. However, the strategic input provided by consultants drives fundamental transformations within organizations, making this service indispensable.

Given the ongoing digital transformation in many sectors, the need for consulting services within the Professional Service Automation Software Market is expected to remain robust, ensuring sustained growth and continuous innovation in how businesses manage their projects and services.

By Deployment

Cloud deployment emerges as the preferred choice, dominating the deployment options with a 65% market share

In 2023, Cloud held a dominant market position in the By Deployment segment of the Professional Service Automation Software Market, capturing more than a 65% share. This significant market share, contrasted with the On-premise deployment, highlights the ongoing shift towards cloud-based solutions across industries.

The preference for Cloud deployment is driven by its scalability, flexibility, and cost-effectiveness, allowing businesses of all sizes to access sophisticated tools without the need for substantial upfront investments in infrastructure. Cloud-based Professional Service Automation Software offers the added advantages of enhanced security, regular updates, and anywhere access, which are critical for businesses operating in dynamic and distributed environments.

Moreover, the cloud model supports real-time collaboration and data sharing, which are essential for the efficient management of projects and resources. This is particularly relevant in today’s work landscape, where remote working arrangements and team collaborations across geographical boundaries are common.

On-premise solutions, while still relevant for certain sectors with specific compliance or security requirements, are increasingly seen as less flexible and more resource-intensive. This has led to a slower growth rate for the On-premise segment compared to Cloud deployments.

As organizations continue to pursue digital transformation strategies, the adoption of cloud-based Professional Service Automation Software is expected to increase. This trend is likely to further consolidate the dominance of Cloud deployment, driven by its ability to provide robust, scalable, and cost-effective solutions that meet the evolving needs of modern businesses.

By Enterprise Size

Large Enterprises lead in enterprise size utilization, holding a significant 55% share of the market.

In 2023, Large Enterprises held a dominant market position in the By Enterprise Size segment of the Professional Service Automation Software Market, capturing more than a 55% share. This segment, compared to Small & Medium Enterprises (SMEs), underscores the substantial investments large organizations are making in sophisticated automation tools to enhance their operational efficiencies and global competitiveness.

Large enterprises often manage complex projects and extensive client portfolios, driving the need for robust professional service automation software that can integrate various business functions—such as project management, resource allocation, billing, and customer relations—into a cohesive platform. The capacity of these software solutions to handle large-scale operations, ensure compliance across different jurisdictions, and provide detailed analytics is particularly appealing to big corporations.

On the other hand, Small & Medium Enterprises also benefit from professional service automation software, but their adoption rate is slightly lower. This is primarily due to budget constraints and the scale of operations, which might not require as comprehensive a solution as that needed by larger organizations. However, SMEs are progressively recognizing the strategic value of such software in scaling operations and improving service delivery, which could drive higher adoption rates in the coming years.

As digital transformation initiatives become more pronounced across all sectors, large enterprises are expected to continue leading the demand for Professional Service Automation Software. This trend is anticipated to persist as more businesses seek to leverage advanced technological solutions to maintain a competitive edge in an increasingly digital marketplace.

By Application

Among applications, Technology Companies are the largest users, with a dominant market share of 35%.

In 2023, Technology Companies held a dominant market position in the By Application segment of the Professional Service Automation Software Market, capturing more than a 35% share. This segment outpaces others including Consulting Firms, Marketing and Communication Companies, Architecture, Engineering, and Construction Companies, Audit and Accounting Firms, Scientific Research and Development Companies, Legal Services, and Others. The strong performance of Technology Companies in this market segment reflects the critical role that automation and efficient project management play in this rapidly evolving sector.

Technology companies, which are at the forefront of innovation and digital transformation, require advanced tools that can keep pace with their dynamic project demands and intricate development cycles. Professional Service Automation Software enables these companies to streamline their operations, optimize resource management, and deliver projects on time and within budget, which is essential in a highly competitive tech industry.

Furthermore, the adoption of these solutions by technology firms often sets a benchmark for other industries, highlighting best practices in leveraging technology for business efficiency. As such, the influence of this segment extends beyond its immediate economic footprint, guiding the integration of similar technologies across other sectors.

The importance of Professional Service Automation Software in supporting the core functions of technology companies—from project tracking and client management to financial oversight and compliance—is expected to drive continued investment and innovation in this field. As businesses across all mentioned sectors strive to enhance their operational capacities, the role of such software in fostering seamless integration and automation will become increasingly pronounced.

Key Market Segments

By Component

- Solutions

- Services

By Solutions

- Project Management

- Project Accounting

- Billing & Invoice Management

- Resource Management

- Timesheet & Expense Management

- Project Analytics

- Opportunity Management

- Contract Management

- Others (Knowledge Management and Others)

By Services

- System Integration Services

- Consulting

- Training and Support

By Deployment

- Cloud

- On-premise

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises

By Application

- Consulting Firms

- Marketing and Communication Companies

- Technology Companies

- Architecture, Engineering, and Construction Companies

- Audit and Accounting Firms

- Scientific Research and Development Companies

- Legal Services

- Others

Growth Opportunity

Integration with AI and Machine Learning for Predictive Analytics

The integration of Artificial Intelligence (AI) and machine learning into Professional Service Automation (PSA) software represents a significant growth opportunity in 2023. By leveraging AI, PSA tools can offer predictive analytics capabilities that provide deeper insights into project outcomes, resource optimization, and financial forecasting. This technological advancement enables service organizations to anticipate project risks, adjust strategies proactively, and enhance decision-making processes.

As businesses increasingly prioritize data-driven strategies to maintain competitiveness, the demand for AI-enhanced PSA solutions is expected to surge. Companies that can effectively incorporate AI to not only interpret historical data but also predict future trends will likely see a substantial competitive advantage, thus driving market growth in this segment.

Expansion into Small and Medium-Sized Enterprises (SMEs)

Another pivotal growth area for the PSA software market in 2023 is its expansion into the SME sector. Traditionally, the high cost and complexity of PSA solutions have limited their adoption primarily to larger corporations. However, with the advent of more scalable, cloud-based PSA models, there is a significant opportunity to tailor these solutions for SMEs. These businesses stand to benefit immensely from the operational efficiencies and improved project visibility that PSA software offers.

By creating more affordable and user-friendly PSA solutions, vendors can tap into this underserved market segment, significantly expanding their customer base and fostering market growth. This strategic focus not only broadens the market reach but also aligns with the broader digital transformation trends observed across industries globally.

Latest Trends

Increasing Use of Mobile Applications for Remote Management

In 2023, the global Professional Service Automation (PSA) Software Market is witnessing a significant trend towards the increasing use of mobile applications for remote management. This shift is largely driven by the growing need for flexibility and accessibility in managing projects and teams, especially with the continued prevalence of remote and hybrid work arrangements. Mobile PSA applications allow managers and team members to stay connected and updated on project statuses, resource allocations, and time tracking from anywhere, at any time.

This capability enhances communication, improves project oversight, and accelerates management decision-making processes, making it an essential feature for modern service organizations. As more businesses recognize the benefits of mobile enablement in enhancing operational efficiency and employee satisfaction, the demand for mobile-friendly PSA solutions is expected to rise sharply, further driving market growth and innovation.

Development of Hybrid PSA Solutions Combining Cloud and On-Premise Functionalities

Another emerging trend in the PSA software market is the development of hybrid solutions that combine the best aspects of cloud and on-premise functionalities. These hybrid PSA systems are designed to meet the diverse needs of organizations seeking both the security and control of on-premise software and the scalability and accessibility of cloud services.

This trend caters to organizations that are cautious about fully committing to the cloud due to data security concerns or regulatory compliance issues. By offering hybrid options, PSA vendors can attract a broader range of customers, particularly in sectors like healthcare and finance where data sensitivity is paramount. The flexibility of hybrid solutions not only appeals to a wider audience but also positions vendors as adaptable and customer-centric, further stimulating market growth and differentiation in a competitive landscape.

Regional Analysis

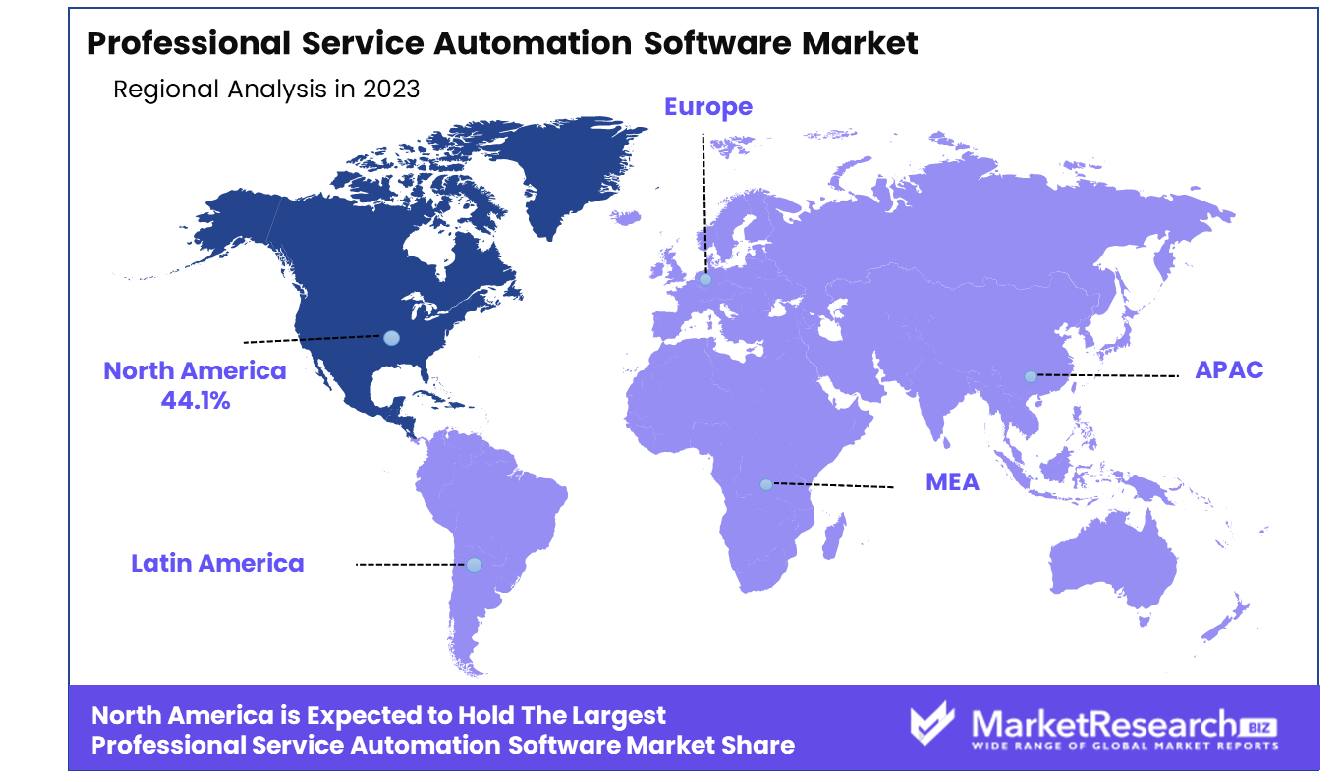

The North American region dominates the Professional Service Automation Software Market, holding a 44.1% market share.

North America holds the dominant position in the global PSA software market, accounting for 44.1% of the market share. This dominance is fueled by the presence of a robust technological infrastructure and the concentration of numerous multinational corporations with complex service management needs. The region's market leadership is further supported by high adoption rates of advanced technologies and a strong emphasis on operational efficiency in service-oriented businesses.

Europe follows, with a significant share characterized by growing demands for business efficiency and regulatory compliance across its diverse economies. European businesses are increasingly investing in PSA solutions to enhance their project management capabilities and customer relations, driving the adoption of both cloud-based and hybrid PSA systems.

In Asia Pacific, the market is expanding rapidly, thanks to the region’s growing IT services sector and increasing digital transformation initiatives. Small to medium-sized enterprises (SMEs) in this region are particularly contributing to the market growth as they seek cost-effective solutions for improving their competitive edge.

The Middle East & Africa, and Latin America regions, though smaller in market size compared to their counterparts, are experiencing gradual growth. These regions are witnessing increased adoption of PSA software due to the rising need for automation and efficient project handling in service industries, particularly in countries focused on diversifying their economies through technological advancements.

This regional segmentation underscores the varying degrees of market maturity and technological adoption across the globe, with North America leading the way in leveraging PSA software to drive business efficiency and innovation.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Professional Service Automation (PSA) Software Market is shaped significantly by the activities and innovations of key players. Among these, several companies stand out due to their strategic innovations, market expansion efforts, and robust product offerings.

Autotask Corporation and ConnectWise, Inc. are notable for their comprehensive service management solutions that cater particularly well to IT service providers, integrating seamlessly with other IT management solutions to provide a holistic service management suite.

Atlassian and Microsoft Corporation bring to the table their extensive ecosystems of collaboration and productivity tools, which integrate smoothly with their PSA offerings, making them attractive to organizations that already rely on their platforms for other business operations.

BMC Software, Inc. and Oracle Corporation are recognized for their enterprise-scale solutions, which are particularly suited to large organizations with complex service delivery models, offering extensive customization and scalability.

Deltek, Inc. and FinancialForce.com, on the other hand, focus on niche markets such as engineering and professional services firms, offering specialized solutions that cater to the unique project management needs of these sectors.

Kimble Apps and Klient, Inc. stand out for their agile and innovative approaches to PSA, emphasizing flexibility and user-friendly interfaces that appeal to dynamic and fast-growing businesses.

NetSuite OpenAir, Inc., Planview, and PROJECTOR PSA provide robust cloud-based solutions that emphasize scalability and accessibility, aligning with the needs of businesses undergoing digital transformation.

SAP SE offers deep integration capabilities with existing enterprise resource planning (ERP) systems, making it a preferred choice for organizations looking for a seamless blend of ERP and PSA functionalities.

Lastly, Upland Software, Inc., Workday, Inc., and a notable entry Comp15, demonstrate strong growth through strategic acquisitions and expansions into new market segments, enhancing their product capabilities and geographic reach.

Market Key Players

- Autotask Corporation

- Atlassian

- BMC Software, Inc.

- ConnectWise, Inc.

- Deltek, Inc.

- FinancialForce.com

- Kimble Apps

- Klient, Inc,

- Microsoft Corporation

- NetSuite OpenAir, Inc.

- Oracle Corporation

- Planview

- PROJECTOR PSA

- SAP SE

- Upland Software, Inc.

- Workday, Inc.

- Comp15

Recent Development

- In July 2023, BMC Software, Inc. acquired a startup specializing in cloud-based PSA solutions for $150 million. This acquisition aims to expand their offerings and strengthen their capabilities in managing IT services and operations.

- In May 2024, ConnectWise, Inc. announced in May 2024 a new partnership with a leading analytics firm to provide advanced data analytics capabilities in their PSA software. This partnership is expected to enhance the data-driven decision-making tools available to their users.

- In March 2024, Autotask Corporation introduced a new feature in their PSA software that integrates artificial intelligence to predict project timelines and resource needs more accurately. This enhancement is designed to improve efficiency and decision-making in project management.

Report Scope

Report Features Description Market Value (2023) USD 11.7 Billion Forecast Revenue (2033) USD 33.8 Billion CAGR (2024-2032) 11.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component(Solutions, Services), By Solutions(Project Management, Project Accounting, Billing & Invoice Management, Resource Management, Timesheet & Expense Management, Project Analytics, Opportunity Management, Contract Management, Others (Knowledge Management and Others)), By Services(System Integration Services, Consulting, Training and Support), By Deployment(Cloud, On-premise), By Enterprise Size(Large Enterprises, Small & Medium Enterprises), By Application(Consulting Firms, Marketing and Communication Companies, Technology Companies , Architecture, Engineering, and Construction Companies, Audit and Accounting Firms, Scientific Research and Development Companies, Legal Services, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Autotask Corporation, Atlassian, BMC Software, Inc., ConnectWise, Inc., Deltek, Inc., FinancialForce.com, Kimble Apps, Klient, Inc,, Microsoft Corporation, NetSuite OpenAir, Inc., Oracle Corporation, Planview, PROJECTOR PSA , SAP SE, Upland Software, Inc., Workday, Inc., Comp15 Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Autotask Corporation

- Atlassian

- BMC Software, Inc.

- ConnectWise, Inc.

- Deltek, Inc.

- FinancialForce.com

- Kimble Apps

- Klient, Inc,

- Microsoft Corporation

- NetSuite OpenAir, Inc.

- Oracle Corporation

- Planview

- PROJECTOR PSA

- SAP SE

- Upland Software, Inc.

- Workday, Inc.

- Comp15

Our Clients

View Our Licence Options