Pre Insulated Pipes Market By Material Type(Polymers, Metal & Alloys), By Pipe Configuration(Twin Pipe, Single Pipe), By Installation(Below Ground, Above Ground), By End User(District Heating and Cooling, Oil & Gas, Chemical, Pharmaceutical, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

12656

-

April 2024

-

155

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

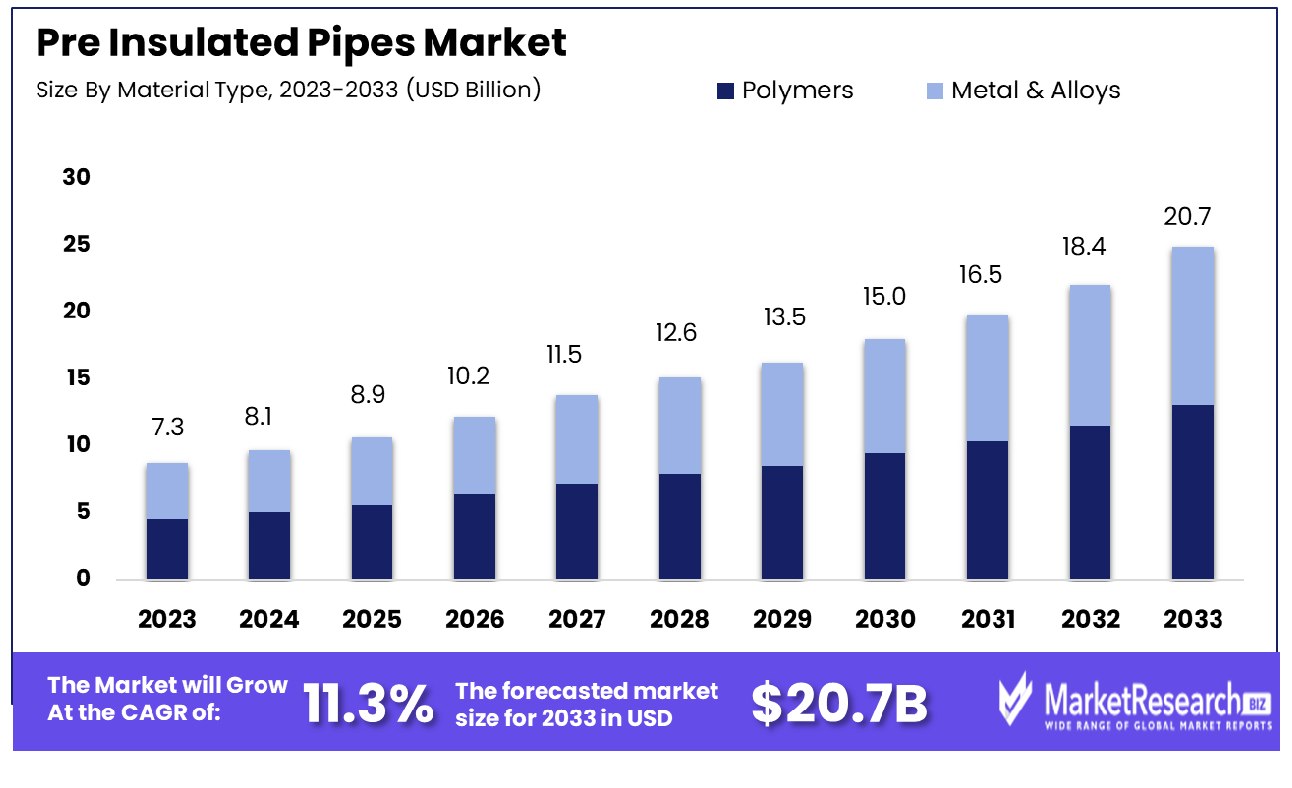

The Global Pre Insulated Pipes Market was valued at USD 7.3 billion in 2023. It is expected to reach USD 20.7 billion by 2033, with a CAGR of 11.3% during the forecast period from 2024 to 2033. The surge in demand for new advanced technologies and rise in end-use industries, and high investment in research & development are some of the main key driving factors for the pre-insulated pipes.

The pre-insulated pipes are defined as advanced piping systems that are designed for transporting liquids while decreasing heat loss or gain. Such pipes feature a layer of insulation enclosed in the inner pipes, generally made of material like polyurethane foam or mineral wool which helps in maintaining the temperature of the fluid being conveyed. These are commonly used in different industries that consist of district heating and cooling systems, hot water distribution, and industrial methods where maintaining constant temperature is important.

The insulation layer offers heat efficiency, decreasing energy consumption and operational expenses. These pipes are designed for longevity and reliability with outer casings made of materials such as high-density polyethylene and steel to safeguard the insulation and inner pipes from external factors like moisture, mechanical damage, and corrosion. The pre-insulated pipes provide an easy and effective solution for transporting fluids at controlled temperatures by maintaining constant performance and preserving energy in different applications.

According to Plasteurope in October 2022, highlights that insulating materials supplier Armacell purchased Austroflex, a manufacturer of pre-insulated pipes systems, heat solar pipes, and technical insulating materials. After the acquisition, Armacell is widening its geographical presence and business activities in Europe. The portfolio consists of flexible pipes with HDPE jacket pipes, polyurethane insulations, polyethylene foam (XPE), mineral wool, and rubber goods. At its headquarters site, the company has a production area of 55,000 m² and employs more than 80. Armacell’s business covers the divisions of advanced insulation and engineered foams, 27 production sites, 3,200 employees, and representation in 19 countries.

Last year, the company reported sales of EUR 677 MN and an EBITDA of EUR 117 MN. Pre-insulated pipes provide great advantages like decreasing thermal loss or gain, and maintaining fluid temperature integration. They lessen energy consumption by leading to saving expenses. Such pipes also need less space and labor for installations, they also offer improved sturdy against external factors and make effective fluid transportation in different industrial and commercial applications. The demand for the pre-instruction pipes will increase due to their requirement in the different construction sites that will help in market expansion in the coming years.

Key Takeaways

- Market Growth: The Global Pre Insulated Pipes Market was valued at USD 7.3 billion in 2023. It is expected to reach USD 20.7 billion by 2033, with a CAGR of 11.3% during the forecast period from 2024 to 2033.

- By Material Type: Polymers dominate due to durability, flexibility, and corrosion resistance.

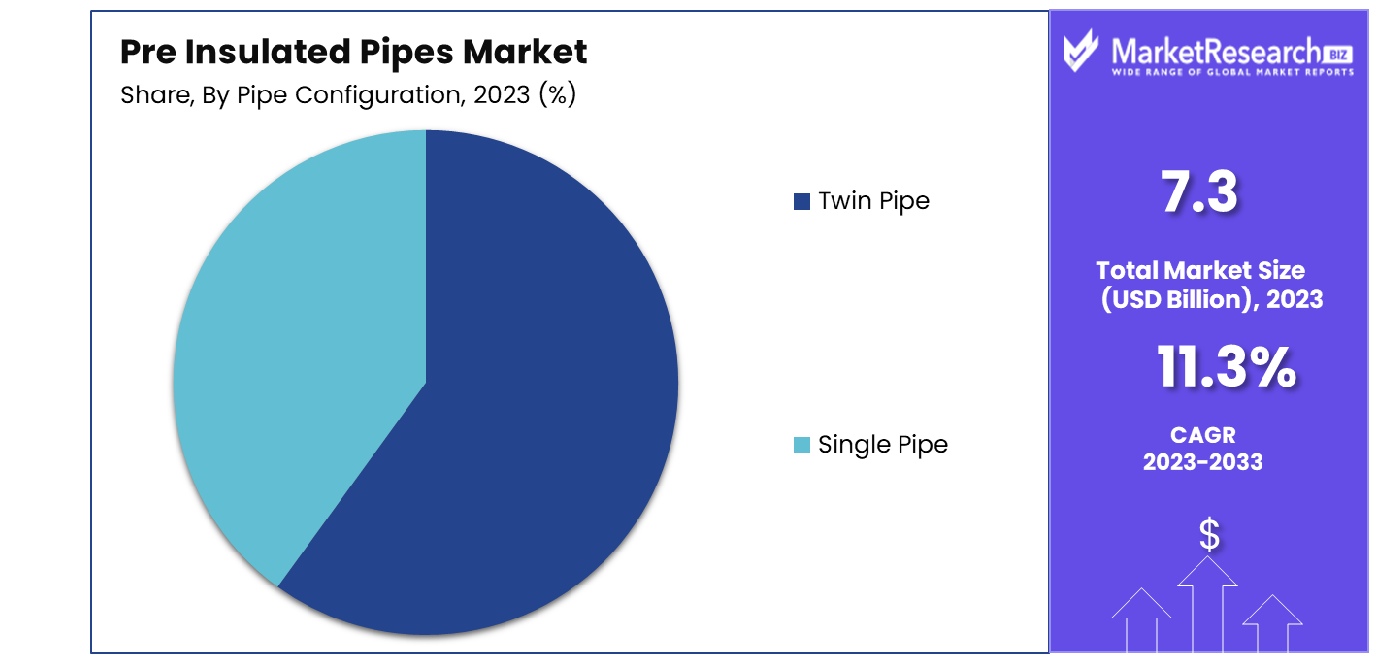

By Pipe Configuration: Twin pipe configuration enhances system reliability and efficiency significantly.

By Installation: Below-ground installation ensures minimal visual impact and environmental disruption.

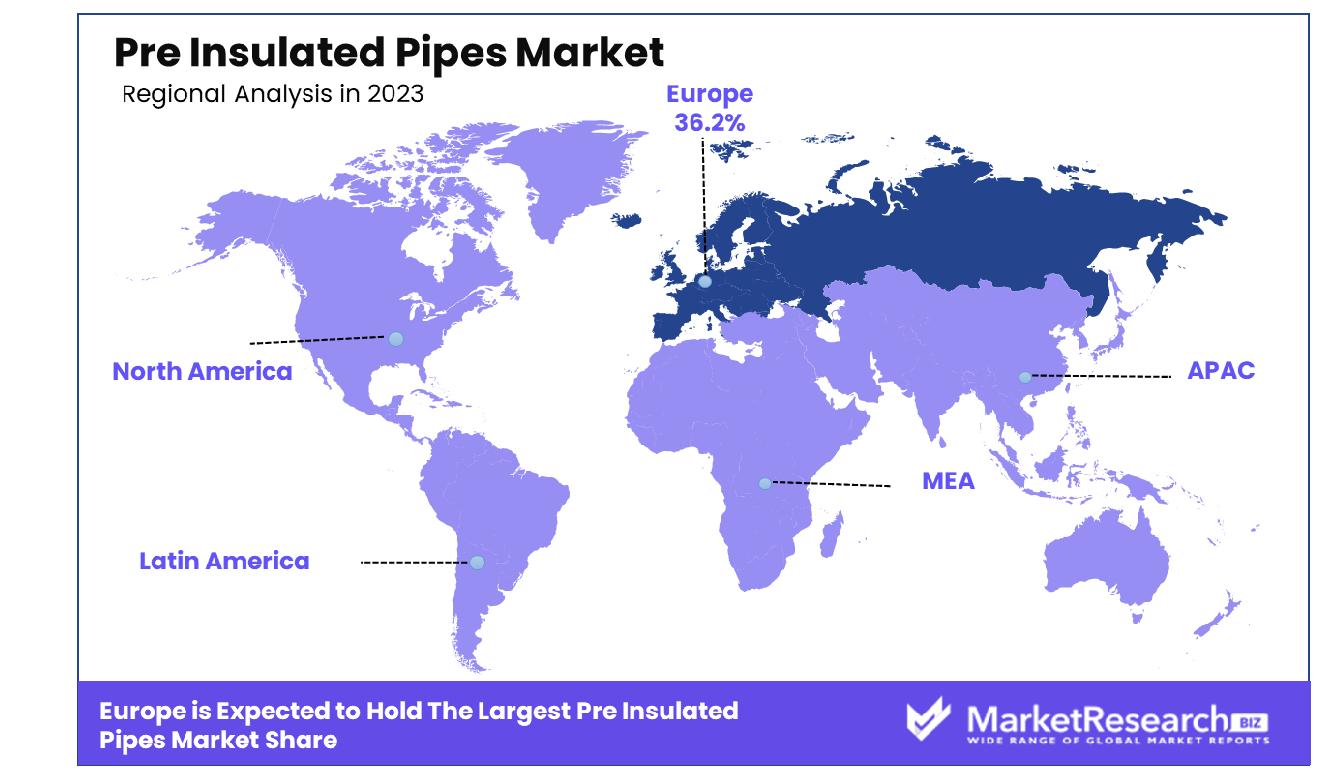

By End User: District heating and cooling end-users benefit from cost-effective, sustainable solutions. - Regional Dominance: In Europe, the pre-insulated pipes market holds a substantial 36.2% share.

- Growth Opportunity: The global pre-insulated pipes market in 2023 presents opportunities driven by infrastructure development in emerging economies, the adoption of energy-efficient solutions in construction, and expansion into industrial applications like oil and gas pipelines.

Driving factors

Government Regulations Driving Demand for Pre-Insulated Pipes

Stringent government regulations aimed at reducing carbon footprint and promoting energy-efficient buildings have become pivotal drivers of the Pre-Insulated Pipes Market. As governments worldwide intensify their efforts to combat climate change, regulations mandating the use of energy-efficient materials in construction projects have surged. Pre-insulated pipes, renowned for their thermal stability and ability to minimize heat loss, align seamlessly with these regulatory mandates.

For instance, in Europe, initiatives such as the Energy Performance of Buildings Directive (EPBD) emphasize the importance of energy-efficient heating systems, propelling the adoption of pre-insulated pipes. According to recent statistics, the European pre-insulated pipes market is projected to witness robust growth, with a compound annual growth rate (CAGR) exceeding 6% over the forecast period.

Attractive Properties Fueling Market Growth

The Pre-Insulated Pipes Market is experiencing a significant upsurge due to the attractive properties of pre-insulated pipes, including thermal stability and cost-saving nature. End-users across various industries, such as oil and gas, chemicals, and pharmaceuticals, are increasingly recognizing the value proposition offered by pre-insulated pipes.

These pipes not only ensure efficient energy transfer but also mitigate heat loss, thereby reducing operational costs. Moreover, the versatility of pre-insulated pipes makes them suitable for a wide range of applications, further driving their adoption. With cost-saving becoming a paramount consideration for industries worldwide, pre-insulated pipes have emerged as a preferred solution, fostering market growth.

Rising Demand Across End-User Industries

The burgeoning demand for energy-efficient solutions in end-user industries like the oil and gas sector, chemicals, and pharmaceuticals is fueling the growth of the Pre-Insulated Pipes Market. With industries facing pressure to enhance operational efficiency while minimizing environmental impact, the adoption of pre-insulated pipes has surged.

These pipes not only facilitate efficient energy transfer but also contribute to the reduction of greenhouse gas emissions, aligning with sustainability goals. As a result, the demand for pre-insulated pipes is expected to witness steady growth across diverse end-user industries, propelling market expansion.

Restraining Factors

Impact of High Installation Costs on Pre-Insulated Pipes Market Growth

High installation costs represent a significant restraining factor for the Pre-Insulated Pipes Market. While pre-insulated pipes offer long-term cost savings through improved energy efficiency and reduced maintenance requirements, the initial investment for installation can be substantial. The high upfront costs deter some potential customers, particularly in cost-sensitive sectors such as construction and infrastructure development.

Moreover, the complex installation process of pre-insulated pipes, which often involves specialized equipment and expertise, further contributes to the overall installation expenses. Despite the long-term benefits, the perceived financial burden of installation remains a key barrier to market expansion. As per industry analysis, the installation costs associated with pre-insulated pipes can be up to 30% higher compared to conventional piping systems, deterring widespread adoption.

Limited Availability of Skilled Labor Hindering Market Growth

The limited availability of skilled labor for the installation of pre-insulated pipes poses a significant challenge to market growth. The specialized nature of pre-insulated pipe installation requires technicians with specific expertise and training, including knowledge of insulation techniques, welding, and pipe fitting. However, the shortage of skilled labor in the construction and engineering sectors has led to bottlenecks in the adoption of pre-insulated piping systems.

Furthermore, the intricate nature of pre-insulated pipe installation demands precision and attention to detail, exacerbating the shortage of qualified professionals. Consequently, project delays and cost overruns often occur due to the scarcity of skilled labor, impeding the widespread implementation of pre-insulated pipes. Addressing this challenge necessitates investments in vocational training programs and initiatives to attract talent to the construction industry.

By Material Type Analysis

Pre-insulated pipes made from polymers offer durability, flexibility, and resistance to corrosion and chemical degradation.

In 2023, polymers held a dominant market position in the "By Material Type" segment of the pre-insulated pipes market. Polymers, owing to their versatility and cost-effectiveness, emerged as the material of choice for various applications within the pre-insulated pipes industry. This dominance can be attributed to several factors, including the growing demand for lightweight and durable piping solutions across diverse end-user industries such as construction, HVAC (heating, ventilation, and air conditioning), and district heating.

Polymers offer numerous advantages over traditional materials like metals and alloys. Firstly, their innate flexibility allows for easier installation, reducing both time and labor costs associated with piping systems. Additionally, polymers exhibit excellent corrosion resistance, ensuring longevity and minimal maintenance requirements compared to metal-based alternatives. Moreover, advancements in polymer technology have led to the development of high-performance materials capable of withstanding extreme temperatures and pressures, further enhancing their suitability for demanding applications.

Despite the dominance of polymers, the market for metal and alloys in pre-insulated pipes remains significant, particularly in applications requiring higher mechanical strength or elevated operating temperatures. Metals and alloys are favored in industrial sectors settings where durability and resistance to harsh conditions are paramount.

By Pipe Configuration Analysis

Twin pipe configuration allows for simultaneous transportation of hot and cold water in district heating systems.

In 2023, Twin Pipe emerged as the dominant player in the "By Pipe Configuration" segment of the pre-insulated pipes market. Twin Pipe configurations gained prominence due to their superior thermal efficiency and versatility across various applications. This dominance can be attributed to several key factors, including the ability of Twin Pipe systems to provide separate conduits for hot and cold fluids, minimizing heat loss and enhancing energy efficiency in heating, cooling, and district heating applications.

Twin Pipe systems offer distinct advantages over Single Pipe configurations. By maintaining separate channels for hot and cold fluids, Twin Pipe configurations effectively prevent thermal bridging, ensuring consistent temperature control and reducing energy consumption. This characteristic makes them particularly suitable for applications where precise temperature regulation and energy conservation are critical, such as in commercial buildings, residential complexes, and industrial facilities.

Despite the dominance of Twin Pipe systems, Single Pipe configurations continue to play a significant role in the pre-insulated pipes market. Single-pipe systems offer simplicity and cost-effectiveness, making them suitable for smaller-scale projects or applications with less stringent temperature control requirements.

By Installation Analysis

Below-ground installation minimizes visual impact and protects pre-insulated pipes from external damage or environmental factors.

In 2023, Below Ground installations asserted a dominant position in the "By Installation" segment of the pre-insulated pipes market. This supremacy underscores the preference for Below Ground installations in various applications, driven by major factors such as enhanced durability, space optimization, and environmental considerations. Ground installations are favored for their ability to safeguard piping systems from external elements, ensuring longevity and reliability, particularly in underground utilities, district heating networks, and geothermal systems.

The dominance of Below Ground installations can be attributed to their inherent advantages over Above Ground alternatives. Underground placement provides protection against weather-related damage, vandalism, and accidental impacts, reducing the risk of disruptions and maintenance costs associated with above-ground installations. Additionally, Below Ground configurations offer space-saving benefits, allowing for efficient land use and aesthetic integration within urban landscapes.

Despite the prevalence of below-ground installations, above-ground options remain relevant in certain scenarios. Above-ground installations offer greater accessibility for inspection, maintenance, and repairs, making them suitable for applications where frequent access to piping systems is necessary or where underground installation is impractical due to site constraints or environmental considerations.

By End User Analysis

District heating and cooling systems in urban areas are major users of pre-insulated pipes for energy distribution.

In 2023, District Heating and Cooling emerged as the dominant player in the "By End User" segment of the pre-insulated pipes market. This dominance underscores the widespread adoption of pre-insulated piping solutions in district heating and cooling systems, driven by the increasing focus on energy efficiency, urbanization, and sustainable infrastructure development. District Heating and Cooling applications encompass a wide range of residential, commercial, and industrial projects, including urban district heating networks, residential complexes, hospitals, educational institutions, and industrial parks.

The dominance of District Heating and Cooling in the pre-insulated pipes market can be attributed to several growth factors. Firstly, district heating and cooling systems offer energy-efficient solutions for large-scale heating and cooling requirements, leveraging centralized heat generation and distribution networks to optimize energy usage and reduce carbon emissions. Additionally, the growing emphasis on decarbonization and climate change mitigation has spurred investments in district energy infrastructure, driving demand for pre-insulated pipes in these applications.

Despite the dominance of District Heating and Cooling, other end-user segments such as Oil & Gas, Chemical, Pharmaceutical, and Others remain significant contributors to the pre-insulated pipes market. These industries utilize pre-insulated piping solutions for various applications, including process heating, chemical transport, pharmaceutical manufacturing, and specialized industrial processes. However, the prevalence of District Heating and Cooling reflects the increasing prioritization of sustainable heating and cooling solutions in both urban and rural areas, driving the demand for pre-insulated pipes in these applications.

Key Market Segments

By Material Type

- Polymers

- Metal & Alloys

By Pipe Configuration

- Twin Pipe

- Single Pipe

By Installation

- Below Ground

- Above Ground

By End User

- District Heating and Cooling

- Oil & Gas

- Chemical

- Pharmaceutical

- Others

Growth Opportunity

Infrastructure Development Projects in Emerging Economies

The year 2023 presents significant opportunities for the global pre-insulated pipes market, particularly driven by infrastructure development projects in emerging economies. With rapid urbanization and industrialization underway in regions such as Asia-Pacific, Africa, and Latin America, there is a growing demand for efficient and sustainable infrastructure solutions.

Pre-insulated pipes offer advantages in terms of energy efficiency, durability, and ease of installation, making them ideal for applications in water supply networks, district heating systems, and urban development projects. Market major players can capitalize on this trend by expanding their presence in emerging markets and forging strategic partnerships with local stakeholders to leverage growth opportunities.

Adoption of Energy-Efficient Solutions in Building Construction

Another key opportunity in 2023 for the global pre-insulated pipes market lies in the increasing adoption of energy-efficient solutions in building construction. With rising awareness of environmental sustainability and energy conservation, there is a growing demand for green building technologies that reduce energy consumption and carbon emissions.

Pre-insulated pipes play a crucial role in enhancing the energy efficiency of heating, ventilation, and air conditioning (HVAC) systems, as well as in providing reliable thermal insulation for plumbing and hydronic heating applications. Market players can leverage this trend by offering innovative pre-insulated pipe solutions tailored to the needs of the construction industry and positioning themselves as leaders in sustainable building infrastructure.

Expansion into Industrial Applications such as Oil and Gas Pipelines

Furthermore, the expansion into industrial applications such as oil and gas pipelines presents significant opportunities for the global pre-insulated pipes market in 2023. With the growing demand for energy resources and the increasing focus on pipeline safety and efficiency, there is a rising need for advanced piping solutions that can withstand harsh operating conditions and minimize heat loss during transport.

Pre-insulated pipes offer advantages such as corrosion resistance, thermal stability, and ease of installation, making them well-suited for use in oil and gas pipelines, chemical processing plants, and industrial facilities. Market players can capitalize on this opportunity by developing specialized pre-insulated pipe solutions tailored to the requirements of industrial applications and establishing partnerships with key players in the energy sector to penetrate new markets and drive revenue growth.

Latest Trends

Increasing Infrastructure Development Projects Driving Demand

In 2023, the global pre-insulated pipes market is witnessing a surge in demand fueled by increasing infrastructure development projects, particularly in the construction and HVAC sectors. The growing need for efficient and sustainable building solutions in both residential and commercial construction projects is propelling the adoption of pre-insulated pipes.

These pipes offer advantages such as enhanced thermal efficiency, reduced heat loss, and simplified installation processes, making them a preferred choice for heating, ventilation, and air conditioning systems. Market players are strategically positioning themselves to capitalize on this trend by expanding their product portfolios and targeting key projects in emerging and established markets.

Emphasis on Energy Efficiency and Environmental Sustainability

Another significant trend shaping the global pre-insulated pipes market in 2023 is the increasing emphasis on energy efficiency and environmental sustainability. With rising awareness of climate change and the need to reduce carbon emissions, there is a growing demand for green building technologies that minimize energy consumption and promote environmental stewardship.

Pre-insulated pipes play a crucial role in meeting these objectives by providing efficient thermal insulation for heating and cooling systems, thereby reducing energy wastage and lowering carbon footprints. Market players are responding to this trend by developing innovative pre-insulated pipe solutions with enhanced insulation properties and eco-friendly materials. Additionally, strategic partnerships and collaborations with sustainability-focused organizations are being leveraged to drive market growth and differentiation.

Regional Analysis

In Europe, pre-insulated pipes hold a market share of 36.2%, reflecting significant demand and adoption.

The pre-insulated pipes market exhibits varied dynamics across different regions, including North America, Europe, Asia Pacific, the Middle East &; Africa, and Latin America.

In Europe, the market holds a dominant position, capturing a significant share of 36.2%. This dominance can be attributed to stringent regulations promoting energy efficiency and sustainability, coupled with extensive infrastructure development initiatives across the region. Furthermore, the presence of established players and technological advancements in pre-insulated pipe solutions contribute to Europe's leading position in the market.

North America follows closely, driven by robust construction activities and increasing adoption of energy-efficient building solutions. The region benefits from a mature construction industry and growing investments in renewable energy projects, which bolster the demand for pre-insulated pipes. Additionally, government incentives aimed at promoting green building practices further propel market growth in North America.

Asia Pacific emerges as a rapidly growing market, fueled by urbanization, industrialization, and investments in infrastructure development. Countries such as China, India, and Southeast Asian nations witness significant demand for pre-insulated pipes, driven by the need for modernizing urban infrastructure and enhancing energy efficiency in buildings.

Middle East & Africa exhibit promising growth opportunities, supported by investments in oil and gas infrastructure, district cooling projects, and urban development initiatives. The region's harsh climatic conditions necessitate reliable and efficient piping solutions, driving the adoption of pre-insulated pipes.

Latin America presents a burgeoning market driven by urbanization, industrial growth, and increasing focus on sustainable construction practices. Government initiatives promoting infrastructure development and energy efficiency further stimulate market growth in the region.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global pre-insulated pipes market sees notable contributions from key players such as Georg Fischer AG, Uponor Corporation, Watts Water Technologies, LOGSTOR A/S, Brugg Group Ag, Polypipe Group PLC, Vital Energi Utilities Limited, Perma-Pipe International Holdings Inc., Elips - Empower Logstor, KE KELIT, Thermaflex International Holding b.v., Ecoline S.R.L., Aquatherm GmbH, CPV LTD, Insul-Pipe Systems, Thermal Pipe Systems, Inc., IPL Pre-Insulated Pipes, Unifix Plast Pvt. Ltd., and ZECO Aircon Ltd.

These key players play a pivotal role in driving innovation, meeting customer demands, and shaping market trends in the pre-insulated pipes industry. With diverse product portfolios, extensive distribution networks, and a strong focus on research and development, these companies are well-positioned to capitalize on growth opportunities in various regions and sectors.

In particular, key companies like Georg Fischer AG and Uponor Corporation stand out for their longstanding reputation, technological expertise, and commitment to sustainability. Their innovative solutions and strategic partnerships enable them to address the evolving needs of customers while maintaining a competitive edge in the market.

Moreover, emerging players such as Elips-Empower Logstor and Aquatherm GmbH are making significant strides in the market with their innovative product offerings and strategic expansion initiatives. These companies bring fresh perspectives and unique capabilities to the market, further enriching the competitive landscape and driving market growth.

Market Key Players

- Georg Fischer AG

- Uponor Corporation

- Watts Water Technologies

- LOGSTOR A/S

- Brugg Group Ag

- Polypipe Group PLC

- Vital Energi Utilities Limited

- Perma-Pipe International Holdings Inc.

- Elips - Empower Logstor

- KE KELIT

- Thermaflex International Holding b.v.

- Ecoline S.R.L.

- Aquatherm GmbH

- CPV LTD

- Insul-Pipe Systems

- Thermal Pipe Systems, Inc.

- IPL Pre-Insulated Pipes

- Unifix Plast Pvt. Ltd.

- ZECO Aircon Ltd.

Recent Development

- In October 2023, GF Piping Systems emphasized the sustainability benefits of plastic piping in battery cell production, highlighting energy and CO2 savings. Their COOL-FIT pre-insulated pipes offer efficient cooling solutions, contributing to energy efficiency.

- In September 2023, The Thermal Insulation Contractors Association (TICA) called for a review of the pre-insulated pipe and duct market due to concerns over fire safety claims and testing regimes of manufacturers.

- In August 2023, Empower reported robust H1 2023 revenues of AED 1,225 million, driven by increasing demand for district cooling from new projects, showcasing impressive growth in revenue and EBITDA.

Report Scope

Report Features Description Market Value (2023) USD 7.3 Billion Forecast Revenue (2033) USD 20.7 Billion CAGR (2024-2032) 11.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Material Type(Polymers, Metal & Alloys), By Pipe Configuration(Twin Pipe, Single Pipe), By Installation(Below Ground, Above Ground), By End User(District Heating and Cooling, Oil & Gas, Chemical, Pharmaceutical, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Georg Fischer AG, Uponor Corporation, Watts Water Technologies, LOGSTOR A/S, Brugg Group Ag, Polypipe Group PLC, Vital Energi Utilities Limited, Perma-Pipe International Holdings Inc., Elips - Empower Logstor, KE KELIT, Thermaflex International Holding b.v., Ecoline S.R.L., Aquatherm GmbH, CPV LTD, Insul-Pipe Systems, Thermal Pipe Systems, Inc., IPL Pre-Insulated Pipes, Unifix Plast Pvt. Ltd., ZECO Aircon Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Georg Fischer AG

- Uponor Corporation

- Watts Water Technologies

- LOGSTOR A/S

- Brugg Group Ag

- Polypipe Group PLC

- Vital Energi Utilities Limited

- Perma-Pipe International Holdings Inc.

- Elips - Empower Logstor

- KE KELIT

- Thermaflex International Holding b.v.

- Ecoline S.R.L.

- Aquatherm GmbH

- CPV LTD

- Insul-Pipe Systems

- Thermal Pipe Systems, Inc.

- IPL Pre-Insulated Pipes

- Unifix Plast Pvt. Ltd.

- ZECO Aircon Ltd.

Our Clients

View Our Licence Options