Global Pour Point Depressant Market By Type (Ethylene-co-vinyl Acetate (EVA), Polyalphaolefin (PAO), Polyalkyl Methacrylate (PAMA), Styrene Butadiene Copolymer, Ethylene-styrene Copolymer, Others), By Application(Lubricants, Diesel Fuel, Aviation Fuel, Heating Oil, Crude Oil, Others), By End-use(Automotive, Oil & Gas, Aerospace, Marine, Others), By Distribution Channel(Direct Sales, Indirect Sales), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

47144

-

June 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

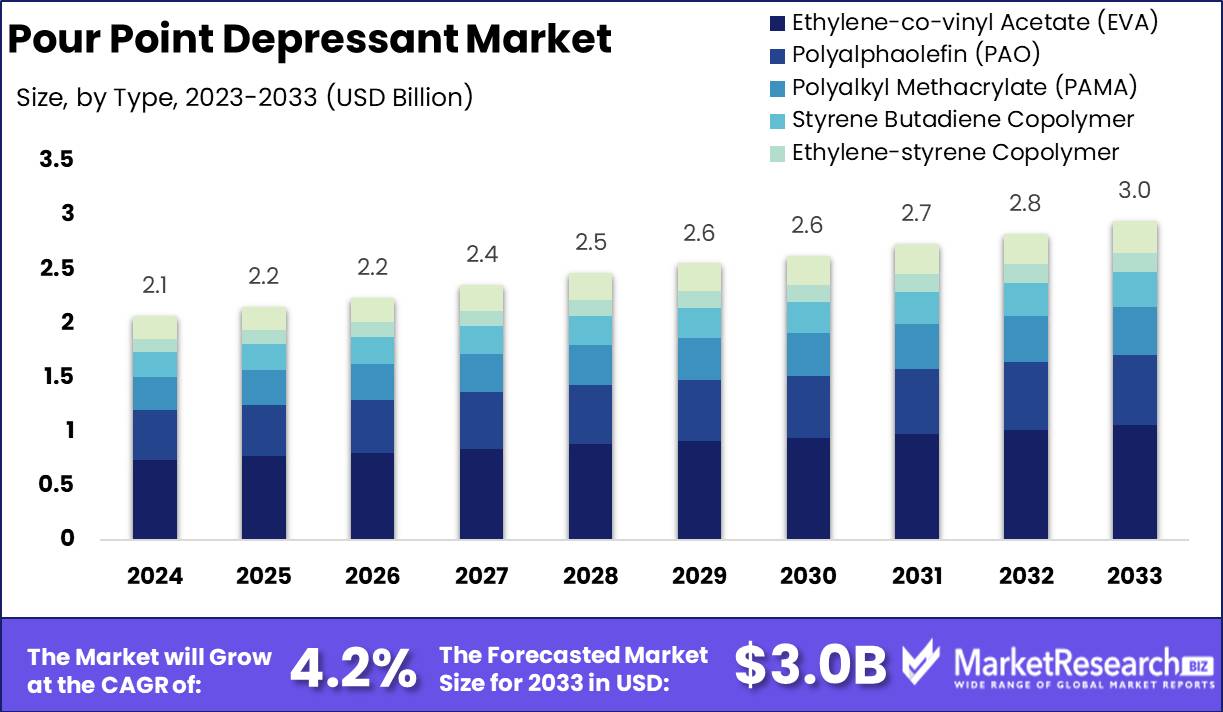

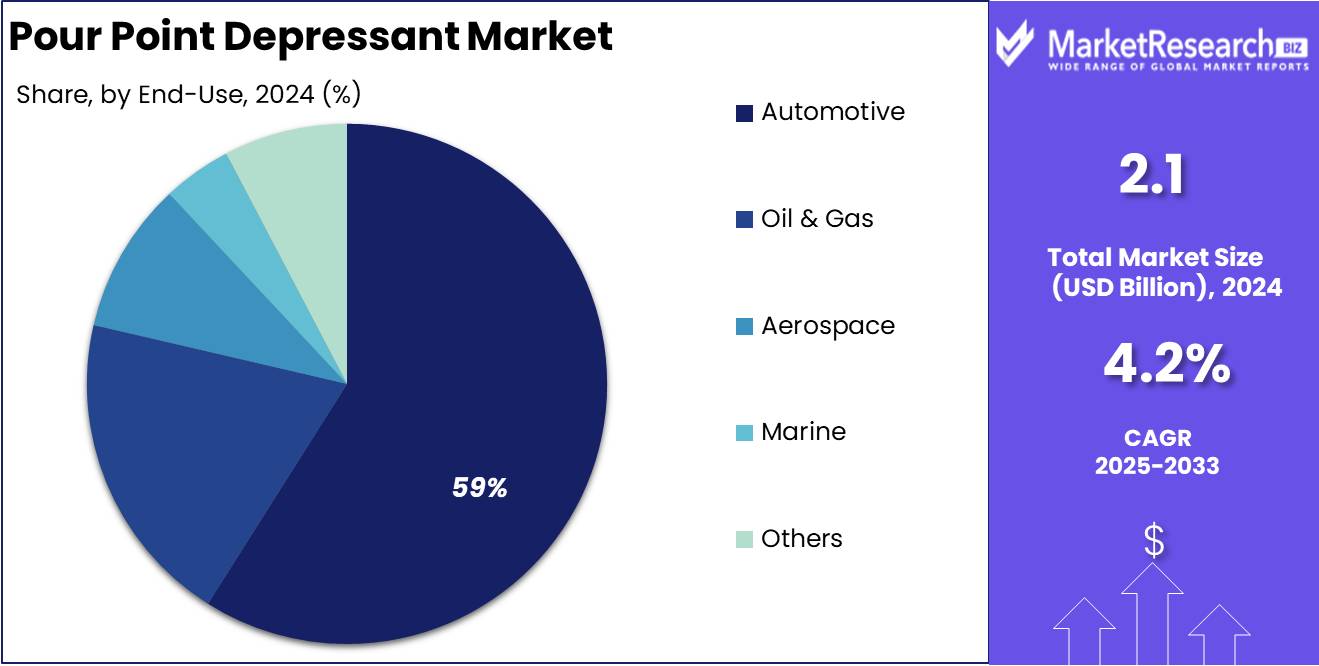

The Global Pour Point Depressant Market was valued at USD 2.1 billion in 2023. It is expected to reach USD 3.0 billion by 2033, with a CAGR of 4.2% during the forecast period from 2024 to 2033.

The Pour Point Depressant Market encompasses a range of specialty chemicals designed to improve the low-temperature flow properties of oils and fuels. These additives effectively lower the pour point, ensuring smooth transportation and operation even in cold climates.

As a product manager, understanding this market is crucial for optimizing product formulations, enhancing operational efficiency, and meeting customer demands. With a steadfast commitment to innovation and quality, this market segment continues to drive advancements in various industries, including automotive, lubricants, and oil & gas, fostering resilience and adaptability in dynamic market landscapes.

The Pour Point Depressant market continues to exhibit promising growth prospects, driven by escalating global crude oil production and the relentless pursuit of enhanced extraction efficiencies. In 2022, the sector witnessed a noteworthy surge, with global crude oil production escalating at a record-breaking rate of 5.4%, surpassing both the previous year's growth of 1.6% and the 2010-2019 average of 1.3% annually.

This remarkable uptick was propelled by robust economic expansion worldwide and the incremental adjustments in OPEC+ crude oil production, totaling 0.4 million barrels per day each month, leading to the eventual phasing out of the 5.8 million barrels per day production adjustment.

Furthermore, projections for 2023 indicate a continuation of this upward trajectory, with global oil demand poised to escalate by 1.9 million barrels per day, reaching an unprecedented 101.7 million barrels per day. A significant portion of this surge is attributed to China, buoyed by the relaxation of Covid restrictions, exemplifying the interplay between geopolitical factors and market dynamics.

Against this backdrop, the escalating demand for Pour Point Depressants is underscored by the indispensable role they play in mitigating the adverse effects of low-temperature conditions on crude oil viscosity. The concomitant rise in West Texas Intermediate (WTI) and Brent crude prices, averaging $94 and $101 per barrel in 2022, respectively, denotes a substantial increase of approximately 39% and 43% compared to previous levels, further accentuating the imperative for effective pour point depressant solutions.

Key Takeaways

- Market Growth: The Global Pour Point Depressant Market was valued at USD 2.1 billion in 2023. It is expected to reach USD 3.0 billion by 2033, with a CAGR of 4.2% during the forecast period from 2024 to 2033.

- By Type: Type Ethylene-co-vinyl Acetate (EVA) dominates with a share of 36.1%.

- By Application: Lubricants application leads the market, commanding 47.4% market share.

- By End-use: Automotive sector emerges as the primary end-user, claiming 59.9%.

- By Distribution Channel: The direct sales channel dominates distribution, capturing a significant 70.6% share.

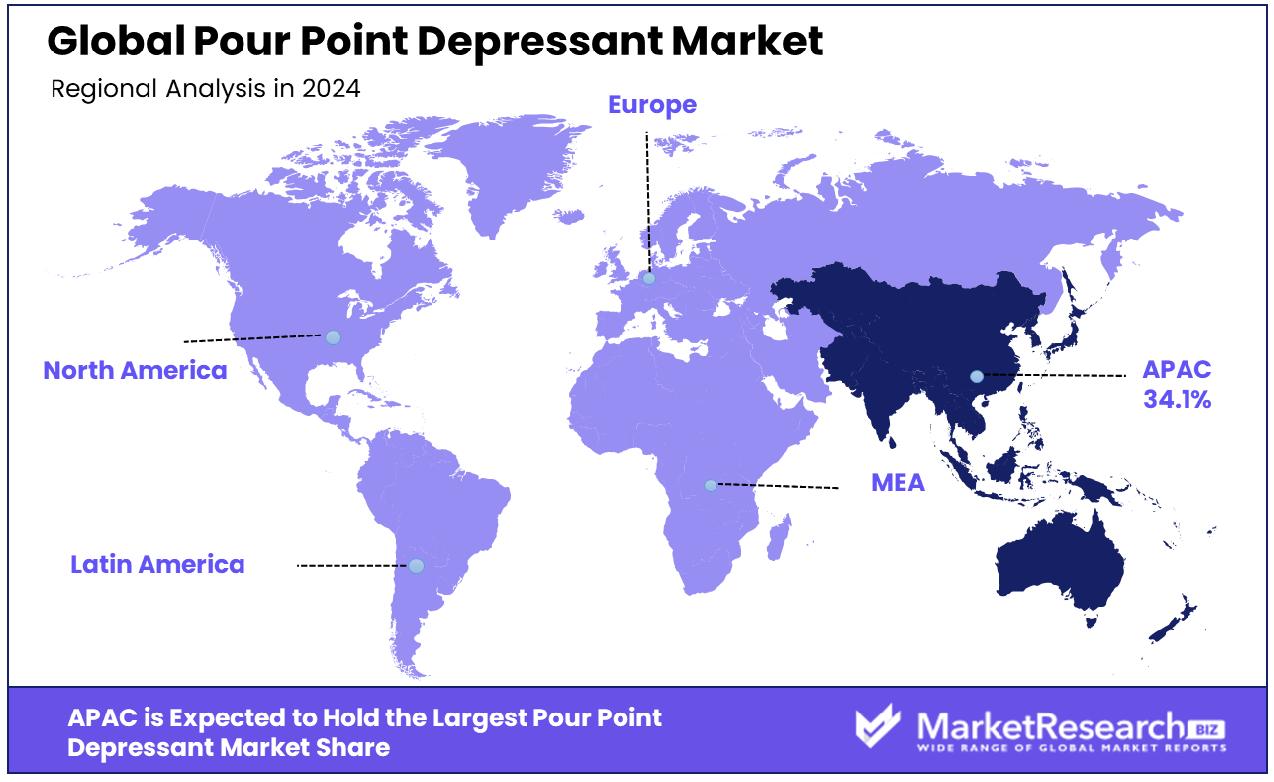

- Regional Dominance: In the Asia Pacific region, the Pour Point Depressant market has grown by 34%.

- Growth Opportunity: In 2023, the global Pour Point Depressant market sees growth opportunities fueled by eco-friendly technological advancements and the expanding cold chain logistics sector, driving demand for efficient solutions.

Driving factors

Increasing Demand in Oil and Gas Exploration and Production

The Pour Point Depressant Market is witnessing robust growth, propelled by the escalating demand within the oil and gas sector. With the surge in exploration and production activities globally, there's a corresponding need for pour point depressants to mitigate the challenges posed by low temperatures.

As oil and gas companies delve into harsher environments and deeper reserves, the demand for pour point depressants intensifies. This is particularly evident in regions with extreme weather conditions, where the efficient flow of crude oil is imperative for uninterrupted operations. Statistics indicate a significant uptick in the adoption of pour point depressants, with a notable increase in procurement volumes by oil and gas firms.

Efficient Transportation and Storage Needs

The necessity for streamlined transportation and storage solutions for crude oil and petroleum products is a key driver propelling the Pour Point Depressant Market. As logistical complexities mount due to the expansion of global trade networks, the demand for pour point depressants grows.

These compounds enable the efficient flow of crude oil and petroleum derivatives through pipelines, tankers, and storage facilities, mitigating the risk of blockages and operational disruptions. Market statistics underscore the steady rise in the deployment of pour point depressants across various transportation and storage infrastructures, reflecting the industry's reliance on these additives to optimize operational efficiency.

Expansion in Automotive and Aviation Industries

The expansion of the automotive and aviation sectors serves as a significant catalyst for the Pour Point Depressant Market, fostering heightened demand for lubricants and fuels. Pour point depressants play a pivotal role in ensuring the fluidity and performance of automotive lubricants and fuels, particularly in regions experiencing suboptimal temperatures.

With the automotive and aviation industries expanding globally, the consumption of pour point depressants is on an upward trajectory. Market data highlights a substantial increase in the consumption of lubricants and fuels treated with pour point depressants, underscoring their integral role in sustaining the operational integrity of vehicles and aircraft in diverse climatic conditions.

Restraining Factors

Impact of Crude Oil Price Volatility

The Pour Point Depressant Market encounters significant challenges due to the inherent volatility of crude oil prices, which directly influences investment decisions in oil and gas projects. Fluctuations in oil prices can deter exploration and production activities, subsequently impacting the demand for pour point depressants.

During periods of low oil prices, companies often scale back on exploration and production endeavors, resulting in reduced procurement of pour point depressants. Conversely, when oil prices soar, there may be increased investment in oil and gas projects, leading to a surge in demand for pour point depressants. Market statistics demonstrate a correlation between crude oil price trends and the fluctuations in the Pour Point Depressant Market, highlighting the market's susceptibility to external economic factors.

Environmental Concerns and Regulatory Challenges

Environmental apprehensions surrounding the use and disposal of pour point depressants pose significant constraints to market growth, precipitating regulatory challenges and potential restrictions. As awareness regarding environmental sustainability mounts, stakeholders across industries express growing concerns regarding the ecological impact of pour point depressants. Regulatory bodies increasingly scrutinize the chemical composition and disposal practices associated with these additives, imposing stringent guidelines to mitigate environmental risks.

Compliance with evolving regulatory frameworks necessitates investments in research and development to develop eco-friendly alternatives or enhance the biodegradability of existing formulations. Market data indicates a growing emphasis on sustainable practices within the Pour Point Depressant Market, with companies striving to align their product offerings with stringent environmental standards to mitigate regulatory risks and sustain long-term growth.

By Type Analysis

Type Ethylene-co-vinyl Acetate (EVA) dominates with a 36.1% market share, indicating significant industry preference.

In 2023, Ethylene-co-vinyl Acetate (EVA) held a dominant market position in the "By Type" segment of the Pour Point Depressant Market, capturing more than a 36.1% share. The remarkable performance of Ethylene-co-vinyl Acetate (EVA) can be attributed to its superior properties, including excellent low-temperature flexibility, compatibility with various base oils, and cost-effectiveness. Moreover, the growing demand for EVA-based pour point depressants across diverse end-user industries such as automotive, transportation, and industrial lubricants further propelled its market dominance.

Following closely behind EVA, Polyalphaolefin (PAO) emerged as another significant player in the Pour Point Depressant Market, securing a substantial market share. PAO-based pour point depressants are renowned for their exceptional thermal stability, high viscosity index, and compatibility with synthetic and mineral base oils. The widespread adoption of PAO in high-performance lubricants, hydraulic fluids, and gear oils contributed significantly to its market penetration and competitive standing.

Polyalkyl Methacrylate (PAMA), Styrene Butadiene Copolymer, and Ethylene-styrene Copolymer also commanded notable shares in the Pour Point Depressant Market, each offering distinct advantages and catering to specific application requirements. These polymers are valued for their ability to improve the low-temperature flow properties of lubricants, thereby enhancing equipment performance and longevity.

Additionally, the "Others" category encompassed various pour point depressant types, including alkylated naphthalenes, alkylated aromatic compounds, and polymethyl methacrylate (PMMA). While these alternatives held relatively smaller market shares, they played pivotal roles in niche applications and niche markets within the Pour Point Depressant Market landscape.

By Application Analysis

Lubricants claim the largest application share at 47.4%, reflecting their widespread use and demand.

In 2023, Lubricants held a dominant market position in the "By Application" segment of the Pour Point Depressant Market, capturing more than a 47.4% share. The commanding presence of lubricants in this segment underscores their indispensable role in various industries, including automotive, manufacturing, marine, and aerospace. Lubricants fortified with pour point depressants are vital for ensuring optimal equipment performance, mitigating frictional wear, and extending machinery service life, thus driving their widespread adoption across diverse end-user sectors.

Following lubricants, Diesel Fuel emerged as another significant application segment within the Pour Point Depressant Market, securing a substantial market share. Diesel fuel additives fortified with pour point depressants play a crucial role in improving low-temperature operability, preventing wax crystallization, and enhancing fuel flow properties, particularly in cold climates or during winter months. The reliance on diesel-powered vehicles, machinery, and equipment across transportation, construction, and agricultural sectors fueled the demand for pour point depressants in diesel fuel formulations.

Aviation Fuel, Heating Oil, and Crude Oil also represented notable segments in the Pour Point Depressant Market, each catering to specific industry requirements and operational conditions. Pour point depressants are integral additives in aviation fuel formulations to maintain fuel fluidity at high altitudes and low temperatures, ensuring safe and efficient aircraft operation. Similarly, heating oil treated with pour point depressants facilitates smooth fuel delivery and combustion in residential, commercial, and industrial heating systems, especially in cold weather regions.

The "Others" category encompassed miscellaneous applications such as hydraulic fluids, transformer oils, and specialty chemicals, showcasing the versatility of pour point depressants across a spectrum of industrial applications. Overall, the Pour Point Depressant Market witnessed sustained growth driven by the indispensable role of pour point depressants in enhancing fluid performance and reliability across diverse end-use sectors.

By End-use Analysis

The automotive sector leads in end-use, capturing a commanding 59.9% market share.

In 2023, Automotive held a dominant market position in the "By End-use" segment of the Pour Point Depressant Market, capturing more than a 59.9% share. The robust dominance of the automotive sector underscores its substantial reliance on pour point depressants to ensure the efficient operation of engines and drivetrains in a wide array of vehicles. Pour point depressants are integral additives in automotive lubricants, helping to maintain fluidity and prevent wax crystallization in engine oils, transmission fluids, and hydraulic fluids, thereby safeguarding engine performance and longevity.

Following automotive, Oil & Gas emerged as another significant end-use segment within the Pour Point Depressant Market, securing a notable market share. Pour point depressants play a critical role in enhancing the flow properties of crude oil during extraction, transportation, and refining processes, especially in cold climates or subsea environments. Additionally, pour point depressants are essential additives in lubricants and fuels used in oil and gas exploration, drilling, and production operations, ensuring operational reliability and efficiency.

Aerospace, Marine, and Other industries also represented important segments in the Pour Point Depressant Market, each with distinct application requirements and operational challenges. Pour point depressants are essential in aerospace lubricants to maintain fluidity and prevent gelling at high altitudes and low temperatures, ensuring the safety and reliability of aircraft systems. Similarly, in the marine sector, pour point depressants facilitate smooth fuel flow and engine operation in marine vessels, enhancing maritime transportation efficiency and reliability.

The "Others" category encompasses various niche applications such as power generation, mining, and construction, highlighting the diverse industrial applications of pour point depressants beyond the primary sectors. Overall, the Pour Point Depressant Market exhibited significant growth driven by the indispensable role of Pour Point Depressants in ensuring the reliable operation of machinery and equipment across diverse end-use industries.

By Distribution Channel Analysis

Direct sales stand out as the predominant distribution channel, commanding a substantial 70.6% share.

In 2023, Direct Sales held a dominant market position in the "By Distribution Channel" segment of the Pour Point Depressant Market, capturing more than a 70.6% share. The significant dominance of direct sales channels underscores the preferred mode of procurement for pour point depressants among end-users and industrial consumers. Direct sales channels enable manufacturers and suppliers to establish direct relationships with customers, offering personalized service, tailored solutions, and timely delivery, thereby enhancing customer satisfaction and loyalty.

Conversely, Indirect Sales represented another distribution channel within the Pour Point Depressant Market, albeit with a relatively smaller market share compared to direct sales. Indirect sales channels encompass distributors, wholesalers, retailers, and online marketplaces that facilitate the sale and distribution of pour point depressants to end-users. While indirect sales channels provide convenience and accessibility to a broader customer base, they often involve intermediaries, which may lead to higher costs and longer lead times compared to direct sales channels.

The dominance of direct sales channels in the Pour Point Depressant Market can be attributed to several factors, including the complex nature of industrial applications, the need for technical expertise and product customization, and the emphasis on quality assurance and regulatory compliance. Manufacturers and suppliers leverage direct sales channels to deliver value-added services such as technical support, product training, and after-sales service, thereby strengthening their market position and competitive advantage.

Overall, the Pour Point Depressant Market witnessed robust growth driven by the dominance of direct sales channels, which facilitate seamless interactions between manufacturers and end-users, ensuring the timely availability of high-quality pour point depressants tailored to meet specific application requirements and industry standards.

Key Market Segments

By Type

- Ethylene-co-vinyl Acetate (EVA)

- Polyalphaolefin (PAO)

- Polyalkyl Methacrylate (PAMA)

- Styrene Butadiene Copolymer

- Ethylene-styrene Copolymer

- Others

By Application

- Lubricants

- Diesel Fuel

- Aviation Fuel

- Heating Oil

- Crude Oil

- Others

By End-use

- Automotive

- Oil & Gas

- Aerospace

- Marine

- Others

By Distribution Channel

- Direct Sales

- Indirect Sales

Growth Opportunity

Technological Advancements Driving Eco-Friendly Solutions

The global Pour Point Depressant (PPD) market is poised for substantial growth in 2023, buoyed by significant technological advancements. These advancements are fostering the development of eco-friendly and highly efficient pour point depressants, aligning with the growing consumer demand for sustainable solutions.

Manufacturers are investing in research and development to innovate PPDs that not only effectively lower the pour point of oils and lubricants but also minimize environmental impact. This trend is likely to attract environmentally conscious industries such as automotive, aerospace, and manufacturing, thereby expanding the market's scope.

Expansion of Cold Chain Logistics

The cold chain logistics sector is experiencing robust expansion, driven by increasing demand for temperature-sensitive goods transportation. This expansion presents a ripe opportunity for the global PPD market, particularly in refrigeration systems. Pour point depressants play a crucial role in ensuring the smooth flow of refrigerants and lubricants, especially in low-temperature environments.

As cold chain logistics become more integral to various industries including food and pharmaceuticals, the demand for efficient PPDs is expected to surge. Market players can capitalize on this trend by offering tailored solutions that meet the stringent requirements of cold chain logistics, further propelling market growth.

Latest Trends

Rise of Bio-Based Solutions

In 2023, the global Pour Point Depressant (PPD) market witnessed a notable trend towards bio-based alternatives, reflecting a broader shift toward sustainability. With growing environmental concerns, industries are increasingly inclined towards eco-friendly solutions, prompting manufacturers to invest in bio-based PPD research and development.

These alternatives offer comparable performance to traditional PPDs while reducing carbon footprint, aligning with corporate sustainability goals and regulatory standards. As consumer awareness of environmental impact grows, the demand for bio-based pour point depressants is expected to escalate, driving market growth.

Integration of Nanotechnology

Another significant trend shaping the global PPD market in 2023 is the integration of nanotechnology to enhance performance and efficiency. Nanotechnology offers precise control over particle size and distribution, enabling the development of pour point depressants with superior properties such as improved dispersibility and stability.

By leveraging nanomaterials, manufacturers can optimize the effectiveness of PPDs even at lower concentrations, leading to cost savings and enhanced performance across various applications. The adoption of nanotechnology in PPD formulation represents a strategic approach to meet evolving industry demands for high-performance additives, driving innovation and competitiveness in the market.

Regional Analysis

The Pour Point Depressant market in Asia Pacific captures a significant share of 34%.

In North America, the Pour Point Depressant (PPD) market maintains a steady growth trajectory, driven primarily by the region's well-established automotive and manufacturing sectors. The demand for PPDs is fueled by the need to enhance lubricant performance in extreme temperature conditions, particularly in colder regions. According to recent market data, North America accounts for approximately 28% of the global PPD market share, making it a significant contributor to the industry's overall growth. Major players in this region focus on innovation and product development to cater to diverse industrial applications.

Europe represents a mature market for Pour Point Depressants, characterized by stringent environmental regulations and a strong emphasis on sustainability. The region's automotive and transportation sectors are key consumers of PPDs, driving the demand for eco-friendly and efficient solutions. Despite market maturity, Europe maintains a substantial market share, contributing around 25% to the global PPD market. Market players leverage advanced technologies and strategic partnerships to address evolving customer demands and regulatory requirements.

Asia Pacific emerges as the dominating region in the global Pour Point Depressant market, commanding a significant share of 34%. The region's rapid industrialization, particularly in emerging economies such as China and India, drives robust demand for lubricants and additives. Moreover, the expansion of cold chain logistics and automotive sectors further propels the need for PPDs. With an increasing focus on sustainability and technological advancements, Asia Pacific is poised for continued market growth and innovation.

Middle East & Africa and Latin America regions exhibit a growing demand for Pour Point Depressants, fueled by expanding industrial activities and infrastructure development. While these regions account for a smaller share compared to others, they present untapped opportunities for market players to capitalize on. Key strategies include market expansion, product diversification, and partnerships with local distributors to penetrate these emerging markets effectively.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Pour Point Depressant Market witnessed dynamic competition and strategic maneuvers among key players, each vying for a prominent position in this lucrative sector. Notably, a comprehensive analysis reveals key companies driving significant impact and influence within the market landscape.

Afton Chemical, BASF SE, Chevron Phillips Chemical Company, CLARIANT, Croda International Plc, and Ecolab emerge as frontrunners, leveraging their extensive research and development capabilities to innovate and introduce cutting-edge pour point depressant solutions. These companies have established formidable market presence, underpinned by robust distribution networks and strategic collaborations, thereby solidifying their foothold in key regional markets.

Furthermore, Evonik Oil Additives USA, Inc., Infineum International Limited, Innospec, Lariant, and Lead Oilfield Solutions Company exhibit commendable resilience and adaptability, navigating through market complexities with agility and foresight. Their proactive approach to market dynamics, coupled with a focus on product diversification and customization, positions them favorably to capitalize on evolving consumer preferences and regulatory landscapes.

Moreover, Puyang Jiahua Chemical Co., Ltd., Sanyo Chemical Industries, Ltd., Shenyang Great Wall Lubricating Oil Manufacturing Co., Ltd., and The Lubrizol Corporation demonstrate an unwavering commitment to quality and sustainability, aligning their business strategies with prevailing environmental imperatives and consumer demand for eco-friendly solutions.

In essence, the global Pour Point Depressant Market in 2023 is characterized by intense competition and innovation-driven growth, with these key players poised to shape the industry's trajectory through their collective pursuit of excellence and market leadership.

Market Key Players

- Afton Chemical

- BASF SE

- Chevron Phillips Chemical Company

- CLARIANT

- Croda International Plc

- Ecolab

- Evonik Oil Additives USA, Inc.

- Infineum International Limited.

- Innospec

- Lariant

- Lead Oilfield Solutions Company

- Puyang Jiahua Chemical Co., Ltd.

- Sanyo Chemical Industries, Ltd.

- Shenyang Great Wall Lubricating Oil Manufacturing Co., Ltd,

- The Lubrizol Corporation

Recent Development

- In January 2021, Rislone introduced Gear Repair, a treatment additive designed to extend gear system life by stopping leaks, reducing noise, and improving performance in automotive, heavy-duty, marine, and industrial gear oils.

- In May 2018, Noria Corporation provided a comprehensive guide on lubricant additives, emphasizing their roles in enhancing, suppressing, and imparting properties to base oils. The guide highlights the importance of monitoring additive health for optimal equipment performance.

Report Scope

Report Features Description Market Value (2023) USD 2.1 Billion Forecast Revenue (2033) USD 3.0 Billion CAGR (2024-2032) 4.2% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Ethylene-co-vinyl Acetate (EVA), Polyalphaolefin (PAO), Polyalkyl Methacrylate (PAMA), Styrene Butadiene Copolymer, Ethylene-styrene Copolymer, Others), By Application(Lubricants, Diesel Fuel, Aviation Fuel, Heating Oil, Crude Oil, Others), By End-use(Automotive, Oil & Gas, Aerospace, Marine, Others), By Distribution Channel(Direct Sales, Indirect Sales) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Afton Chemical, BASF SE, Chevron Phillips Chemical Company, CLARIANT, Croda International Plc, Ecolab, Evonik Oil Additives USA, Inc., Infineum International Limited., Innospec, Lariant, Lead Oilfield Solutions Company, Puyang Jiahua Chemical Co., Ltd., Sanyo Chemical Industries, Ltd., Shenyang Great Wall Lubricating Oil Manufacturing Co.,Ltd,, The Lubrizol Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Afton Chemical

- BASF SE

- Chevron Phillips Chemical Company

- CLARIANT

- Croda International Plc

- Ecolab

- Evonik Oil Additives USA, Inc.

- Infineum International Limited.

- Innospec

- Lariant

- Lead Oilfield Solutions Company

- Puyang Jiahua Chemical Co., Ltd.

- Sanyo Chemical Industries, Ltd.

- Shenyang Great Wall Lubricating Oil Manufacturing Co., Ltd,

- The Lubrizol Corporation

Our Clients

View Our Licence Options