Palm Acid Oil Market Report By Distribution Channel (Direct Sales, Indirect Sales), By End-Use Industry (Animal Feed Industry, Biofuel Industry, Soap and Detergent Industry, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

27622

-

August 2024

-

325

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

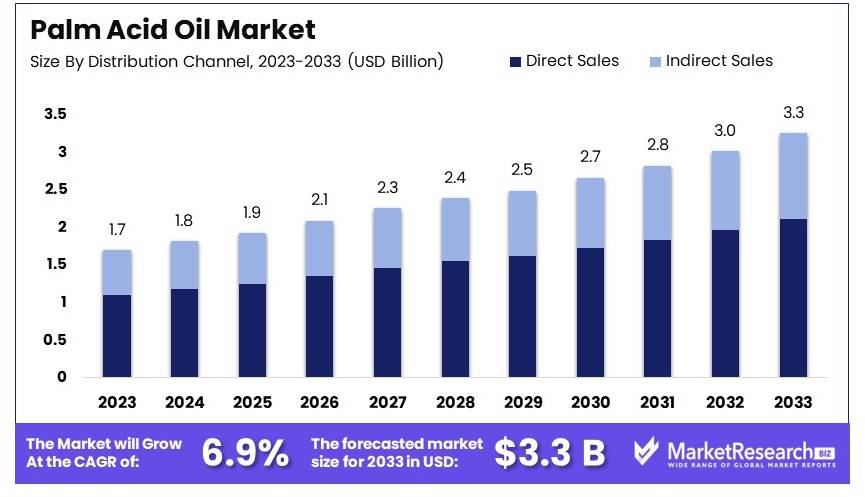

The Global Palm Acid Oil Market size is expected to be worth around USD 3.3 Billion by 2033, from USD 1.7 Billion in 2023, growing at a CAGR of 6.9% during the forecast period from 2024 to 2033.

The palm acid oil market involves the extraction and processing of palm acid oil, a byproduct of palm oil refining. This oil is primarily used in the production of soaps, animal feed, and biofuels. The market is driven by the increasing demand for sustainable and cost-effective raw materials in various industries.

Key players include palm oil refineries, biofuel manufacturers, and soap producers. The market benefits from the growing emphasis on waste utilization and environmental sustainability. Innovations in refining processes and applications are expected to drive future growth. The market is competitive, with significant contributions from major palm oil-producing regions.

The palm acid oil (PAO) market is witnessing significant growth, driven by its increasing use in biodiesel production and the oleochemical industry. Countries like Indonesia and Malaysia are leading this expansion due to their robust palm oil industries. In 2022, Indonesia produced approximately 5.8 million tons of biodiesel, showcasing its strong commitment to renewable energy initiatives. This emphasis on biodiesel is further supported by government regulations, such as Indonesia's mandate to blend 30% palm oil-derived biodiesel (B30) with conventional diesel.

China's biomass-based diesel imports surged by 40% in 2023, with over 90% of this being palm oil biodiesel from Indonesia and Malaysia. This highlights the growing international demand for PAO in biodiesel production. Additionally, Malaysia's oleochemical industry, with its 19 plants and a processing capacity of approximately 2.67 million tons annually, primarily produces fatty acids for soap manufacturing. This substantial capacity underlines the importance of PAO in various industrial applications.

Government regulations and initiatives significantly influence the PAO market. For example, the European Union's Renewable Energy Directive II (RED II) sets sustainability criteria for biofuels, impacting PAO usage through import regulations. These regulations ensure that biofuels, including those derived from PAO, meet stringent environmental standards.

The PAO market is poised for continued growth, driven by its critical role in biodiesel production and the oleochemical industry. The strong regulatory support from governments and increasing international demand further enhance its prospects. This trend reflects a broader commitment to renewable energy and sustainable industrial practices, positioning PAO as a vital component in these sectors.

Key Takeaways

- Market Value: The Palm Acid Oil Market was valued at USD 1.7 billion in 2023 and is projected to reach USD 3.3 billion by 2033, with a CAGR of 6.9%.

- Application Analysis: Biodiesel Production dominates at 55%; the renewable energy trend significantly propels this sector.

- Distribution Channel Analysis: Direct Sales account for 65%; direct supplier relationships enhance transaction efficiencies.

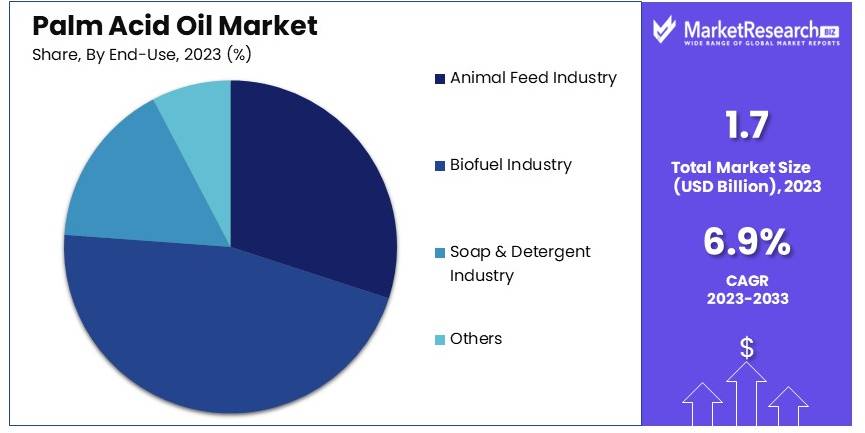

- End-Use Industry Analysis: The Biofuel Industry leads with 60%; global energy shifts toward sustainability highlight its critical role.

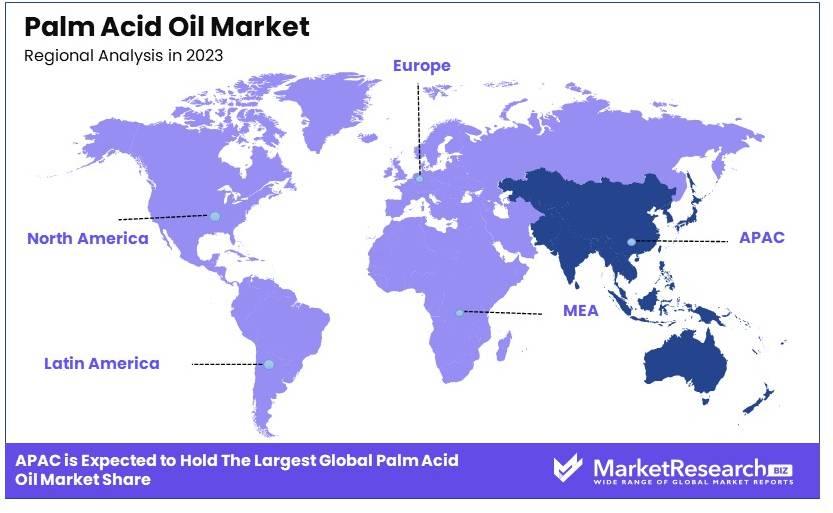

- Dominant Region: APAC's share of 38.5% is driven by robust industrial and agricultural activities.

Driving Factors

Increasing Demand in the Biodiesel Industry Drives Market Growth

Palm acid oil has emerged as a valuable feedstock for biodiesel production due to its high free fatty acid content and lower cost compared to refined palm oil. As countries worldwide push for renewable energy sources to reduce carbon emissions, the demand for biodiesel is rising, consequently driving the palm acid oil market.

For instance, Indonesia, the world's largest palm oil producer, has implemented a B30 biodiesel mandate (30% biodiesel blend), which has significantly increased the demand for palm acid oil as a biodiesel feedstock. This policy-driven demand is expected to continue supporting market growth in the coming years. The interaction between government policies promoting renewable energy and the need for cost-effective biodiesel feedstocks is a key driver in this market.

Growing Applications in the Oleochemical Industry Drive Market Growth

Palm acid oil is increasingly being used as a raw material in the oleochemical industry for the production of fatty acids, fatty alcohols, and glycerol. These derivatives find applications in various industries, including personal care, pharmaceuticals, and industrial chemicals.

The versatility of palm acid oil in oleochemical production is driving its demand. For example, major oleochemical producers like Wilmar International and Emery Oleochemicals are expanding their use of palm acid oil to meet the growing demand for sustainable and bio-based chemicals in products ranging from soaps to lubricants. The alignment of palm acid oil’s properties with the growing demand for bio-based products underscores its significant role in the oleochemical market.

Cost-Effectiveness as an Animal Feed Ingredient Drives Market Growth

Palm acid oil is gaining traction as an energy-rich feed ingredient in animal nutrition, particularly in the poultry feed and swine industries. Its high caloric value and lower cost compared to other vegetable oils make it an attractive option for feed manufacturers looking to optimize feed formulations while managing costs.

For instance, in Malaysia, one of the world's largest palm oil producers, companies like FGV Holdings Berhad are marketing palm acid oil as a cost-effective feed ingredient to local and international livestock producers. This contributes to market growth in the animal nutrition sector. The combination of nutritional value and cost savings makes palm acid oil a preferred choice for animal feed, supporting its market expansion.

Restraining Factors

Quality Inconsistencies and Impurities Restrain Market Growth

Palm acid oil, a by-product of palm oil refining, can exhibit varying quality and impurity levels depending on its source and processing methods. These inconsistencies pose challenges for industries needing standardized inputs, such as biodiesel production or certain oleochemical applications.

For example, biodiesel producers might struggle to meet strict fuel quality standards when using palm acid oil with high impurity levels, necessitating extra processing steps and increasing costs. Such quality variability limits the adoption of palm acid oil in high-value applications, restraining market growth in certain sectors.

Competition from Alternative Feedstocks Restrains Market Growth

Palm acid oil competes with other vegetable oils and by-products in various applications. In the biodiesel industry, used cooking oil (UCO) is becoming more popular due to its lower environmental impact and favorable government incentives. Similarly, in animal nutrition, alternatives like soybean oil or animal fats challenge palm acid oil's market share.

For instance, when soybean oil prices drop, feed manufacturers might prefer it over palm acid oil, potentially limiting the market growth in the animal feed sector. This competition from alternative feedstocks affects the demand and expansion of palm acid oil.

Distribution Channel Analysis

Direct sales lead the distribution channels with a 65% share, influenced by the need for bulk purchasing among large-scale industrial users.

The distribution of Palm Acid Oil is segmented into direct sales and indirect sales. Direct sales hold the majority market share, reflecting the preference of large industrial buyers, like biodiesel producers and soap manufacturers, for establishing long-term, bulk procurement contracts directly with PAO producers. This channel offers cost benefits and supply assurance, which are crucial for operational stability in these industries.

Indirect sales, though smaller, play a vital role in reaching smaller and medium-sized enterprises. This channel includes distributors and traders who supply PAO to markets that do not require large volumes, such as small local soap making workshops or regional animal feed producers.

The growth of the indirect sales channel is supported by the increasing small-scale use and the globalization of supply chains, allowing PAO to reach a broader market. This expansion is essential for the overall stability and growth of the PAO market, catering to varied market demands and consumer bases.

End-Use Industry Analysis

The Biofuel industry, utilizing Palm Acid Oil as a primary feedstock, accounts for 60% of the market, driven by the global push for sustainable energy solutions.

Palm Acid Oil finds significant applications across various end-use industries including the animal feed, biofuel, soap and detergent industries, among others. The biofuel industry dominates this segment, utilizing PAO extensively in biodiesel production due to its renewable profile and cost-effectiveness compared to other biofuel feedstocks. This industry's growth is propelled by global initiatives to reduce carbon emissions and the favorable policies supporting biofuel production.

In the animal feed industry, PAO is used to enhance the energy content of feed products. Its role in the soap and detergent industry is also critical, where it contributes to the saponification process essential for soap production.

Other industries that utilize PAO include the cosmetics industry for products requiring organic and sustainable oils and the chemical industry where PAO is used in various chemical processes. The diverse utility of PAO across these industries not only underscores its importance but also stabilizes its market demand, projecting a steady growth trajectory influenced by global sustainability trends.

Key Market Segments

By Distribution Channel

- Direct Sales

- Indirect Sales

By End-Use Industry

- Animal Feed Industry

- Biofuel Industry

- Soap and Detergent Industry

- Others

Growth Opportunities

Emerging Applications in Biolubricants Offer Growth Opportunity

There's growing potential for palm acid oil in the development of bio-based lubricants. As industries seek more sustainable alternatives to petroleum-based lubricants, palm acid oil's fatty acid composition makes it a promising feedstock for biolubricant production.

This represents a high-value application that could significantly boost the palm acid oil market. For instance, companies like Biosynthetic Technologies are exploring the use of palm-derived fatty acids in the production of high-performance, biodegradable lubricants for automotive and industrial applications, opening up new market opportunities. This trend towards sustainability in industrial applications can drive demand for palm acid oil and promote its growth in new sectors.

Expansion in Personal Care and Cosmetics Offers Growth Opportunity

The personal care and cosmetics industry is increasingly looking for natural, sustainable ingredients, presenting an opportunity for palm acid oil derivatives. Palm-derived fatty acids and alcohols can be used in the formulation of various cosmetic products, from soaps to moisturizers.

For example, Croda International, a major specialty chemical company, has been developing palm-derived ingredients for personal care products, capitalizing on the trend towards natural formulations. This growing demand in the beauty industry could drive innovation in palm acid oil processing and create new market segments. The preference for natural and sustainable ingredients in personal care products offers significant potential for market expansion.

Trending Factors

Increasing Focus on Circular Economy Principles Are Trending Factors

There's a growing trend towards implementing circular economy principles in the palm oil industry, which benefits the palm acid oil market. As a by-product, the efficient utilization of palm acid oil aligns well with waste reduction and resource maximization goals.

For example, Sime Darby Plantation in Malaysia has implemented advanced refining technologies that not only improve palm oil quality but also enhance the recovery and quality of palm acid oil, positioning it as a valuable product rather than a waste stream. This trend is driving innovation in palm oil refining processes, thereby supporting sustainable practices and creating new market opportunities for palm acid oil.

Rise of Palm Oil Sustainability Certifications Are Trending Factors

The trend towards sustainable palm oil production, driven by initiatives like the Roundtable on Sustainable Palm Oil (RSPO), is influencing the palm acid oil market. Certified sustainable palm acid oil is gaining preference among environmentally conscious buyers, particularly in industries like personal care and food.

For instance, AAK, a leading producer of specialty vegetable oils, offers RSPO-certified palm-based ingredients, including those derived from palm acid oil, to meet the growing demand for sustainable options in various industries. This shift towards certified sustainable products is creating a premium market segment, encouraging producers to adopt sustainable practices and gain certifications.

Regional Analysis

APAC Dominates with 38.5% Market Share in the Palm Acid Oil Market

The Asia Pacific (APAC) region's dominance in the palm acid oil market with a 38.5% share is primarily due to the extensive palm oil plantations in countries like Indonesia and Malaysia. These countries are the world's top producers of palm oil, providing a significant raw material base for palm acid oil production. Efficient supply chains and low production costs further bolster the region’s strong position.

APAC benefits from integrated supply chains and mature markets for by-products of palm oil, including palm acid oil. The region’s favorable climate for palm cultivation and the established infrastructure for processing and exportation enhance its market capacity. Additionally, the high demand within the regional biofuel industry and soap manufacturing sector drives significant consumption.

The future influence of APAC in the palm acid oil market appears robust. Continued demand from biofuel sectors and emerging markets for environmentally friendly products are likely to sustain, if not increase, the region's market share. Investments in greener technologies and further expansion of palm cultivation could also support growth.

Regional Market Shares:

- North America: Controls about 15% of the market share. The demand here is driven by the renewable energy sector and industrial applications of palm acid oil.

- Europe: Holds approximately 20% of the market. Europe’s market is driven by stringent environmental regulations favoring sustainable and renewable raw materials in various industries.

- Middle East & Africa: Accounts for around 10% of the global share, with growth influenced by increasing industrialization and the demand for cost-effective raw materials.

- Latin America: With about 16.5% of the market, the region sees growth due to expanding agricultural activities and rising demand for bio-based products.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The palm acid oil market is influenced by major players with strategic positioning and market impact. Wilmar International Limited and Cargill, Incorporated lead with extensive global operations and strong supply chain networks. IOI Corporation Berhad and Kuala Lumpur Kepong Berhad (KLK) emphasize sustainable practices and high-quality production.

Sime Darby Plantation Berhad and Musim Mas Group leverage advanced refining technologies to optimize palm acid oil recovery and quality. PT Astra Agro Lestari Tbk and Golden Agri-Resources Ltd. focus on efficient production methods and strategic market expansions.

Asian Agri and Felda Global Ventures Holdings Berhad (FGV) utilize their large-scale plantations and integrated operations to maintain competitive positions. United Plantations Berhad and Bumitama Agri Ltd. emphasize innovation and sustainability in their production processes.

Genting Plantations Berhad and Mewah International Inc. enhance their market influence through diversified product offerings and strategic partnerships. Sarawak Oil Palms Berhad focuses on improving production efficiency and sustainability to meet market demands.

These companies drive the palm acid oil market through sustainable practices, technological advancements, and strategic expansions, ensuring a competitive and dynamic market environment.

Market Key Players

- Wilmar International Limited

- Cargill, Incorporated

- IOI Corporation Berhad

- Kuala Lumpur Kepong Berhad (KLK)

- Sime Darby Plantation Berhad

- Musim Mas Group

- PT Astra Agro Lestari Tbk

- Golden Agri-Resources Ltd.

- Asian Agri

- Felda Global Ventures Holdings Berhad (FGV)

- United Plantations Berhad

- Bumitama Agri Ltd.

- Genting Plantations Berhad

- Mewah International Inc.

- Sarawak Oil Palms Berhad

Recent Developments

March 2021: Indonesia's Oleochemical Market: Indonesia is reported to have the world's largest capacity for palm oil-based oleochemical production, boasting a capacity of 23.3 million tons annually. The country has seen a significant export increase in oleochemical products, such as fatty acids and methyl esters, with a notable rise during the COVID-19 pandemic. The export value reached USD 2.64 billion in 2020, marking a 26% increase from the previous year (GAPKI).

2023: Musim Mas's Oleochemicals Initiative: Musim Mas has been focusing on transforming palm oil into a variety of oleochemicals. The company emphasizes sustainable production practices and the development of oleochemicals that play a crucial role in everyday products like soaps, detergents, and cosmetics (Musim Mas).

Report Scope

Report Features Description Market Value (2023) USD 1.7 Billion Forecast Revenue (2033) USD 3.3 Billion CAGR (2024-2033) 6.9% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Distribution Channel (Direct Sales, Indirect Sales), By End-Use Industry (Animal Feed Industry, Biofuel Industry, Soap and Detergent Industry, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Wilmar International Limited, Cargill, Incorporated, IOI Corporation Berhad, Kuala Lumpur Kepong Berhad (KLK), Sime Darby Plantation Berhad, Musim Mas Group, PT Astra Agro Lestari Tbk, Golden Agri-Resources Ltd., Asian Agri, Felda Global Ventures Holdings Berhad (FGV), United Plantations Berhad, Bumitama Agri Ltd., Genting Plantations Berhad, Mewah International Inc., Sarawak Oil Palms Berhad Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Wilmar International Limited

- Cargill, Incorporated

- IOI Corporation Berhad

- Kuala Lumpur Kepong Berhad (KLK)

- Sime Darby Plantation Berhad

- Musim Mas Group

- PT Astra Agro Lestari Tbk

- Golden Agri-Resources Ltd.

- Asian Agri

- Felda Global Ventures Holdings Berhad (FGV)

- United Plantations Berhad

- Bumitama Agri Ltd.

- Genting Plantations Berhad

- Mewah International Inc.

- Sarawak Oil Palms Berhad

Our Clients

View Our Licence Options