Metal Bellows Market By Product Type (Welded Bellows, Mechanically Formed Bellows, Others), By Material Type (Titanium Alloys, Stainless Steel Alloys, Nickel Alloys, Others), By End-Use Industry (Aerospace, Automotive, Oil & Gas, Semiconductors, Power generation, Medical, Other), By Application (Traditional Boilers, Gas Turbines, Steam Turbines, Gas Fuel Ducting Systems, Exhaust Systems for Engines), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

45477

-

April 2024

-

250

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

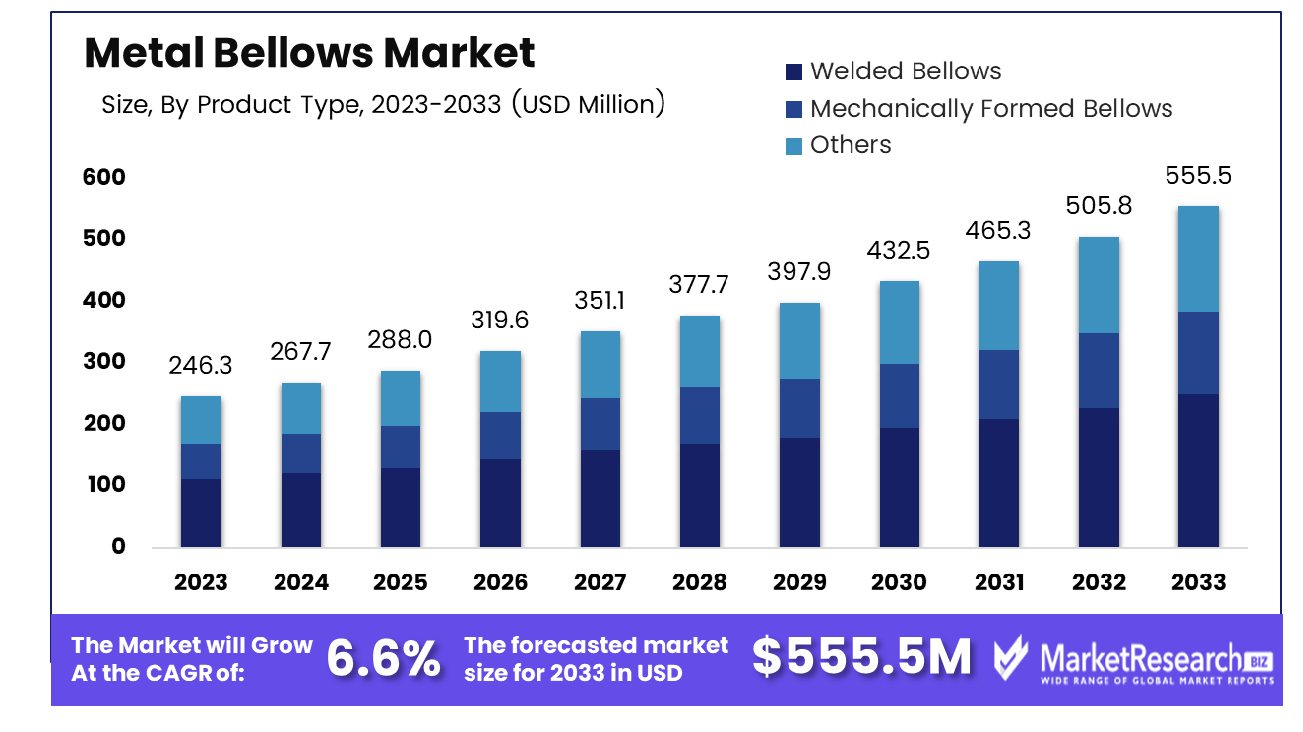

The Global Metal Bellows Market was valued at USD 246.3 Mn in 2023. It is expected to reach USD 555.5 Mn by 2033, with a CAGR of 6.6% during the forecast period from 2024 to 2033.

The Metal Bellows Market encompasses the vibrant sector of flexible mechanical components designed to absorb axial, angular, and lateral movements in various industrial applications. These precision-engineered metallic structures offer unparalleled resilience, ensuring the integrity of critical systems under extreme conditions, such as high pressure, temperature differentials, and corrosive environments. From aerospace to automotive, healthcare to oil and gas, the Metal Bellows Market serves as a cornerstone for innovation and reliability, facilitating seamless operations and enhancing product longevity. Its versatility and adaptability make it an indispensable asset for organizations seeking to optimize performance and mitigate risks across diverse sectors.

The Metal Bellows Market is poised for substantial growth, driven by a myriad of factors including increasing demand from end-use industries such as aerospace, automotive, oil & gas, and healthcare. Metal bellows find extensive applications in these sectors owing to their ability to withstand high pressure, temperature variations, and corrosive environments.

The Metal Bellows Market is poised for substantial growth, driven by a myriad of factors including increasing demand from end-use industries such as aerospace, automotive, oil & gas, and healthcare. Metal bellows find extensive applications in these sectors owing to their ability to withstand high pressure, temperature variations, and corrosive environments.The standard material for metal bellows, titanium-stabilized austenitic stainless steel 1.4571, offers commendable properties such as high corrosion resistance, yield and fatigue strength, workability, weldability, and cost-effectiveness. Additionally, materials like 1.4404 and 1.4441 are gaining traction in niche sectors like food, medical, and vacuum technology applications due to their specific attributes despite marginally reduced mechanical properties compared to 1.4571.

Supportive data indicates that metal bellows exhibit remarkable stability characteristics under symmetrical cyclic tension and compression (SCTC) loading, with deformation primarily concentrated in the wave trough. The gradual stabilization of macroscopic mechanical properties after 20 cycles underscores the reliability and durability of metal bellows, further bolstering their attractiveness across various industries.

Key Takeaways

- Market Value: The Global Metal Bellows Market was valued at USD 246.3 Mn in 2023. It is expected to reach USD 555.5 Mn by 2033, with a CAGR of 6.6% during the forecast period from 2024 to 2033.

- By Product Type: Welded bellows take the lead with a commanding 45% dominance in our product type distribution.

- By Material Type: Stainless steel alloys emerge as the frontrunner in material type, holding a substantial 40% dominance.

- By End-Use Industry: In the realm of end-use industries, Aerospace reigns supreme, commanding a significant 25% dominance.

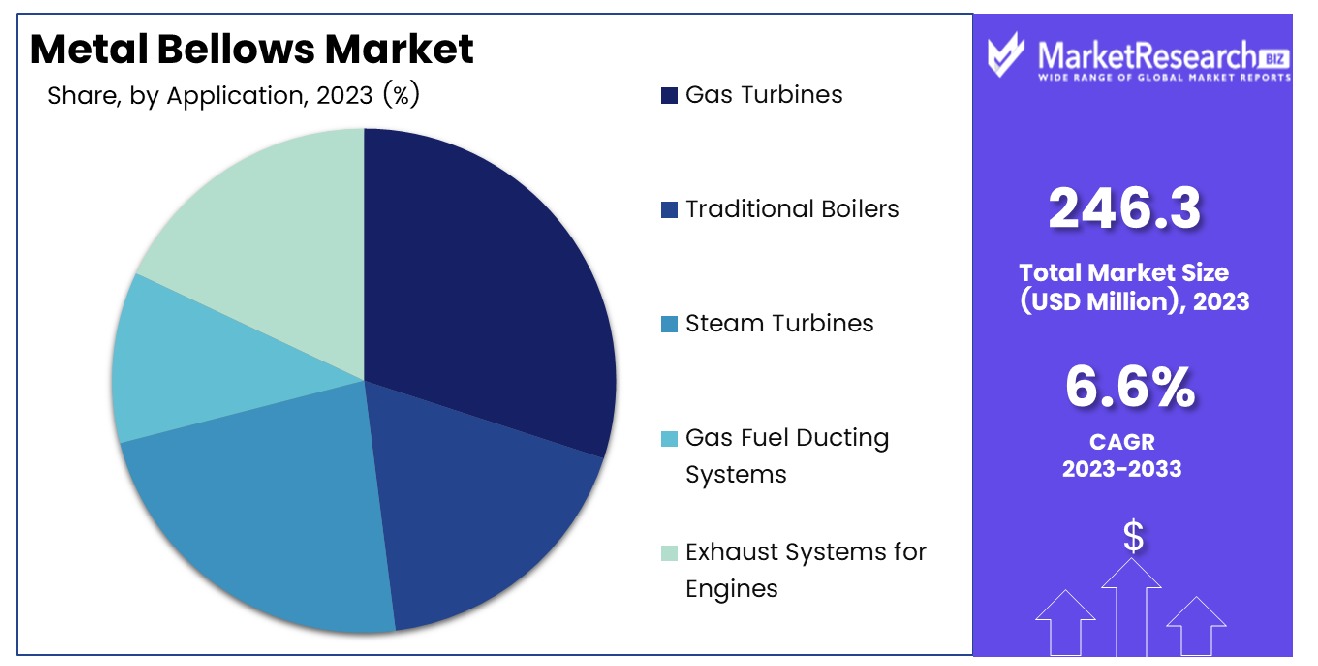

- By Application: Within applications, gas turbines soar to prominence with an impressive 30% dominance, reflecting their pivotal role in power generation.

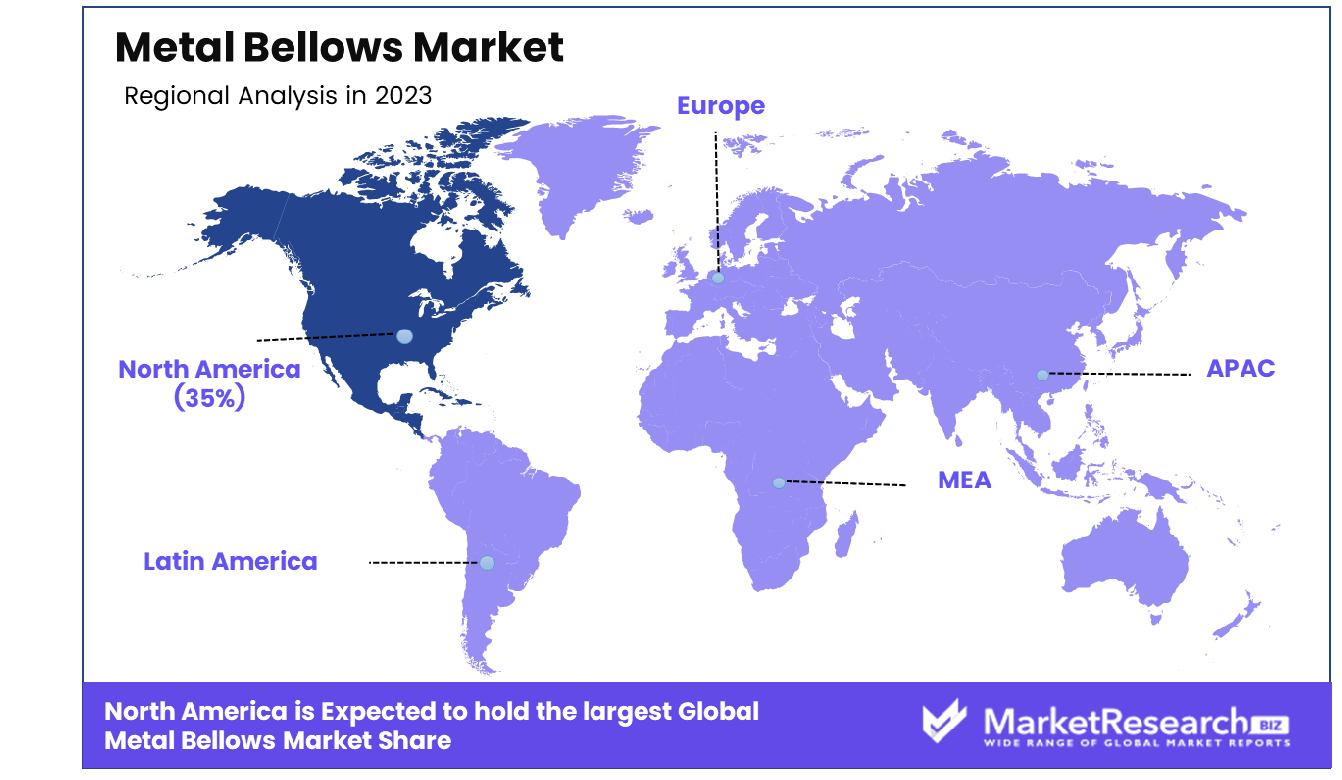

- Regional Dominance: The exact percentage of North America's dominance in the global metal bellows market was estimated to be around 35%.

- Growth Opportunity: The driving force behind the metal bellows market's growth lies in its versatility across diverse industries, propelling demand and innovation. It is expected to experience robust growth fueled by increasing demand from automotive, aerospace, and industrial sectors.

Driving factors

Increasing Demand for Energy-Efficient Appliances

The growing demand for energy-efficient appliances has been a significant driving force behind the expansion of the metal bellows market. As consumers become increasingly conscious of energy consumption and its environmental impact, they are seeking products that offer higher efficiency and reduced energy usage. Metal bellows play a crucial role in enhancing the efficiency of various appliances by providing reliable sealing solutions and precise motion control.

According to recent studies, the global market for energy-efficient appliances is projected to witness substantial growth in the coming years, driven by factors such as government initiatives promoting energy conservation and rising consumer awareness. This upward trend directly benefits the metal bellows market, as manufacturers in industries like HVAC, automotive, and aerospace incorporate these components to improve the energy performance of their products.

Emphasis on Environmental Sustainability

The increasing emphasis on environmental sustainability across industries has propelled the adoption of metal bellows due to their eco-friendly properties and contribution to reducing carbon footprint. As governments worldwide enforce stringent environmental regulations and corporations embrace sustainable practices, the demand for environmentally friendly components has surged.

Metal bellows, known for their durability, reliability, and recyclability, align well with sustainability objectives. Unlike traditional sealing solutions that may contain harmful materials or contribute to pollution through leakage or frequent replacements, metal bellows offer a greener alternative. Their ability to withstand harsh conditions and maintain sealing integrity minimizes resource consumption and waste generation over the product lifecycle.

Diverse Industry Applications

The metal bellows market thrives on its diverse range of applications across various industries, from aerospace and automotive to medical devices and semiconductor manufacturing. This broad applicability ensures a steady demand for metal bellows, regardless of fluctuations in specific sectors, thereby driving market growth.

In aerospace and defense, metal bellows are integral components used in aircraft engines, fuel systems, and avionics for their ability to withstand extreme temperatures, pressure differentials, and vibration. Similarly, in automotive applications, they play a crucial role in exhaust systems, suspension components, and fuel injection systems, contributing to vehicle performance and emissions control.

Technological Advancements in Materials and Manufacturing

Advancements in materials science and manufacturing technologies have been instrumental in enhancing the performance, reliability, and cost-effectiveness of metal bellows, thereby driving market expansion. Innovations in metallurgy, such as the development of high-performance alloys and coatings, have enabled metal bellows to operate in increasingly demanding environments with improved durability and corrosion resistance.

Advancements in manufacturing processes, such as laser welding, hydroforming, and additive manufacturing, have enhanced the precision and scalability of metal bellows production while reducing lead times and production costs. This has widened the application scope of metal bellows and made them more accessible to industries seeking high-performance sealing solutions.

Restraining Factors

Stringent Government Regulations

Metal bellows manufacturers encounter significant challenges due to stringent government regulations. These regulations span various aspects, including product safety standards, environmental compliance, and worker safety. Compliance with these regulations often necessitates substantial investment in research, development, and operational adjustments to meet the required standards.

Additionally, differing regulations across regions or countries can further complicate matters, requiring companies to navigate a complex regulatory landscape. Failure to comply with these regulations can result in fines, legal consequences, damage to reputation, and even market exclusion. Consequently, companies must allocate resources to ensure compliance while simultaneously managing the associated costs and operational impacts. Furthermore, regulatory changes or updates can require swift adaptation, adding another layer of complexity to business operations.

Volatility in Raw Material Prices

The metal bellows industry is highly susceptible to fluctuations in raw material prices, primarily due to its reliance on materials such as stainless steel, titanium, and nickel alloys. Changes in supply and demand dynamics, geopolitical factors, currency fluctuations, and market speculation can all contribute to price volatility. Sudden spikes in raw material prices can significantly impact production costs, squeezing profit margins for manufacturers.

Moreover, the uncertainty surrounding raw material prices can disrupt supply chains, leading to delays, inventory management challenges, and pricing inconsistencies. To mitigate the impact of volatile raw material prices, companies may employ various strategies such as hedging, supplier diversification, long-term contracts, and inventory management techniques. However, effectively managing raw material price volatility remains a persistent challenge in the metal bellows industry.

By Product Type

Welded Bellows dominated the Metal Bellows Market segment, commanding over 40% of the market share.

In 2023, Welded Bellows held a dominant market position in the Welded Bellows segment of the Metal Bellows Market, capturing more than a 40% share. Welded Bellows are renowned for their robust construction and reliability, making them highly sought after across various industries such as aerospace, automotive, and semiconductor manufacturing. Their ability to withstand high pressures and temperatures while maintaining structural integrity has solidified Welded Bellows as the preferred choice for demanding applications where precision and durability are paramount.

Mechanically Formed Bellows, on the other hand, emerged as a strong contender within the Metal Bellows Market, showcasing considerable growth potential. With their versatility and cost-effectiveness, Mechanically Formed Bellows have found widespread adoption in industries ranging from HVAC systems to medical devices. Despite facing stiff competition from Welded Bellows, Mechanically Formed Bellows have carved out a significant niche due to their ability to accommodate varying design specifications and production volumes.

The remaining market share is held by Other types of bellows, which encompass a diverse range of products catering to specialized applications or niche markets. While these segments may not command the same market share as Welded Bellows or Mechanically Formed Bellows, they play a crucial role in fulfilling specific industry requirements where standard bellows may not suffice. Examples of such applications include ultra-high vacuum systems, cryogenic equipment, and precision instrumentation.

By Material Type

Stainless Steel Alloys dominated the Metal Bellows Market's material segment, with over 40% market share.

In 2023, Stainless Steel Alloys held a dominant market position in the By Material Type segment of the Metal Bellows Market, capturing more than a 40% share. Renowned for their exceptional corrosion resistance, high strength, and versatility, Stainless Steel Alloys have emerged as the material of choice across a wide range of industries, including oil and gas, aerospace, and chemical processing. Their ability to withstand harsh environments and extreme temperatures while maintaining structural integrity makes them indispensable for critical applications where reliability is paramount.

Titanium Alloys, though representing a smaller share of the Metal Bellows Market, have exhibited significant growth potential owing to their unique combination of lightweight properties, high strength-to-weight ratio, and exceptional corrosion resistance. Nickel Alloys, while facing competition from Stainless Steel and Titanium, maintain a notable presence in the Metal Bellows Market, particularly in applications requiring superior heat resistance and mechanical properties. Industries such as petrochemicals, power generation, and automotive rely on Nickel Alloys for components operating in high-temperature and corrosive environments, where traditional materials may falter.

The remaining market share is attributed to Other material types, encompassing a variety of specialty alloys and exotic metals tailored to specific application requirements or niche markets. These materials, such as Hastelloy, Inconel, and Monel, find use in specialized applications where standard alloys may not suffice, including nuclear reactors, semiconductor manufacturing, and cryogenic systems.

By End-Use Industry

Aerospace led the Metal Bellows Market segment, commanding over 25% of the market share.

In 2023, Aerospace held a dominant market position in the Aerospace segment of the Metal Bellows Market, capturing more than a 25% share. The aerospace industry demands precision-engineered components that can withstand extreme conditions such as high pressures, temperature differentials, and dynamic forces. Metal bellows play a crucial role in aerospace applications, including aircraft engines, fuel systems, and hydraulic systems, where their reliability, durability, and ability to maintain structural integrity under challenging conditions are paramount.

Following closely behind, Automotive emerged as a significant player in the Metal Bellows Market, driven by the increasing adoption of bellows in automotive exhaust systems, engine mounts, and suspension systems. Metal bellows contribute to improved vehicle performance, reduced emissions, and enhanced durability, aligning with the automotive industry's. Oil & Gas, another key end-use industry segment, relies on metal bellows for critical applications such as valve actuators, pressure sensors, and pipeline expansion joints.

Semiconductors represent a growing market segment for metal bellows, driven by the semiconductor industry's increasing demand for vacuum components and precision instrumentation. Power generation, Medical, and Other industries also contribute to the Metal Bellows Market, albeit with smaller market shares. In power generation, metal bellows are utilized in turbine engines, heat exchangers, and steam systems to accommodate thermal expansion and contraction, vibration isolation, and pressure regulation. The "Other" category encompasses a diverse range of applications, including cryogenic systems, vacuum technology, and industrial automation, where metal bellows fulfill specialized requirements across various industries.

By Application

Gas Turbines dominated the Metal Bellows Market segment, securing over 30% of the market share.

In 2023, Gas Turbines held a dominant market position in the Gas Turbines segment of the Metal Bellows Market, capturing more than a 30% share. Gas turbines are extensively utilized in power generation, aviation, and industrial applications due to their high efficiency, reliability, and versatility. Traditional Boilers, while still significant, represent a slightly smaller share of the Metal Bellows Market compared to Gas Turbines. Metal bellows find application in traditional boiler systems for pressure relief, temperature compensation, and vibration dampening, contributing to improved safety, efficiency, and operational reliability in boiler installations across various industries, including power generation, petrochemicals, and manufacturing.

Steam Turbines, although facing competition from gas turbines, maintain a notable presence in the Metal Bellows Market. Metal bellows are integral components in steam turbine systems, providing sealing solutions for steam inlet and exhaust systems, as well as accommodating thermal expansion and contraction to prevent leaks and ensure efficient energy conversion in power plants and industrial processes. Gas Fuel Ducting Systems represent a specialized segment within the Metal Bellows Market, catering to applications such as natural gas pipelines, fuel delivery systems, and exhaust gas recirculation (EGR) systems in automotive and industrial engines.

Exhaust Systems for Engines, while constituting a smaller share of the Metal Bellows Market, are essential for optimizing engine performance, reducing emissions, and ensuring compliance with regulatory standards. Metal bellows in exhaust systems accommodate thermal expansion, reduce noise and vibration, and provide flexibility for engine movement, contributing to improved efficiency and durability in automotive, marine, and industrial engine applications.

Key Market Segments

By Product Type

- Welded Bellows

- Mechanically Formed Bellows

- Others

By Material Type

- Titanium Alloys

- Stainless Steel Alloys

- Nickel Alloys

- Others

By End-Use Industry

- Aerospace

- Automotive

- Oil & Gas

- Semiconductors

- Power generation

- Medical

- Other

By Application

- Traditional Boilers

- Gas Turbines

- Steam Turbines

- Gas Fuel Ducting Systems

- Exhaust Systems for Engines

Growth Opportunity

Growth in Semiconductor Manufacturing

The semiconductor industry continues to witness robust growth, fueled by technological advancements and the increasing demand for electronics across various sectors. Metal bellows play a crucial role in semiconductor manufacturing processes, particularly in equipment used for vacuum deposition, etching, and ion implantation.

As semiconductor manufacturers scale up production to meet escalating demand, the demand for metal bellows is expected to surge. Additionally, innovations in semiconductor fabrication techniques, such as the adoption of advanced materials and processes, are likely to further drive the demand for specialized metal bellows.

Expansion in Aerospace and Defense Sectors

The aerospace and defense sectors are experiencing significant expansion, driven by increasing defense budgets and a growing demand for commercial aircraft. Metal bellows find extensive applications in critical components of aerospace and defense systems, including actuators, control systems, and propulsion systems.

As aerospace and defense OEMs strive for lighter, more durable, and high-performance solutions, the demand for advanced metal bellows is expected to soar. Moreover, emerging technologies such as unmanned aerial vehicles (UAVs) and space exploration initiatives are creating new avenues for the utilization of metal bellows in novel applications.

Latest Trends

Focus on Energy Efficiency and Sustainability

In response to growing environmental concerns and regulatory pressures, stakeholders in the Metal Bellows Market are increasingly prioritizing energy efficiency and sustainability in their product offerings. Metal bellows, known for their flexibility and durability in various applications, are being redesigned and optimized to enhance energy efficiency and minimize environmental impact.

Manufacturers are exploring innovative materials and manufacturing processes that reduce energy consumption while maintaining product performance. Additionally, there is a rising demand for bellows that contribute to the overall sustainability goals of end-users, especially in industries such as automotive, aerospace, and energy.

Customization and Tailored Solutions for Specific Applications

The demand for customized and tailored solutions is driving innovation in the Metal Bellows Market. End-users across diverse industries have unique requirements and operating conditions that necessitate specialized bellows designs. Manufacturers are investing in advanced engineering capabilities and flexible production processes to deliver bespoke solutions that meet precise specifications and performance criteria.

From extreme temperature environments to corrosive atmospheres, customized bellows are engineered to withstand the most challenging conditions while optimizing performance and longevity. By offering tailored solutions, companies can enhance customer satisfaction, differentiate their offerings, and capture niche market segments.

Regional Analysis

The North American metal bellows market is booming, capturing a hefty 35% share globally.

The metal bellows market continues to exhibit robust growth, capturing a significant share of the global market with a dominance of 35%, North America is poised to maintain its leading position owing to substantial investments in key industries such as automotive, aerospace, and oil & gas. The United States, being a major contributor, witnesses significant demand owing to the flourishing automotive, aerospace, and semiconductor industries. Increasing investments in research and development activities for product innovation further propel market growth in this region. According to recent market studies, North America commands a dominant share of the global metal bellows market, with a notable percentage of market dominance.

Europe emerges as a prominent market for metal bellows, driven by the thriving automotive and manufacturing sectors. Countries like Germany, France, and the UK are at the forefront of market growth, fueled by investments in industrial automation and expansion of the aerospace industry.

Asia Pacific showcases significant growth opportunities in the metal bellows market, attributed to rapid industrialization, infrastructure development, and the presence of a large manufacturing base. Countries such as China, Japan, and India are witnessing substantial demand for metal bellows across various end-use industries, including automotive, electronics, and healthcare. The region's burgeoning automotive sector, coupled with increasing investments in aerospace and defense, fuels market expansion.

The Middle East & Africa region is experiencing steady growth in the metal bellows market, driven by increasing investments in oil and gas exploration activities, petrochemicals, and construction projects. Countries like Saudi Arabia, UAE, and Qatar are major contributors to market growth due to their significant investments in infrastructure development and industrial expansion.

Latin America emerges as a promising market for metal bellows, supported by growing industrialization and infrastructure development initiatives. Countries like Brazil, Mexico, and Argentina are witnessing increased adoption of metal bellows in sectors such as automotive, oil & gas, and aerospace. Despite economic uncertainties and political challenges, Latin America offers considerable growth prospects for metal bellows manufacturers, fueled by expanding industrial activities and infrastructure projects.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global Metal Bellows Market is poised for significant growth, with several key players positioned to influence market dynamics. Among these, Eaton Corporation Plc emerges as a frontrunner, leveraging its extensive experience and robust technological infrastructure to maintain a competitive edge. As a multinational conglomerate, Eaton's diverse portfolio and strategic investments in R&D enable it to deliver innovative solutions tailored to meet evolving customer needs. Its strong emphasis on quality assurance and adherence to industry standards further solidify its reputation as a reliable supplier in the metal bellows segment.

USA Bellows Inc. stands out as another key player, renowned for its specialization in custom-engineered bellows solutions across various industries. With a focus on precision manufacturing and flexible design capabilities, USA Bellows Inc. continues to attract clients seeking bespoke solutions for demanding applications. The company's commitment to customer satisfaction and continuous improvement underscores its significance in the global market landscape.

Smith Group, Servometer, and EagleBurgmann KE also warrant attention as prominent contributors to the metal bellows market. Each brings unique strengths to the table, whether it's Smith Group's expertise in high-performance bellows for aerospace applications, Servometer's reputation for miniature bellows in medical devices, or EagleBurgmann KE's focus on advanced sealing solutions for industrial processes.

Overall, these key players, along with Duraflex Inc., Technoflex Corporation, EnPro Industries Inc., and others, are expected to drive innovation, expand market reach, and shape the trajectory of the global Metal Bellows Market in 2024 and beyond. Their collective efforts in product development, strategic partnerships, and customer-centric approaches will likely define the competitive landscape and fuel growth opportunities in the coming years.

Market Key Players

- Eaton Corporation Plc

- USA Bellows Inc.

- Smith Group

- Servometer

- EagleBurgmann KE

- Duraflex Inc.

- Technoflex Corporation

- EnPro Industries Inc.

- Hyspan Precision Products Inc.

- Freudenberg Group

- KSM Corporation

- Meggitt PLC

- MW Industries, Inc.

Recent Development

- In January 2024, Nangoku Flexible Hose Industry Co., Ltd., led by Masaki Yokomakura, advances its global expansion strategy, focusing on innovation and quality in liquid hydrogen handling. Targeting ASEAN markets, notably Vietnam, for long-term growth.

- In January 2022, KSM Architecture's design for Metallic Bellows Factory Office in Vallam, India, prioritizes sustainability by utilizing locally sourced bricks, reducing concrete usage, and insulating to decrease CO2 emissions.

- In January 2022, BOA Group's SFZ division contributes to the SILER seismic research project, crafting innovative expansion joints for nuclear power plants, with unprecedented capabilities to withstand extreme pressure and temperature conditions.

Report Scope

Report Features Description Market Value (2023) USD 246.3 Mn Forecast Revenue (2033) USD 555.5 Mn CAGR (2024-2033) 6.6% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Welded Bellows, Mechanically Formed Bellows, Others), By Material Type (Titanium Alloys, Stainless Steel Alloys, Nickel Alloys, Others), By End-Use Industry (Aerospace, Automotive, Oil & Gas, Semiconductors, Power generation, Medical, Other), By Application (Traditional Boilers, Gas Turbines, Steam Turbines, Gas Fuel Ducting Systems, Exhaust Systems for Engines) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Eaton Corporation Plc, USA Bellows Inc., Smith Group, Servometer, EagleBurgmann KE, Duraflex Inc., Technoflex Corporation, EnPro Industries Inc., Hyspan Precision Products Inc., Freudenberg Group, KSM Corporation, Meggitt PLC, MW Industries, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Eaton Corporation Plc

- USA Bellows Inc.

- Smith Group

- Servometer

- EagleBurgmann KE

- Duraflex Inc.

- Technoflex Corporation

- EnPro Industries Inc.

- Hyspan Precision Products Inc.

- Freudenberg Group

- KSM Corporation

- Meggitt PLC

- MW Industries, Inc.

Our Clients

View Our Licence Options