Implantable Drug Delivery Devices Market Implantable Drug Delivery Devices Market, By Product Type (Drug infusion pumps, Intraocular drug delivery devices, Contraceptive drug delivery devices, Stents, Drug-eluting stents, Bio absorbable stents), By Technology (Biodegradable Implants, Non-Biodegradable Implants), By Application (Ophthalmology, Cardiovascular, Birth control/Contraception, Obstetrics and Gynecology, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

2590

-

July 2024

-

179

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

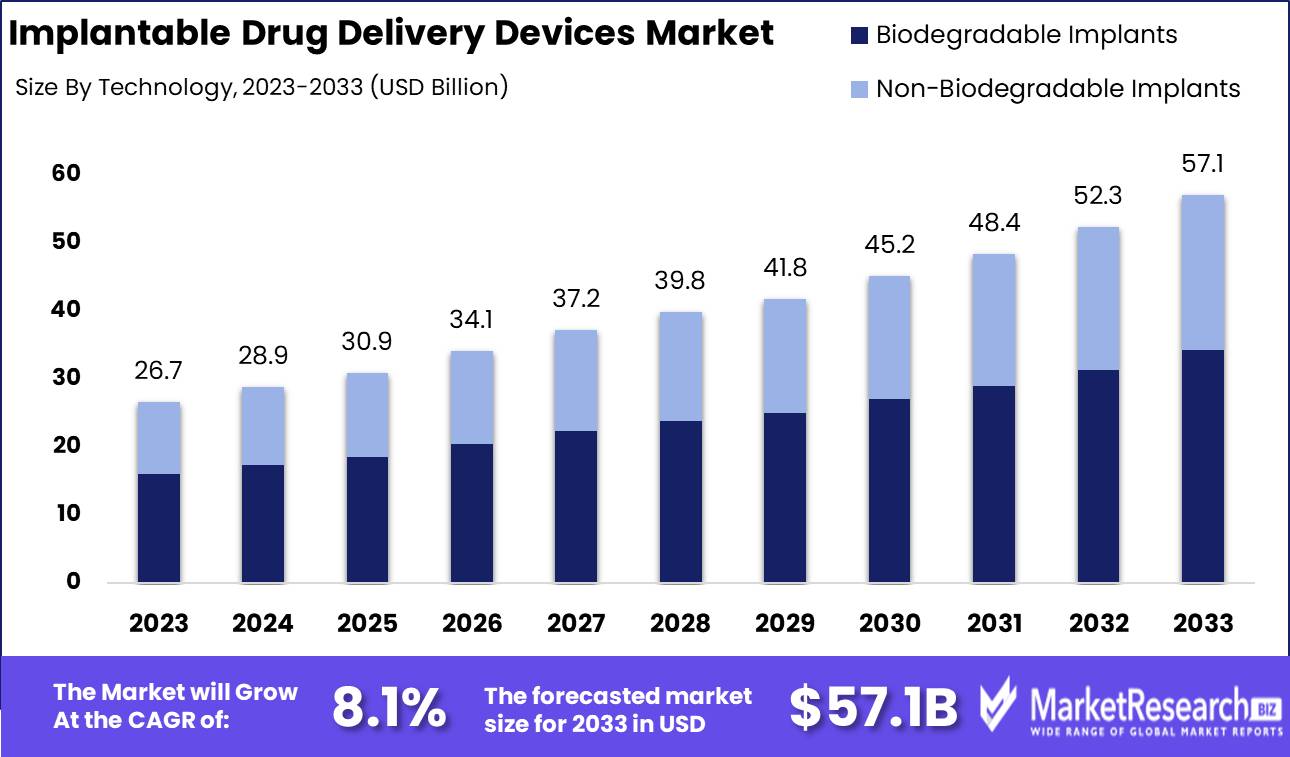

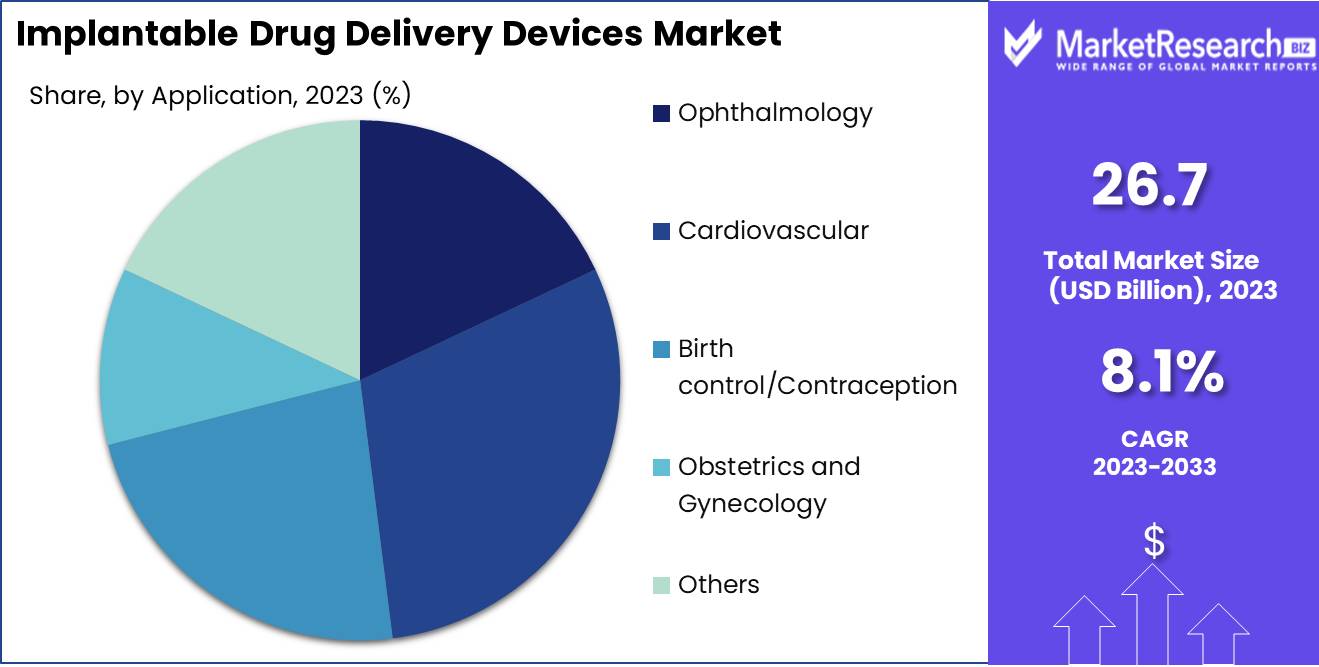

The Global Implantable Drug Delivery Devices Market was valued at USD 26.7 Bn in 2023. It is expected to reach USD 57.1 Bn by 2033, with a CAGR of 8.1% during the forecast period from 2024 to 2033.

The implantable drug delivery devices market encompasses a range of smart medical devices designed to deliver therapeutic agents directly to targeted areas within the body over extended periods. These devices, which include pumps, biodegradable implants, and other sophisticated mechanisms, provide controlled and sustained release of medications, enhancing patient compliance and treatment efficacy. Primarily used in chronic disease management, oncology, pain management, and contraception, implantable drug delivery systems offer significant advantages by minimizing systemic side effects and ensuring precise drug dosage. The market is characterized by ongoing innovations aimed at improving device performance, safety, and patient outcomes.

The implantable drug delivery devices market is poised for substantial growth, driven by advancements in medical technology and a rising prevalence of chronic diseases. The evolution of biodegradable implants in the 2000s marked a significant milestone, particularly in oncology and contraception, where these devices have enabled continuous drug release without the need for surgical removal. This innovation has not only improved patient convenience but also reduced healthcare costs associated with repeated surgical interventions.

The market is witnessing an upsurge in clinical trials, with over 200 trials ongoing in 2021. This surge reflects the increasing confidence and investment in developing sophisticated implantable solutions that promise enhanced therapeutic efficacy and patient adherence. The growing body of clinical evidence supporting the safety and effectiveness of these devices is expected to accelerate regulatory approvals and market adoption.

From a strategic perspective, companies operating in this space should focus on advancing their R&D capabilities to innovate and diversify their product portfolios. Strategic partnerships and acquisitions could play a crucial role in consolidating market positions and expanding geographic reach. Additionally, leveraging data analytics to monitor patient outcomes and device performance can provide valuable insights for continuous improvement and personalized treatment approaches.

Key Takeaways

- Market Value: The Global Implantable Drug Delivery Devices Market was valued at USD 26.7 Bn in 2023. It is expected to reach USD 57.1 Bn by 2033, with a CAGR of 8.1% during the forecast period from 2024 to 2033.

- By Product Type: Drug Infusion Pumps represent 30% of the market, crucial for controlled drug delivery in chronic conditions.

- By Technology: Biodegradable Implants comprise 60%, preferred for their ability to eliminate surgical removal post-treatment.

- By Application: Cardiovascular diseases use 30% of these devices, underscoring the need for precise medication management.

- Regional Dominance: North America holds a 45% share, led by advanced medical technologies and strong healthcare infrastructure.

- Growth Opportunity: Expanding applications in oncology and chronic pain management can significantly drive market growth.

Driving factors

Increasing Prevalence of Chronic Diseases

The rising incidence of chronic diseases such as diabetes, cardiovascular diseases, and cancer is a significant driver for the global drug delivery devices market. Chronic conditions require long-term treatment, often involving complex medication regimens. Drug delivery devices, such as insulin pumps for diabetes or implantable drug-eluting stents for cardiovascular diseases, improve patient compliance and treatment efficacy. According to recent studies, chronic diseases account for approximately 60% of all deaths worldwide, underscoring the urgent need for efficient and user-friendly drug delivery solutions.

Advancements in Drug Delivery Technology

Technological advancements in drug delivery systems have revolutionized patient care by enhancing the precision and efficiency of drug administration. Innovations such as medical injection needle free, smart pills, and micro-needle patches minimize discomfort and improve patient adherence to medication regimes. For instance, smart pills equipped with sensors can monitor drug intake and relay information to healthcare providers, ensuring better disease management. The continuous improvement in these technologies is anticipated to propel market growth significantly.

Growing Demand for Targeted Drug Delivery

Targeted drug delivery systems are designed to deliver drugs directly to the affected area, minimizing systemic side effects and improving therapeutic outcomes. This method is particularly beneficial in cancer treatment, where precision in drug delivery can significantly impact patient survival rates. The increasing adoption of targeted therapies, driven by their superior efficacy and reduced adverse effects, is a critical growth factor for the drug delivery devices market.

Restraining Factors

High Cost of Devices

The high cost associated with advanced drug delivery devices poses a substantial barrier to market growth. Many of these devices, incorporating cutting-edge technology and biocompatible materials, are expensive to produce and purchase. This financial burden limits accessibility, particularly in low- and middle-income countries, thereby constraining the market expansion.

Regulatory Challenges

Regulatory hurdles represent another significant restraint on the market. Drug delivery devices must comply with stringent regulatory standards to ensure safety and efficacy, leading to prolonged approval times and increased development costs. Navigating these complex regulatory landscapes requires substantial investment and expertise, which can delay market entry for new products.

By Product Type Analysis

Drug infusion pumps dominated the By Product Type segment of the Implantable Drug Delivery Devices Market in 2023, capturing more than a 30% share.

In 2023, Drug infusion pumps held a dominant market position in the By Product Type segment of the Implantable Drug Delivery Devices Market, capturing more than a 30% share. This leadership is driven by the critical role these devices play in delivering precise and continuous medication dosages directly into the bloodstream or specific body sites. Drug infusion pumps are extensively used in managing chronic conditions such as cancer, diabetes, and severe pain, providing significant benefits in terms of controlled drug administration and improved patient compliance.

Intraocular drug delivery devices are crucial for treating ocular conditions such as glaucoma, macular degeneration, and diabetic retinopathy. These devices ensure targeted drug delivery within the eye, enhancing therapeutic efficacy while minimizing systemic side effects. Despite their importance, their market share is smaller compared to drug infusion pumps due to the niche nature of ophthalmic applications.

Contraceptive drug delivery devices, including implants and intrauterine devices, provide long-term birth control solutions. They are valued for their high efficacy, convenience, and user compliance. However, their market share remains lower than drug infusion pumps, reflecting the specific application scope and demographic focus.

Stents, including drug-eluting and bioabsorbable stents, are critical in cardiovascular interventions to keep blood vessels open and deliver medication directly to the arterial walls. While these devices are essential in preventing restenosis and enhancing patient outcomes, their combined market share is smaller compared to drug infusion pumps due to their specialized use in cardiovascular treatments.

Bioabsorbable stents offer the added advantage of dissolving within the body after fulfilling their purpose, reducing long-term complications associated with permanent stents. Their adoption is growing, yet their market share is less than that of traditional drug-eluting stents due to higher costs and ongoing clinical evaluations.

By Technology Analysis

Biodegradable Implants dominated the By Technology segment of the Implantable Drug Delivery Devices Market in 2023, capturing more than a 60% share.

In 2023, Biodegradable Implants held a dominant market position in the By Technology segment of the Implantable Drug Delivery Devices Market, capturing more than a 60% share. The prominence of biodegradable implants is driven by their ability to provide therapeutic effects without the need for surgical removal after the treatment period. These implants gradually dissolve within the body, reducing long-term complications and the risk of infection.

Non-Biodegradable Implants, while still crucial in many medical treatments, hold a smaller market share due to the necessity for eventual removal or long-term management of potential complications.

By Application Analysis

Cardiovascular dominated the By Application segment of the Implantable Drug Delivery Devices Market in 2023, capturing more than a 30% share.

In 2023, Cardiovascular applications held a dominant market position in the By Application segment of the Implantable Drug Delivery Devices Market, capturing more than a 30% share. This leadership is attributed to the high prevalence of cardiovascular diseases and the critical need for effective treatment solutions. Implantable drug delivery devices, such as drug-eluting stents and biodegradable vascular scaffolds, play a vital role in managing conditions like coronary artery disease by ensuring localized drug delivery and preventing restenosis.

Ophthalmology applications involve the use of intraocular implants for treating chronic eye conditions, providing localized and sustained drug delivery. While significant, their market share is smaller compared to cardiovascular applications due to the narrower scope of use and patient population.

Birth control/Contraception applications leverage implantable devices to provide long-term contraceptive solutions. These devices offer high efficacy and convenience, contributing to steady market growth. However, the market share remains lower than cardiovascular applications due to the specific demographic and health focus.

Obstetrics and Gynecology applications include implants for hormone therapy and other reproductive health treatments. These devices are essential for managing various conditions but hold a smaller market share compared to broader cardiovascular applications.

Others encompass a range of therapeutic areas, including pain management and oncology, where implantable drug delivery devices provide significant benefits. While important, this category holds a smaller market share due to the diverse and specialized nature of the applications.

Key Market Segments

By Product Type

- Drug infusion pumps

- Intraocular drug delivery devices

- Contraceptive drug delivery devices

- Stents

- Drug-eluting stents

- Bio absorbable stents

By Technology

- Biodegradable Implants

- Non-Biodegradable Implants

By Application

- Ophthalmology

- Cardiovascular

- Birth control/Contraception

- Obstetrics and Gynecology

- Others

Growth Opportunity

Development of Biocompatible Materials

The advent of biocompatible materials presents a substantial growth opportunity for the drug delivery devices market. These materials reduce the risk of adverse reactions and enhance the compatibility of devices with human tissue, improving patient outcomes. Continuous research and development in this area are expected to lead to more innovative and effective drug delivery solutions, driving market growth.

Rising Focus on Personalized Medicine

The shift towards personalized medicine is another promising opportunity for the drug delivery devices market. Personalized medicine tailors treatment to individual patient profiles, necessitating advanced drug delivery systems capable of precise and controlled drug administration. As healthcare moves towards more individualized treatment approaches, the demand for sophisticated drug delivery devices is set to increase, creating significant market opportunities.

Latest Trends

Integration with Smart and Connected Devices

The integration of drug delivery systems with smart and connected devices is a key trend shaping the market. These smart devices enable real-time monitoring and data collection, facilitating better disease management and patient adherence. For example, smart insulin pens can track dosage and timing, sending reminders to patients and data to healthcare providers, thus enhancing treatment outcomes and patient engagement.

Use of Nanotechnology in Drug Delivery Systems

Nanotechnology is revolutionizing drug delivery by enabling the development of nano-carriers that can deliver drugs at the cellular or molecular level. This technology improves the bioavailability and targeting of drugs, reducing side effects and enhancing therapeutic efficacy. The application of nanotechnology in drug delivery systems is anticipated to drive significant advancements in the market, offering more effective and precise treatment options for various diseases.

Regional Analysis

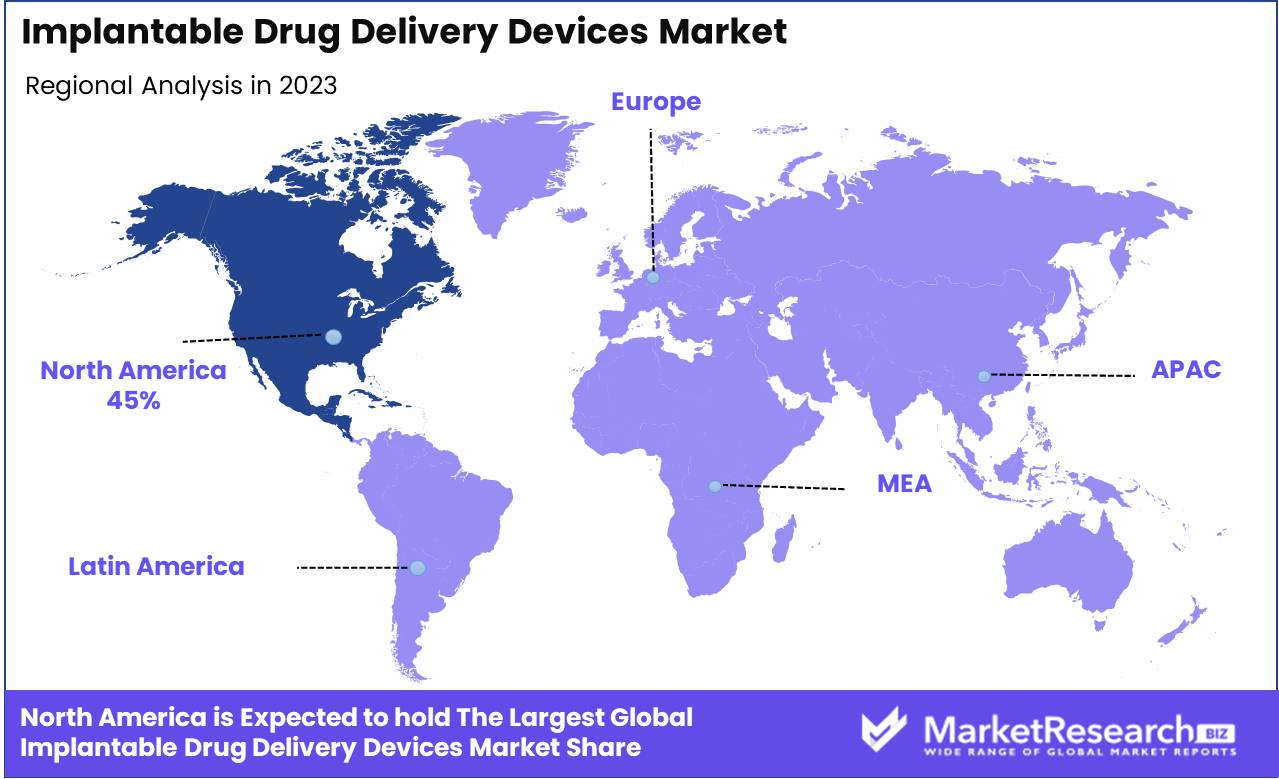

North America dominated the Implantable Drug Delivery Devices Market in 2023, capturing 45% of the market share.

In 2023, North America led the Implantable Drug Delivery Devices Market, capturing a substantial 45% share. This dominance is attributed to the region's advanced healthcare infrastructure, high prevalence of chronic diseases, and significant investment in medical research and development. The United States and Canada are at the forefront, with robust adoption of innovative medical technologies and a strong presence of key market players.

Europe holds a significant position in the market, driven by the growing elderly population and the rising incidence of chronic illnesses. Countries such as Germany, France, and the UK are leading adopters of implantable drug delivery devices due to their advanced healthcare systems and favorable regulatory environments.

Asia Pacific is experiencing rapid growth in the implantable drug delivery devices market, propelled by the increasing healthcare investments, rising prevalence of chronic diseases, and improving healthcare infrastructure in countries like China, India, and Japan. The region's large population base and growing middle class with increasing healthcare awareness contribute to the expanding market.

Middle East & Africa show promising potential, driven by increasing investments in healthcare infrastructure and the growing need for advanced medical treatments. The adoption of implantable drug delivery devices is gradually rising as awareness and access to healthcare services improve.

Latin America is emerging as a growing market for implantable drug delivery devices, with countries like Brazil and Mexico leading the demand. The region benefits from improvements in healthcare infrastructure and a growing focus on advanced medical treatments.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the implantable drug delivery devices market is poised for significant growth, driven by advancements in technology and increasing demand for targeted therapies. Key players in this market include Merck & Co., Inc., Allergan, Inc., Bausch & Lomb Inc., Abbott Laboratories, Bayer AG, Psivida Corp, Medtronic Plc., Arrow International, Boston Scientific Corporation, and Theragenics Corporation.

Merck & Co., Inc. continues to leverage its robust R&D capabilities to innovate in the field of oncology and chronic disease management. Their focus on integrating nanotechnology within drug delivery systems could set new standards for efficacy and safety.

Allergan, Inc., renowned for its expertise in ophthalmology, is expanding its portfolio to include more diverse therapeutic areas. Their implantable devices aim to improve patient compliance and outcomes, particularly in treating chronic eye conditions.

Bausch & Lomb Inc. is expected to make significant strides with its ophthalmic drug delivery implants, focusing on sustained-release mechanisms that enhance therapeutic effects and reduce the frequency of administration.

Abbott Laboratories, with its broad medical device portfolio, is well-positioned to integrate advanced drug delivery systems across various therapeutic areas, particularly cardiovascular and neurological conditions.

Bayer AG’s strong pharmaceutical division is likely to focus on oncology and women’s health, utilizing its proprietary technologies to develop implantable systems that ensure precise drug delivery.

Psivida Corp’s innovative approach in developing sustained-release drug delivery products for ophthalmology places it at the forefront of this niche market. Their micro-insert technologies offer potential for treating chronic eye diseases more effectively.

Medtronic Plc. continues to lead with its extensive expertise in medical devices, offering comprehensive solutions for chronic pain and neurological disorders through implantable pumps and targeted drug delivery systems.

Arrow International, a subsidiary of Teleflex, is expected to expand its product offerings in interventional radiology and oncology, enhancing precision in drug delivery through its catheter-based systems.

Boston Scientific Corporation remains a key player by integrating its expertise in interventional cardiology with drug delivery devices, focusing on improving patient outcomes through innovative, minimally invasive solutions.

Theragenics Corporation, with its focus on brachytherapy, is set to advance its implantable devices for targeted radiation therapy, which could significantly impact the treatment landscape for various cancers.

Market Key Players

- Merck & Co., Inc.

- Allergan, Inc.

- Bausch & Lomb Inc.

- Abbott Laboratories

- Bayer AG

- Psivida Corp

- Medtronic Plc.

- Arrow International

- Boston Scientific Corporation

- Theragenics Corporation

Recent Development

- In June 2024, Medtronic launched a new implantable drug delivery system for chronic pain management, enhancing patient comfort and treatment efficacy.

- In May 2024, Boston Scientific introduced an advanced implantable drug delivery device for targeted cancer therapy, improving precision and outcomes.

Report Scope

Report Features Description Market Value (2023) USD 26.7 Bn Forecast Revenue (2033) USD 57.1 Bn CAGR (2024-2033) 8.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Implantable Drug Delivery Devices Market, By Product Type (Drug infusion pumps, Intraocular drug delivery devices, Contraceptive drug delivery devices, Stents, Drug-eluting stents, Bio absorbable stents), By Technology (Biodegradable Implants, Non-Biodegradable Implants), By Application (Ophthalmology, Cardiovascular, Birth control/Contraception, Obstetrics and Gynecology, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Merck & Co., Inc., Allergan, Inc., Bausch & Lomb Inc., Abbott Laboratories, Bayer AG, Psivida Corp, Medtronic Plc., Arrow International, Boston Scientific Corporation, Theragenics Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Merck & Co., Inc.

- Allergan, Inc.

- Bausch & Lomb Inc.

- Abbott Laboratories

- Bayer AG

- Psivida Corp

- Medtronic Plc.

- Arrow International

- Boston Scientific Corporation

- Theragenics Corporation

Our Clients

View Our Licence Options