Idiopathic Thrombocytopenic Purpura Therapeutics Market By Drug Class (Corticosteroids, Immunoglobulins, Thrombopoietin Receptor Agonists, Others), By End-User (Hospitals, Specialty Clinics, Research Institutes), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

50415

-

Aug 2024

-

302

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

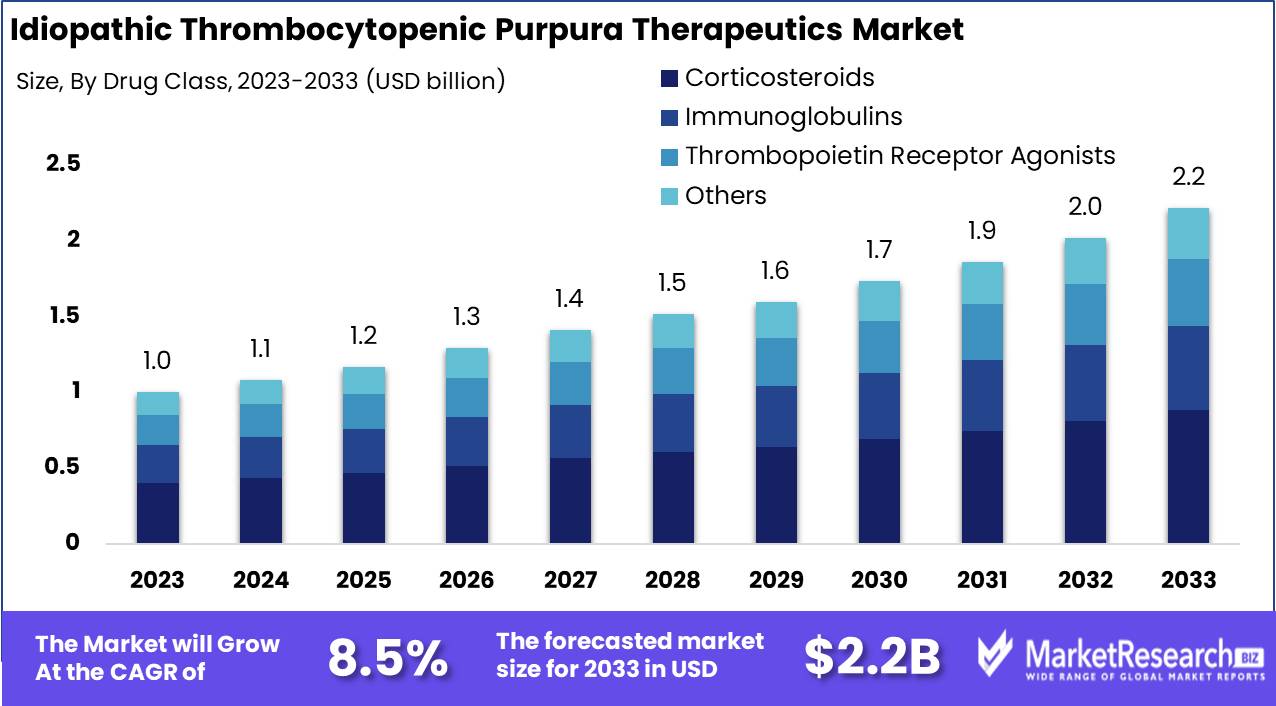

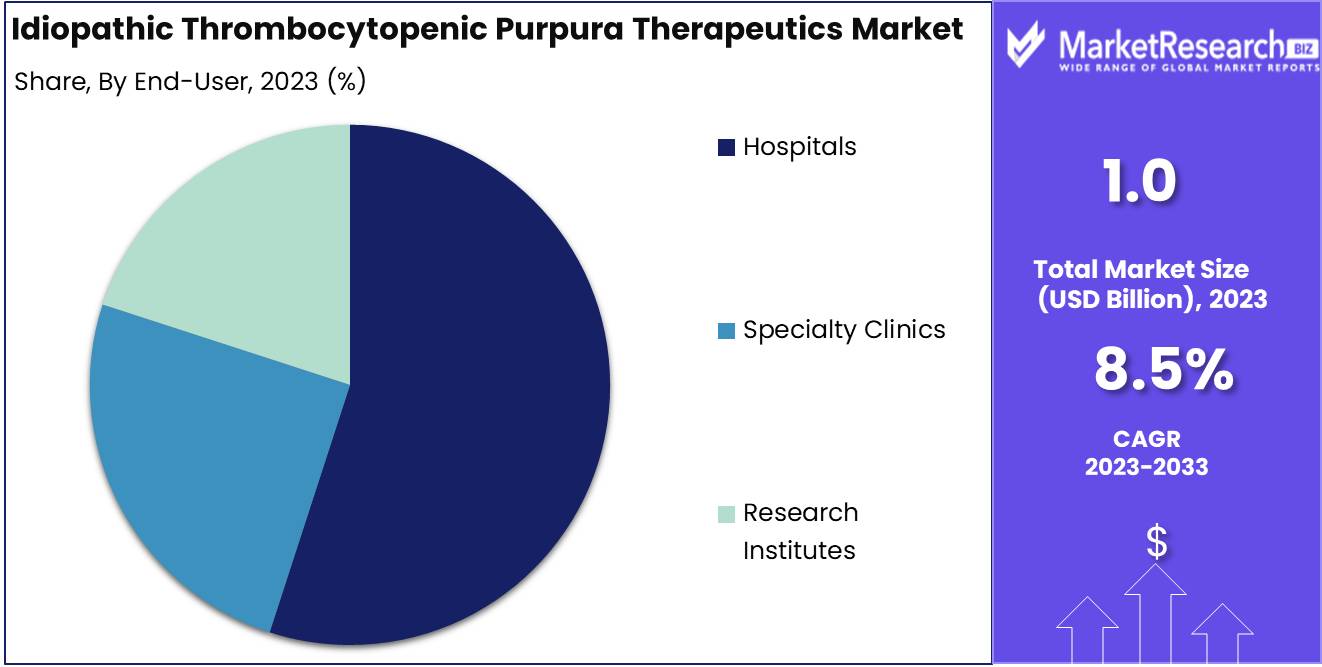

The Global Idiopathic Thrombocytopenic Purpura Therapeutics Market was valued at USD 1 Bn in 2023. It is expected to reach USD 2.2 Bn by 2033, with a CAGR of 8.5% during the forecast period from 2024 to 2033.

The Idiopathic Thrombocytopenic Purpura (ITP) Therapeutics Market focuses on treatments for a rare autoimmune disorder characterized by abnormally low platelet counts, leading to increased bleeding risk. This market includes a range of therapeutic options, such as corticosteroids, immunoglobulins, and thrombopoietin receptor agonists, aimed at managing and improving platelet production. Driven by advancements in biotechnology, increasing awareness, and the development of novel therapies, the market is poised for growth. Ongoing research into personalized medicine and targeted therapies further propels innovation, making ITP therapeutics a critical area of focus within the broader autoimmune disease treatment landscape.

The Idiopathic Thrombocytopenic Purpura (ITP) Therapeutics Market is evolving rapidly, driven by the growing prevalence of autoimmune disorders and significant advancements in treatment modalities. Traditionally, therapies such as corticosteroids and intravenous immunoglobulin (IVIG) have been the mainstay of ITP management, with IVIG known for its effectiveness in rapidly increasing platelet counts within 24 to 48 hours during acute episodes. Ongoing research is focused on optimizing dosing to minimize side effects like neutropenia, a challenge that underscores the need for continued innovation in this space.

The Idiopathic Thrombocytopenic Purpura (ITP) Therapeutics Market is evolving rapidly, driven by the growing prevalence of autoimmune disorders and significant advancements in treatment modalities. Traditionally, therapies such as corticosteroids and intravenous immunoglobulin (IVIG) have been the mainstay of ITP management, with IVIG known for its effectiveness in rapidly increasing platelet counts within 24 to 48 hours during acute episodes. Ongoing research is focused on optimizing dosing to minimize side effects like neutropenia, a challenge that underscores the need for continued innovation in this space.A notable trend within the market is the shift towards personalized medicine, particularly through therapies that modulate B and T cell activity. This approach is reflective of a broader movement in healthcare towards more targeted, individualized treatments. The focus on immune system modulation is particularly relevant in ITP, where the disease's autoimmune nature calls for more sophisticated therapeutic interventions. Currently, there are over 200 clinical trials investigating these novel approaches, highlighting the market’s potential for breakthroughs that could significantly improve patient outcomes.

As the ITP Therapeutics Market continues to advance, companies that invest in the development of personalized therapies and optimize existing treatments are likely to gain a competitive edge. The ongoing clinical trials and research initiatives not only expand the therapeutic landscape but also position the market for substantial growth, making it a critical focus area within the broader field of autoimmune disorder therapeutics.

Key Takeaways

- Market Value: The Global Idiopathic Thrombocytopenic Purpura Therapeutics Market was valued at USD 1.0 Bn in 2023. It is expected to reach USD 2.2 Bn by 2033, with a CAGR of 8.5% during the forecast period from 2024 to 2033.

- By Drug Class: Corticosteroids make up 40% of the market, used as a first-line treatment for this autoimmune disorder.

- By End-User: Hospitals dominate with 55%, providing critical care and treatment for patients with severe cases.

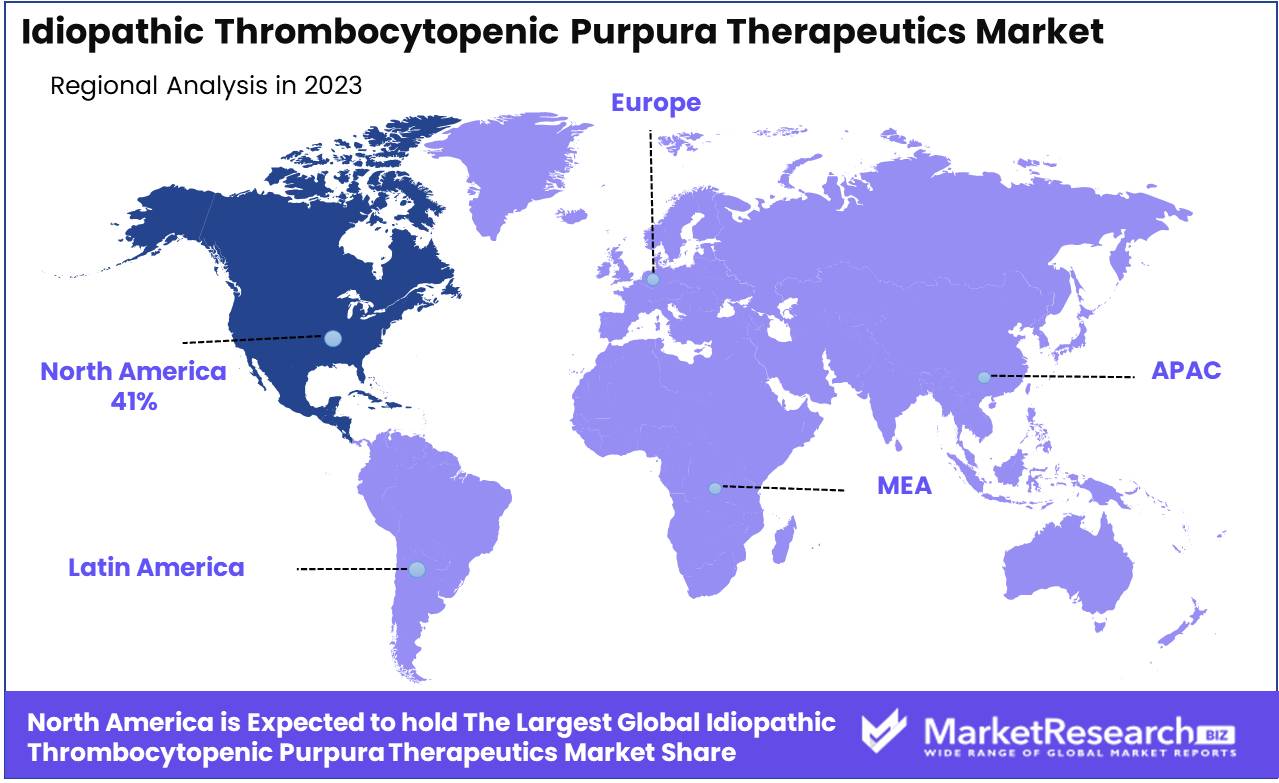

- Regional Dominance: North America holds a 41% market share, driven by advanced healthcare infrastructure and high disease awareness.

- Growth Opportunity: Expanding research into novel therapies and biologics can improve treatment outcomes and drive market growth.

Driving factors

Rising Incidence of ITP and Other Autoimmune Disorders Driving Demand for Effective Therapeutics

The increasing prevalence of Idiopathic Thrombocytopenic Purpura (ITP) and other autoimmune disorders is a significant driver of the ITP therapeutics market. ITP, characterized by a decrease in the platelet count leading to excessive bleeding and bruising, is increasingly recognized as a global health concern. The rising incidence of autoimmune disorders, including ITP, has led to a growing patient population requiring effective treatment options. According to recent epidemiological studies, the global incidence of ITP is estimated to be between 2 to 4 cases per 100,000 adults annually, with higher rates observed in children and elderly populations. This growing patient pool directly translates to an increased demand for specialized therapeutics, driving the expansion of the market.

The rising incidence of other autoimmune disorders such as lupus, rheumatoid arthritis, and multiple sclerosis has contributed to the heightened awareness and diagnosis of ITP. As autoimmune disorders often coexist or increase the likelihood of developing conditions like ITP, the interconnected rise of these diseases has bolstered the demand for targeted therapies. This trend is expected to continue as the incidence of autoimmune diseases grows, emphasizing the need for continued advancements in ITP therapeutics to meet the increasing demand from a larger patient population.

Advancements in Immunotherapy and Targeted Treatments Catalyzing Market Growth

Advancements in immunotherapy and targeted treatments are playing a crucial role in the growth of the ITP therapeutics market. The shift from traditional therapies, such as corticosteroids and splenectomy, to innovative immunotherapeutic approaches has revolutionized the treatment landscape for ITP. Immunotherapies, including monoclonal antibodies like rituximab and thrombopoietin receptor agonists (TPO-RAs) such as eltrombopag and romiplostim, have demonstrated significant efficacy in managing ITP, particularly in patients who are refractory to conventional treatments. These advancements have not only improved patient outcomes but also expanded the therapeutic options available, thereby fueling market growth.

Targeted treatments have also emerged as a game-changer in ITP management. The development of therapies that specifically target the underlying immune mechanisms responsible for platelet destruction has enhanced the precision and effectiveness of treatment. The use of drugs targeting the Fc receptor pathway or the B-cell depletion mechanism has shown promise in controlling the disease with fewer side effects. The continuous innovation in this space is expected to drive the adoption of these advanced therapies, leading to a robust expansion of the ITP therapeutics market in the coming years.

Increasing Awareness and Diagnosis Rates Elevating Market Opportunities

The growing awareness and improved diagnosis rates of ITP are key contributors to the market's expansion. Historically, ITP was often underdiagnosed due to its nonspecific symptoms and the limited availability of diagnostic tools. Increased awareness campaigns, better education among healthcare professionals, and advancements in diagnostic technologies have significantly improved the detection of ITP. The availability of more accurate and accessible diagnostic methods, such as flow cytometry and advanced blood tests, has led to earlier and more precise diagnosis, allowing for timely intervention and management of the disease.

Increased awareness has also driven patient engagement and proactive healthcare seeking behavior. Patients are now more informed about the symptoms and risks associated with ITP, leading to earlier consultation with healthcare providers and subsequent diagnosis. This shift in patient behavior, coupled with the rising awareness among physicians, has expanded the diagnosed patient population, thereby increasing the demand for therapeutic solutions. As awareness and diagnostic capabilities continue to improve, the ITP therapeutics market is poised for sustained growth, with a greater emphasis on early and effective treatment interventions.

Restraining Factors

High Cost of Treatment and Limited Access in Developing Regions Constraining Market Expansion

The high cost of Idiopathic Thrombocytopenic Purpura (ITP) treatments remains a significant retraining factor, particularly in developing regions. Advanced therapies, such as immunotherapies and targeted treatments, are often expensive, placing a substantial financial burden on patients and healthcare systems. In many low- and middle-income countries, the lack of affordable healthcare options exacerbates the issue, limiting access to these cutting-edge treatments. Patients in these regions may rely on less effective or outdated therapies, thereby stalling the overall market growth.

Limited healthcare infrastructure in developing regions further hinders access to effective ITP treatments. The scarcity of specialized healthcare providers and diagnostic facilities, coupled with inadequate healthcare funding, restricts the availability of advanced therapies. This scenario contributes to delayed diagnosis and suboptimal management of ITP, resulting in poorer patient outcomes. To achieve more equitable growth in the global ITP therapeutics market, addressing the cost barriers and improving healthcare infrastructure in these regions is essential.

Side Effects and Risks Associated with Long-Term Therapy Diminishing Patient Compliance

The side effects and risks associated with long-term therapy for ITP pose another significant retraining factor in the market. While advanced therapies such as thrombopoietin receptor agonists (TPO-RAs) and immunotherapies offer substantial benefits, they are often accompanied by adverse effects that can impact patient quality of life. Common side effects include fatigue, headaches, and an increased risk of infections, particularly with immunosuppressive treatments.

The long-term risks associated with continuous treatment can be a deterrent for both patients and healthcare providers. Concerns about potential complications, such as increased risk of thromboembolic events or secondary malignancies, may lead to cautious use of these therapies, particularly in older or more vulnerable patient populations. These risks necessitate close monitoring and frequent adjustments to treatment regimens, further complicating the management of ITP. The need to balance the benefits of long-term therapy with its associated risks and side effects remains a critical challenge, potentially limiting the broader adoption of advanced ITP treatments.

By Drug Class Analysis

In 2023, Corticosteroids held a dominant market position in the By Drug Class segment of the Idiopathic Thrombocytopenic Purpura Therapeutics Market, capturing more than a 40% share.

Corticosteroids are the first-line treatment for Idiopathic Thrombocytopenic Purpura (ITP) due to their effectiveness in rapidly increasing platelet counts in patients. Their ability to suppress the immune system’s attack on platelets makes them a widely used option, particularly in acute cases. The broad application of corticosteroids, coupled with their availability and the immediate therapeutic effects they provide, solidifies their leading position in this segment. Their cost-effectiveness and well-established use in clinical trials contribute to their significant market share.

Thrombopoietin Receptor Agonists (TPO-RAs) and Immunoglobulins also play crucial roles in the management of ITP, especially in patients who are refractory to corticosteroids or require long-term management. TPO-RAs help in stimulating platelet production, while Immunoglobulins are often used in cases where a rapid increase in platelet count is necessary. Although these treatments are vital, their higher costs and more specific indications result in a smaller market share compared to corticosteroids.

By End-User Analysis

In 2023, Hospitals held a dominant market position in the By End-User segment of the Idiopathic Thrombocytopenic Purpura Therapeutics Market, capturing more than a 55% share.

Hospitals are the primary treatment centers for patients with Idiopathic Thrombocytopenic Purpura, especially those with severe or acute presentations. The need for continuous monitoring, emergency care, and complex treatment regimens in hospital settings drives the demand for ITP therapeutics in this segment. Hospitals are equipped with specialized healthcare providers and advanced facilities, making them the most trusted end-users for managing ITP cases. This environment ensures that patients receive comprehensive care, including drug administration, monitoring of side effects, and adjustments in therapy, which is critical for successful treatment outcomes.

Specialty Clinics and Research Institutes, while important, cater to a smaller patient population. Specialty clinics often handle chronic cases that require ongoing management rather than post-acute care, and research institutes focus on developing new treatments and understanding disease mechanisms. However, the critical and immediate care provided by hospitals in managing ITP cases ensures their dominance in this market segment.

Key Market Segments

By Drug Class

- Corticosteroids

- Immunoglobulins

- Thrombopoietin Receptor Agonists

- Others

By End-User

- Hospitals

- Specialty Clinics

- Research Institutes

Growth Opportunity

Development of Novel Biologics and Small Molecule Therapies

The ongoing development of novel biologics and small molecule therapies presents significant growth opportunities for the Idiopathic Thrombocytopenic Purpura (ITP) therapeutics market in 2024. Biologics, including monoclonal antibodies and other advanced immune-modulating agents, are poised to offer more targeted and effective treatment options for ITP patients, particularly those who are refractory to conventional therapies.

Small molecule therapies, which can be designed to precisely target specific pathways involved in the disease, are also emerging as a promising area of innovation. These advancements are expected to enhance treatment efficacy, reduce side effects, and improve overall patient outcomes, thereby driving market growth. The introduction of these novel therapies will likely expand the treatment landscape, providing healthcare providers with more versatile tools to manage ITP, especially in complex cases.

Expansion in Pediatric and Refractory ITP Treatment

Another critical opportunity lies in the expansion of treatment options for pediatric and refractory ITP patients. Pediatric ITP, which often presents with different clinical challenges compared to adult cases, requires specialized therapeutic approaches. The growing focus on developing safe and effective treatments for children with ITP is expected to drive market expansion.

The management of refractory ITP—where patients do not respond to standard treatments—remains a significant unmet need. The anticipated advancements in novel therapies, coupled with an increased emphasis on addressing refractory cases, will create substantial growth opportunities in this segment. By targeting these specific patient populations, the ITP therapeutics market is poised for robust expansion in 2024, capitalizing on the need for more effective and personalized treatment options.

Latest Trends

Use of Personalized Medicine Approaches in ITP Management

One of the most prominent trends in the 2024 Idiopathic Thrombocytopenic Purpura (ITP) therapeutics market is the growing adoption of personalized medicine. As the understanding of ITP's pathophysiology deepens, there is a shift towards tailoring treatment strategies to the individual patient's genetic and immunological profile. Personalized medicine approaches enable healthcare providers to identify the most effective treatment options with minimal side effects, based on a patient’s unique characteristics.

This trend is particularly significant in ITP management, where response to treatment can vary widely among patients. By leveraging advances in genomics and biomarkers, personalized medicine is set to enhance treatment efficacy and patient outcomes, positioning it as a key driver of market growth in 2024.

Growing Interest in Combination Therapies for Improved Outcomes

Another key trend shaping the ITP therapeutics market in 2024 is the increasing interest in combination therapies. Given the complexity of ITP and the varied responses to monotherapies, combining different therapeutic modalities is gaining traction as a strategy to improve treatment outcomes. The use of thrombopoietin receptor agonists (TPO-RAs) in conjunction with immunosuppressive agents or biologics is being explored to achieve more sustained platelet responses and reduce relapse rates.

The rationale behind combination therapies is to target multiple pathways involved in the disease process, thereby enhancing overall treatment efficacy. As research in this area progresses, combination therapies are expected to become a cornerstone of ITP management, offering new avenues for achieving better patient outcomes and driving market growth.

Regional Analysis

North America is the dominating region in the Idiopathic Thrombocytopenic Purpura (ITP) Therapeutics Market, holding a significant 41% share.

In North America, the Idiopathic Thrombocytopenic Purpura (ITP) Therapeutics Market is driven by advanced healthcare infrastructure, high healthcare spending, and a strong focus on research and development in the field of rare diseases. The United States plays a pivotal role in the region's dominance, with a well-established pharmaceutical industry and robust support from government agencies such as the FDA for the development and approval of novel therapeutics. The presence of key biopharmaceutical companies and academic institutions actively involved in ITP research contributes to the region's 41% market share. The increasing prevalence of ITP and growing awareness about available treatment options are further fueling market growth in North America.

Europe is another critical region in the ITP Therapeutics Market, characterized by strong healthcare systems and significant investments in rare disease research. Countries like Germany, the United Kingdom, and France are leading the market, benefiting from government initiatives and collaborations between research institutions and pharmaceutical companies. The European market is also seeing a rising demand for innovative therapies, particularly with the increasing incidence of ITP among the aging population. The region's focus on improving patient outcomes through advanced therapeutics is driving market growth and positioning Europe as a key player in the global market.

The Asia Pacific region is emerging as a rapidly growing market for ITP therapeutics, supported by increasing healthcare expenditure and rising awareness of rare diseases. Countries such as China, Japan, and India are at the forefront of this growth, driven by a growing prevalence of ITP and improving access to healthcare services. The region's expanding middle class and increasing demand for advanced medical treatments are contributing to the adoption of ITP therapeutics.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the Idiopathic Thrombocytopenic Purpura (ITP) Therapeutics Market is marked by the strong presence of several leading pharmaceutical companies. Amgen Inc. stands out with its pioneering therapies such as Nplate, which has transformed treatment paradigms for ITP. Amgen's commitment to innovation and extensive clinical research reinforces its leadership position in the market.

Novartis AG, with its prominent product Promacta, continues to be a key player by providing effective therapeutic options for ITP patients. Novartis’ focus on expanding its clinical trials and strengthening its product portfolio highlights its strategic approach to addressing unmet medical needs.

CSL Limited, known for its innovative therapies like the CSL Behring product line, contributes significantly to the market. The company’s dedication to research and its global distribution capabilities enhance its competitive standing.

Grifols S.A., Rigel Pharmaceuticals Inc., and Argenx SE further enrich the market with their specialized treatments and ongoing development efforts. Their investment in research and strategic collaborations are instrumental in advancing therapeutic options for ITP.

Market Key Players

- Amgen Inc.

- Novartis AG

- CSL Limited

- Grifols S.A.

- Rigel Pharmaceuticals Inc.

- Argenx SE

- Bioverativ Inc.

- Dova Pharmaceuticals

- Octapharma AG

- Hansa Biopharma AB

Recent Development

- In June 2024, Amgen Inc. announced positive results from a Phase III trial of their novel ITP treatment, which demonstrated a 30% improvement in patient outcomes. These results are anticipated to pave the way for broader market adoption.

- In April 2024, Grifols S.A. expanded its ITP treatment portfolio with the acquisition of a promising biotech company. This acquisition is projected to enhance Grifols' therapeutic offerings and increase their market share by 25%.

Report Scope

Report Features Description Market Value (2023) USD 1 Bn Forecast Revenue (2033) USD 2.2 Bn CAGR (2024-2033) 8.5% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Drug Class (Corticosteroids, Immunoglobulins, Thrombopoietin Receptor Agonists, Others), By End-User (Hospitals, Specialty Clinics, Research Institutes) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Amgen Inc., Novartis AG, CSL Limited, Grifols S.A., Rigel Pharmaceuticals Inc., Argenx SE, Bioverativ Inc., Dova Pharmaceuticals, Octapharma AG, Hansa Biopharma AB Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Amgen Inc.

- Novartis AG

- CSL Limited

- Grifols S.A.

- Rigel Pharmaceuticals Inc.

- Argenx SE

- Bioverativ Inc.

- Dova Pharmaceuticals

- Octapharma AG

- Hansa Biopharma AB

Our Clients

View Our Licence Options