Home Care Packaging Market By Material (Plastic, Paper, Metal, Glass), By Packaging Type (Bags & Pouches, Bottles, Jars & Containers, Boxes, Cans, Others), By Products (Dishwashing, Insecticides, Laundry Care, Toiletries, Polishes, Air Care, Other Products), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

46176

-

May 2024

-

300

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

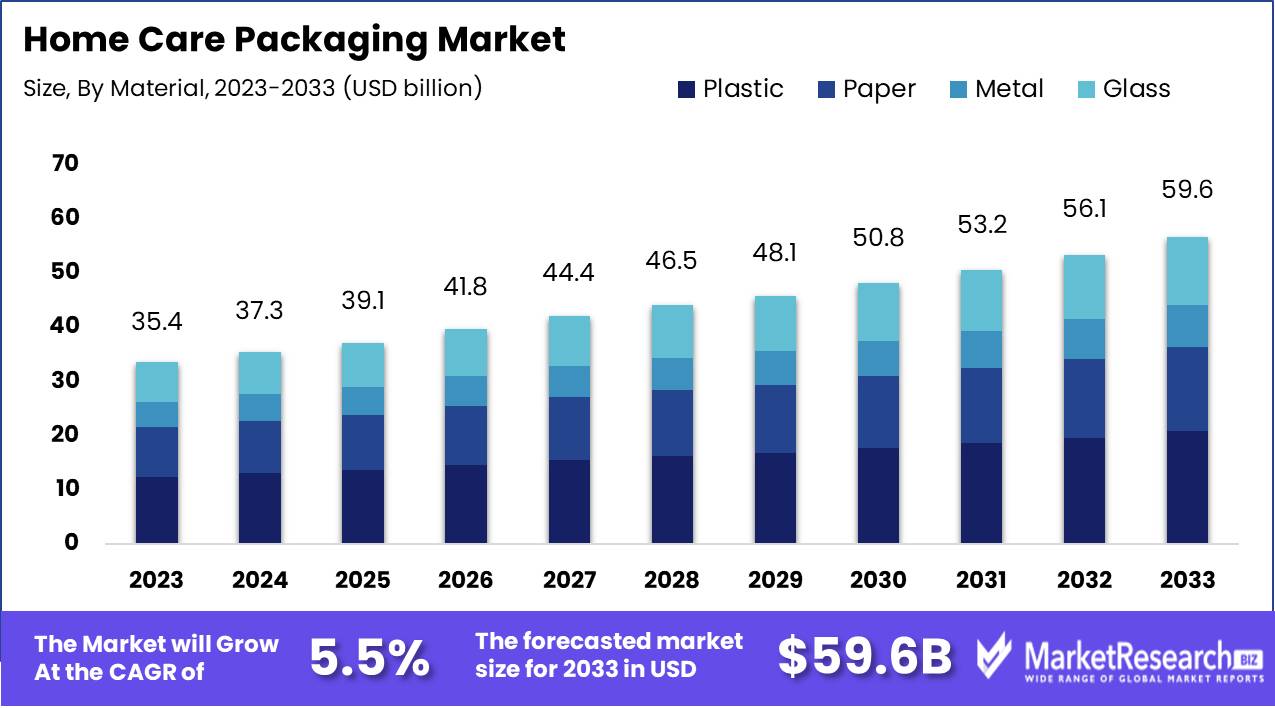

The Home Care Packaging Market size is estimated at USD 35.4 billion in 2023 and is expected to reach USD 59.6 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2024-2033.

The Home Care Packaging Market encompasses the design, production, and distribution of packaging solutions for household care products, including cleaning agents, laundry detergents, and air fresheners. This market is driven by innovations in sustainable materials, consumer demand for convenience, and the need for enhanced product safety. Key trends include the shift towards eco-friendly packaging, advancements in smart packaging technologies, and increased regulatory scrutiny on packaging waste.

The home care packaging market is undergoing significant transformation, driven by evolving consumer preferences and heightened environmental concerns. The shift towards sustainable packaging solutions is a primary trend, as consumers increasingly prioritize eco-friendly products. This shift is not only influencing packaging design but also compelling manufacturers to innovate with materials such as biodegradable plastics and recycled content. Furthermore, the integration of smart packaging technologies, such as QR codes and RFID tags, is enhancing product transparency and consumer engagement. These advancements are particularly pertinent in an era where informed consumers demand greater accountability and information on product sourcing and environmental impact.

According to the report, recent data highlights that 67% of consumers are willing to pay a premium for products with sustainable packaging, reflecting a clear market shift towards eco-conscious purchasing behavior. Additionally, regulatory pressures are mounting, with 58% of global packaging companies reporting increased compliance requirements related to environmental standards. This regulatory landscape is pushing companies to adopt more sustainable practices, driving innovation and investment in new packaging technologies. These statistics underscore the growing importance of sustainability in the home care packaging market, shaping the strategic decisions of industry players.

As companies navigate these shifts, those that can effectively integrate sustainability into their packaging strategies are likely to gain a competitive edge, positioning themselves favorably in a market increasingly defined by environmental stewardship.

Key Takeaways

- Market Growth: The Home Care Packaging Market size is estimated at USD 35.4 billion in 2023 and is expected to reach USD 59.6 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2024-2033.

- By Material: Plastic leads home care packaging due to versatility, cost, and durability.

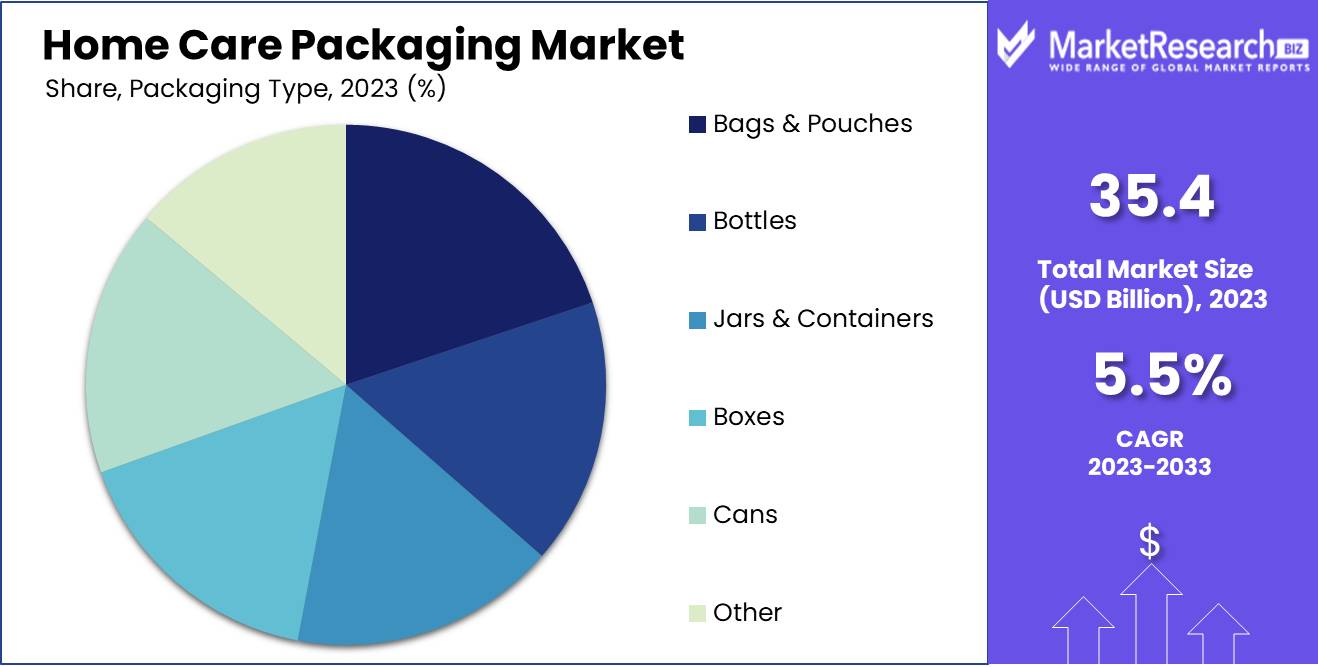

- By Packaging Type: In 2023, Bags and Pouches dominated the home care packaging market.

- By Products: In 2023, Dishwashing led home care packaging with innovative solutions.

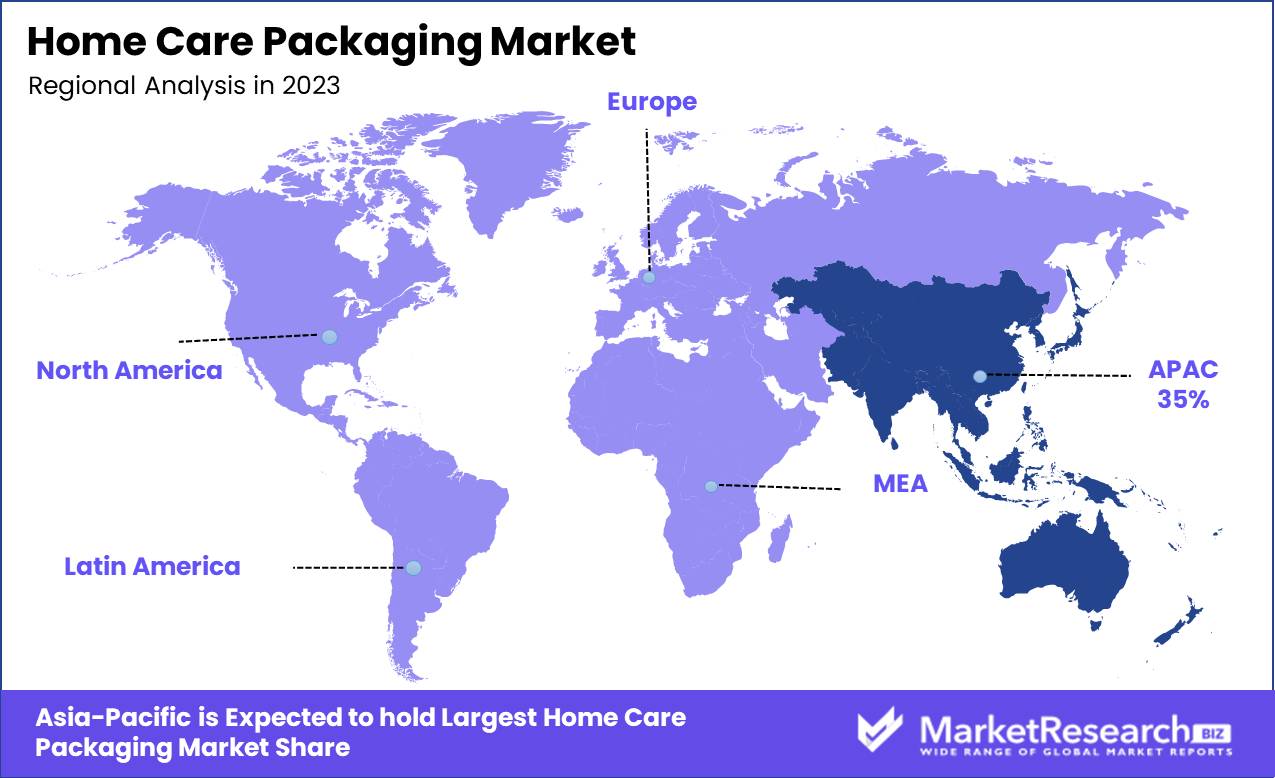

- Regional Dominance: Asia Pacific leads home care packaging, 35% share, driven by urbanization.

- Growth Opportunity: Leveraging health and sustainability trends will drive substantial market growth.

Driving factors

Product Innovation and Differentiation: Catalyzing Market Expansion

Product innovation and differentiation are pivotal in driving the growth of the home care packaging market. Companies continuously invest in developing unique packaging solutions that not only protect the contents but also enhance the user experience. Innovations such as child-resistant packaging, ergonomic designs, and smart packaging that integrate digital elements have set brands apart in a crowded marketplace. For instance, smart packaging that uses QR codes or NFC tags to provide consumers with detailed product information or usage tips can significantly elevate customer engagement and loyalty. This differentiation is crucial as it allows brands to command premium pricing and build a robust market presence.

Consumer Demand for Eco-Friendly Packaging: A Sustainable Growth Driver

The rising consumer demand for eco-friendly packaging is a substantial growth driver in the home care packaging market. With increasing environmental awareness, consumers are gravitating towards products that offer sustainable packaging solutions. This trend is supported by a significant number of consumers willing to pay more for products with minimal environmental impact. According to recent statistics, 73% of global consumers are willing to change their consumption habits to reduce their environmental footprint. Companies are responding by adopting biodegradable materials, and recyclable plastics, and reducing packaging waste.

Convenience and Ease of Use: Enhancing Consumer Experience and Adoption

Convenience and ease of use in packaging significantly influence consumer purchasing decisions and, consequently, care packaging market growth. Modern consumers, especially those with busy lifestyles, prioritize products that offer straightforward and efficient use. Packaging innovations such as easy-to-open lids, single-use packets, and resealable pouches are becoming increasingly popular. These features not only enhance the user experience but also improve product usability and reduce waste. According to a survey, 52% of consumers are more likely to repurchase a product if they find the packaging convenient.

Restraining Factors

High Cost of Raw Materials: A Barrier to Competitive Pricing and Innovation

The home care packaging market faces significant pressure from the escalating costs of raw materials, which substantially impacts the overall market growth. The high cost of raw materials such as plastics, glass, and metals, often driven by fluctuations in the global supply chain and geopolitical factors, directly translates into increased production costs for manufacturers. This, in turn, affects the pricing strategies that companies can adopt, making it challenging to offer competitive prices without compromising on profit margins.

Statistics indicate that the cost of raw materials can account for up to 60% of the total production cost in the packaging industry. As these costs rise, manufacturers may be forced to pass on the increased expenses to consumers, leading to higher retail prices for home care products. This price increase can dampen consumer demand, particularly in price-sensitive markets, thereby restraining the overall market growth.

Lack of Good Recycling Infrastructure: Hindering Sustainability Efforts and Market Expansion

The inadequate recycling infrastructure in many regions poses a significant challenge to the growth of the home care packaging market. Effective recycling systems are essential for managing the disposal and reuse of packaging materials, particularly as consumers and regulatory bodies increasingly prioritize sustainability.

In many parts of the world, the recycling infrastructure is either underdeveloped or inefficient, leading to a low rate of recycling for home care packaging materials. For example, in the United States, only about 9% of plastics are recycled, highlighting the gap between the production of plastic packaging and the capacity to recycle it. This inefficiency results in higher volumes of waste, contributing to environmental pollution and increasing the scrutiny from environmental advocacy groups and regulators.

By Material Analysis

Plastic leads home care packaging due to versatility, cost, and durability.

In 2023, Plastic held a dominant market position in the "By Material" segment of the Home Care Packaging Market. This leadership can be attributed to plastic's versatility, cost-effectiveness, and durability, which make it an ideal choice for a wide range of home care products, including cleaners, detergents, and sprays. Plastic's lightweight nature and ability to be molded into various shapes enhance its appeal for manufacturers seeking innovative packaging solutions that reduce transportation costs and improve shelf appeal.

Conversely, paper packaging is gaining traction due to its eco-friendly attributes and increasing consumer preference for sustainable options. The demand for recyclable and biodegradable packaging is driving the adoption of paper, especially in secondary and tertiary packaging. Metal packaging, known for its robustness and ability to preserve product integrity, is favored in segments where long shelf life and protection from external elements are critical . Glass packaging, though less prevalent due to its fragility and higher cost, is preferred for premium products that benefit from its aesthetic appeal and perception of quality.

By Packaging Type Analysis

In 2023, Bags and Pouches dominated the home care packaging market.

In 2023, Bags and Pouches held a dominant market position in the "By Packaging Type" segment of the Home Care Packaging Market. This segment includes various packaging options such as Bags and Pouches, Bottles, Jars & Containers, Boxes, Cans, and Others. Bags and Pouches gained prominence due to their flexibility, lightweight nature, and cost-effectiveness, catering well to the rising consumer demand for convenient and eco-friendly packaging solutions. Bottles followed, widely preferred for liquid home care products due to their durability and ease of use.

Jars & Containers, though less dominant, are essential for products requiring airtight and resealable options, ensuring product longevity. Boxes are favored for bulk packaging and premium products, offering robustness and enhanced brand presentation. Cans, typically used for aerosol-based home care products, provide superior protection and extended shelf life. The "Others" category encompasses innovative and niche packaging solutions, including biodegradable and reusable options, reflecting the market's adaptation to sustainability trends. Collectively, these segments illustrate a diverse market landscape where functionality, consumer convenience, and sustainability drive packaging choices in the home care industry.

By Products Analysis

In 2023, Dishwashing led home care packaging with innovative solutions.

In 2023, Dishwashing held a dominant market position in the Products segment of the Home Care Packaging Market. This preeminence is driven by the escalating consumer demand for convenient and effective cleaning solutions. With the growing emphasis on hygiene, the dishwashing segment has seen significant advancements in packaging innovation, aimed at enhancing user experience and environmental sustainability.

Meanwhile, Insecticides have maintained a crucial role due to increasing concerns over pest control, necessitating robust and secure packaging solutions. The laundry care sector continues to expand, fueled by urbanization and rising disposable incomes, which drive the demand for diverse and premium packaging options. Toiletries also capture a significant market share, with packaging that focuses on both aesthetic appeal and functionality. Polishes are witnessing steady care packaging market growth, driven by the need for maintenance of household surfaces, thus requiring specialized packaging to ensure product longevity. The Air Care segment is evolving, with innovations in packaging to cater to consumer preferences for aesthetic and long-lasting products.

Lastly, Other Products encompass a wide array of home care items, each necessitating unique and tailored packaging solutions to meet diverse consumer needs and regulatory standards.

Key Market Segments

By Material

- Plastic

- Paper

- Metal

- Glass

By Packaging Type

- Bags & Pouches

- Bottles

- Jars & Containers

- Boxes

- Cans

- Others

By Products

- Dishwashing

- Insecticides

- Laundry Care

- Toiletries

- Polishes

- Air Care

- Other Products

Growth Opportunity

Increasing Health Awareness Driving Market Growth

The global home care packaging market is poised for significant growth in 2024, driven by the rising consumer awareness of health and hygiene. The COVID-19 pandemic has underscored the importance of maintaining cleanliness in residential settings, leading to a heightened demand for home care products. This trend is particularly evident in the increased sales of disinfectants, cleaning agents, and related packaging solutions. Packaging manufacturers are responding by innovating with materials that offer superior protection against contamination, aligning with consumer preferences for products that ensure health and safety.

The Increasing Importance of Sustainability as a Key Market Driver

Sustainability is becoming a cornerstone of the home care packaging market. Consumers are increasingly prioritizing environmentally friendly products, driven by a global push towards reducing plastic waste and carbon footprints. Packaging companies are innovating with biodegradable materials, recyclable plastics, and reusable containers to meet these demands. Additionally, regulatory pressures and corporate sustainability goals are propelling the shift towards greener packaging solutions. Companies that can effectively integrate sustainability into their packaging strategies are likely to gain a competitive edge, attracting eco-conscious consumers and enhancing brand loyalty.

Latest Trends

Increased Focus on Convenience and Portability

In 2024, convenience and portability will significantly drive innovation in the home care packaging market. Consumers’ fast-paced lifestyles demand solutions that simplify everyday tasks, leading to the development of user-friendly packaging designs. Companies are expected to invest heavily in packaging that enhances ease of use, such as single-use pods, resealable pouches, and ergonomic bottle designs. These innovations not only cater to consumer preferences for practicality but also align with environmental goals by reducing product waste. The trend towards smaller, more portable packaging also reflects a broader shift towards urban living and smaller household sizes, necessitating compact and efficient packaging solutions that fit seamlessly into modern living spaces.

Rise of E-commerce and Online Shopping

The surge in e-commerce and online shopping is reshaping the home care packaging landscape, prompting brands to rethink their packaging strategies to meet the unique demands of digital retail. Packaging for e-commerce must ensure product protection during transit, reduce shipping costs, and enhance the unboxing experience, which has become a critical aspect of brand differentiation. In 2024, we anticipate a greater adoption of robust, lightweight, and eco-friendly materials designed to withstand the rigors of shipping while minimizing environmental impact.

Additionally, the rise of subscription services and direct-to-consumer models will drive the need for packaging that supports recurring deliveries, emphasizing durability and convenience. Brands that successfully integrate these elements will likely gain a competitive edge in the increasingly digital marketplace.

Regional Analysis

Asia Pacific leads home care packaging, 35% share, driven by urbanization.

The home care packaging market exhibits significant regional variances driven by consumer preferences, economic conditions, and regulatory environments. North America and Europe are mature markets, characterized by high demand for sustainable and innovative packaging solutions. In North America, the market is propelled by the U.S., which prioritizes eco-friendly homecare packaging, reflecting a compound annual growth rate (CAGR) of 4.1% from 2021 to 2028. Europe follows closely, with stringent regulations and high consumer awareness driving a robust CAGR of 3.8%.

Asia Pacific stands out as the dominating region, accounting for approximately 35% of the global market largest share in 2023. This dominance is fueled by rapid urbanization, rising disposable incomes, and a burgeoning middle class in countries like China and India. China alone represents a significant portion of this growth, with an estimated market value of USD 12 billion in 2023.

The Middle East & Africa and Latin America are emerging markets with substantial potential, driven by improving economic conditions and increasing adoption of home care products. While these regions currently represent smaller market shares, they are expected to witness steady growth rates, contributing to the global expansion of the home care packaging market.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- The rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global home care packaging market is poised for substantial growth, driven by evolving consumer preferences and heightened emphasis on sustainability. Key industry players, including Amcor, PLC, Ball Corporation, RPC Group, Winpak Ltd, AptarGroup Inc., Sonoco Products Company, Silgan Holdings, Constantia Flexibles Group GmbH, DS Smith PLC, Can-Pack SA, and ProAmpac LLC, are strategically positioned to capitalize on these trends.

Amcor and Ball Corporation are leveraging their extensive R&D capabilities to innovate eco-friendly packaging solutions, aligning with the increasing demand for sustainable products. RPC Group and Winpak Ltd are focusing on advanced barrier properties and lightweight materials, addressing both functionality and environmental concerns.

AptarGroup Inc. and Sonoco Products Company are enhancing their portfolios with smart packaging technologies, improving consumer convenience and product safety. Silgan Holdings and Constantia Flexibles Group GmbH are expanding their market reach through strategic acquisitions and partnerships, aiming to consolidate their positions in the global market.

DS Smith PLC and Can-Pack SA are emphasizing circular economy principles, incorporating recycled materials to meet regulatory requirements and consumer expectations. ProAmpac LLC is differentiating itself through customizable and innovative packaging designs, catering to diverse consumer needs.

Market Key Players

- Amcor

- PLC

- Ball Corporation

- RPC Group

- Winpak Ltd

- AptarGroup Inc.

- Sonoco Products Company

- Silgan Holdings

- Constantia Flexibles Group GmbH

- DS Smith PLC

- Can-Pack SA

- ProAmpac LLC

Recent Development

- In April 2024, Unilever announced a major shift towards 100% recyclable packaging for its home care products by 2025, significantly accelerating its sustainability efforts.

- In February 2024, Procter & Gamble introduced a new line of concentrated cleaning solutions that use 50% less packaging, responding to increasing consumer demand for environmentally friendly products.

- In December 2023, Mondi Group announced the launch of the EcoWicketBag, a paper-based diaper packaging that is fully compostable and recyclable, enhancing its sustainability credentials.

Report Scope

Report Features Description Market Value (2023) USD 35.4 Billion Forecast Revenue (2033) USD 59.6 Billion CAGR (2024-2032) 5.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Material (Plastic, Paper, Metal, Glass), By Packaging Type (Bags & Pouches, Bottles, Jars & Containers, Boxes, Cans, Others), By Products (Dishwashing, Insecticides, Laundry Care, Toiletries, Polishes, Air Care, Other Products) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Amcor , PLC , Ball Corporation , RPC Group , Winpak Ltd , AptarGroup Inc. , Sonoco Products Company , Silgan Holdings , Constantia Flexibles Group GmbH , DS Smith PLC , Can-Pack SA , ProAmpac LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Amcor

- PLC

- Ball Corporation

- RPC Group

- Winpak Ltd

- AptarGroup Inc.

- Sonoco Products Company

- Silgan Holdings

- Constantia Flexibles Group GmbH

- DS Smith PLC

- Can-Pack SA

- ProAmpac LLC

Our Clients

View Our Licence Options