Global Healthy Energy Drink Market By Type(Traditional Health, Natural/Organic, Functional, Sports Performance, Low-Calorie, Others), By Packaging Type(Glass Bottles, Metal Can, PET Bottles), By Format(Shots, Powder, Ready-To-Drink (RTD)), By End User(Kids, Adults, Teenagers), By Distribution Channel(Convenience Stores, Online Retail, Supermarket/Hypermarket, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

47290

-

June 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

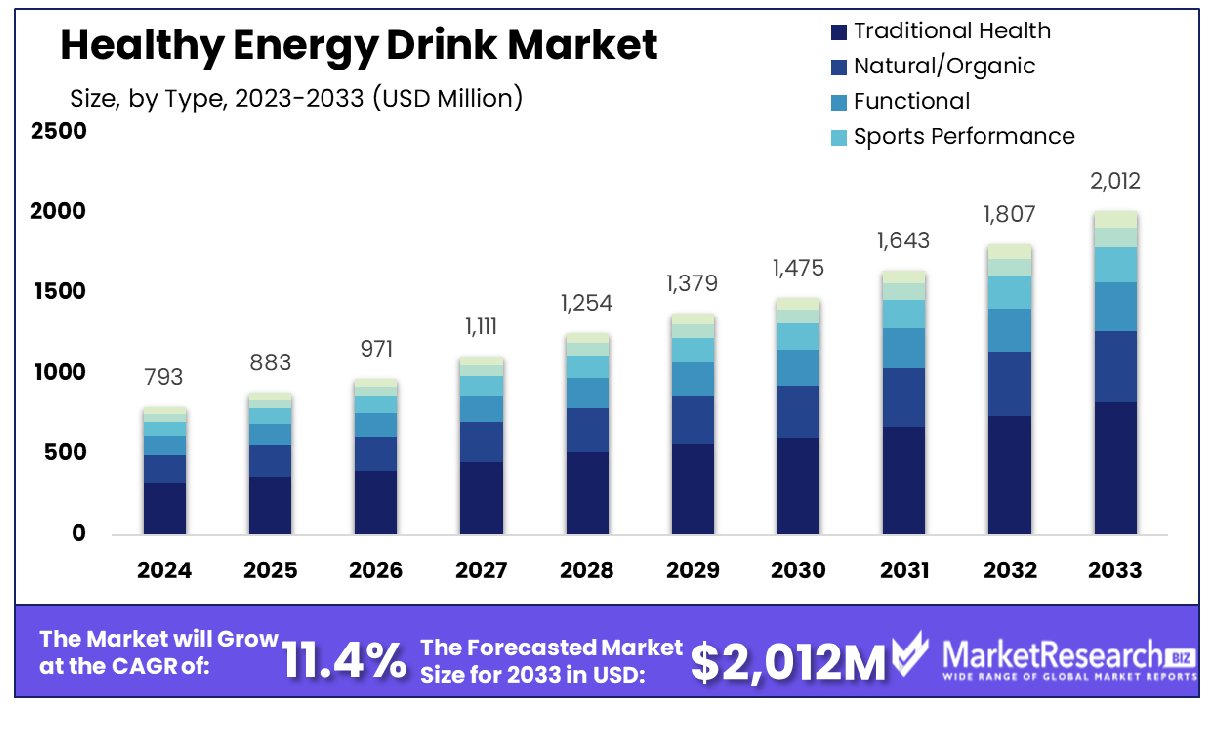

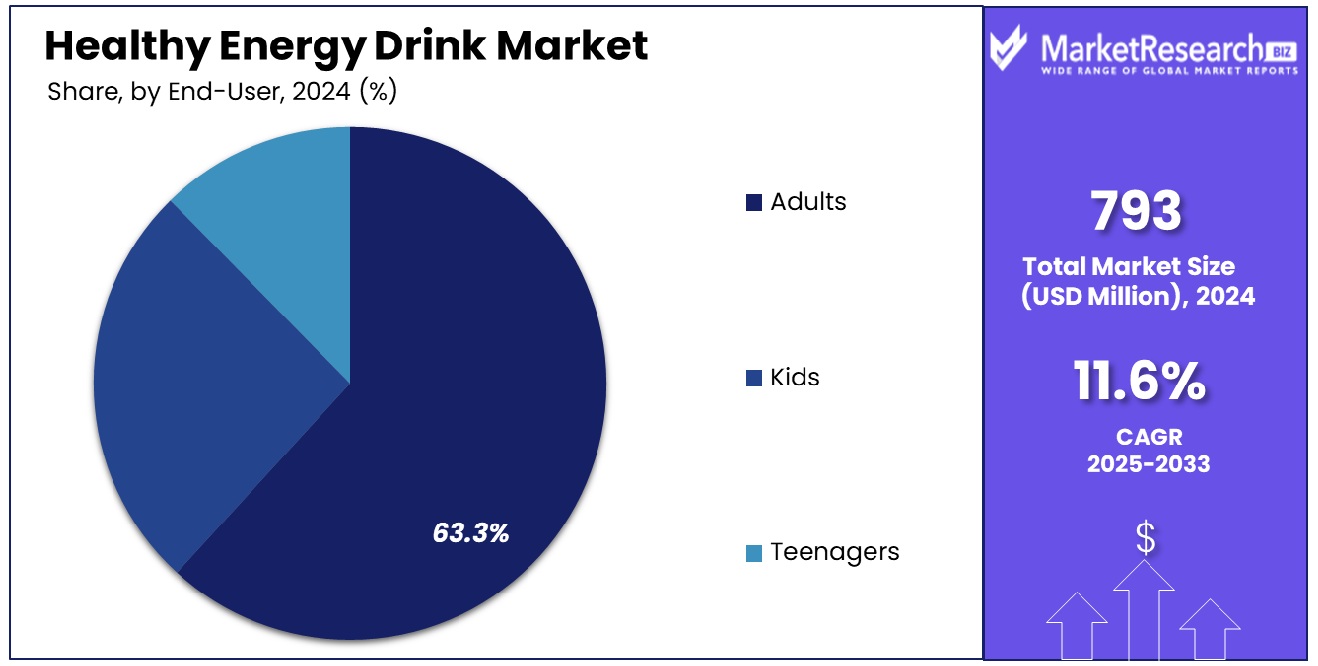

The Global Healthy Energy Drink Market was valued at USD 793 Million in 2023. It is expected to reach USD 2012 Million by 2033, with a CAGR of 11.40% during the forecast period from 2024 to 2033.

The Healthy Energy Drink Market refers to the dynamic segment within the beverage industry that caters to consumers seeking revitalization and wellness without compromising on health standards. These drinks typically offer a potent blend of natural ingredients, including vitamins, minerals, adaptogens, and organic stimulants, aimed at providing sustained energy levels and promoting overall well-being.

With a growing emphasis on health-conscious lifestyles, this market is witnessing robust expansion, fueled by increasing consumer awareness regarding the adverse effects of traditional energy drinks. Key players are innovating to meet evolving consumer preferences, presenting lucrative opportunities for strategic product differentiation and market penetration.

The Healthy Energy Drink Market has witnessed significant growth in recent years, driven by consumers' increasing demand for functional beverages that offer sustained energy without compromising on health. This surge can be attributed to several factors, including rising health consciousness among consumers, the desire for natural and organic ingredients, and the need for convenient energy-boosting solutions in today's fast-paced lifestyle.

In this context, it's imperative to highlight the prevailing concerns associated with traditional energy drinks, which typically contain high levels of caffeine substitutes and sugar. With energy drinks commonly harboring 80-150 mg of caffeine per 8 ounces, equivalent to approximately two 12-ounce cans of caffeinated soda, consumers are becoming increasingly aware of the adverse effects such as increased heart rate, elevated blood pressure, and cardiac arrhythmias. Moreover, the substantial sugar content, averaging 39-41 grams per 12-ounce serving, poses risks of weight gain, type 2 diabetes, cardiovascular diseases, and gout.

Of particular concern is the demographic profile of energy drink consumers, notably adolescents and young adults, despite these beverages being unsuitable for these age groups. The statistics reveal a troubling trend, with over 1,400 adolescents aged 12-17 requiring emergency room visits due to energy drink-related emergencies in 2011 alone.

As the market continues to evolve, consumers are increasingly seeking healthier alternatives that provide sustained energy without the negative health repercussions associated with traditional energy drinks. This paradigm shift presents a lucrative opportunity for companies to innovate and capitalize on the growing demand for healthier energy drink options, tapping into the intersection of functionality, convenience, and wellness in the beverage industry.

Key Takeaways

- Market Growth: The Global Healthy Energy Drink Market was valued at USD 793 Million in 2023. It is expected to reach USD 2012 Million by 2033, with a CAGR of 11.40% during the forecast period from 2024 to 2033.

- By Type: Traditional health products dominate the market share, comprising 41.1%.

- By Packaging Type: Metal cans are the preferred packaging, capturing 41.2% of the market.

- By Format: Ready-to-drink format leads, constitute 45.3% of consumption.

- By End User: Adults represent primary end users, comprising 63.3% of the market.

- By Distribution Channel: Convenience stores are a key distribution channel, capturing 38.4% share.

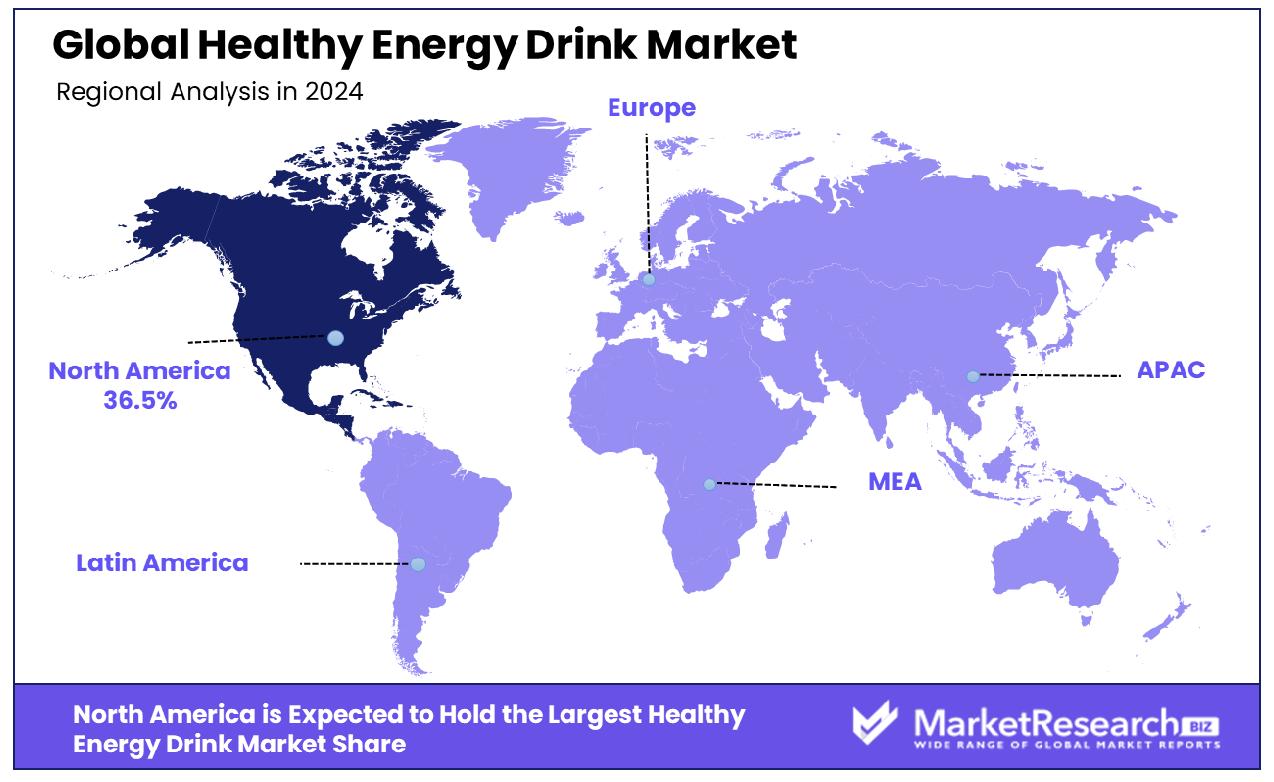

- Regional Dominance: The Healthy Energy Drink market in North America grew by 36.5% over the last fiscal year.

- Growth Opportunity: In 2023, the global healthy energy drink market flourished through expansion into emerging markets and innovation in product formulations and packaging, driven by rising health consciousness among consumers.

Driving factors

Increasing Consumer Awareness about Health and Wellness

The growth of the healthy energy drink market can be attributed significantly to the increasing consumer awareness about health and wellness. As more individuals become conscious of the impact of their dietary choices on overall well-being, there's a discernible shift towards healthier alternatives in the beverage sector. Market research indicates that over 70% of consumers prioritize health benefits when selecting energy drinks.

This heightened awareness prompts consumers to seek products that offer not just a boost in energy but also contribute positively to their health. Healthy energy drinks, positioned as a healthier alternative to traditional options, capitalize on this trend. Through targeted marketing campaigns emphasizing nutritional benefits and reduced sugar content, companies are able to appeal to health-conscious consumers, thereby driving market growth.

Growing Demand for Natural and Organic Ingredients

The surge in demand for natural and organic ingredients plays a pivotal role in propelling the healthy energy drink market forward. Consumers increasingly scrutinize product labels, seeking transparency and cleaner ingredient lists. Market studies reveal that over 60% of consumers are willing to pay a premium for products containing natural ingredients.

In response, manufacturers are reformulating their energy drink offerings to include ingredients like natural caffeine sources, organic fruit extracts, and plant-based sweeteners. This shift not only aligns with consumer preferences but also taps into the broader trend toward clean-label products. As a result, healthy energy drinks positioned as containing natural and organic ingredients experience heightened demand, driving market expansion.

Rising Preference for Functional Beverages

The rising preference for functional beverages is a key driver fueling the growth of the healthy energy drink market. Functional beverages, designed to offer specific health benefits beyond basic hydration, resonate with consumers seeking more from their beverages. Research indicates that nearly 80% of consumers are interested in functional beverages that address specific health concerns.

Healthy energy drinks, formulated to provide not only a boost in energy but also additional benefits such as enhanced focus, immunity support, or stress relief, cater to this demand. By incorporating ingredients like adaptogens, vitamins, and amino acids, these beverages offer a holistic approach to health and wellness, appealing to a broader consumer base and driving market growth.

Restraining Factors

Regulatory Challenges and Compliance Issues

Regulatory challenges and compliance issues present significant hurdles for the healthy energy drink market. Stringent regulations surrounding labeling, ingredients, and health claims can impede product development and market entry. Market analysis indicates that compliance costs can represent a substantial portion of a company's budget, particularly for smaller players.

Moreover, varying regulations across different regions add complexity to market expansion efforts. However, these challenges also foster innovation and differentiation within the market. Companies invest in research and development to formulate products that meet regulatory standards while still delivering on consumer expectations for health and functionality. By navigating regulatory landscapes effectively, firms can establish themselves as trusted brands, gaining a competitive edge and driving market growth.

Intense Competition from Traditional Energy Drinks

The healthy energy drink market faces intense competition from traditional energy drinks, which dominate the beverage landscape. Traditional energy drinks boast widespread brand recognition, extensive distribution networks, and an established market presence. Market research suggests that traditional energy drinks command over 80% of the energy drink market share. However, this competition also presents opportunities for differentiation and market positioning.

Healthy energy drink brands emphasize their unique selling points, such as natural ingredients, reduced sugar content, or functional benefits, to carve out a distinct niche within the market. Strategic marketing campaigns highlight these differences, appealing to health-conscious consumers seeking alternatives to conventional offerings. As consumer preferences continue to shift towards healthier options, healthy energy drink brands have the opportunity to capitalize on this trend, driving market growth despite the competitive landscape.

By Type Analysis

Traditional health products account for 41.1% of the market, showcasing enduring consumer preference.

In 2023, Traditional Health held a dominant market position in the By Type segment of the Healthy Energy Drink Market, capturing more than a 41.1% share. The Traditional Health segment encompasses energy drinks formulated with ingredients sourced from traditional medicinal practices, often incorporating herbs, roots, and natural extracts renowned for their health-promoting properties. This segment's robust performance can be attributed to growing consumer preference for beverages that offer not only a boost of energy but also potential health benefits derived from natural sources.

Moreover, the Traditional Health segment's success can be further elucidated by the rising demand for holistic wellness products, fueled by increasing health consciousness among consumers. The perceived efficacy of traditional ingredients in enhancing vitality and overall well-being has propelled the adoption of energy drinks within this category.

Furthermore, the market's receptiveness to Traditional Health energy drinks can be evidenced by the strategic product innovations and marketing initiatives deployed by key industry players. These efforts have effectively communicated the unique value proposition of Traditional Health energy drinks, resonating with health-conscious consumers seeking alternatives to conventional energy beverages.

Looking ahead, the Traditional Health segment is poised for sustained growth, driven by continued investments in research and development to introduce novel formulations and capitalize on emerging consumer trends. Additionally, collaborations with wellness experts and endorsement by healthcare professionals are expected to bolster consumer confidence and further consolidate the segment's market position.

By Packaging Type Analysis

Metal can packaging holds a dominant share at 41.2%, signifying robust market demand.

In 2023, Metal Can held a dominant market position in the By Packaging Type segment of the Healthy Energy Drink Market, capturing more than a 41.2% share. Metal Can packaging has emerged as the preferred choice for energy drink manufacturers due to its numerous advantages, including durability, portability, and preservation of product freshness. The widespread adoption of Metal Can packaging can be attributed to its ability to provide superior protection against external factors such as light, air, and moisture, thereby extending the shelf life of energy drinks and maintaining their quality over time.

Furthermore, the dominance of Metal Can packaging is reinforced by its widespread availability and cost-effectiveness, making it an attractive option for both manufacturers and consumers alike. The convenience of Metal Can packaging, characterized by its lightweight and easy-to-handle design, aligns with modern consumer lifestyles characterized by on-the-go consumption habits.

Moreover, the aesthetic appeal of Metal Can packaging, coupled with advancements in printing and labeling technologies, enables energy drink brands to differentiate themselves on store shelves and effectively communicate their brand identity to consumers. This has contributed to Metal Can's market leadership position, as consumers are drawn to visually appealing packaging that conveys a sense of quality and reliability.

Looking ahead, Metal Can packaging is poised to maintain its dominant position in the Healthy Energy Drink Market's Packaging Type segment, driven by ongoing innovations aimed at enhancing convenience, sustainability, and brand visibility. Additionally, strategic collaborations with retailers and logistics partners will further strengthen the distribution network for Metal Can-packaged energy drinks, ensuring continued market penetration and growth.

By Format Analysis

Ready-to-drink format leads with 45.3%, reflecting convenience-driven consumer behavior.

In 2023, Ready-To-Drink (RTD) held a dominant market position in the By Format segment of the Healthy Energy Drink Market, capturing more than a 45.3% share. RTD format energy drinks have surged in popularity, primarily due to their convenience and immediate consumption appeal. This format offers consumers a hassle-free solution for obtaining an energy boost on the go, aligning with modern lifestyles characterized by fast-paced routines and time constraints.

The dominance of RTD format energy drinks can be attributed to their ready availability across various retail channels, including convenience stores, supermarkets, and online platforms. Manufacturers have capitalized on this accessibility by strategically positioning RTD energy drinks as impulse purchases, leveraging eye-catching packaging and prominent shelf placement to capture consumer attention at point-of-sale.

Furthermore, the versatility of RTD format energy drinks, which are available in a wide range of flavors and formulations, caters to diverse consumer preferences and dietary requirements. This customization enables brands to target specific demographic segments and capitalize on emerging trends, such as plant-based ingredients and natural sweeteners, thereby enhancing their competitive edge in the market.

Looking ahead, the dominance of RTD format energy drinks is poised to persist, driven by continuous product innovation and investments in marketing and distribution infrastructure. Manufacturers are expected to focus on enhancing the nutritional profile of RTD energy drinks, incorporating functional ingredients and fortifications to appeal to health-conscious consumers seeking holistic wellness solutions.

By End User Analysis

Adults constitute a significant end-user segment, commanding a notable share of 63.3%.

In 2023, Adults held a dominant market position in the By End User segment of the Healthy Energy Drink Market, capturing more than a 63.3% share. This segment's prominence reflects the substantial demand among adult consumers for energy-boosting beverages tailored to their specific needs and preferences. Adults represent a diverse demographic encompassing individuals across various age groups and lifestyles, including working professionals, athletes, and health-conscious individuals seeking vitality and performance enhancement.

The dominance of the Adult segment can be attributed to several key factors, including the growing awareness of the importance of maintaining energy levels and mental alertness amidst demanding work schedules and active lifestyles. Energy drinks formulated for adults often feature targeted ingredients such as caffeine, vitamins, and amino acids, designed to support cognitive function, physical endurance, and overall well-being.

Moreover, the widespread availability and accessibility of adult-oriented energy drinks across retail channels, coupled with extensive marketing efforts aimed at positioning these products as lifestyle essentials, have contributed to the segment's market leadership position. Manufacturers have leveraged endorsements from fitness experts, nutritionists, and celebrities to endorse their products, thereby instilling trust and credibility among adult consumers.

Looking ahead, the dominance of the Adults segment is poised to persist, driven by ongoing product innovation and segmentation strategies aimed at addressing the diverse needs and preferences within this demographic. Manufacturers are expected to continue exploring new formulations and flavors tailored to specific adult consumer segments, such as professionals seeking mental focus and athletes pursuing peak performance.

By Distribution Channel Analysis

Convenience stores emerge as a key distribution channel, capturing a substantial market portion at 38.4%.

In 2023, Convenience Stores held a dominant market position in the By Distribution Channel segment of the Healthy Energy Drink Market, capturing more than a 38.4% share. Convenience stores have emerged as pivotal distribution channels for energy drinks, offering consumers convenient access to a wide range of products in high-traffic locations. The prominence of convenience stores can be attributed to their strategic placement in urban and suburban areas, catering to consumers' need for quick and accessible solutions to their energy requirements.

The dominance of Convenience Stores in the Healthy Energy Drink Market's Distribution Channel segment is further underscored by their ability to capitalize on impulse purchases and capitalize on consumer demand for on-the-go refreshment options. Energy drink manufacturers have forged partnerships with convenience store chains to ensure prominent shelf placement and maximize visibility, thereby driving sales and market penetration.

Moreover, convenience stores offer a diverse selection of energy drink brands and variants, catering to different consumer preferences and taste profiles. This extensive product assortment, coupled with promotional activities such as discounts, bundling deals, and point-of-sale displays, enhances the appeal of convenience stores as preferred destinations for purchasing energy drinks.

Looking ahead, the dominance of Convenience Stores in the Healthy Energy Drink Market's Distribution Channel segment is poised to persist, fueled by ongoing urbanization trends, changing consumer lifestyles, and convenience-driven shopping behavior. Manufacturers are expected to continue leveraging convenience stores as key distribution partners, investing in collaborative marketing initiatives and innovative merchandising strategies to maintain their competitive edge and capitalize on evolving consumer preferences.

Key Market Segments

By Type

- Traditional Health

- Natural/Organic

- Functional

- Sports Performance

- Low-Calorie

- Others

By Packaging Type

- Glass Bottles

- Metal Can

- PET Bottles

By Format

- Shots

- Powder

- Ready-To-Drink (RTD)

By End User

- Kids

- Adults

- Teenagers

By Distribution Channel

- Convenience Stores

- Online Retail

- Supermarket/Hypermarket

- Others

Growth Opportunity

Expansion into Emerging Markets Drives Growth

The global healthy energy drink market witnessed promising growth opportunities in 2023, primarily fueled by strategic expansions into emerging markets characterized by a burgeoning health-conscious demographic. This shift reflects a paradigmatic evolution in consumer preferences, with discerning individuals seeking healthier alternatives to traditional energy beverages.

Market players capitalized on this trend by penetrating untapped territories, leveraging the rising awareness of health benefits associated with their products. Such strategic maneuvers not only expanded market reach but also diversified revenue streams, mitigating risks associated with saturation in established markets.

Innovation in Formulations and Packaging

Innovation emerged as a cornerstone for market growth in 2023, with significant investments directed towards enhancing product formulations and packaging. Market leaders prioritized research and development initiatives aimed at concocting novel blends enriched with natural ingredients, catering to evolving consumer demands for healthier options devoid of artificial additives.

Additionally, packaging innovations played a pivotal role in captivating consumer interest, with emphasis placed on sustainability, convenience, and aesthetics. Sleek, eco-friendly designs not only resonated with environmentally-conscious consumers but also conveyed a premium image, fostering brand loyalty and consumer trust.

Latest Trends

Clean Label and Transparent Sourcing: A Dominant Trend

The global healthy energy drink market in 2023 witnessed a significant shift towards clean label and transparent ingredient sourcing, representing a dominant trend reshaping consumer preferences and industry standards. Increasingly health-conscious consumers, discerning about what they consume, demanded products with easily recognizable, natural ingredients and clear sourcing practices.

Market players responded by reformulating their offerings, eliminating artificial additives, preservatives, and sweeteners, and emphasizing the use of organic, non-GMO ingredients. This transition towards cleaner labels not only appealed to health-conscious consumers but also bolstered brand trust and loyalty, positioning companies as transparent and ethical stewards of consumer well-being.

Rising Popularity of Plant-based and Adaptogenic Ingredients

Another noteworthy trend shaping the global healthy energy drink market in 2023 was the rising popularity of plant-based and adaptogenic ingredients. As consumers increasingly sought holistic wellness solutions, they gravitated towards beverages fortified with botanical extracts known for their health-promoting properties.

Market leaders capitalized on this trend by incorporating ingredients such as ginseng, ashwagandha, and turmeric, renowned for their adaptogenic properties, which help the body adapt to stress and promote overall well-being. Moreover, the surge in demand for plant-based lifestyles propelled the adoption of ingredients like coconut water, green tea, and fruit juices, further enhancing the nutritional profile of energy drinks while catering to diverse dietary preferences.

Regional Analysis

The healthy energy drink market in North America has grown by 36.5% according to recent market analysis.

The Healthy Energy Drink market exhibits a robust growth trajectory across diverse regions, including North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. North America emerges as a dominant force in this market landscape, with a remarkable growth rate of 36.5% over the past fiscal year, indicative of the region's strong consumer demand and favorable regulatory environment. In North America, the rising health consciousness among consumers, coupled with a growing preference for natural and functional beverages, has propelled the demand for healthy energy drinks.

In Europe, a similar trend is observed, with consumers increasingly seeking healthier alternatives to traditional energy drinks, thereby driving significant market growth. The region benefits from a well-established market infrastructure and a growing number of health-conscious consumers, contributing to the expansion of the healthy energy drink segment.

The Asia Pacific region presents substantial growth opportunities for the healthy energy drink market, fueled by increasing urbanization, rising disposable incomes, and changing lifestyle patterns among consumers. With a large and diverse consumer base, coupled with a growing awareness regarding health and wellness, Asia Pacific emerges as a key market for healthy energy drinks, experiencing significant growth in recent years.

In the Middle East & Africa and Latin America regions, the healthy energy drink market is also witnessing steady growth, propelled by factors such as changing consumer preferences, urbanization, and increasing health awareness. While these regions may have unique market dynamics and challenges, they represent emerging markets with untapped potential for healthy energy drink manufacturers.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In the thriving landscape of the global Healthy Energy Drink Market in 2023, several key players have emerged as frontrunners, each contributing uniquely to the industry's growth and dynamics. Among these prominent entities are Aspire Drinks, RITA Food & Drink Co., Ltd., Jouleshealth Enterprise Pvt Ltd., RVIITA, Jeunesse, Unicity, Le-vel, Amway, Vemma Retail, Better Body Company, and ZOA Energy.

These companies exhibit diverse strategies and product offerings, catering to the evolving preferences of health-conscious consumers worldwide. Aspire Drinks, for instance, is recognized for its commitment to natural ingredients and innovative formulations, positioning itself as a pioneer in the healthy energy segment. Similarly, RITA Food & Drink Co., Ltd., and Jouleshealth Enterprise Pvt Ltd., leverage their expertise in beverage manufacturing to introduce nutritious alternatives to traditional energy drinks.

Moreover, brands like RVIITA and ZOA Energy capitalize on the rising demand for functional beverages by incorporating botanical extracts and vitamins into their product lines, appealing to consumers seeking holistic wellness solutions. Jeunesse and Unicity, with their established presence in the wellness industry, offer credibility and reliability, further bolstering the market's expansion.

As the global population increasingly prioritizes health and wellness, companies like Le-vel, Amway, Vemma Retail, and Better Body Company seize the opportunity to promote healthy lifestyles through their diverse product portfolios and robust distribution networks.

In essence, the presence of these key players underscores the dynamism and potential of the Healthy Energy Drink Market in 2023. Their innovative approaches, coupled with a commitment to quality and consumer well-being, position them as pivotal influencers shaping the trajectory of the industry.

Market Key Players

- Aspire Drinks

- RITA Food & Drink Co.,Ltd

- Jouleshealth Enterprise Pvt Ltd.

- RVIITA

- Jeunesse

- Unicity

- Le-vel

- Amway

- Vemma Retail

- Better Body Company

- ZOA Energy

Recent Development

- In May 2023, Ingredient suppliers like Florida Food Products and Van Drunen Farms/FutureCeuticals are innovating with natural caffeine sources from coffee and tea, offering benefits like reduced acidity and additional health perks.

- In August 2018, Leading energy drink brands are innovating with cleaner, organic ingredients like matcha and cascara to address health concerns and boost sales. Red Bull's 'Organics' range and MatchaBar's carbonated matcha drink reflect this trend.

Report Scope

Report Features Description Market Value (2023) USD 793 Million Forecast Revenue (2033) USD 2012 Billion CAGR (2024-2032) 11.40 Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type(Traditional Health, Natural/Organic, Functional, Sports Performance, Low-Calorie, Others), By Packaging Type(Glass Bottles, Metal Can, PET Bottles), By Format(Shots, Powder, Ready-To-Drink (RTD)), By End User(Kids, Adults, Teenagers), By Distribution Channel(Convenience Stores, Online Retail, Supermarket/Hypermarket, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Aspire Drinks, RITA Food & Drink Co.,Ltd, Jouleshealth Enterprise Pvt Ltd., RVIITA, Jeunesse, Unicity, Le-vel, Amway, Vemma Retail, Better Body Company, ZOA Energy Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Aspire Drinks

- RITA Food & Drink Co.,Ltd

- Jouleshealth Enterprise Pvt Ltd.

- RVIITA

- Jeunesse

- Unicity

- Le-vel

- Amway

- Vemma Retail

- Better Body Company

- ZOA Energy

Our Clients

View Our Licence Options