Generative AI in Computer Vision Market By Technology(Deep Learning, Generative Adversarial Networks (GANs), Other Technologies), By Application(Content Creation and Enhancement, Image and Video Synthesis, Other Applications), By Industry Vertical(Healthcare, Automotive, Retail, Other Industry Verticals), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

43158

-

Jan 2024

-

179

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

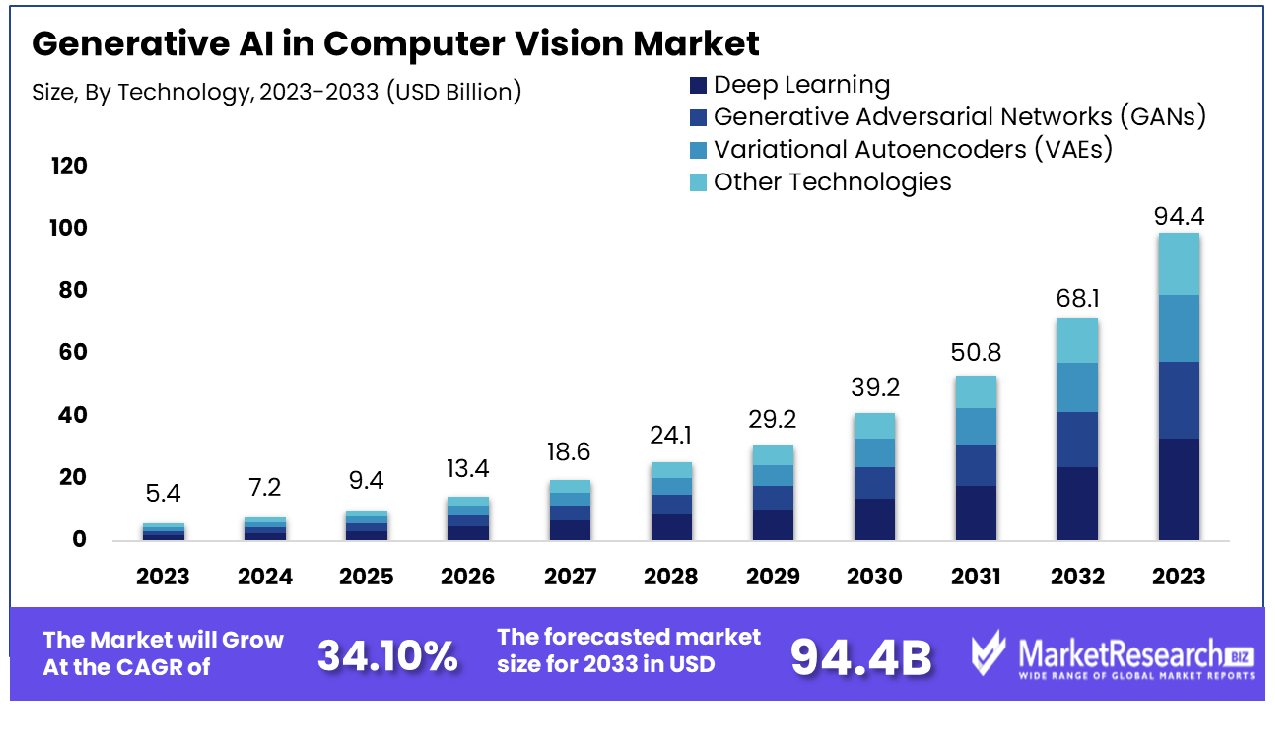

The generative AI in computer vision market was valued at USD 5.4 billion in 2023. It is expected to reach USD 94.4 billion by 2033, with a CAGR of 34.10% during the forecast period from 2024 to 2033.

The surge in demand in various verticals of industries and advanced technologies are some of the main key driving factors for generative AI in the computer vision market. Computer vision is an important innovation that is transforming how to engage and know the world around us. Computer vision technology has the potential of using gen AI and image processing that helps the machines to interpret and detail the visual information to the human sights. These can examine and make sense of images and videos, perceiving objects and patterns with exceptional precision.

Computer vision signifies an important tool for image processing that transact with the science of machines and computers that are enabled visually. It also helps in automating the task flow that needs the human visual system and enhances its precision. Moreover, computer vision systems can be up to 99% precise in several tasks. These are even more precise than human vision. The integration with gen AI is the engagement between computer science and engineering. This integration helps firms and industries automate their processes and decreases the requirement to use human interference to develop processes more efficiently.

For example, in the medical field particularly in the case of skin cancer gen AI and computer vision play a crucial role. The advanced technology that is implemented in artificial intelligence is the form of convolutional neural networks that help medical experts and patients identify skin cancer as soon as possible in its initial stages for proactive treatment. According to a report published by Scientific Reports in March 2022, skin cancer is one of the most common cancers seen in the US with 5 million patients every year.

Melanoma is the deadliest form that took over 9000 lives per year worldwide. It has a 5-year survival rate of 95% for cancer patients at the advanced stages and a mortality of 1.62% for those with early stages of melanoma. The technology used in identifying skin cancer matches the dermatologist's performance in melanoma and carcinoma categorization. It’s just the level of performance compares to that of well-known dermatologists when it comes to categorization through deep learning algorithms.

There are several advantages of using generative AI in computer vision such as it helps in surging the diversity of training data, producing synthetic images, and generating more realistic data samples. The demand for gen AI will increase due to its requirement in different industrial fields to enhance their efficacy and automate the tasks that will help in market expansion in the coming year.

Driving Factors

Automated Visual Inspection Propels Generative AI in Computer Vision

The escalating demand for automated visual inspection and quality control in manufacturing catalyzes the growth of Generative AI in Computer Vision. Traditional manual inspection, with an error rate of 20-30%, pales in comparison to the near 100% defect detection rates achieved through AI-enhanced automated systems.

Crucially, Generative AI's ability to produce synthetic visual data for training computer vision models obviates the need for extensive labeled datasets, streamlining the process and ensuring more efficient and accurate defect detection. This shift towards automation is not just a trend but a fundamental change in manufacturing quality control, likely to expand further as technology evolves.

Advancements in GANs and Diffusion Models Expand Market Applications

Technological leaps in Generative Adversarial Networks (GANs) and diffusion models, exemplified by innovations like StyleGAN and DALL-E, significantly enhance the Generative AI in the Computer Vision market. These advancements, expected to improve image-based machine learning accuracy by 30-40%, have broadened the scope of generative AI applications.

This progress in GANs and diffusion models represents a cornerstone in the evolution of computer vision, enabling more precise and varied applications, thus propelling market growth.

Enhanced Model Accuracy Augments Market Reach

Improvements in generative AI techniques are leading to more realistic and accurate image generation, crucial for tasks like object detection. This enhancement in model accuracy broadens the potential market, making generative AI an indispensable tool in various sectors that rely on precise computer vision.

The ongoing refinement of these models promises to further expand the market size, indicating a future where generative AI's role in computer vision is not just supplementary but central to numerous industries.

Restraining Factors

Data Privacy Concerns Impede Generative AI in Computer Vision Market Growth

Generative models, including those used for computer vision applications, run the risk of unintentionally exposing private data utilized during training. This issue is particularly pertinent in scenarios dealing with sensitive visual data, such as medical imaging.

A notable case is Samsung's ban on the use of AI-powered chatbots like ChatGPT by its employees, following an incident where sensitive internal source code was inadvertently leaked via such a platform. This incident underscores the potential risks of data compromise, making companies cautious in adopting these technologies, especially when handling confidential or sensitive visual data.

Model Training Costs Restrict Generative AI in Computer Vision Market Expansion

Techniques such as Generative Adversarial Networks (GANs) and Variational Autoencoders (VAEs) demand considerable computational resources and extensive dataset labeling for effective training. These requirements entail significant financial investment, making it particularly challenging for smaller firms with limited budgets to engage in developing or utilizing these advanced models.

The high cost of model training not only limits access for smaller players but also restricts the scope and speed of innovation in the field, as the financial barrier excludes a significant portion of potential market participants.

By Technology Analysis

Deep Learning stands as the dominant technology in the Generative AI in the Computer Vision market, accounting for a 38% market share. This preeminence is attributed to deep learning's ability to process and analyze vast datasets, enabling more accurate and detailed image recognition and classification. Deep learning algorithms, particularly convolutional neural networks (CNNs), have revolutionized computer vision by providing unparalleled accuracy in tasks such as object detection, image classification, and segmentation.

Generative Adversarial Networks (GANs) and Variational Autoencoders (VAEs) are other significant technologies in this segment. GANs, known for their ability to generate highly realistic images, are pivotal in applications like data augmentation and synthetic image generation. VAEs play a crucial role in image generation and reconstruction tasks. Despite the growing importance of these technologies, the comprehensive capabilities and widespread adoption of deep learning models solidify its dominance in the market.

By Application Analysis

Content Creation and Enhancement is the leading application segment in Generative AI in Computer Vision, holding a 25% market share. This segment's growth is driven by the increasing demand for high-quality visual content across various media platforms. Generative AI significantly enhances content creation workflows by automating and refining the process of image and video generation, making it faster and more efficient.

Image and Video Synthesis, Image-to-Image Translation, and Style Transfer are other crucial applications. Image-to-Image Translation and Style Transfer are particularly notable for their ability to modify and enhance images in creative ways, finding applications in advertising, film, and gaming industries. However, the broad applicability and demand for content creation and enhancement, from social media to professional media production, highlight this segment's market leadership.

By Industry Vertical Analysis

Healthcare emerges as the dominant industry vertical in the Generative AI in Computer Vision market, with a 19% market share. In healthcare, generative AI is transforming diagnostic imaging, enabling more precise and faster analysis of medical images such as X-rays, MRIs, and CT scans. It also plays a significant role in medical research, where it helps in creating detailed anatomical models and simulations.

Automotive, Retail, Entertainment and Media, Manufacturing, and other industry verticals also extensively use generative AI in computer vision. In the automotive industry trend, it aids in developing advanced driver-assistance systems (ADAS) and autonomous vehicles. In retail, generative AI enhances customer experiences through virtual try-on solutions and personalized marketing. Yet, the transformational power of ingenuity-based AI in improving diagnosis and care for patients and the rapid growth of AI in healthcare, confirms its leading position on the market.

Generative AI in Computer Vision Industry Segments

By Technology

- Deep Learning

- Generative Adversarial Networks (GANs)

- Variational Autoencoders (VAEs)

- Other Technologies

By Application

- Content Creation and Enhancement

- Image and Video Synthesis

- Image-to-Image Translation

- Style Transfer

- Other Applications

By Industry Vertical

- Healthcare

- Automotive

- Retail

- Entertainment and Media

- Manufacturing

- Other Industry Verticals

Growth Opportunity

Automated Visual Inspection: Generative AI Revolutionizes Manufacturing Quality Control

The integration of Generative AI in automated visual inspection presents substantial growth opportunities within the computer vision market. This technology addresses the challenge of manual curation of defect datasets, a significant pain point in manufacturing. By generating synthetic defect data for training, Generative AI enhances the efficiency and accuracy of product inspections, ensuring higher quality standards.

This innovation not only streamlines the inspection process but also reduces costs and time associated with manual inspections. As manufacturers increasingly recognize the benefits of this technology, its adoption is poised to expand, driving significant growth in the Generative AI and computer vision market.

Autonomous Navigation: Generative AI Enhances Safety and Efficiency

In the realm of autonomous navigation, particularly for self-driving

vehicles, Generative AI is emerging as a game-changer. The technology's ability to simulate rare but critical events, such as encounters with emergency vehicles, is invaluable for ensuring comprehensive edge case testing. This reduces the reliance on real-world driving data, which can be limited in capturing such uncommon scenarios.A prime example is Wayve's GAIA-1, a generative AI world model, which underscores the technology's potential to enhance the safety and reliability of autonomous vehicles. The adoption of Generative AI in autonomous navigation is set to grow, driven by its ability to significantly improve testing efficiency and vehicle safety, marking a substantial growth sector within the computer vision market.

Latest Trends

Enhanced Realism in Synthetic Data Generation

A significant trend in the Generative AI space within the computer vision market is the creation of highly realistic synthetic datasets. These advancements allow for the training of more accurate and robust computer vision models, especially in scenarios where real-world data is scarce, sensitive, or difficult to obtain, thus accelerating AI development while ensuring privacy compliance.

AI-driven Augmentation for Visual Data

Another emerging trend is the use of Generative AI for augmenting visual data, which includes improving image quality, generating new images from existing ones, and creating realistic animations from static images. This technology not only enhances the capabilities of computer vision systems in interpreting and interacting with the visual world but also opens up new possibilities in various applications such as virtual reality, augmented reality, and video enhancement.

Regional Analysis

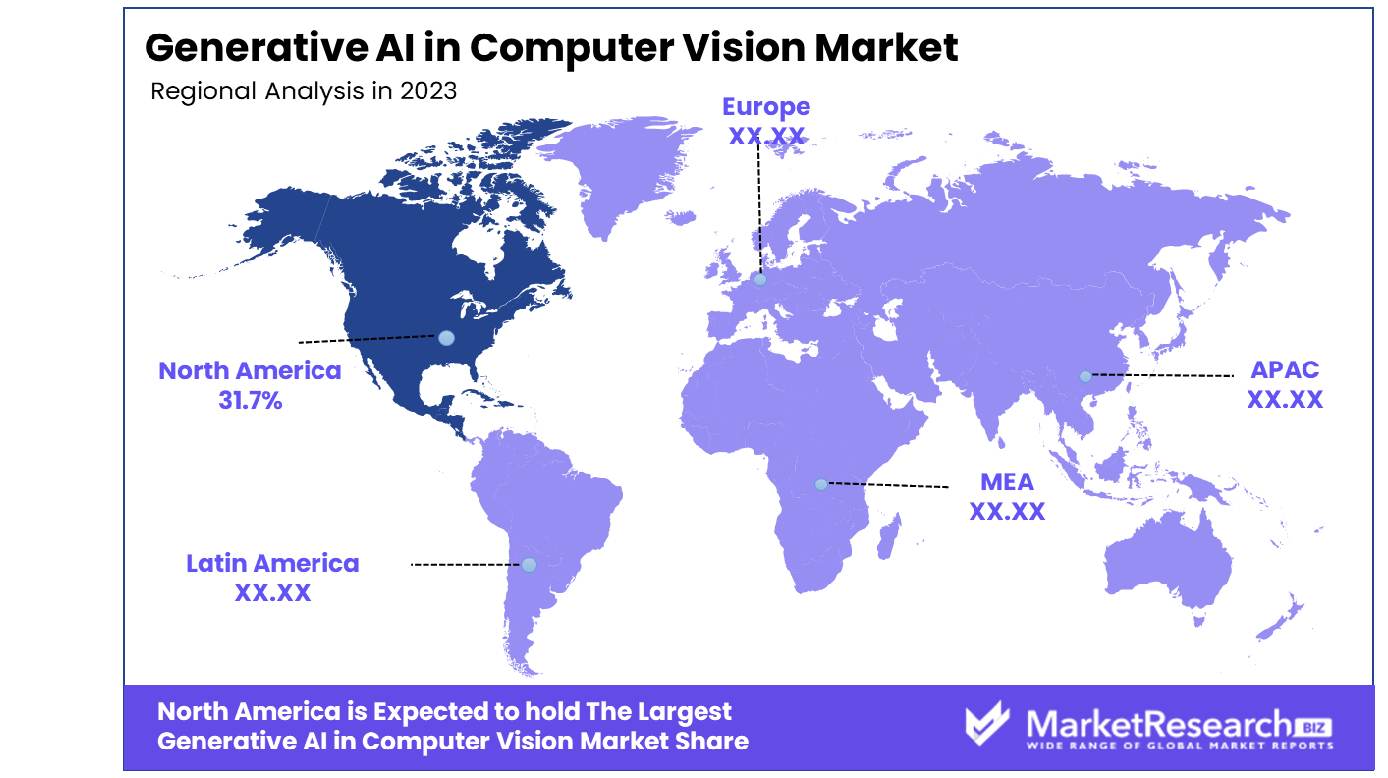

North America Pioneers with 31.7% Stake in Generative AI in Computer Vision Market

North America's commanding 31.7% share in the Generative AI in Computer Vision market is primarily propelled by its robust technological infrastructure and significant investments in AI research. The region, spearheaded by the United States, is home to leading tech giants and innovative startups specializing in AI and computer vision. This market dominance is further augmented reality by a strong ecosystem of universities and research institutions contributing to cutting-edge advancements in AI. Additionally, the region's policy environment and funding initiatives offer fertile ground for AI development, fostering a climate of innovation and experimentation.

The market dynamics in North America are characterized by rapid adoption of AI technologies across various sectors including healthcare, automotive, and retail. The integration of generative AI in computer vision is revolutionizing these industries by enhancing capabilities in image recognition, data analysis, and automated decision-making. The market is also buoyed by an increasing demand for advanced surveillance and security systems, leveraging AI for more efficient and accurate monitoring. Collaborations between tech companies and industrial sectors are catalyzing the practical application of these technologies, further fueling market growth.

Europe: A Hub of Innovation and Regulation

Europe's market share in Generative AI in Computer Vision is driven by a strong focus on innovation coupled with stringent data privacy regulations. The region's emphasis on ethical AI development and GDPR compliance presents a unique market dynamic where safety and innovation intersect.

Asia-Pacific: Rapid Growth and Expanding Applications

In Asia-Pacific, the market is seeing rapid growth due to the increase in technology adoption and investments in AI as well as computer vision. Countries such as China along with Japan are among the top in implementing AI in surveillance and manufacturing which indicates the growing potential and applications in international markets.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In the rapidly evolving Generative AI in Computer Vision Market, the listed companies are at the vanguard, each carving out distinct strategic niches and exerting varying degrees of market influence. NVIDIA Corporation is a pivotal player, leveraging its robust GPU technology to power AI-driven computer vision solutions. Its strategic positioning at the intersection of hardware and AI software development gives it a unique competitive edge.

Intel Corporation and Qualcomm Technologies, Inc. similarly capitalize on their hardware prowess, offering advanced chipsets that facilitate complex AI computations essential for generative computer vision tasks. Their role underscores the critical synergy between hardware capabilities and AI functionalities.

Microsoft Corporation, IBM Corporation, and Amazon Web Services (AWS) distinguish themselves with expansive cloud platforms and AI services. These platforms enable scalable and sophisticated computer vision applications, reflecting the market's trend towards cloud-based AI solutions.

Market Key Players

- NVIDIA Corporation

- Intel Corporation

- Microsoft Corporation

- IBM Corporation

- Google LLC

- Facebook, Inc.

- OpenAI

- Samsung Electronics Co., Ltd.

- Qualcomm Technologies, Inc.

- Amazon Web Services (AWS)

- Other Key Players

Recent Development

- In January 2024, The evolution of generative AI sees Microsoft unveiling promising Small Language Models (SLMs) like PHI-2. SLMs, trained on high-quality datasets, offer efficiency on less powerful hardware, enhancing generative capabilities.

- In January 2024, RagaAI, founded by Gaurav Agarwal in 2021, raised $4.7 million in seed funding for its comprehensive AI testing platform. The platform enables developers to road-test and identify errors in AI models.

- In January 2024, Arcee, a GenAI platform developed by former Hugging Face engineers, secured $5.5 million in funding to offer end-to-end training, deploying, and monitoring of AI models within secure virtual private clouds for highly regulated industries.

- In December 2023, Ambarella, Inc. showcases multi-modal large language models (LLMs) on its N1 SoC series at CES, aiming to bring power-efficient generative AI to edge devices. The solution offers 3x power efficiency compared to GPUs.

- In November 2023, Cambridge University established the Institute for Technology and Humanity, aiming to ensure AI advancements benefit humanity. The interdisciplinary institute brings together experts in AI, ethics, and philosophy to address technological risks.

Report Scope

Report Features Description Market Value (2023) USD 5.4 Billion Forecast Revenue (2033) USD 94.4 Billion CAGR (2024-2032) 34.10% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology(Deep Learning, Generative Adversarial Networks (GANs), Variational Autoencoders (VAEs), Other Technologies), By Application(Content Creation and Enhancement, Image and Video Synthesis, Image-to-Image Translation Style Transfer, Other Applications), By Industry Vertical(Healthcare, Automotive, Retail, Entertainment and Media, Manufacturing, Other Industry Verticals) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape NVIDIA Corporation, Intel Corporation, Microsoft Corporation, IBM Corporation, Google LLC, Facebook, Inc., OpenAI, Samsung Electronics Co., Ltd., Qualcomm Technologies, Inc., Amazon Web Services (AWS), Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- NVIDIA Corporation

- Intel Corporation

- Microsoft Corporation

- IBM Corporation

- Google LLC

- Facebook, Inc.

- OpenAI

- Samsung Electronics Co., Ltd.

- Qualcomm Technologies, Inc.

- Amazon Web Services (AWS)

- Other Key Players

Our Clients

View Our Licence Options