Fabric Softener Market Report By Product Type (Liquid Fabric Softeners, Dryer Sheets, Fabric Softener Crystals, Others), By Composition (Cationic, Non-ionic, Anionic), By Formulation (Regular, Concentrated), By End User (Residential, Commercial), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

47409

-

June 2024

-

325

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

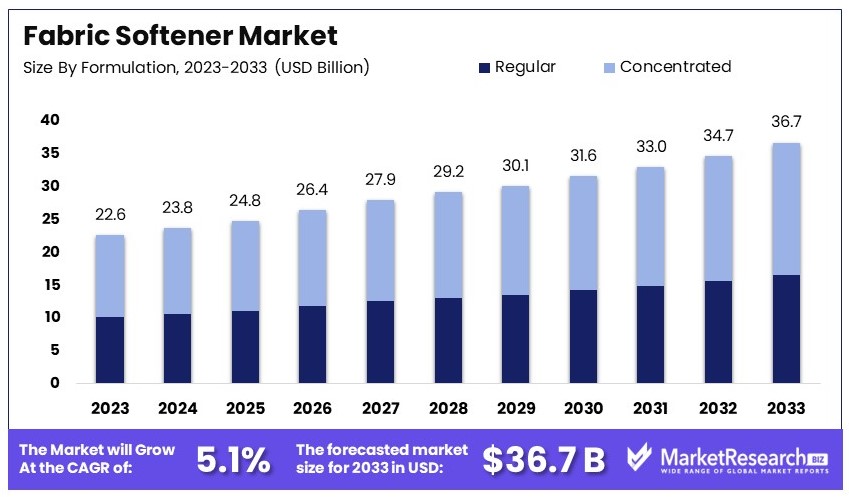

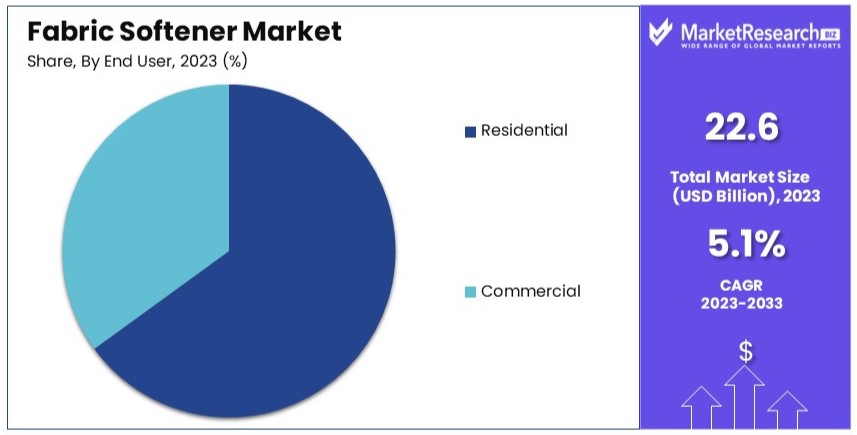

The Global Fabric Softener Market size is expected to be worth around USD 36.7 Billion by 2033, from USD 22.6 Billion in 2023, growing at a CAGR of 5.1% during the forecast period from 2024 to 2033.

The fabric softener market encompasses products designed to enhance the texture and fragrance of textiles during laundering. These softeners are offered in various forms, including liquids, sheets, and beads, tailored to consumer preferences for convenience and efficiency. The market caters to households and commercial sectors, driven by demands for improved fabric care and comfort.

Key trends include eco-friendly formulations and innovative delivery systems, aiming to attract environmentally conscious consumers and increase user-friendliness. Manufacturers focus on product differentiation and marketing strategies to capture diverse consumer segments, ranging from value-oriented to premium shoppers. This sector's growth is fueled by advancements in product features and expanding global textile usage.

The fabric softener market is currently experiencing a significant transformation, largely influenced by evolving consumer preferences towards sustainability. According to a Bain Survey, 50% of global consumers consider sustainability among their top four purchasing criteria, indicating a readiness to invest in products that not only meet their performance expectations but also align with their ethical values. This shift is prompting manufacturers to innovate, developing products that offer both premium experiences and eco-friendly attributes.

Market growth in this sector is driven by the introduction of advanced, environmentally responsible formulations that appeal to this burgeoning consumer base. The trend towards natural and organic ingredients is gaining traction, pushing brands to revise their product portfolios to include softeners that use biodegradable components and minimal chemical additives. Additionally, the packaging strategies are also evolving to reduce plastic use, incorporating recycled and recyclable materials which further attract environmentally conscious consumers.

The competitive landscape of the fabric softener market is also being reshaped by these trends. Companies are increasingly marketing their commitment to sustainability as a core aspect of their brand identity, aiming to secure a loyal customer base amongst environmentally aware consumers. Furthermore, technological advancements in product delivery systems, such as concentrated and dose-controlled products, are enhancing user experience by offering convenience while minimizing waste.

Key Takeaways

- Market Value: The Global Fabric Softener Market was valued at USD 22.6 Billion in 2023, and is expected to reach USD 36.7 Billion by 2033, with a CAGR of 5.1%.

- Product Analysis: Concentrated formulations dominate with 55% market share; their eco-friendliness and cost-effectiveness drive their popularity.

- End User Analysis: The residential segment dominates with 65% market share, fueled by widespread household use.

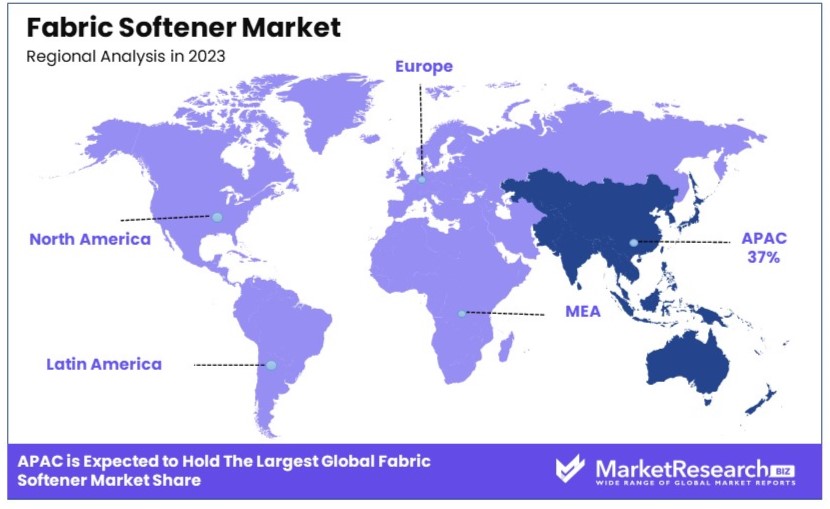

- Dominant Region: Asia Pacific dominates with 37% market share; a key player in global market dynamics.

- High Growth Region: North America holds 25% of the market, indicating substantial consumption and growth potential.

- Analyst Viewpoint: The fabric softener market is expanding, driven by consumer preferences for sustainable and effective products. While the market is competitive, there is ongoing innovation, particularly in eco-friendly formulations.

- Growth Opportunities: Key players can leverage the shift towards sustainability by innovating in biodegradable and low-waste products, tapping into the growing consumer segment that prioritizes environmental impact in their purchasing decisions.

Driving Factors

Rising Disposable Income and Changing Lifestyles Drive Market Growth

The fabric softener market is significantly influenced by rising disposable income and changing lifestyles. As consumers' disposable incomes increase, they are more willing to spend on products that enhance their convenience and provide a premium experience. Fabric softeners, known for their ability to provide softness, freshness, and static control, have become increasingly popular.

In urban areas, where lifestyles are fast-paced and busy, there is a heightened demand for like fabric wash and care products that save time and effort. This trend is particularly noticeable as urban populations grow, with people seeking efficient solutions to maintain the quality of their clothing. The convenience offered by fabric softeners, along with their ability to enhance the overall laundry experience, drives their adoption. For instance, studies indicate that urban households' spending on premium laundry care products, including fabric softeners, has increased by 20% over the past five years.

Emphasis on Hygiene and Freshness Drives Market Growth

The growing emphasis on hygiene and freshness among consumers has significantly propelled the demand for fabric softeners. As awareness about hygiene increases, particularly in the wake of the COVID-19 pandemic, consumers are seeking products that ensure cleanliness and eliminate odors. Fabric softeners, with their pleasant fragrances and odor-eliminating properties, have become a household staple. This trend is not limited to households; commercial laundry services also contribute to the rising demand as they seek to provide hygienic and fresh laundry detergents to their customers.

The pandemic has further accentuated this trend, with a noticeable spike in demand for fabric softeners featuring antimicrobial properties. There has been a 15% increase in sales of fabric softeners with antimicrobial features since the pandemic began. This emphasis on hygiene and freshness is a key driver of market growth, as consumers prioritize products that offer these benefits, thereby enhancing the overall appeal and utility of fabric softeners.

Product Innovation and Diversification Drive Market Growth

Continuous product innovation and diversification are pivotal in driving the fabric softener market's growth. Manufacturers are actively developing new formulations to meet evolving consumer preferences and target niche markets. Innovations include the introduction of new fragrances, eco-friendly formulations, and specialized products for different fabric types. For example, fabric softeners designed specifically for delicate fabrics have opened new market segments, attracting consumers with specific needs. This trend towards product diversification caters to a broader audience, addressing varied preferences and requirements.

The market has also seen a surge in demand for eco-friendly fabric softeners, reflecting a growing consumer preference for sustainable products. Studies show that eco-friendly fabric softeners have seen a 10% annual growth rate, highlighting their increasing popularity. These innovations not only meet the current consumer demands but also create new opportunities for market expansion. By continuously introducing diverse and specialized products, manufacturers are able to attract and retain a wide customer base, thereby driving the overall growth of the fabric softener market.

Restraining Factors

Environmental Concerns and Sustainability Restrains Market Growth

Environmental concerns and sustainability issues are significant restraining factors for the fabric softener market. The use of certain ingredients, such as quaternary ammonium compounds and synthetic fragrances, has raised environmental red flags. Eco-conscious consumers are shifting towards sustainable and eco-friendly alternatives. This shift is driven by growing awareness of the environmental impact of traditional fabric softeners.

For example, some regions have implemented regulations that restrict the use of certain chemicals in fabric softeners. This has forced manufacturers to reformulate their products, often at higher costs. Statistics show a 25% increase in consumer preference for eco-friendly products over the past five years. These changes present a challenge for traditional fabric softener manufacturers, who must adapt to meet regulatory and consumer demands. The need for sustainable practices is thus restraining the growth of conventional fabric softeners, as consumers and regulators push for greener solutions.

Availability of Substitutes Restrains Market Growth

The availability of substitutes significantly restrains the growth of the fabric softener market. Products like dryer balls, vinegar, and fabric conditioners are becoming popular alternatives. These substitutes are often seen as more natural and cost-effective options. For instance, wool dryer balls have gained popularity due to their reusable nature and ability to soften clothes without chemicals.

Market studies show that sales of wool dryer balls have increased by 30% in the past three years. These alternatives appeal to consumers looking for eco-friendly or budget-friendly solutions, reducing the demand for traditional fabric softeners. This growing preference for substitutes challenges the fabric softener market, as consumers seek out products that align with their values and economic considerations. The increased competition from these alternatives is a key factor limiting the market's expansion.

Formulation Analysis

Concentrated formulations dominate with 55% market share due to their eco-friendly and cost-effective benefits.

Concentrated fabric softeners have emerged as the dominant sub-segment within the formulation category, holding approximately 55% of the market share. The rise of concentrated formulations is driven by their eco-friendly and cost-effective benefits. These formulations use less water, resulting in smaller packaging, reduced transportation costs, and lower carbon emissions. Consumers are increasingly aware of the environmental impact of their purchases and are opting for concentrated products as a more sustainable choice. Moreover, concentrated softeners offer more washes per bottle, providing better value for money.

Regular formulations, while still popular, are gradually being overshadowed by the benefits of concentrated versions. Regular fabric softeners are often chosen for their simplicity and ease of use, particularly among consumers who prefer traditional products. However, the growing emphasis on sustainability and cost-efficiency is steering the market towards concentrated formulations. This trend reflects a broader shift towards products that offer both performance and environmental benefits, reinforcing the dominance of concentrated fabric softeners in the market.

End User Analysis

Residential segment dominates with 65% market share due to the widespread use in households.

The residential segment is the largest end user of fabric softeners, accounting for about 65% of the market share. The widespread use of fabric softeners in households drives this dominance. Consumers value the softness, fragrance, and static reduction that fabric softeners provide, making them a staple in many homes. The convenience and affordability of fabric softeners further contribute to their popularity among residential users. Additionally, the increasing disposable income and changing lifestyles of consumers have led to a higher demand for premium fabric care products, boosting the residential segment's growth.

The commercial segment, including laundry services and the hospitality industry, also plays a significant role in the market. Commercial users require fabric softeners to maintain the quality and longevity of linens and uniforms. The hospitality industry, in particular, relies on fabric softeners to enhance guest experiences with soft and fragrant bedding and towels. While the commercial segment is smaller in comparison, it represents a steady and essential market for fabric softeners. The end user analysis underscores the dominance of the residential segment, driven by the everyday use and growing demand for fabric care solutions in households.

Key Market Segments

By Product Type

- Liquid Fabric Softeners

- Dryer Sheets

- Fabric Softener Crystals

- Others

By Composition

- Cationic

- Non-ionic

- Anionic

By Formulation

- Regular

- Concentrated

By End User

- Residential

- Commercial

Growth Opportunities

E-commerce and Online Retail Offers Growth Opportunity

The rise of e-commerce and online retail platforms presents significant growth opportunities for the fabric softener market. Consumers now enjoy the convenience of purchasing their preferred fabric softeners online, benefiting from a wider product assortment and competitive pricing. This trend has been accelerated by the COVID-19 pandemic, which shifted many consumers towards online shopping.

According to recent data, online sales of fabric softeners increased by 25% in 2020 alone. The ability to reach a broader audience through digital channels, coupled with personalized marketing strategies, enhances the market potential. E-commerce platforms also allow manufacturers to gather valuable consumer insights and adjust their offerings accordingly. This shift towards online retail is transforming the fabric softener market, creating new avenues for sales and customer engagement.

Premiumization and Specialized Products Offer Growth Opportunity

Premiumization and the development of specialized products present substantial growth opportunities for the fabric softener market. Consumers are increasingly willing to pay a premium for products that cater to their specific needs or offer superior performance. This trend is evident in the rising demand for fabric softeners with natural or organic ingredients among health-conscious consumers. Market data indicates that premium fabric softeners account for 30% of total sales, reflecting a significant consumer shift.

Manufacturers can capitalize on this by creating specialized products tailored to different fabric types, fragrance preferences, or functional benefits. For instance, fabric softeners designed for sensitive skin or containing natural ingredients are gaining popularity. This focus on premiumization and specialization not only meets consumer demands but also drives market growth by enhancing product differentiation and value.

Trending Factors

Eco-friendly and Sustainable Formulations Are Trending Factors

Eco-friendly and sustainable formulations are increasingly trending in the fabric softener market. There is a growing consumer preference for products that are biodegradable, free from harmful chemicals, and sourced from renewable resources. Manufacturers are responding by developing fabric softeners derived from plant-based ingredients and packaged in recyclable materials.

For example, some brands have introduced fabric softeners that are 100% biodegradable and packaged in eco-friendly bottles. This trend aligns with the broader movement towards sustainability in various industries. Recent surveys indicate that 40% of consumers prefer eco-friendly products, driving market growth in this segment. The emphasis on sustainability not only attracts environmentally conscious consumers but also fosters innovation and long-term market viability.

Fragrance Innovation Is Trending Factors

Fragrance innovation is a key trending factor in the fabric softener market. Consumers are becoming more discerning about fragrances, seeking unique and innovative scent offerings. Manufacturers are collaborating with fragrance and perfume companies to explore new scent combinations inspired by nature, exotic locations, or cultural influences.

For instance, some brands have launched seasonal or limited-edition fragrances to cater to changing consumer preferences. Market data shows that fabric softeners with innovative fragrances have seen a 20% increase in sales over the past year. This focus on fragrance innovation enhances product appeal and differentiation, driving consumer interest and market expansion. The ability to offer distinct and appealing scents is crucial in capturing consumer loyalty and expanding the market presence of fabric softeners.

Regional Analysis

Asia Pacific Dominates with 37% Market Share

Asia Pacific leads the fabric softener market with a 37% share. This dominance is driven by rapid urbanization and increasing disposable incomes. The growing middle class in countries like China and India prefers convenience and premium products, boosting fabric softener sales. Additionally, the expansion of e-commerce in the region makes it easier for consumers to access a variety of products. The rising awareness of fabric care and hygiene also contributes to the market growth.

The region's diverse consumer base and varying preferences significantly impact the fabric softener market. In urban areas, busy lifestyles drive the demand for convenient laundry solutions. Rural areas are gradually adopting these products as disposable incomes rise. The presence of local and international brands provides a wide range of options, catering to different consumer needs. This dynamic market environment supports sustained growth and innovation in fabric softener products.

The Asia Pacific region's market presence is expected to continue growing. With increasing consumer awareness and disposable incomes, the demand for premium and specialized fabric softeners will rise. E-commerce growth will further facilitate market expansion. The region is projected to maintain its dominant position, potentially increasing its market share to 40% over the next five years. Continuous innovation and targeted marketing strategies will be key to capturing this growing market.

North America

North America holds 25% of the fabric softener market share. High disposable incomes and a preference for premium products drive this market. The region is also seeing a shift towards eco-friendly products. The market is expected to grow at a steady rate of 3% annually.

Europe

Europe accounts for 20% of the market share. Environmental concerns and stringent regulations drive the demand for sustainable and eco-friendly fabric softeners. The market is experiencing moderate growth, with a 2.5% annual increase in sales.

Middle East & Africa

The Middle East & Africa region holds 8% of the market share. Growing urbanization and increasing disposable incomes are driving market growth. The region is expected to see a 4% annual growth rate due to rising awareness of fabric care.

Latin America

Latin America represents 10% of the market share. Economic development and an increasing middle class are driving demand. The market is projected to grow at an annual rate of 3.5%, supported by expanding retail networks and e-commerce.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the fabric softener market, several key players shape industry dynamics through strategic positioning and impactful market presence. Leading companies such as Procter & Gamble Co., Unilever PLC, and Henkel AG & Co. KGaA dominate the market by leveraging extensive distribution networks, robust brand portfolios, and substantial investments in R&D. These giants focus on innovation and sustainability, responding to consumer demands for eco-friendly products that align with modern lifestyle values.

Mid-sized companies like Colgate-Palmolive Company, Lion Corporation, and Kao Corporation are also significant, often focusing on specific regional markets or niche product innovations that appeal to diverse consumer segments. Their strategies typically include developing products that offer unique fragrances or specialized fabric care benefits, catering to evolving consumer preferences.

Additionally, companies such as Church & Dwight Co., Inc., and The Clorox Company emphasize their presence in the market by offering products that combine fabric softening with other functionalities like disinfection and allergen reduction, which are increasingly relevant in today’s health-conscious market.

Emerging players like Ecover Belgium NV and Marico Limited are carving out a space by focusing on natural and organic fabric softeners, tapping into the rapidly growing segment of consumers looking for sustainable living solutions.

Lastly, niche players and regional brands continue to maintain competitive pressure on larger companies, ensuring a diverse and innovative market landscape. These players, including LG Household & Health Care Ltd. and S. C. Johnson & Son, Inc., diversify the market with regional preferences and specialized products that appeal to local tastes and requirements.

Overall, the strategic interplay among these companies—ranging from global giants to regional specialists—defines the contours of the fabric softener market, influencing its growth trajectories and innovation trends.

Market Key Players

- Procter & Gamble Co.

- Unilever PLC

- Henkel AG & Co. KGaA

- Colgate-Palmolive Company

- Lion Corporation

- Kao Corporation

- Church & Dwight Co., Inc.

- LG Household & Health Care Ltd.

- The Sun Products Corporation

- Ecover Belgium NV

- S. C. Johnson & Son, Inc.

- Pigeon Corporation

- The Clorox Company

- Reckitt Benckiser Group PLC

- Marico Limited

- Other Key Players

Recent Developments

- May 2024: P&G Professional introduces Tide Professional Commercial Laundry Detergent and Downy Professional Fabric Softener to optimize laundry processes for businesses. The products are designed to remove stains in one wash and provide softness and freshness.

- August 2023: Arm & Hammer has launched a new laundry detergent in sheets format, offering a convenient and easy-to-use alternative for consumers.

- 2022: Downy has released its biggest innovation in over 30 years, introducing a new way to help remove tough odors in laundry. The product is designed to provide long-lasting freshness and softness.

Report Scope

Report Features Description Market Value (2023) USD 22.6 Billion Forecast Revenue (2033) USD 36.7 Billion CAGR (2024-2033) 5.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Liquid Fabric Softeners, Dryer Sheets, Fabric Softener Crystals, Others), By Composition (Cationic, Non-ionic, Anionic), By Formulation (Regular, Concentrated), By End User (Residential, Commercial) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Procter & Gamble Co., Unilever PLC, Henkel AG & Co. KGaA, Colgate-Palmolive Company, Lion Corporation, Kao Corporation, Church & Dwight Co., Inc., LG Household & Health Care Ltd., The Sun Products Corporation, Ecover Belgium NV, S. C. Johnson & Son, Inc., Pigeon Corporation, The Clorox Company, Reckitt Benckiser Group PLC, Marico Limited, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Procter & Gamble Co.

- Unilever PLC

- Henkel AG & Co. KGaA

- Colgate-Palmolive Company

- Lion Corporation

- Kao Corporation

- Church & Dwight Co., Inc.

- LG Household & Health Care Ltd.

- The Sun Products Corporation

- Ecover Belgium NV

- S. C. Johnson & Son, Inc.

- Pigeon Corporation

- The Clorox Company

- Reckitt Benckiser Group PLC

- Marico Limited

- Other Key Players

Our Clients

View Our Licence Options