Global Data Center Liquid Immersion Cooling Market By Type(Single-phase Immersion Cooling System, Two-phase Immersion Cooling System), By Cooling Fluids(Mineral Oil, Deionized Water, Fluorocarbon-based Fluids, Synthetics Fluids), By Application(High-performance Computing, Edge Computing, Artificial Intelligence, Cryptocurrency Mining, Others), By Data Center(Enterprise, Colocation, Wholesale, Hyperscale, Others), By End-Use Industry(BFSI, Manufacturing, IT & Telecom, Heathcare, Government & Defence, Retail, Energy, Others), By Region And Companies -

-

46212

-

May 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

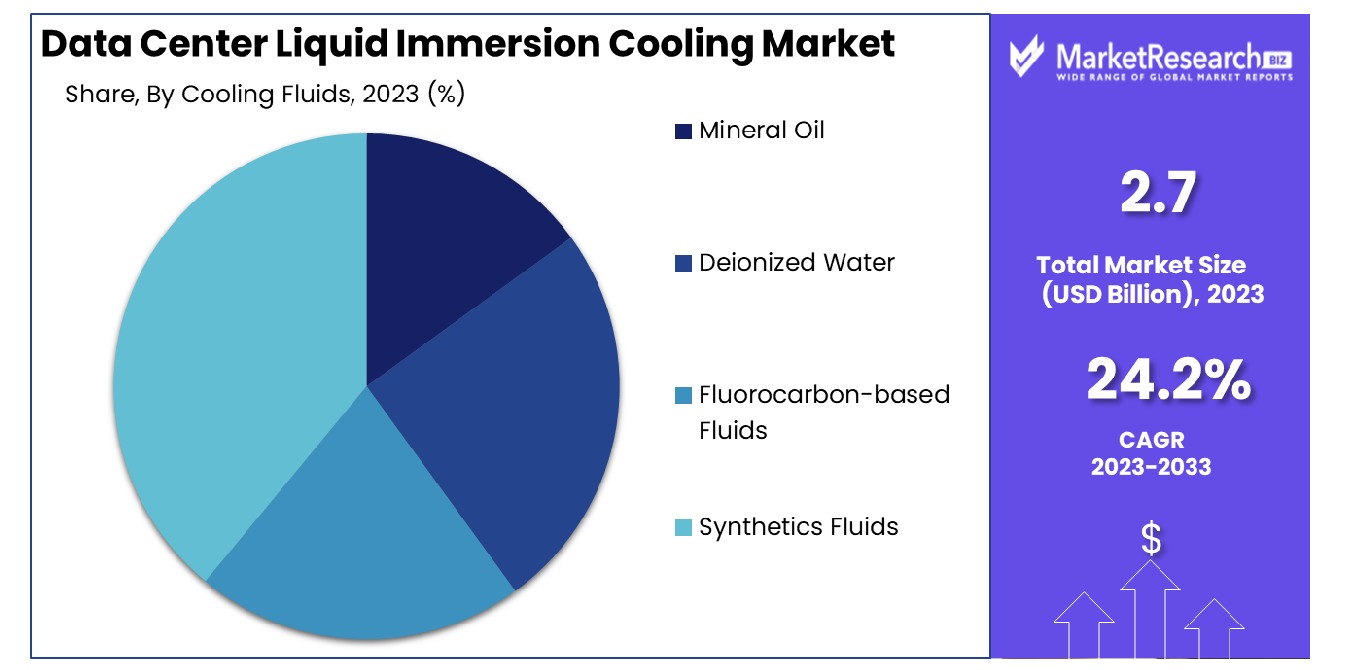

The Global Data Center Liquid Immersion Cooling Market was valued at USD 2.7 billion in 2023. It is expected to reach USD 22.3 billion by 2033, with a CAGR of 24.2% during the forecast period from 2024 to 2033.

The Data Center Liquid Immersion Cooling Market refers to the specialized industry focused on advanced cooling technologies for data centers, where hardware is submerged in a thermally conductive liquid. This method significantly enhances cooling efficiency, reduces energy consumption, and increases the lifespan of components by eliminating air cooling-related issues.

It caters to the escalating demands for high-performance computing and energy-efficient data center solutions. As such, it is critically relevant to executives and product managers who are steering their organizations toward sustainable growth, operational efficiency, and competitive advantage in the technology and data management sectors.

In the realm of data center thermal management, liquid immersion cooling technology stands out as a critical innovation poised to reshape market dynamics significantly. This technology, distinguished by its superior efficiency and reduced environmental impact, supports the growing demand for high-performance computing and large-scale data centers. As organizations increasingly focus on sustainability, immersion cooling offers a substantial reduction in cooling energy usage, which can account for up to 40% of total energy consumption in conventional data centers.

The market's expansion is further driven by the technology's ability to facilitate denser configurations and higher processor loads, which are essential for advanced applications such as artificial intelligence and big data analytics. However, the adoption rate is moderated by initial setup costs and the need for specialized infrastructure adaptations.

Supportive Data: In 2022, the market for immersion cooling technology in cryptocurrency mining was forecasted to be $302 million, and by 2030, it is expected to reach $1.7 billion. The technology's benefits extend beyond mere efficiency; it enables ultra-fast charging capabilities, allowing batteries to recharge in less than 10 minutes. Furthermore, it enhances safety by preventing battery fires and thermal runaway, while also improving cell life and overall battery lifetime through better temperature homogeneity.

Key Takeaways

- Market Growth: The Global Data Center Liquid Immersion Cooling Market was valued at USD 2.7 billion in 2023. It is expected to reach USD 22.3 billion by 2033, with a CAGR of 24.2% during the forecast period from 2024 to 2033.

- By Type: Two-phase immersion cooling dominated with a 70% market share.

- By Cooling Fluids: Synthetic fluids led by commanding 54% of the market.

- By Application: Artificial intelligence applications held a 44% dominance rate.

- By Data Center: Hyperscale data centers prevailed, comprising 45% of the sector.

- By End-Use Industry: Manufacturing, as an end-use industry, led with 27% dominance.

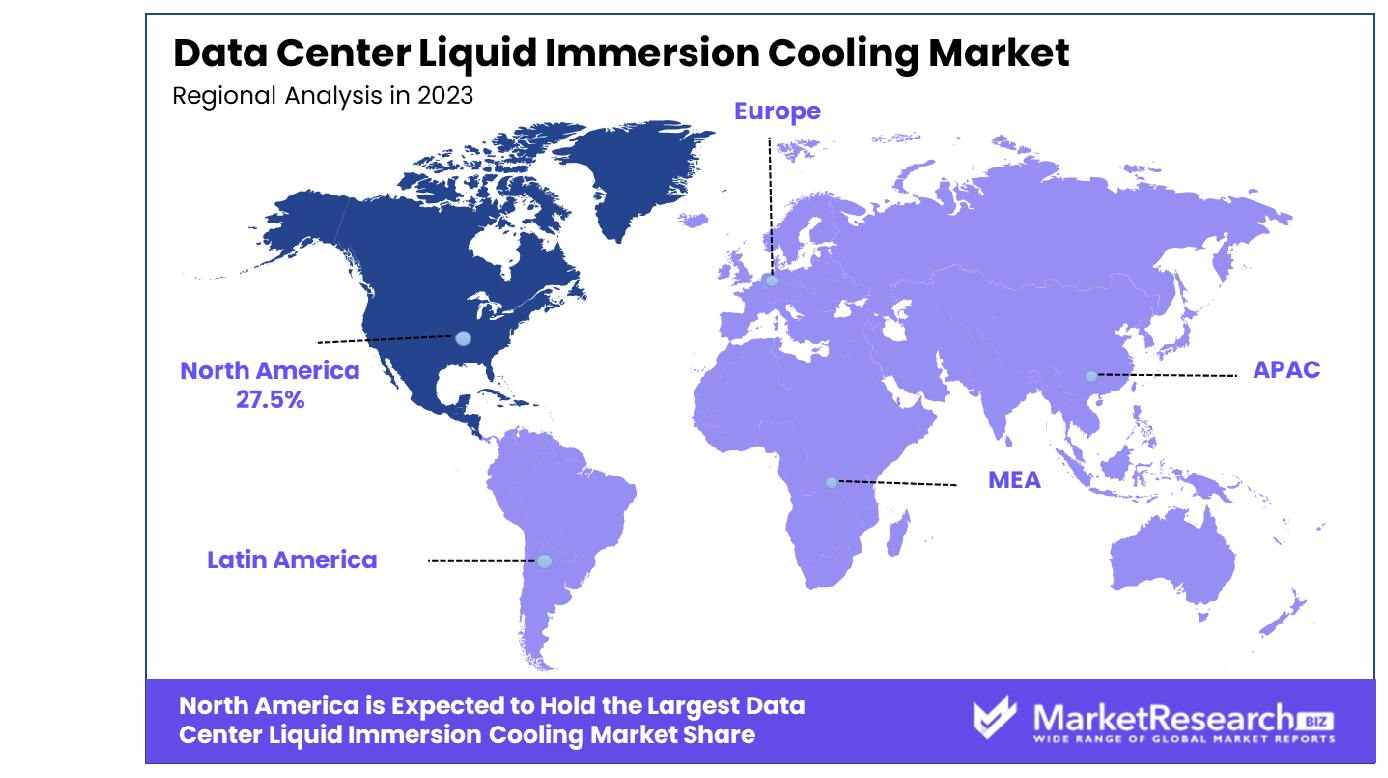

- Regional Dominance: North America holds 27.5% of the Data Center Cooling Market.

- Growth Opportunity: The 2023 growth in the global Data Center Liquid Immersion Cooling Market is driven by increased adoption in hyperscale and smaller data centers, enhancing efficiency and scalability.

Driving factors

Rising Demand for Liquid Immersion Cooling Technology

The surge in demand for liquid immersion cooling technology significantly propels the growth of the Data Center Liquid Immersion Cooling Market. This demand is primarily driven by the technology's ability to efficiently manage the heat generated by increasingly powerful and dense server configurations. Traditional air-cooling methods are becoming insufficient due to their higher energy consumption and lesser effectiveness in cooling high-performance computing systems.

Liquid immersion cooling, by directly immersing hardware in a non-conductive liquid, offers a solution that not only enhances cooling efficiency but also reduces energy consumption by up to 40% compared to conventional methods. This technology's adoption is expected to continue rising as data centers increasingly prioritize energy efficiency and operational cost reduction.

Growing Carbon Impact of Data Centers

The growing carbon footprint of data centers has emerged as a critical driver for the adoption of green technologies such as liquid immersion cooling. Data centers are estimated to consume about 2% of the world's total energy, a figure that is projected to increase given the exponential growth in data generation and processing. This escalation necessitates the implementation of environmentally sustainable practices.

Liquid immersion cooling systems significantly reduce energy usage and, consequently, the carbon emissions associated with cooling processes. By minimizing the reliance on air conditioning and enhancing energy efficiency, these systems contribute directly to the reduction of the overall environmental impact of data centers, fostering market growth amid rising environmental concerns.

Consolidation Operations Across Data Center Operators

The trend of consolidation among data center operators directly influences the adoption of liquid immersion cooling systems. As operators merge and standardize their facilities, there is a growing need for more scalable and efficient cooling solutions. Liquid immersion cooling systems are highly scalable, allowing for easier expansion and customization according to specific operational needs.

This scalability is particularly beneficial in consolidated operations where uniformity and maximization of space and resources are critical. Moreover, the operational efficiency gained through these cooling systems supports the larger infrastructure, optimizing overall performance while driving down costs associated with cooling large, consolidated data centers.

Restraining Factors

High Investment with Greater Capital Expenditure

One of the primary restraining factors for the growth of the Data Center Liquid Immersion Cooling Market is the high initial investment and greater capital expenditure required. The installation of liquid immersion cooling systems involves significant upfront costs including the setup of specialized infrastructure, purchasing non-conductive coolants, and potentially modifying existing hardware to be compatible with liquid cooling solutions.

These expenses can be prohibitive for smaller data centers or those with limited budgets, impacting the adoption rate of this technology. Although liquid immersion cooling can offer long-term savings on energy and operational costs, the initial financial barrier remains a significant hurdle, slowing down market penetration and growth.

Lack of Awareness About the Benefits of Liquid Cooling Among End Users

The lack of awareness about the benefits of liquid immersion cooling technology among end users also significantly restrains market growth. Despite its advantages in efficiency and sustainability, many potential users remain unaware of how liquid cooling systems can be integrated into their existing data center operations. This awareness gap results from the relatively recent development and implementation of such technologies compared to traditional cooling methods.

Education and dissemination of information through industry seminars, workshops, and case studies are crucial for overcoming this barrier. Enhancing understanding among end users about the operational and environmental benefits of liquid immersion cooling is essential to increasing its adoption and mitigating its slow market growth rate.

By Type Analysis

The Two-phase Immersion Cooling System led the market with a 70% dominance by type.

In 2023, the Two-phase Immersion Cooling System held a dominant market position in the "By Type" segment, capturing more than a 70% share. This segment outperformed its counterpart, the Single-phase Immersion Cooling System, which trailed significantly in market adoption. The robust performance of the Two-phase system can be primarily attributed to its superior efficiency in heat dissipation and lower operational costs, making it highly preferable in high-density computing environments such as data centers and cryptocurrency mining operations.

The Two-phase Immersion Cooling System utilizes a bi-phase method where the coolant undergoes a phase change from liquid to vapor, effectively removing heat from the system. This process allows for the cooling of components at a much higher efficiency compared to the Single-phase system, where the coolant remains in a liquid state and circulates within the cooling loop. The advanced cooling mechanism of the Two-phase system significantly enhances the thermal management capabilities, leading to increased reliability and longevity of hardware components.

Moreover, the growing demand for energy-efficient and sustainable cooling solutions has propelled the adoption of Two-phase systems. Organizations are increasingly prioritizing green technologies to reduce their carbon footprint and operational costs, which aligns well with the benefits offered by Two-phase immersion cooling technologies. This trend is expected to continue, further strengthening the market position of Two-phase systems in the upcoming years.

By Cooling Fluids, Analysis

Synthetic fluids were the most used cooling fluids, capturing 54% of the market share.

In 2023, Synthetic Fluids held a dominant market position in the "By Cooling Fluids" segment capturing more than a 54% share. This segment outstripped other types such as Mineral Oil, Deionized Water, and Fluorocarbon-based Fluids in market penetration. The prominence of Synthetic Fluids is largely due to their exceptional thermal and chemical stability, which makes them highly effective in diverse cooling applications, particularly in demanding environments like electronic and data center cooling systems.

Synthetic Fluids, known for their non-conductive and non-corrosive properties, offer significant advantages over alternatives. They are particularly valued in high-tech industries where the protection and longevity of sensitive components are crucial. Unlike Mineral Oils and Deionized Water, Synthetic Fluids can operate at a wider range of temperatures and do not pose the same risks of corrosion or scaling. Furthermore, their compatibility with a broad array of materials reduces the risk of equipment damage and extends maintenance intervals.

The market's inclination towards Synthetic Fluids is also driven by their environmental benefits. These fluids often have a lower environmental impact compared to Fluorocarbon-based Fluids, which are under scrutiny for their potential environmental hazards, including their role in ozone depletion and global warming. This shift is aligned with global trends prioritizing sustainability and regulatory compliance in industrial operations.

The strategic adoption of Synthetic Fluids is anticipated to continue as technological advancements further enhance their efficiency and environmental safety profiles. With ongoing research and development, Synthetic Fluids are set to consolidate their position in the market, responding effectively to the evolving needs of modern industries.

By Application Analysis

Artificial Intelligence applications held the largest segment at 44% in immersion cooling systems.

In 2023, Artificial Intelligence held a dominant market position in the "By Application" segment of capturing more than a 44% share. This segment outpaced other applications such as High-performance Computing, Edge Computing, Cryptocurrency Mining, and Others in market adoption. The significant lead of Artificial Intelligence is primarily driven by the escalating demand for AI applications across various sectors, including healthcare, automotive, finance, and retail, which require substantial data processing capabilities.

Artificial Intelligence applications necessitate high levels of computational power and efficiency, which in turn require advanced cooling solutions to manage the heat generated by intense workloads. This need is particularly acute in data centers and cloud computing environments that host AI systems, where effective heat management is critical to maintain system performance and reliability. The efficiency of cooling directly impacts the operational stability and energy consumption of AI infrastructures.

Moreover, the integration of AI with other emerging technologies like the Internet of Things (IoT) and big data analytics has further expanded the scope of AI applications, thereby increasing the demand for sophisticated cooling solutions. As AI technologies continue to evolve and penetrate new markets, the need for effective thermal management solutions becomes more pronounced, ensuring the long-term sustainability of these systems.

The dominance of Artificial Intelligence in this market segment is expected to grow, bolstered by ongoing technological advancements and increasing investment in AI infrastructure. This trend underscores the critical role of innovative cooling solutions in supporting the expanding capabilities and applications of artificial intelligence.

By Data Center Analysis

Hyperscale data centers primarily adopted immersion cooling systems, representing 45% of the market.

In 2023, Hyperscale data centers held a dominant market position in the "By Data Center" segment capturing more than a 45% share. This segment surpassed other types such as Enterprise, Colocation, Wholesale, and Others in market uptake. The growing dominance of hyperscale data centers is attributed to their ability to efficiently manage vast amounts of data and provide significant scalability options in response to increasing demand for cloud-based services and big data analytics.

Hyperscale data centers are essential in supporting large-scale cloud environments, where they offer robust infrastructure designed to support extensive computations and storage needs of major tech giants and multinational corporations. Their architecture is specifically tailored to optimize energy efficiency and operational costs, which is crucial given the high energy demands associated with maintaining large data repositories and continuous data processing.

Moreover, the increasing reliance on digital technologies and the rapid expansion of the Internet of Things (IoT) have driven the demand for more extensive and reliable data processing capabilities. Hyperscale data centers meet these demands by providing high-capacity networks and the ability to scale resources quickly, making them particularly suited to sectors such as e-commerce, online gaming, and digital communication services.

The market’s inclination towards Hyperscale data centers is expected to persist, as the global data surge necessitates more innovative and expansive data management solutions. This segment's growth is underpinned by its critical role in enabling high-performance computing solutions and extensive data handling capacities required by modern digital economies.

By End-Use Industry Analysis

In the end-use industry category, manufacturing emerged as the top sector with a 27% share.

In 2023, Manufacturing held a dominant market position in the "By End-Use Industry" segment, capturing more than a 27% share. This segment outperformed other industries such as BFSI, IT & Telecom, Healthcare, Government & Defense, Retail, Energy, and Others in terms of market penetration. The substantial lead in Manufacturing is primarily attributed to the industry's escalating demand for advanced technological integration and automation, necessitating robust IT infrastructure support and sophisticated data management systems.

The Manufacturing industry's drive towards Industry 4.0 has significantly contributed to its dominance in this market segment. The integration of IoT, artificial intelligence, and machine learning technologies into manufacturing processes has intensified the need for data centers that can handle large volumes of data with high efficiency and reliability. These technologies not only enhance operational efficiency but also enable predictive maintenance, quality control, and supply chain optimization, all of which require substantial computational resources and data storage capabilities.

Furthermore, the global push for digital transformation within the manufacturing sector has spurred the development of smart factories and interconnected manufacturing units that rely heavily on data-driven insights. This trend has increased the reliance on data centers, which play a critical role in the seamless operation of these advanced facilities by ensuring continuous uptime, data security, and scalability.

The outlook for the Manufacturing sector's reliance on data center solutions remains robust, driven by continuous advancements in technology and the increasing digitization of manufacturing operations worldwide. This sustained demand underscores the critical role of data centers in supporting the expansive and evolving needs of the modern manufacturing industry.

Key Market Segments

By Type

- Single-phase Immersion Cooling System

- Two-phase Immersion Cooling System

By Cooling Fluids

- Mineral Oil

- Deionized Water

- Fluorocarbon-based Fluids

- Synthetics Fluids

By Application

- High-performance Computing

- Edge Computing

- Artificial Intelligence

- Cryptocurrency Mining

- Others

By Data Center

- Enterprise

- Colocation

- Wholesale

- Hyperscale

- Others

By End-Use Industry

- BFSI

- Manufacturing

- IT & Telecom

- Heathcare

- Government & Defence

- Retail

- Energy

- Others

Growth Opportunity

Increasing Number of Hyperscale Data Centers Globally

The global surge in the construction of hyperscale data centers is a prominent driver for the data center liquid immersion cooling market. As data consumption and processing needs escalate, hyperscale data centers have become pivotal in handling large volumes of data efficiently. These facilities typically require advanced cooling solutions to manage the immense heat generated by high-performance computing resources.

Liquid immersion cooling, known for its superior heat dissipation capabilities and energy efficiency, is increasingly being adopted to enhance operational reliability and reduce cooling costs. This trend is expected to boost market growth, as operators of hyperscale data centers seek more sustainable and cost-effective cooling solutions to accommodate escalating computational demands.

Adoption of Liquid Immersion Cooling in Small and Mid-size Data Centers

There is a noticeable shift towards the adoption of liquid immersion cooling technologies in small and mid-size data centers. This trend is driven by the need for energy-efficient cooling solutions that can scale with growing data demands while maintaining a smaller footprint. Liquid immersion cooling offers these facilities a way to achieve higher energy efficiency and potentially lower operational costs compared to traditional air-cooled systems.

As small and mid-size data centers explore ways to optimize their operations and reduce environmental impact, the adoption of liquid immersion cooling presents a significant opportunity for market expansion in 2023 and beyond. This adoption is anticipated to proliferate, supported by increasing awareness and the tangible benefits these cooling systems offer over conventional methods.

Latest Trends

Increasing Use of GPUs in Data Centers

The increasing deployment of Graphics Processing Units (GPUs) in data centers is a significant trend shaping the liquid immersion cooling market in 2023. GPUs, essential for processing complex computations such as artificial intelligence (AI) and machine learning (ML), generate substantial amounts of heat. Traditional air cooling systems are often inadequate for such high-density setups, pushing data center operators towards more efficient solutions like liquid immersion cooling.

This technology not only addresses the high heat dissipation requirements but also enhances energy efficiency and system performance. The trend towards GPU-intensive applications is expected to continue, further driving the adoption of liquid immersion cooling solutions to manage the thermal load effectively.

Conversion of Old Buildings into Data Centers

Another trend gaining momentum is the conversion of old buildings into data centers, which presents unique opportunities for the adoption of liquid immersion cooling systems. These buildings, not originally designed for high-density computing, often lack the infrastructure for traditional cooling methods. Liquid immersion cooling becomes a viable solution, offering flexibility in deployment and superior cooling efficiency.

This adaptability makes it ideal for retrofitting in non-traditional spaces, thereby facilitating the expansion of data center operations without the need for extensive structural modifications. The trend of repurposing real estate into data centers, driven by the growing demand for data processing and storage capacities, is likely to enhance the market for liquid immersion cooling systems in 2023.

Regional Analysis

North America holds a 27.5% share of the global Data Center Liquid Immersion Cooling Market.

The global market for data center liquid immersion cooling is segmented into several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. Each region presents unique growth dynamics based on technological adoption and data center infrastructure development.

North America is the dominating region, holding 27.5% of the market share. The region's leadership in the market can be attributed to the robust presence of technology companies and the rapid adoption of advanced cooling solutions to manage the heat generated by increasing data processing needs. Additionally, the push towards sustainable energy practices in data centers further drives the adoption of energy-efficient cooling methods like liquid immersion cooling.

Europe follows, with a significant adoption rate driven by stringent energy efficiency regulations and the growing number of data centers. Countries like Germany, the UK, and France are seeing increased investments in new data center projects, which include advanced cooling technologies to comply with environmental standards.

The Asia Pacific region is experiencing the fastest growth, fueled by the expanding IT and telecommunications sectors, especially in China and India. The surge in digital services has led to a proliferation of data centers requiring efficient cooling solutions to handle high heat loads effectively.

Meanwhile, the Middle East & Africa, and Latin America are emerging markets in the data center liquid immersion cooling sector. These regions are experiencing gradual adoption due to the increasing move towards digital transformation and the establishment of new data centers, particularly in urban areas.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

The global data center liquid immersion cooling market in 2023 is characterized by the active involvement of several key companies, each contributing uniquely to the industry's landscape. Companies such as 3M Company and Fujitsu Limited are notable for their technological innovations and extensive market reach, driving forward the adoption of advanced cooling solutions in both established and emerging markets.

3M Company, with its expertise in fluid technology, has been pivotal in providing engineered fluids that are central to effective liquid immersion cooling systems. Their products are renowned for safety and environmental sustainability, which is a critical selling point for data centers aiming to reduce their carbon footprint.

Alfa Laval AB and Asetek Group bring robust mechanical and cooling solutions to the table, offering systems that enhance energy efficiency and optimize heat transfer capabilities. Their continuous improvement in product offerings helps meet the increasing requirements of high-performance computing environments.

Emerging players like Asperitas B.V. and Submer Technologies S.L. are disrupting the market with innovative modular and scalable cooling solutions. These solutions cater specifically to the needs of cloud service providers and enterprises with intensive data workloads, highlighting the shift towards customization in cooling technologies.

Meanwhile, Green Revolution Cooling Inc. and Midas Green Technologies LLC focus on turnkey solutions that retrofit existing data center infrastructures, demonstrating the market's adaptability to diverse customer needs.

Schneider Electric SE leverages its global presence to integrate these cooling technologies with overall data center infrastructure management, ensuring holistic and sustainable data center operations.

Collectively, these companies are not just responding to current demands but are also shaping future trends in the data center liquid immersion cooling market. Their efforts are instrumental in driving market growth, with a keen focus on innovation, sustainability, and operational efficiency.

Market Key Players

- 3M Company

- Alfa Laval AB

- Asetek Group

- Asperitas B.V.

- DCX - The Liquid Cooling Company

- Fujitsu Limited

- Green Revolution Cooling Inc.

- Midas Green Technologies LLC

- Schneider Electric SE

- Submer Technologies S.L.

Recent Development

- In April 2024, Microsoft and IBM lead in green tech adoption. Microsoft supports the Green Software Foundation, fostering climate-first software. IBM launches Green IT Analyzer on AWS, assessing carbon footprint for IT infrastructures.

- In April 2024, Chemours proposes two-phase immersion cooling (2-PIC) for data centers, reducing energy usage up to 90%. Advocates for policy safeguarding F-gases to advance sustainability.

Report Scope

Report Features Description Market Value (2023) USD 2.7 Billion Forecast Revenue (2033) USD 22.3 Billion CAGR (2024-2032) 24.2% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type(Single-phase Immersion Cooling System, Two-phase Immersion Cooling System), By Cooling Fluids(Mineral Oil, Deionized Water, Fluorocarbon-based Fluids, Synthetics Fluids), By Application(High-performance Computing, Edge Computing, Artificial Intelligence, Cryptocurrency Mining, Others), By Data Center(Enterprise, Colocation, Wholesale, Hyperscale, Others), By End-Use Industry(BFSI, Manufacturing, IT & Telecom, Heathcare, Government & Defence, Retail, Energy, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape 3M Company, Alfa Laval AB, Asetek Group, Asperitas B.V., DCX - The Liquid Cooling Company, Fujitsu Limited, Green Revolution Cooling Inc., Midas Green Technologies LLC, Schneider Electric SE, Submer Technologies S.L Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- 3M Company

- Alfa Laval AB

- Asetek Group

- Asperitas B.V.

- DCX - The Liquid Cooling Company

- Fujitsu Limited

- Green Revolution Cooling Inc.

- Midas Green Technologies LLC

- Schneider Electric SE

- Submer Technologies S.L.

Our Clients

View Our Licence Options