Computer Microchip Market Report By Type of Microchip (Central Processing Unit (CPU), Graphics Processing Unit (GPU), Memory Chips (RAM, ROM, Flash memory), Application-Specific Integrated Circuit (ASIC), Field-Programmable Gate Array (FPGA), Others), By End-Use Industry (Consumer Electronics , Automotive, Others), By Application, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

2387

-

March 2024

-

172

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

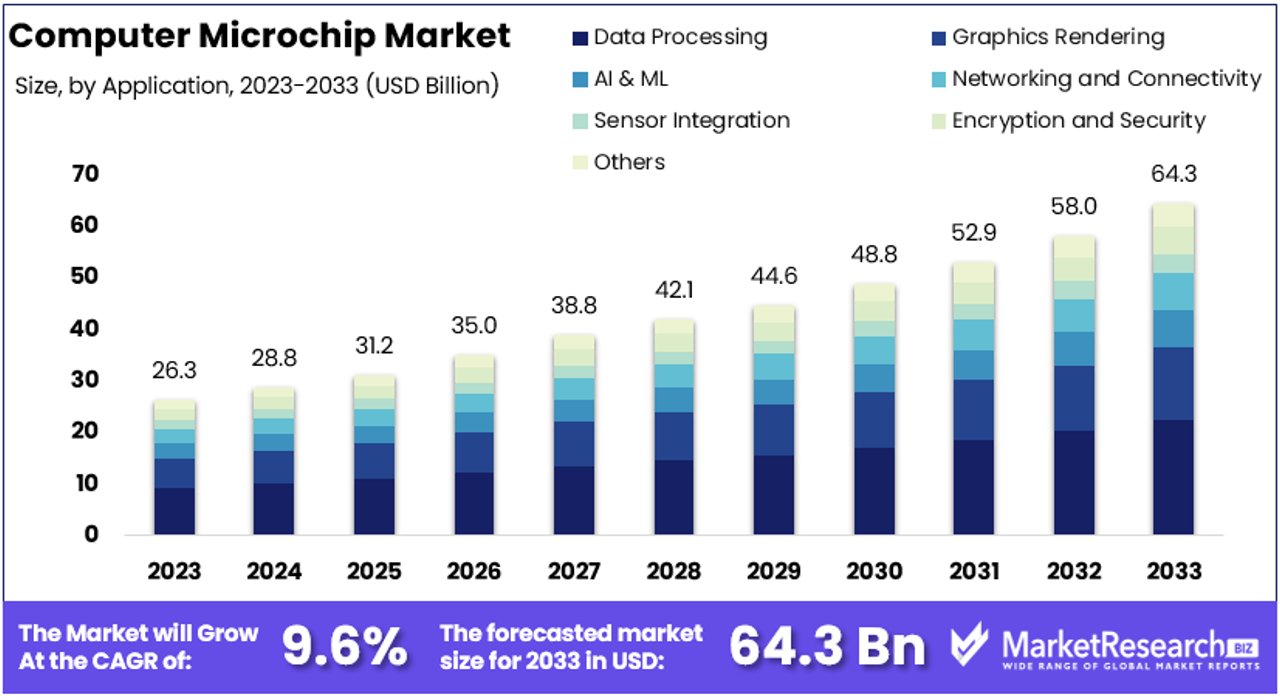

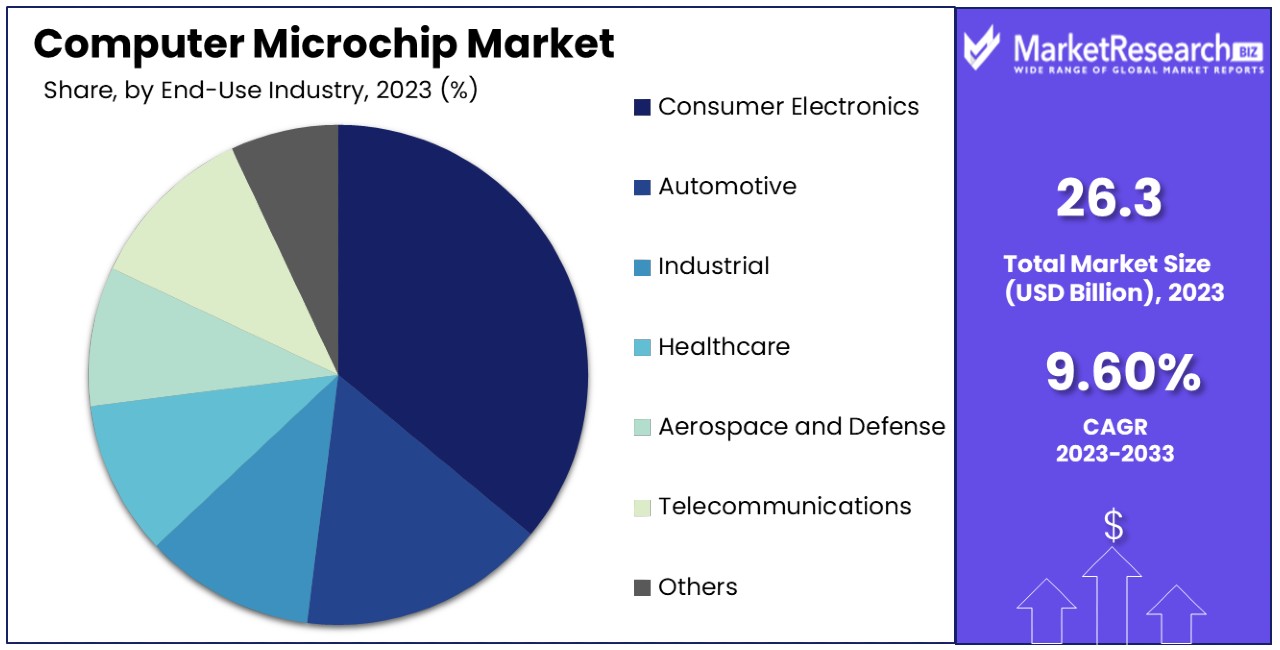

The Global Computer Microchip Market size is expected to be worth around USD 64.3 Billion by 2033, from USD 26.3 Billion in 2023, growing at a CAGR of 9.60% during the forecast period from 2024 to 2033.

The surge in demand for new innovations and rise of microchips in smartphones, television and health monitor devices are some of the main key driving factors for the computer microchip.

The computer microchip is also called as the integrated circuit or semiconductor chip, which is a small electronic device that includes millions to billions of microscopic electronic components like transistors, capacitors and resistors fictitious on a semiconductor material. It also acts as the fundamental building block of contemporary digital technology.

Microchips functions are the central processing unit, memory or other dedicated functions in the computers and electronic devices. They perform instructions, process data and execute calculations at exceedingly high speeds making the functionality of computers, IoT devices, smartphones and different electronic systems.

New advancements in microchip technology have led to surge processing power, minimized size and lessen power consumptions, facilitating the development of smaller, faster and more energy effective electronic devices. Microchips endure to propel innovation all across industries by powering everything from consumer electronics to medical equipments and vital infrastructures.

According to an article published by Reuters in January 2024, highlights that the US commerce department has awarded microchip technology USD 162 million in government permits to step up US production of semiconductors and microcontroller units’ key to consumer and defense sectors.

The investments will also grant microchip to 3X production of mature node semiconductor chips and microcontroller units at 2 US factories. It is second in the USD 52.7 billion program, "Chips for America" that congress has approved in August 2022 to subsidise semiconductor manufacturing and research. The planned award to Microchip, which contains of USD 90 million to enlarge a fabrication facility in Colorado and USD 72 million for expansion of a similar facility in Oregon, will help cut reliance on foreign production.

Computer microchips provides new advantages like improved processing power, making faster data processing and complex computations. They simplify miniaturizations of devices by leading to smaller and more portable electronics. Moreover, microchips preserve energy by contributing to enhanced energy efficiency and durable battery life in electronic equipments. the demand for the computer microchips will increase due to its requirement in the electronic devices that will help in market expansion in the coming years.

Key Takeaways

- Market Value: The Computer Microchip Market is projected to reach approximately USD 64.3 Billion by 2033, showing significant growth from USD 26.3 Billion in 2023, with a CAGR of 9.60% during the forecast period from 2024 to 2033.

- Dominant Segments:

- Type of Microchip Analysis: Central Processing Units (CPUs) lead the market due to their vital role in computing devices, followed by Graphics Processing Units (GPUs) which have expanded their applications into deep learning and analytics.

- End-Use Industry Analysis: Consumer Electronics is the dominant segment, driven by the constant demand for more powerful microchips in smartphones, tablets, PCs, and gaming consoles.

- Regional Analysis: Asia Pacific dominates the market with a 32% market share, followed by North America with approximately 25%, highlighting the strong presence of leading technology companies and innovation ecosystems.

- Key Players: Major players in the Computer Microchip Market include Intel Corporation, Advanced Micro Devices, Inc. (AMD), Huawei Technologies Co., Ltd., NVIDIA Corporation, Qualcomm Incorporated, and others, driving innovation and market growth through advanced technologies and strategic partnerships.

- Analyst Viewpoint: The Computer Microchip Market is dynamic, driven by technological advancements and evolving end-user requirements across various industries and applications, presenting opportunities for growth and innovation.

- Growth Opportunities: Opportunities lie in meeting the increasing demand for faster, more efficient microchips, especially in emerging technologies like AI, machine learning, and 5G. Additionally, addressing specific industry needs such as automotive electrification, IoT integration, and digital security can unlock further growth potential in the market.

Driving Factors

Exponential Growth of Data and Internet of Things (IoT) Drives Market Growth

The relentless expansion of data and the proliferation of Internet of Things (IoT) devices serve as a major propellant for the Computer Microchip Market. With global data volumes poised to hit 175 zettabytes by 2025, according to Deloitte, the demand for sophisticated microchips capable of efficiently processing, storing, and transmitting this colossal amount of information is soaring.

This growth is particularly significant in cloud computing, where giants like Amazon, Microsoft, and Google depend on high-performance chips for their data centers. These microchips are not just the backbone of data management but also play a crucial role in supporting the vast array of services offered by these platforms, highlighting their indispensable nature in today's data-driven ecosystem.

Advancements in Artificial Intelligence (AI) and Machine Learning Drive Market Growth

The Computer Microchip Market is undergoing a transformation driven by rapid advancements in Artificial Intelligence (AI) and Machine Learning. The development of AI accelerators or neural processors, designed for parallel processing and accelerated computations, is crucial for the efficient execution of AI workloads. This evolution is spearheaded by companies like NVIDIA, Google, and Intel, which are heavily investing in AI-specific microchips.

These chips are vital for training deep learning models, pushing the boundaries of what machines can learn and perform. As AI and machine learning technologies become increasingly integrated into various sectors, the demand for these specialized microchips is expected to skyrocket, marking a significant shift in the market's growth trajectory.

Proliferation of Connected Devices and 5G Adoption Drive Market Growth

The Computer Microchip Market is witnessing substantial growth, fueled by the widespread adoption of connected devices and the rollout of 5G networks. With 5G coverage globally anticipated to reach around 40 percent by the end of 2023, and China leading with a 95 percent population coverage, the demand for advanced microchips is on the rise.

These chips are essential for powering a new generation of applications and services that leverage 5G's higher data speeds and lower latency. Key players like Qualcomm and MediaTek are at the forefront, developing chipsets that are enabling this technological leap, indicating a significant market opportunity driven by the 5G revolution.

Advancements in Automotive and Industrial Automation Drive Market Growth

The integration of advanced technologies in the automotive and industrial sectors is significantly influencing the Computer Microchip Market. The adoption of advanced driver assistance systems (ADAS) and autonomous driving technologies in the automotive industry, alongside the embrace of Industry 4.0 and smart manufacturing in industrial automation, necessitates the use of specialized microchips.

These chips are integral for processing sensor data and facilitating real-time decision-making, underscoring the critical role they play in the advancement of these sectors. Companies like NXP Semiconductors and Infineon Technologies are leading the charge, providing microchips that meet the complex requirements of these applications, thereby driving market growth in new and innovative directions.

Restraining Factors

Intellectual Property Challenges and Legal Disputes Restrain Market Growth

The Computer Microchip Market faces significant constraints due to intellectual property (IP) challenges and legal disputes. This highly competitive landscape sees companies vigorously defending their IP rights, often resulting in frequent patent infringements and litigation battles.

Such disputes can lead to substantial financial burdens from litigation costs, product delays, and market uncertainties, all of which impede innovation and the timely adoption of new technologies. A notable example includes the prolonged legal conflict between Qualcomm and Apple, which has instigated widespread uncertainty in the mobile chipset sector. These IP challenges not only deter market expansion but also inhibit the introduction and integration of breakthrough technologies.

Power Consumption and Thermal Management Restrain Market Growth

As microchips advance in power and shrink in size, managing power consumption and heat dissipation emerges as a critical hurdle. The challenge of excessive heat generation is twofold: it can cause performance throttling, diminishing the microchip's reliability and efficiency, and necessitate more elaborate cooling solutions, impacting both device design and user experience.

This scenario forces microchip manufacturers to prioritize the development of more energy-efficient and thermally manageable chips, a process that requires significant research and development investment. The ongoing struggle with power and thermal management not only restricts the potential performance advancements in microchips but also poses a significant barrier to market growth, as manufacturers strive to meet the evolving demands of increasingly compact and powerful electronic devices.

Type of Microchip Analysis

In the diverse landscape of the Computer Microchip Market, Central Processing Units (CPUs) emerge as the dominant sub-segment, primarily due to their indispensable role in computing devices. CPUs, often referred to as the "brain" of computers, execute instructions from software applications, making them crucial for the functioning of computers, smartphones, and many other electronic devices. The demand for CPUs is driven by their continuous evolution towards higher speed, efficiency, and lower power consumption, catering to the ever-increasing computational needs of both consumer and enterprise markets.

The Graphics Processing Unit (GPU) sub-segment, initially designed to accelerate the creation of images in a frame buffer intended for output to a display, has expanded its role significantly. GPUs are now pivotal in accelerating deep learning, analytics, and engineering applications, making them indispensable in fields ranging from gaming to scientific research. The surge in AI and machine learning applications has notably boosted the demand for high-performance GPUs.

Memory Chips, including RAM, ROM, and Flash memory, are essential for storing data and applications in electronic devices. The growing data volumes and the need for faster data access speeds have escalated the demand for advanced memory solutions, making this sub-segment vital for the market's growth.

Application-Specific Integrated Circuits (ASICs) and Field-Programmable Gate Arrays (FPGAs) represent specialized segments. ASICs are customized for a particular use rather than intended for general-purpose use, offering efficiency benefits in specific applications like mining cryptocurrencies. FPGAs, on the other hand, provide flexibility with their programmable features, finding applications in prototyping and in industries requiring specific, adaptable computing tasks.

The "Others" category encompasses a broad range of microchips, including digital signal processors (DSPs), microcontrollers (MCUs), and sensor chips, each serving niche applications that contribute to the overall growth and diversification of the Computer Microchip Market. This diversity reflects the market's dynamic nature, responding to evolving technological advancements and emerging application requirements.

End-Use Industry Analysis

The Computer Microchip Market caters to a vast array of end-use industries, with Consumer Electronics emerging as the dominant segment. This includes a wide range of products such as smartphones, tablets, PCs, and gaming devices. The ubiquity of these devices in daily life, combined with rapid technological advancements, fuels constant demand for newer, more powerful microchips. The push for miniaturization and better energy efficiency in consumer electronics continues to drive innovation and market growth. Moreover the demand for fingerprint sensors is steadily increasing as they are widely used in various applications such as smartphones, laptops, and security systems.

Automotive industry's integration of microchips has been accelerating, driven by advancements in infotainment systems, advanced driver assistance systems (ADAS), and the electrification of vehicles. Microchips in the automotive sector are essential for enhancing vehicle performance, safety, and the user experience.

The Industrial sector, encompassing manufacturing and process control, increasingly relies on microchips for automation and smart factory solutions, which enhance efficiency and productivity. Healthcare is another significant segment, where microchips play crucial roles in diagnostic equipment, wearable health monitors, and medical imaging devices.

Aerospace and Defense demand highly reliable and ruggedized microchips for applications in navigation, communication, and surveillance systems. Meanwhile, Telecommunications relies on microchips for infrastructure, mobile devices, and emerging technologies like 5G.

Application Analysis

In terms of applications, Data Processing stands out as the cornerstone of the Computer Microchip Market, essential for the operation of virtually all electronic devices and systems. This segment's demand is propelled by the increasing need for faster, more efficient data processing capabilities in sectors ranging from consumer electronics to enterprise servers.

Graphics Rendering is critical in the gaming, entertainment, and professional visualization industries, driving demand for GPUs alongside traditional CPUs. The rapid growth in video content creation and consumption further bolsters this segment.

Artificial Intelligence and Machine Learning have become pivotal, with specialized processors like GPUs, TPUs, and FPGAs being developed to handle the complex computations required by these technologies. This segment is experiencing explosive growth due to its wide-ranging applications across industries.

Networking and Connectivity are essential for the functioning of the internet and telecommunications networks, with microchips enabling everything from home routers to global data centers. Sensor Integration, crucial for IoT devices, automotive systems, and smart home technologies, demands microchips that can process data from various sensors efficiently.

Encryption and Security applications are increasingly important in a world where digital security concerns are paramount. Microchips designed for encryption help secure data transactions and storage across multiple platforms.

The "Others" category includes specialized applications such as digital signal processing and power management, each contributing to the market's diversity and growth potential.

Key Market Segments

By Type of Microchip

- Central Processing Unit (CPU)

- Graphics Processing Unit (GPU)

- Memory Chips (RAM, ROM, Flash memory)

- Application-Specific Integrated Circuit (ASIC)

- Field-Programmable Gate Array (FPGA)

- Others

By End-Use Industry

- Consumer Electronics (Smartphones, Tablets, PCs, Gaming Consoles)

- Automotive

- Industrial

- Healthcare

- Aerospace and Defense

- Telecommunications

- Others

By Application

- Data Processing

- Graphics Rendering

- Artificial Intelligence and Machine Learning

- Networking and Connectivity

- Sensor Integration

- Encryption and Security

- Others

Growth Opportunities

Internet of Things (IoT) and Edge Computing Offers Growth Opportunity

The burgeoning Internet of Things (IoT) market is a key driver for the Computer Microchip Market, offering vast opportunities for growth. With billions of devices getting connected, the demand for microchips that are both low-power and high-performance is surging. These chips are essential for processing data locally at the edge, which minimizes latency and boosts efficiency across various applications.

This innovation facilitates real-time data analysis and decision-making, particularly beneficial in sectors such as industrial automation, smart cities, and healthcare. The ability to process data on the device rather than relying on cloud computing reduces bandwidth requirements and speeds up response times, marking a significant shift in how data is managed and utilized.

Autonomous Vehicles and Advanced Driver-Assistance Systems (ADAS) Offer Growth Opportunity

The advent of autonomous vehicles and the enhancement of Advanced Driver-Assistance Systems (ADAS) are significantly influencing the demand for specialized, powerful microchips. These chips must handle and process enormous volumes of sensor data in real time to ensure safe and efficient operation.

Companies like Tesla, Nvidia, and Mobileye are pioneering the development of custom microchips and systems-on-a-chip (SoCs) tailored for these applications. The integration of machine learning and parallel processing technologies is crucial for interpreting complex environmental data, making autonomous driving both possible and practical. As autonomous vehicles edge closer to mainstream adoption, the market for these specialized microchips is poised for exponential growth, underlining their critical role in the future of transportation.

Trending Factors

Artificial Intelligence (AI) and Machine Learning Are Trending Factors

The explosion of AI and machine learning applications across various sectors is a major trend driving the Computer Microchip Market. The need for microchips that support parallel processing and can perform accelerated computations has surged, pushing companies like Nvidia, Google, and AMD to innovate with AI-specific chips such as GPUs and TPUs.

These chips are designed to efficiently handle the intensive workloads of training and running deep learning models, facilitating advancements in AI research and application development. The demand for such specialized microchips is skyrocketing as AI and machine learning become integral to new technologies and services, making them a dominant trend in the microchip industry.

Chiplet and Heterogeneous Integration Are Trending Factors

The shift towards chiplet and heterogeneous integration marks a significant trend within the microchip industry, reflecting a move away from monolithic chip designs. This method combines several smaller, specialized chiplets into a single package, offering a flexible and scalable approach to chip design and manufacturing.

Leading companies like AMD and Intel are leveraging chiplet architectures to enhance performance and power efficiency, as well as to reduce development costs and accelerate time-to-market for new products. This trend is driven by the growing demand for more powerful and efficient computing solutions, making chiplet and heterogeneous integration a key factor in the industry's ongoing evolution and expansion.

Regional Analysis

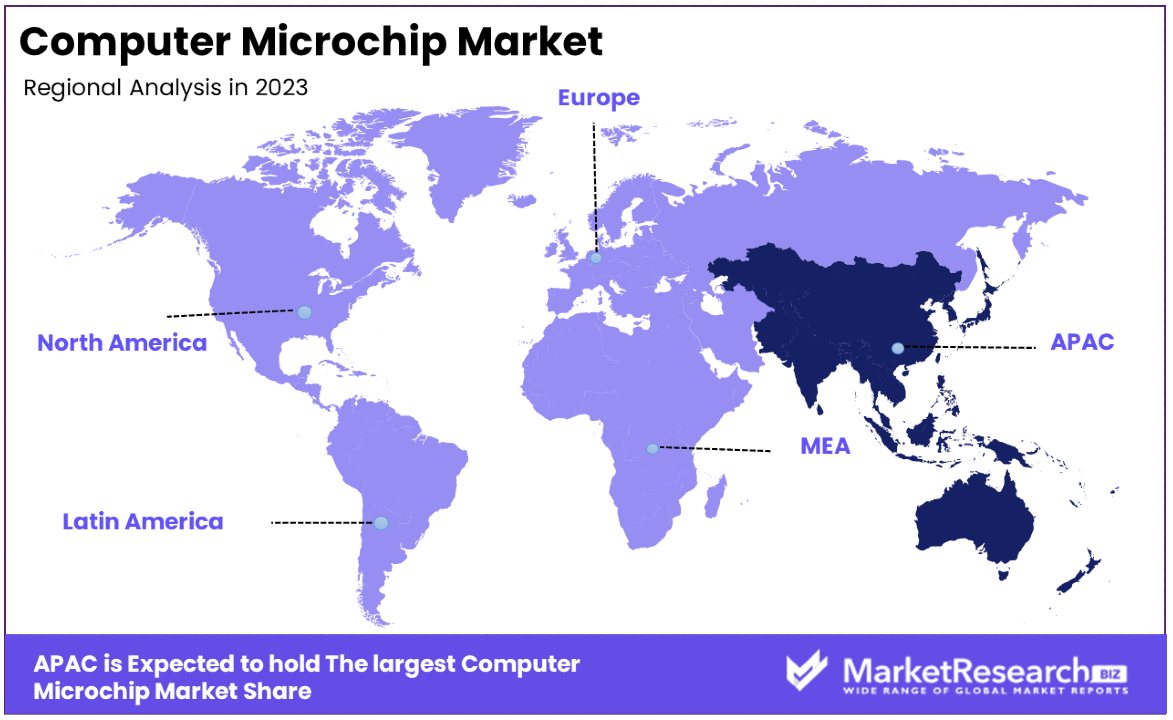

Asia Pacific Dominates with 32% Market Share

Asia Pacific's commanding 32% share of the Computer Microchip Market is no coincidence. This dominance is attributed to several key factors, including the region's robust manufacturing base, significant investments in technology and R&D, and a large, tech-savvy population that drives demand for electronic devices.

Countries like China, South Korea, and Taiwan are major chip manufacturers, hosting leading semiconductor companies and fabrication plants. The region's commitment to advancing digital infrastructure and the growing emphasis on technologies like 5G, AI, and IoT further strengthen its market position.

The Asia Pacific region benefits from a dynamic blend of advanced technological capabilities and a strong focus on innovation. This has established Asia Pacific as a critical hub for microchip production and development. The presence of major semiconductor manufacturing companies, along with government support for tech industries, plays a significant role in the market dynamics. Moreover, the region's rapid adoption of new technologies accelerates the demand for microchips, reinforcing its market dominance.

Regional Market Share Analysis:

- North America: With a market share of approximately 25%, North America remains a significant player in the microchip industry, bolstered by its strong innovation ecosystem and leading technology companies.

- Europe: Europe holds around 20% of the market share, with its strengths in automotive and industrial applications driving demand for microchips.

- Middle East & Africa: This region, while smaller in market share at about 8%, is experiencing rapid growth in technology adoption, presenting potential for future market expansion.

- Latin America: Latin America, with a market share of around 5%, is gradually increasing its presence in the microchip market, driven by digital transformation initiatives and growing tech consumption.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Computer Microchip Market, several key players exert substantial influence. Intel Corporation, AMD, NVIDIA Corporation, and Qualcomm Incorporated are among the foremost contenders, driving innovation and setting trends in electronic components.

Their strategic positioning shapes the forecast period, dictating the direction of chip manufacturing and the types of chips dominating the semiconductor industry. Demand for consumer electronics fuels their market influence, propelling semiconductor demand and necessitating advancements in silicon wafer technologies.

Companies like Broadcom Inc., MediaTek Inc., and Texas Instruments Incorporated also hold significant sway, each specializing in a distinct type of chip crucial to the industry's growth. Micron Technology, Inc., Samsung Electronics Co., Ltd., and SK hynix Inc. contribute substantially to semiconductor demand, each playing a vital role in the chip manufacturing process.

IBM Corporation, Apple Inc., NXP Semiconductors N.V., Analog Devices, Inc., and STMicroelectronics N.V. round out the landscape, each bringing unique expertise and resources to the table, further solidifying their collective dominance in the chip industry.

Market Key Players

- Intel Corporation

- Advanced Micro Devices, Inc. (AMD)

- Huawei Technologies Co., Ltd.

- Semiconductor Manufacturing International Corporation (SMIC)

- MediaTek Inc.

- HiSilicon Technologies Co., Ltd.

- Tsinghua Unigroup Co., Ltd.

- NVIDIA Corporation

- Qualcomm Incorporated

- Broadcom Inc.

- MediaTek Inc.

- Texas Instruments Incorporated

- Micron Technology, Inc.

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- IBM Corporation

- Apple Inc.

- NXP Semiconductors N.V.

- Analog Devices, Inc.

- STMicroelectronics N.V.

Recent Developments

- On March 2024, a new chip designed for AI workloads attracted $18 million in government funding, marking a significant advancement in the field of microelectronics. This innovative chip, developed based on key inventions from a lab at Princeton University, received funding from the Defense Advanced Research Projects Agency (DARPA)

- On February 2024, a computer chip integrated with human brain tissue received military funding of US$407,000 from Australia's National Intelligence and Security Discovery Research Grants program.

- On December 2023, BeagleBoard.org introduced the BeagleV-Fire, a new single-board computer that incorporates Microchip's PolarFire MPFS025T FCVG484E System on Chip (SoC) with FPGA fabric.

- On December 2022, in Phoenix, Semiconductor Manufacturing Company, a Taiwanese microchip manufacturer, announced plans to construct its first U.S. plant in Arizona. This move signifies a commitment to ensuring the well-being of workers during the construction of the plant

Report Scope

Report Features Description Market Value (2023) USD 26.3 Billion Forecast Revenue (2033) USD 64.3 Billion CAGR (2024-2033) 9.60% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type of Microchip (Central Processing Unit (CPU), Graphics Processing Unit (GPU), Memory Chips (RAM, ROM, Flash memory), Application-Specific Integrated Circuit (ASIC), Field-Programmable Gate Array (FPGA), Others), By End-Use Industry (Consumer Electronics , Automotive, Industrial, Healthcare, Aerospace and Defense, Telecommunications, Others), By Application (Data Processing, Graphics Rendering, Artificial Intelligence and Machine Learning, Networking and Connectivity, Sensor Integration, Encryption and Security, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Intel Corporation, Advanced Micro Devices, Inc. (AMD), Huawei Technologies Co., Ltd., Semiconductor Manufacturing International Corporation (SMIC), MediaTek Inc., HiSilicon Technologies Co., Ltd., Tsinghua Unigroup Co., Ltd., NVIDIA Corporation, Qualcomm Incorporated, Broadcom Inc., MediaTek Inc., Texas Instruments Incorporated, Micron Technology, Inc., Samsung Electronics Co., Ltd., SK hynix Inc., IBM Corporation, Apple Inc., NXP Semiconductors N.V., Analog Devices, Inc., STMicroelectronics N.V. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Broadcom Limited

- QUALCOMM Incorporated

- Advanced Micro Devices, Inc.

- Taiwan Semiconductor Manufacturing Company Limited

- Texas Instruments Incorporated

- NVIDIA Corporation

- United Microelectronics Corporation

- Micron Technology, Inc.

Our Clients

View Our Licence Options