Cerebral Palsy Market Report By Type of Cerebral Palsy (Spastic Cerebral Palsy, Dyskinetic (Athetoid) Cerebral Palsy, Ataxic Cerebral Palsy, Mixed Cerebral Palsy), By Clinical Presentation (Motor Disabilities, Intellectual Disabilities, Sensory Impairments, Speech and Language Disorders, Epilepsy), By Treatment Type, By End Users, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

45649

-

May 2024

-

291

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

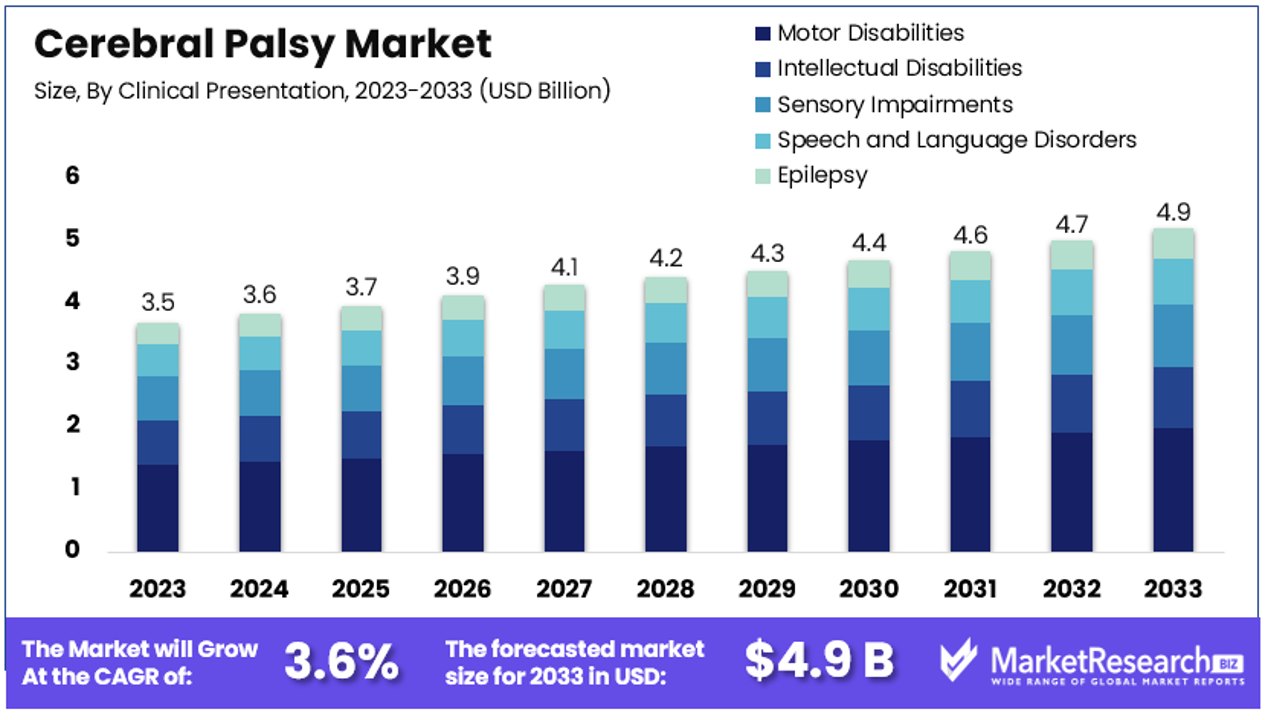

The Global Cerebral Palsy Market size is expected to be worth around USD 4.9 Billion by 2033, from USD 3.5 Billion in 2023, growing at a CAGR of 3.6% during the forecast period from 2024 to 2033.

The cerebral palsy market refers to the sector focused on medical and therapeutic services, devices, and medications catering to individuals diagnosed with cerebral palsy. This market encompasses a range of products including mobility aids, communication devices, pharmaceuticals, and therapeutic services designed to improve the quality of life for patients.

Key stakeholders include healthcare providers, medical device manufacturers, and pharmaceutical companies. The growth of this market can be attributed to advances in medical technology, increased awareness, and governmental support for disabilities. Strategic investments in research and development are crucial for companies aiming to lead in this specialized healthcare sector.

The cerebral palsy market is poised for nuanced growth, influenced by demographic trends and advancements in medical therapies. In the United States, cerebral palsy affects approximately 3 per 1,000 8-year-old children, equating to 1 in 345 children diagnosed with this condition.

This incidence rate represents a slight decrease from 3.6 per 1,000 live births in 2010, suggesting improvements in neonatal care and preventive measures. Globally, the incidence of cerebral palsy fluctuates between less than 2 to 5 babies per 1,000 live births. This variation underscores the challenge of underreporting in developing regions, where medical infrastructure may lag.

Approximately 65% of affected individuals exhibit mild to moderate disabilities, demanding solutions that enhance daily functionality and integration into society. The remaining 35% suffer from severe disabilities, necessitating more comprehensive care approaches and specialized medical and support services.

The market dynamics of the cerebral palsy sector are shaped by these epidemiological factors, driving demand for innovative medical devices, therapeutic solutions, and pharmaceuticals tailored to diverse needs. Market leaders and new entrants are prompted to invest in research and development to address the complex spectrum of disabilities associated with cerebral palsy. Additionally, the ongoing emphasis on improving quality of life for individuals with disabilities fosters a conducive environment for market growth.

Strategic partnerships between healthcare providers, non-profits, and biotech firms, along with supportive government policies, are critical for sustaining this growth. These collaborations aim to leverage technological advancements and improved care strategies to better serve this unique patient population. The cerebral palsy market, therefore, not only presents a significant opportunity for healthcare innovation but also highlights the imperative for socially responsible business practices in addressing healthcare disparities.

Key Takeaways

- Market Value: The Global Cerebral Palsy Market is projected to reach USD 4.9 billion by 2033, indicating growth from USD 3.5 billion in 2023, with a steady CAGR of 3.6% during the forecast period from 2024 to 2033.

- Type Analysis: Spastic Cerebral Palsy leads with 70-80% prevalence due to its higher visibility in clinical diagnoses, driving demand for treatments tailored to managing spasticity and improving mobility.

- Clinical Presentation Analysis: Motor Disabilities dominate with significant influence on daily functioning and quality of life, requiring immediate and ongoing treatment interventions such as physical and occupational therapies.

- Treatment Type Analysis: Physical Therapy dominates with a pivotal role in managing symptoms and enhancing mobility, influencing substantial investments in research and treatment facilities.

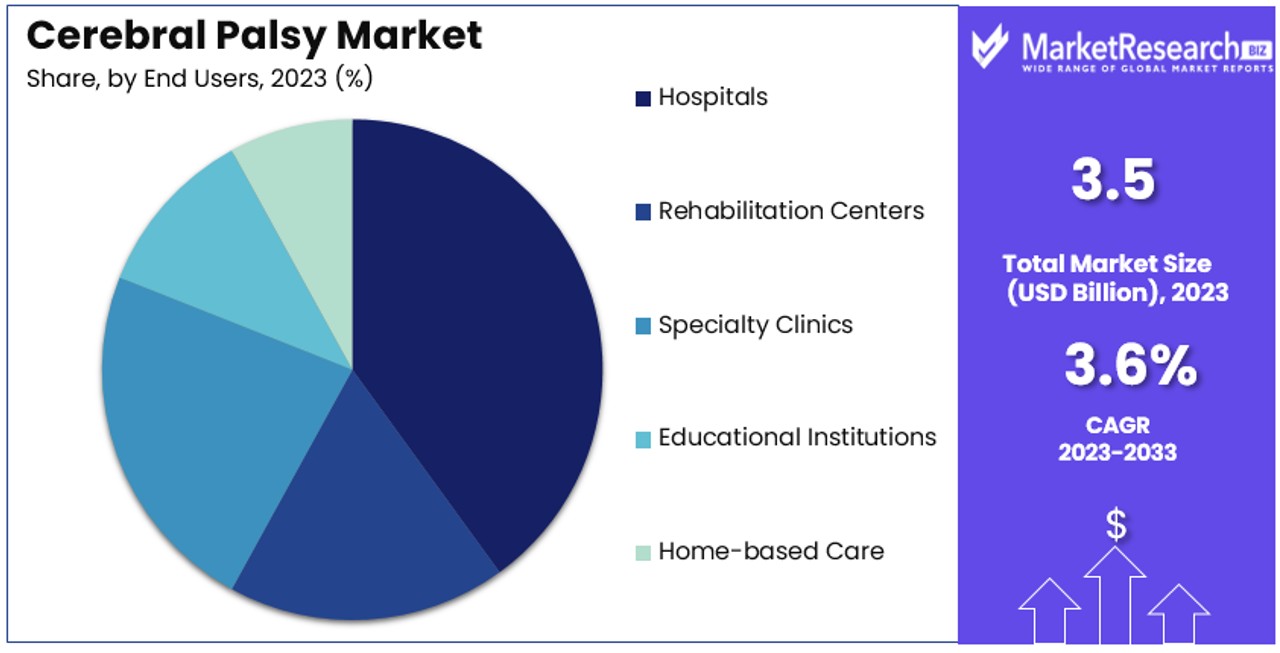

- End Users Analysis: Hospitals dominate the market due to their comprehensive care facilities and multidisciplinary treatment offerings, positioning them as critical hubs for innovation and comprehensive cerebral palsy care.

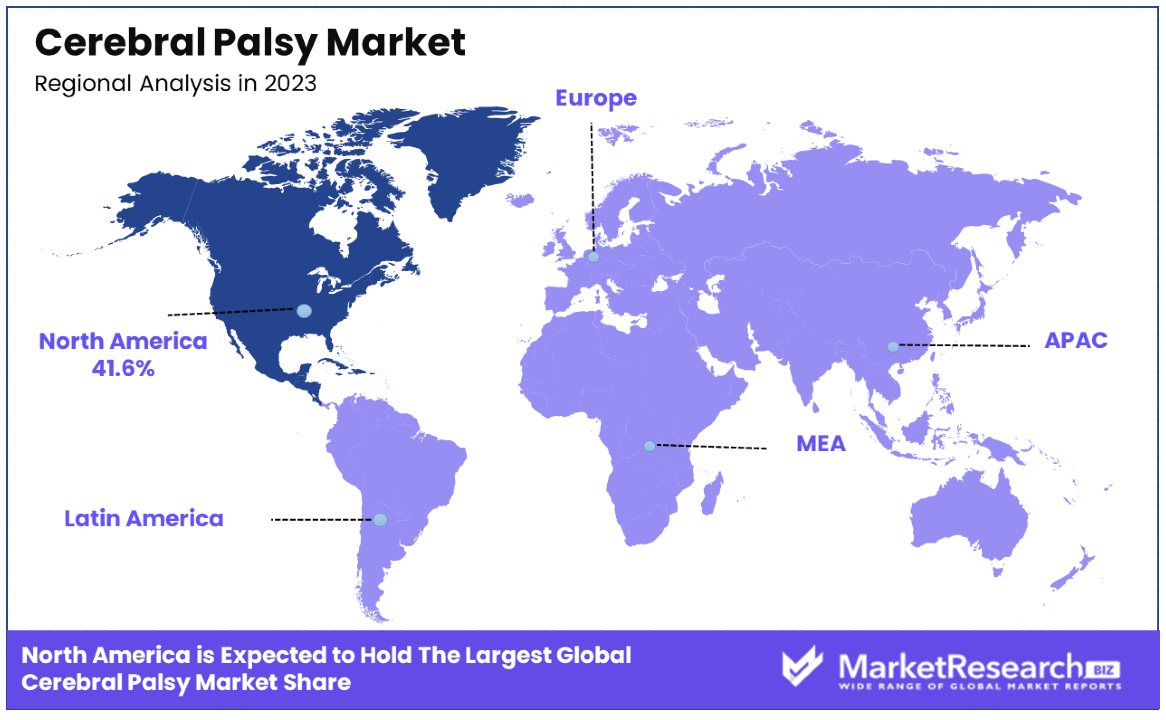

- North America: Dominates the market with a 41.6% market share, driven by advanced healthcare infrastructure and high-quality multidisciplinary care facilities.

- Europe: Holds a substantial market share of approximately 29%, benefiting from advanced healthcare systems and significant investments in research and treatment facilities.

- Analyst Viewpoint: Analysts project steady growth in the Cerebral Palsy Market, driven by increasing awareness, advancements in treatment options, and continued investments in research and development.

- Growth Opportunities: Growth opportunities lie in the development of innovative treatments tailored to specific cerebral palsy types, expansion of multidisciplinary care facilities, and integration of emerging therapies such as stem cell therapy.

Driving Factors

Increasing Prevalence of Cerebral Palsy Drives Market Growth

The rising incidence of cerebral palsy significantly fuels the expansion of the market dedicated to its management and treatment. The Centers for Disease Control and Prevention (CDC) reports that cerebral palsy affects approximately 1 in 345 children in the United States. This statistic underscores a persistent demand for medical and therapeutic services tailored to this population.

As the prevalence of conditions linked to cerebral palsy, such as complications during pregnancy, premature births, and birth injuries, continues to climb, so too does the need for specialized healthcare solutions. This increase in patient numbers directly correlates with heightened demand for existing treatments and spurs the development of new therapies and support systems. The market's growth is driven not only by the increasing number of diagnoses but also by the ongoing need for comprehensive care that these patients require throughout their lives.

Advancements in Treatment Options Drives Market Growth

Technological innovations and advances in medical research are key drivers behind the growth of the cerebral palsy market. Developments in treatment methodologies, such as stem cell therapy, robotic rehabilitation, and advanced surgical techniques, are revolutionizing the care landscape for individuals with cerebral palsy.

For instance, robotic devices like the Lokomat and Armeo are increasingly utilized to enhance mobility and daily function, demonstrating significant improvements in patient outcomes. These advancements not only expand the therapeutic possibilities but also push the market forward by increasing the efficacy and accessibility of treatments. As these technologies evolve and become more integrated into patient care plans, they attract investment and interest from healthcare providers and patients alike, further stimulating market growth.

Increasing Awareness and Early Intervention Drives Market Growth

Enhanced awareness and the push for early intervention play pivotal roles in the cerebral palsy market's expansion. Heightened public and medical awareness lead to earlier diagnoses, which is crucial for effective management of cerebral palsy. Early detection allows for the prompt initiation of treatment plans, which can substantially improve long-term outcomes for those affected. As awareness grows, so does the utilization of therapies, assistive devices, and rehabilitation services, all of which are essential for improving quality of life.

This trend not only boosts the market for specific cerebral palsy-related services and products but also fosters an environment where continual improvement in diagnostic and treatment options is demanded. Consequently, this drives ongoing development and refinement of resources, ensuring that the market not only grows but also evolves in response to the needs of patients.

Restraining Factors

High Treatment Costs Restrains Market Growth

The significant expenses associated with therapies and treatments for cerebral palsy pose a major challenge to market growth. Many advanced therapies, including new pharmacological treatments, physical therapy sessions, and cutting-edge assistive technologies, come with high costs that are often unaffordable for low-income families and economically disadvantaged regions.

This financial barrier restricts access to essential health services and innovative treatments, particularly in developing countries where health insurance coverage may be limited or non-existent. As a result, the potential market expansion is curtailed, as a large segment of the global population cannot afford these critical healthcare solutions.

Lack of Awareness and Healthcare Infrastructure Restrains Market Growth

In many parts of the world, a lack of awareness about cerebral palsy combined with insufficient healthcare infrastructure significantly hampers the market's growth. The absence of adequate awareness programs results in delayed diagnosis and treatment, which are crucial for managing the condition effectively. This is particularly evident in rural and underdeveloped regions, where healthcare facilities may not be equipped to diagnose or manage cerebral palsy appropriately.

Such limitations in healthcare provision not only affect patient outcomes but also restrict the market's expansion by preventing widespread adoption of existing treatments and technologies. These systemic issues ensure that the market does not reach its full potential, maintaining a cycle of inadequate care and limited market growth.

Type of Cerebral Palsy Analysis

Spastic Cerebral Palsy dominates with 70-80% due to its higher prevalence and visibility in clinical diagnoses.

Spastic Cerebral Palsy is the most prevalent form of the condition, accounting for approximately 70-80% of all cases. This dominance is primarily due to its distinct clinical symptoms, including muscle stiffness and impaired movement, which are more noticeable and therefore diagnosed more frequently than other types. This sub-segment significantly influences the cerebral palsy market's dynamics by driving demand for specific treatments and therapies designed to manage spasticity and improve mobility.

The treatments often include muscle relaxants, physical therapy, and in some cases, surgical interventions to reduce muscle tightness. This market segment's substantial size compels healthcare providers and pharmaceutical companies to focus heavily on developing and refining treatments that cater specifically to this group. Other types, such as Dyskinetic (Athetoid) Cerebral Palsy, Ataxic Cerebral Palsy, and Mixed Cerebral Palsy, also contribute to the market but to a lesser extent. These forms require distinct therapeutic approaches, which diversifies the market offerings but places them as smaller segments compared to spastic type.

Clinical Presentation Analysis

Motor Disabilities dominate with significant influence due to their direct impact on daily functioning and quality of life.

Motor disabilities are the most pronounced clinical presentation in the cerebral palsy market, affecting the majority of individuals diagnosed with the condition. This segment's dominance is driven by the visibility of physical symptoms that require immediate and ongoing treatment, which significantly impacts the demand for physical and occupational therapies.

Motor impairments necessitate a range of interventions from assistive devices like wheelchairs and orthoses to specialized surgeries, which form a substantial part of the market. Intellectual disabilities, sensory impairments, speech and language disorders, and epilepsy are also critical segments that require dedicated services and treatments. However, the pervasive impact of motor disabilities on a patient's autonomy and quality of life makes it the primary driver of healthcare utilization and market growth in cerebral palsy care, underscoring the need for innovative treatment solutions in this area.

Treatment Type Analysis

Physical Therapy dominates with a pivotal role due to its foundational importance in managing symptoms and enhancing mobility.

Physical therapy represents a cornerstone treatment in the cerebral palsy market, crucial for nearly all patients to some degree. This dominance is based on the therapy's ability to improve mobility, reduce pain, and increase independence. As a foundational approach in managing cerebral palsy, physical therapy influences substantial investments in research and treatment facilities tailored to enhancing motor functions.

Other treatment types, such as occupational therapy, speech therapy, and the use of medications like muscle relaxants and anticonvulsants, also play essential roles but are often adjunct to the primary physical treatment protocols. Surgical interventions and assistive devices constitute significant sub-segments, providing critical support for severe cases, whereas emerging treatments like stem cell therapy offer promising future prospects. However, the ubiquity and immediate necessity of physical therapy make it the largest and most influential segment in treatment types.

End Users Analysis

Hospitals dominate due to their comprehensive care facilities and ability to offer multidisciplinary treatments for cerebral palsy.

Hospitals are the primary end-users in the cerebral palsy market, primarily due to their capacity to provide comprehensive and multidisciplinary care. This segment's dominance is facilitated by the availability of specialized staff and advanced medical equipment necessary for diagnosing and treating various aspects of cerebral palsy.

Rehabilitation centers, specialty clinics, schools/educational institutions, and home-based care also represent significant segments within the market. Each offers unique contributions to managing cerebral palsy, such as specialized therapies and educational support. However, the central role that hospitals play in acute care and severe cases, along with their ability to offer surgical treatments and emergency care, places them at the forefront of the market. This positioning is likely to remain as they continue to serve as critical hubs for innovation and comprehensive treatment approaches in cerebral palsy care.

Key Market Segments

By Type of Cerebral Palsy

- Spastic Cerebral Palsy

- Dyskinetic (Athetoid) Cerebral Palsy

- Ataxic Cerebral Palsy

- Mixed Cerebral Palsy

By Clinical Presentation

- Motor Disabilities

- Intellectual Disabilities

- Sensory Impairments

- Speech and Language Disorders

- Epilepsy

By Treatment Type

- Physical Therapy

- Occupational Therapy

- Speech Therapy

- Medications (Muscle Relaxants, Anticonvulsants)

- Surgical Interventions (Orthopedic Surgeries, Neurosurgical Procedures)

- Assistive Devices (Orthoses, Wheelchairs)

- Stem Cell Therapy

- Others

By End Users

- Hospitals

- Rehabilitation Centers

- Specialty Clinics

- Schools/Educational Institutions

- Home-based Care

Growth Opportunities

Developing New Assistive Technologies Offers Growth Opportunity

The ongoing development of new assistive technologies represents a substantial growth opportunity within the cerebral palsy market. Innovations such as advanced exoskeletons, robotic limbs, and brain-computer interfaces are poised to significantly enhance mobility, communication, and daily living independence for individuals with cerebral palsy.

These technologies not only aim to improve the quality of life but also integrate cutting-edge engineering and software solutions, making daily tasks more manageable and less reliant on human assistance. The potential market for such devices is expanding as awareness and accessibility increase, driving investment and research in technologically advanced solutions that cater to the specific challenges faced by this population.

Personalized and Precision Medicine Approaches Offer Growth Opportunity

The integration of personalized and precision medicine into the cerebral palsy treatment landscape offers a promising growth avenue. This approach utilizes genomics, biomarkers, and advanced diagnostic tools to tailor treatments specifically to individual patient profiles, enhancing the efficacy of therapeutic interventions.

By focusing on the unique genetic and physiological characteristics of each patient, healthcare providers can optimize treatment plans, potentially leading to more successful outcomes and fewer side effects. This precision in treatment not only promises better care but also stimulates further research and development in the field, attracting funding and interest from biotech and pharmaceutical companies looking to lead in innovative, patient-centered solutions.

Trending Factors

Telehealth and Remote Monitoring Solutions Are Trending Factors

The rapid growth in the adoption of telehealth and remote monitoring solutions marks a significant trend in the Cerebral Palsy Market. These technologies facilitate healthcare providers in delivering continuous, real-time healthcare support to patients, regardless of geographical limitations. By enabling virtual consultations and remote patient monitoring, these tools significantly reduce the need for frequent hospital visits, easing the logistical burden on patients and their families.

This trend is especially crucial in improving access to specialized neurological and rehabilitative care, which might not be readily available in many regions. As telehealth technology advances, its integration into patient care plans is expected to increase, thereby broadening the market's reach and enhancing the continuity of care.

Regenerative Medicine and Stem Cell Therapy Are Trending Factors

Regenerative medicine and stem cell therapy have emerged as prominent trending factors within the Cerebral Palsy Market. These innovative treatments focus on repairing or replacing damaged tissues and cells, offering the potential for substantial improvements in motor functions and cognitive abilities. Recent advancements and successful case studies have increased both public interest and clinical research in these therapies.

As evidence of their effectiveness grows, so does their acceptance among healthcare providers and patients, leading to increased investment and exploration in regenerative approaches. This trend is not only reshaping treatment paradigms but also driving market growth through the development of new therapeutic options that could fundamentally change the management of cerebral palsy.

Regional Analysis

North America Dominates with 41.6% Market Share

North America’s significant market share in the Cerebral Palsy Market can be attributed to advanced healthcare infrastructure, a strong focus on research and development, and high healthcare spending per capita. The region benefits from widespread awareness of cerebral palsy and a robust framework for early diagnosis and intervention. Additionally, North America houses numerous leading companies specializing in neurological disorders, which actively invest in innovative treatments and technologies.

The regional dynamics of North America are shaped by its comprehensive healthcare policies and initiatives aimed at supporting individuals with disabilities. This includes government funding for healthcare services and special education programs that integrate medical support with patient education, further fostering an environment conducive to market growth.

North America is expected to maintain its dominance in the Cerebral Palsy Market due to ongoing advancements in medical technology and strong policy support. The continued focus on personalized medicine and regenerative treatments is likely to further enhance its market position, driving future growth and innovation.

Regional Market Shares:

- Europe: Holding a market share of approximately 29%, Europe stands strong due to its excellent healthcare systems and significant government support for research and treatment of neurological conditions.

- Asia Pacific: This region accounts for about 18% of the market, driven by increasing healthcare expenditure and rapidly developing healthcare infrastructure.

- Middle East & Africa: With a smaller share of around 7%, this region's market is growing due to rising awareness and improving health services.

- Latin America: Also holding around 5%, Latin America’s market is gradually expanding with improving healthcare policies and increasing access to treatment facilities.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The cerebral palsy market is poised for substantial growth during the forecast period, driven by increasing development activities and product launches aimed at addressing various disease types. Major players in this market are strategically positioned to capitalize on this growth and exert significant influence.

In this competitive landscape, several key factors contribute to the strategic positioning of major players. Pfizer Inc., Teva Pharmaceutical Industries Ltd., and AbbVie Inc. are among the major players with a substantial market share. These companies have been actively engaged in the development of novel treatments and therapies, driving the cerebral palsy treatment market growth.

GlaxoSmithKline Plc and Bayer AG also play a significant role in shaping the market landscape. Their expertise in anti-inflammatories and other therapeutic areas positions them as key contributors to the market's expansion.

Furthermore, Emanuel Cleaver, Brian Fitzpatrick, and other notable players such as Rohto Pharmaceutical and Supernus Pharmaceuticals have been instrumental in introducing innovative treatment approaches and expanding market reach.

Acorda Therapeutics, Inc., Tris Pharma, Inc., and Takeda Pharmaceutical Company Limited are among the major players focusing on addressing specific disease types within the cerebral palsy spectrum. Their targeted therapies cater to the diverse needs of patients, further driving market growth.

Sun Pharmaceutical Industries Ltd., Biogen Inc., and Bristol-Myers Squibb Company also hold a significant share in the market, leveraging their expertise in drug development and commercialization to drive innovation and market expansion.

Overall, the cerebral palsy market is characterized by intense competition and dynamic growth fueled by the collective efforts of these major players. Their strategic positioning, innovative product offerings, and proactive development activities are expected to drive significant market expansion during the forecast period.

Market Key Players

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- AbbVie Inc.

- GlaxoSmithKline Plc

- Bayer AG

- Emanuel Cleaver

- Brian Fitzpatrick

- Rohto Pharmaceutical

- Supernus Pharmaceuticals

- Acorda Therapeutics

- Tris Pharma, Inc.

- Takeda Pharmaceutical Company Limited

- Sun Pharmaceutical Industries Ltd.

- Biogen Inc.

- Bristol-Myers Squibb Company

- Sanofi SA

- Acorda Therapeutics, Inc.

- Hikma Pharmaceuticals PLC

- Cellular Biomedicine Group

- Allergen Plc

Recent Developments

- On April 2024, SpineX announced positive results from a first-in-human study using its electrical neuromodulation device in a 60-year-old woman with cerebral palsy. The patient experienced significant functional improvements after eight weeks of SpineX’s SCiP therapy, including a 14.2-point increase in gross motor function, achieving a Minimal Clinically Important Difference (MCID) score of five points. Activities like kneeling, sitting, and walking improved, with sustained motor enhancement at the 20-week follow-up post-therapy.

- On September 2023, MIT engineers introduced a pose-mapping technique to remotely evaluate motor function in patients with cerebral palsy. By analyzing videos of over 1,000 children with cerebral palsy, this method uses computer vision and machine-learning to compute a clinical score based on detected pose patterns. The technique demonstrated over 70% accuracy in matching clinical scores assigned during in-person assessments, offering a potential solution to reduce the burden of frequent in-person evaluations for children with cerebral palsy.

Report Scope

Report Features Description Market Value (2023) USD 3.5 Billion Forecast Revenue (2033) USD 4.9 Billion CAGR (2024-2033) 3.60% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type of Cerebral Palsy (Spastic Cerebral Palsy, Dyskinetic (Athetoid) Cerebral Palsy, Ataxic Cerebral Palsy, Mixed Cerebral Palsy), By Clinical Presentation (Motor Disabilities, Intellectual Disabilities, Sensory Impairments, Speech and Language Disorders, Epilepsy), By Treatment Type (Physical Therapy, Occupational Therapy, Speech Therapy, Medications (Muscle Relaxants, Anticonvulsants), Surgical Interventions (Orthopedic Surgeries, Neurosurgical Procedures), Assistive Devices (Orthoses, Wheelchairs), Stem Cell Therapy, Others), By End Users (Hospitals, Rehabilitation Centers, Specialty Clinics, Schools/Educational Institutions, Home-based Care) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Pfizer Inc., Teva Pharmaceutical Industries Ltd., AbbVie Inc., GlaxoSmithKline Plc, Bayer AG, Emanuel Cleaver, Brian Fitzpatrick, Rohto Pharmaceutical, Supernus Pharmaceuticals, Acorda Therapeutics, Tris Pharma, Inc., Takeda Pharmaceutical Company Limited, Sun Pharmaceutical Industries Ltd., Biogen Inc., Bristol-Myers Squibb Company, Sanofi SA, Acorda Therapeutics, Inc., Hikma Pharmaceuticals PLC, Cellular Biomedicine Group, Allergen Plc Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- AbbVie Inc.

- GlaxoSmithKline Plc

- Bayer AG

- Emanuel Cleaver

- Brian Fitzpatrick

- Rohto Pharmaceutical

- Supernus Pharmaceuticals

- Acorda Therapeutics

- Tris Pharma, Inc.

- Takeda Pharmaceutical Company Limited

- Sun Pharmaceutical Industries Ltd.

- Biogen Inc.

- Bristol-Myers Squibb Company

- Sanofi SA

- Acorda Therapeutics, Inc.

- Hikma Pharmaceuticals PLC

- Cellular Biomedicine Group

- Allergen Plc

Our Clients

View Our Licence Options