Medical Robots Market By Type (Equipment, Service, Consumables), By Product (Surgical Robots, Rehabilitation Robots, Noninvasive Radiosurgery Robots, Hospital and Pharmacy Robots, Others), By Application (Neurology, Oncology, Orthopedic Robotic Systems, Laparoscopy, Cardiology, Others), By Setting (Home-Care, In-Patient, Out-Patient), By End User (Hospitals & Clinics, Specialty Centers, Rehabilitation Centers, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

2214

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

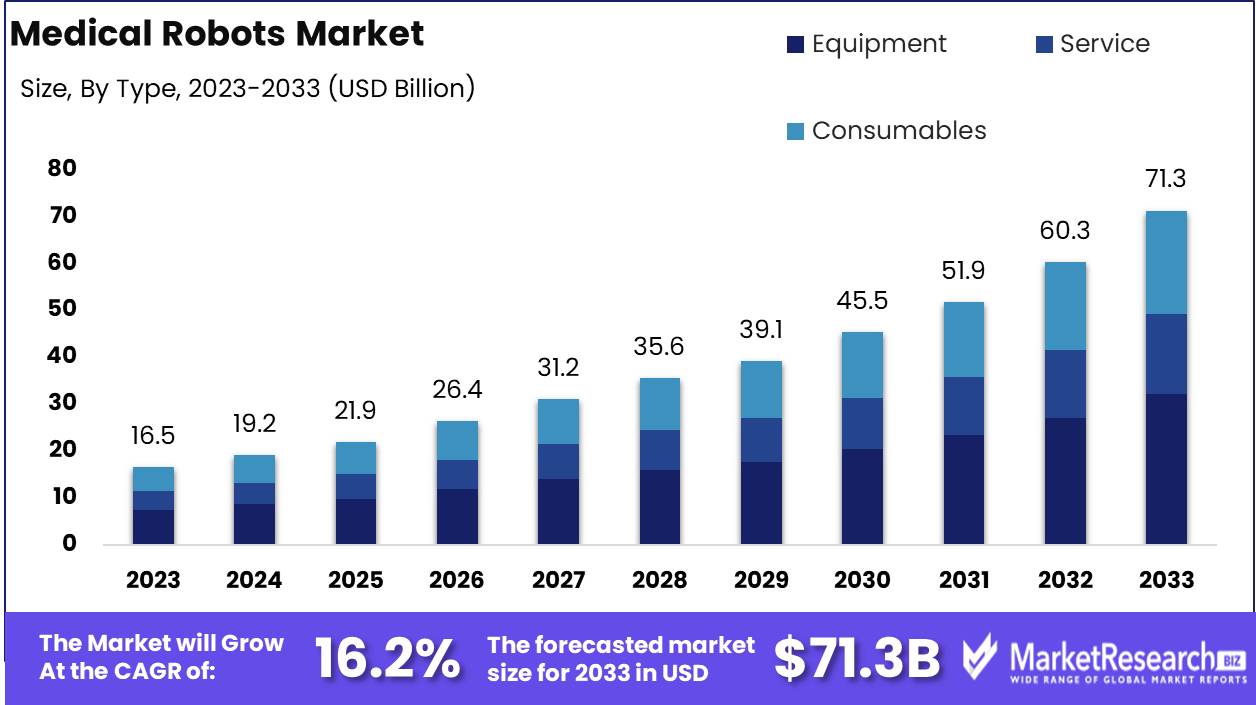

The Medical Robots Market was valued at USD 16.5 billion in 2023. It is expected to reach USD 71.3 billion by 2033, with a CAGR of 16.2% during the forecast period from 2024 to 2033.

The Medical Robots Market encompasses the development and deployment of robotic systems designed to assist in various medical procedures, including surgery, rehabilitation, and diagnostics. These advanced robots enhance precision, efficiency, and safety in healthcare delivery. Key segments include surgical robots, rehabilitation robots, and hospital logistics robots. Innovations in artificial intelligence, machine learning, and sensor technology drive market growth, enabling robots to perform complex tasks with minimal human intervention.

The Medical Robots Market is poised for substantial growth, driven by advancements in AI and machine learning, which are integrating into robotic systems to enhance innovation and efficiency. These technologies are not only revolutionizing traditional surgical procedures but are also expanding the capabilities of medical robots to include telemedicine and remote surgery. This expansion is particularly beneficial for remote and underserved areas, where access to specialized medical care is limited. The integration of 3D printing and customization further accelerates the development and usage of personalized robotic systems, catering to individual patient needs and improving clinical outcomes.

However, the market faces significant challenges. High costs remain a major barrier to widespread adoption, especially in developing regions where healthcare budgets are constrained. Additionally, the regulatory landscape presents substantial hurdles. Stringent regulations and lengthy approval processes can delay the market entry of new products, impeding innovation and market growth.

Despite these challenges, the market's potential is underscored by the continuous advancements in technology and the increasing demand for minimally invasive surgeries. Companies investing in overcoming these barriers are likely to benefit from the expanding opportunities in the Medical Robots Market, positioning themselves at the forefront of this transformative industry.

Key Takeaways

- Market Growth: The Medical Robots Market was valued at USD 16.5 billion in 2023. It is expected to reach USD 71.3 billion by 2033, with a CAGR of 16.2% during the forecast period from 2024 to 2033.

- By Type: Equipment dominated the Medical Robots Market's By Type segment.

- By Product: Surgical Robots dominated the diverse Medical Robots Market segments.

- By Application: Neurology dominated the Medical Robots Market by application.

- By Setting: Home care dominated the Medical Robots Market by setting.

- By End User: Hospitals and clinics dominate the Medical Robots Market by end user.

- Regional Dominance: North America dominates the medical robots market with a 40% largest share.

- Growth Opportunity: The global medical robots market is set to capitalize on significant growth opportunities driven by advancements in surgical and rehabilitation robotics.

Driving factors

Minimizing Medication Errors as a Catalyst for Market Growth

The growing need to minimize medication errors is a significant driving factor in the Medical Robots Market. Medication errors can have severe consequences, including increased patient morbidity and mortality, which places a considerable burden on healthcare systems. Medical robots, particularly robotic-assisted dispensing systems, and automated medication management solutions, are designed to enhance precision and accuracy in medication delivery. These technologies reduce human error, ensuring that patients receive the correct medication and dosage.

According to the report, medication errors harm at least 1.5 million people annually in the United States alone. The implementation of medical robots can significantly reduce this number, thereby improving patient outcomes and lowering healthcare costs. This growing emphasis on patient safety and error reduction is driving the adoption of medical robots in hospitals and other healthcare facilities, contributing to market growth.

Rising Demand for Minimally Invasive Procedures Driving Adoption

The increasing demand for minimally invasive procedures (MIPs) is another critical factor propelling the growth of the Medical Robots Market. MIPs, which include laparoscopic and robotic-assisted surgeries, offer numerous advantages over traditional open surgeries, such as reduced pain, smaller incisions, shorter hospital stays, and faster recovery times. Medical robots play a pivotal role in enhancing the precision and control of surgeons during these procedures. For instance, the da Vinci Surgical System, a widely recognized robotic platform, enables surgeons to perform complex surgeries with greater accuracy and minimal invasiveness.

A study reported that robotic-assisted surgeries have a 52% lower complication rate than open surgeries. This increased efficacy and patient preference for MIPs drives the demand for medical robots, thus fueling market expansion.

Technological Advancements in AI and Robotics Revolutionizing Healthcare

Advancements in artificial intelligence (AI) and robotic technology are revolutionizing the Medical Robots Market. AI integration enhances the capabilities of medical robots by enabling them to learn from data, make informed decisions, and perform complex tasks with high precision. AI-driven medical robots can assist in various applications, including surgery, diagnostics, and patient care. For example, AI algorithms can analyze vast amounts of medical data to assist robots in making accurate diagnoses or planning surgical procedures.

Additionally, innovations in robotics technology, such as improved sensors, enhanced mobility, and greater dexterity, are expanding the functionalities and applications of medical robots. According to a report, the AI in healthcare market is expected to grow from $6.6 billion in 2020 to $45.2 billion by 2026, reflecting a compound annual growth rate (CAGR) of 44.9%. This rapid technological progress drives the adoption of advanced medical robots, thus accelerating market growth.

Restraining Factors

High Costs of Implementation and Maintenance: A Significant Barrier to Market Expansion

The high costs associated with the implementation and maintenance of medical robots represent a substantial barrier to the growth of the Medical robot market. The initial investment required for acquiring advanced robotic systems, coupled with the ongoing expenses for their maintenance, can be prohibitive for many healthcare facilities, particularly smaller hospitals and clinics. This financial burden is exacerbated by the need for specialized training for medical staff, further increasing operational costs.

According to industry reports, the cost of acquiring a surgical robot can range from $1 million to $2.5 million, with annual maintenance costs reaching up to $150,000. These financial challenges can deter potential adopters and slow the overall market growth, as the return on investment may not be immediately apparent to healthcare providers.

Lack of Standardization and Regulation: Hindering Widespread Adoption

The absence of standardization and regulation within the Medical Robots Market creates significant uncertainty and complexity, which can impede market growth. The lack of consistent standards and regulatory frameworks leads to variability in the quality and performance of medical robots, raising concerns among healthcare providers regarding safety and efficacy. This inconsistency can result in delays in regulatory approvals, as each new system may require extensive evaluation and testing to meet diverse regulatory requirements across different regions.

Additionally, the absence of standardized protocols for training and operation can lead to inefficiencies and increased risks during medical procedures. These regulatory and standardization challenges not only slow the pace of technological advancement and innovation but also contribute to a cautious approach among potential adopters, thereby restraining the market's growth potential.

By Type Analysis

In 2023, Equipment dominated the Medical Robots Market's By Type segment.

In 2023, Equipment held a dominant market position in the By Type segment of the Medical Robots Market. This segment includes a wide range of advanced robotic systems used in various medical applications such as surgery, rehabilitation, and patient care. The significant market share of the Equipment segment can be attributed to the increasing adoption of robotic-assisted surgical procedures, which offer enhanced precision, minimal invasiveness, and faster recovery times. Additionally, technological advancements and the integration of AI and machine learning in medical robots have further fueled the demand for sophisticated equipment.

The Service segment, encompassing maintenance, training, and software updates, also witnessed notable growth due to the rising need for continuous support and optimization of robotic systems. The Consumables segment, which includes disposable items used in robotic procedures, experienced steady demand driven by the increasing volume of robotic surgeries and the necessity for sterile, single-use products. Overall, the robust performance of these segments reflects the growing reliance on medical robots to improve patient outcomes and operational efficiency in healthcare settings.

By Product Analysis

In 2023, Surgical Robots dominated the diverse Medical Robots Market segments.

In 2023, Surgical Robots held a dominant market position in the By Product segment of the Medical Robots Market. This segment includes a variety of advanced robotic systems designed for performing minimally invasive surgeries with high precision and control. Surgical Robots accounted for the largest share due to their widespread adoption in procedures such as prostatectomy, hysterectomy, and cardiac surgery, driven by benefits like reduced recovery times and minimized surgical risks.

Rehabilitation Robots, which assist patients in recovering motor functions post-stroke or injury, also showed significant growth. These robots are increasingly used in physical therapy, offering repetitive, task-specific training that enhances patient outcomes. Noninvasive Radiosurgery Robots, used for precise tumor targeting in cancer treatments without incisions, are gaining traction due to their noninvasive nature and efficacy in treating complex conditions.

Hospital and Pharmacy Robots, which automate tasks such as medication dispensing and supply chain management, contributed notably to market growth by improving efficiency and reducing human error in hospital settings. This segment's rise is attributed to the increasing need for streamlined operations in healthcare facilities.

Lastly, the Others category, encompassing various emerging robotic technologies for different medical applications, saw steady growth as innovation continues to expand the capabilities and applications of medical robots. Collectively, these segments illustrate the diverse and rapidly evolving landscape of the Medical Robots Market.

By Application Analysis

In 2023, Neurology dominated the Medical Robots Market by application.

In 2023, Neurology held a dominant market position in the "By Application" segment of the Medical Robots Market. The extensive use of robotic systems in neurological procedures, due to their precision and minimally invasive nature, significantly contributed to this dominance. Oncology applications also witnessed considerable growth, driven by the increasing adoption of robotic systems for complex cancer surgeries, enhancing patient outcomes and recovery times. Orthopedic Robotic Systems emerged as a crucial segment, propelled by advancements in robotic-assisted joint replacement surgeries, which offer higher accuracy and improved post-operative results.

Laparoscopy, another vital application area, experienced substantial market penetration due to the widespread use of robotic systems in minimally invasive abdominal surgeries. This trend is attributed to the benefits of reduced patient recovery times and enhanced surgical precision. Cardiology also showcased significant potential, with robotic-assisted cardiac surgeries gaining traction for their precision and ability to handle intricate cardiovascular procedures.

Additionally, the "Others" category, encompassing various miscellaneous medical applications, demonstrated a steady market presence. This category includes robotic systems used in urology, gynecology, and general surgery, reflecting a broadening scope of robotic applications in the medical field.

By Setting Analysis

In 2023, Home Care dominated the Medical Robots Market by setting.

In 2023, Home-Care held a dominant market position in the By Setting segment of the Medical Robots Market. This dominance can be attributed to the increasing demand for personalized and efficient home-based healthcare solutions, driven by an aging population and the rising prevalence of chronic diseases. The shift towards home care is supported by advancements in robotic technology, which enable precise and minimally invasive procedures that can be conducted in the comfort of patients' homes. Additionally, home-care medical robots have proven to enhance patient outcomes, reduce hospital readmissions, and lower overall healthcare costs.

In contrast, the In-Patient and Out-Patient segments have experienced moderate growth. In-patient settings benefit from high-tech robotic surgical systems that enhance the precision of complex procedures, while Outpatient settings utilize medical robots for diagnostic and therapeutic purposes, improving operational efficiency. However, the high costs and infrastructure requirements associated with these technologies have limited their expansion compared to the home care segment.

By End User Analysis

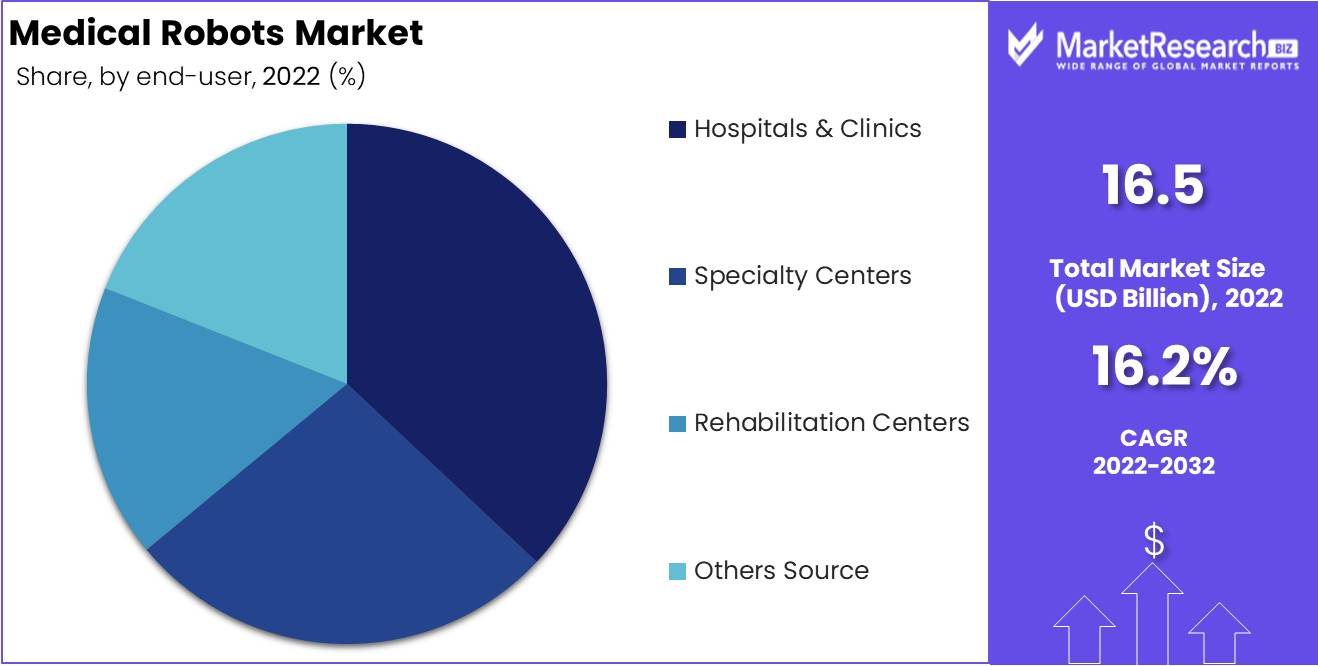

Hospitals and clinics dominate the Medical Robots Market by end users.

In 2023, Hospitals & Clinics held a dominant market position in the By End User segment of the Medical Robots Market. This segment benefits significantly from the widespread adoption of robotic-assisted surgeries and advanced medical robotic systems for various complex procedures. Hospitals and clinics leverage these technologies to improve surgical precision, reduce recovery times, and enhance patient outcomes, thereby driving market dominance.

Specialty Centers represent another crucial segment, focusing on specific medical disciplines such as orthopedics, neurology, and cardiology. These centers utilize specialized robotic systems tailored to their unique requirements, contributing to their growing market share.

Rehabilitation Centers are increasingly incorporating medical robots to enhance physical therapy and rehabilitation processes. Robots in these settings assist in patient mobility training and repetitive task exercises, ensuring consistent and efficient therapy, which supports their market presence.

The Others segment, encompassing a variety of healthcare facilities and applications, also plays a role in the market. This segment includes research institutions and outpatient care centers that employ medical robots for diverse purposes, ranging from diagnostic procedures to experimental treatments.

Key Market Segments

By Type

- Equipment

- Service

- Consumables

By Product

- Surgical Robots

- Rehabilitation Robots

- Noninvasive Radiosurgery Robots

- Hospital and Pharmacy Robots

- Others

By Application

- Neurology

- Oncology

- Orthopedic Robotic Systems

- Laparoscopy

- Cardiology

- Others

By Setting

- Home-Care

- In-Patient

- Out-Patient

By End User

- Hospitals & Clinics

- Specialty Centers

- Rehabilitation Centers

- Others Source

Growth Opportunity

Surgical Robotics Advancements

The global medical robots market is poised for significant growth, driven by advancements in surgical robotics. Technological innovations are enhancing the precision, efficiency, and outcomes of surgical procedures. Companies are investing heavily in R&D to develop next-generation robotic systems that offer minimally invasive solutions. These systems are designed to reduce patient recovery time, minimize surgical complications, and improve overall patient care. The increasing adoption of these advanced surgical robots by healthcare institutions worldwide presents a substantial growth opportunity. The market is expected to benefit from the integration of artificial intelligence and machine learning, which will further refine surgical precision and automate complex procedures.

Rehabilitation Robotics Expansion

Another promising area within the medical robots market is rehabilitation robotics. As the global population ages, the demand for effective rehabilitation solutions is rising. Rehabilitation robots are playing a critical role in providing personalized therapy, enhancing patient mobility, and accelerating recovery processes. These robots offer tailored exercises and real-time feedback, which are crucial for patients recovering from strokes, injuries, and surgeries. The expansion of rehabilitation robotics is supported by increased investments in healthcare infrastructure and a growing awareness of the benefits of robotic-assisted rehabilitation. This segment is anticipated to witness robust growth, driven by technological advancements and an increasing focus on improving patient outcomes.

Latest Trends

Surgical Robotics Advancements

The medical robots market is anticipated to witness substantial growth, driven by significant advancements in surgical robotics. Innovations in robotic-assisted surgery are enhancing precision, reducing recovery times, and improving patient outcomes. The integration of high-definition 3D visualization, real-time imaging, and haptic feedback in surgical robots is enabling surgeons to perform complex procedures with greater accuracy. Moreover, the development of minimally invasive surgical robots is expanding the scope of robotic surgery to a broader range of medical fields, including orthopedics, neurosurgery, and cardiovascular surgery. This trend is expected to contribute to increased adoption of surgical robots in hospitals and surgical centers worldwide.

AI Integration in Surgical Robots

The integration of artificial intelligence (AI) into surgical robots represents a pivotal trend. AI algorithms are enhancing the capabilities of surgical robots by providing advanced analytics, real-time decision support, and predictive insights. Machine learning models are being utilized to improve surgical planning, optimize intraoperative navigation, and predict potential complications. AI-driven robotic systems are also facilitating personalized surgery by analyzing patient-specific data and tailoring surgical approaches accordingly. This integration is expected to reduce surgical errors, enhance procedural efficiency, and improve patient safety. As AI technology continues to evolve, it is anticipated that the synergy between AI and surgical robotics will revolutionize the medical field, setting new standards for precision and outcomes in surgery.

Regional Analysis

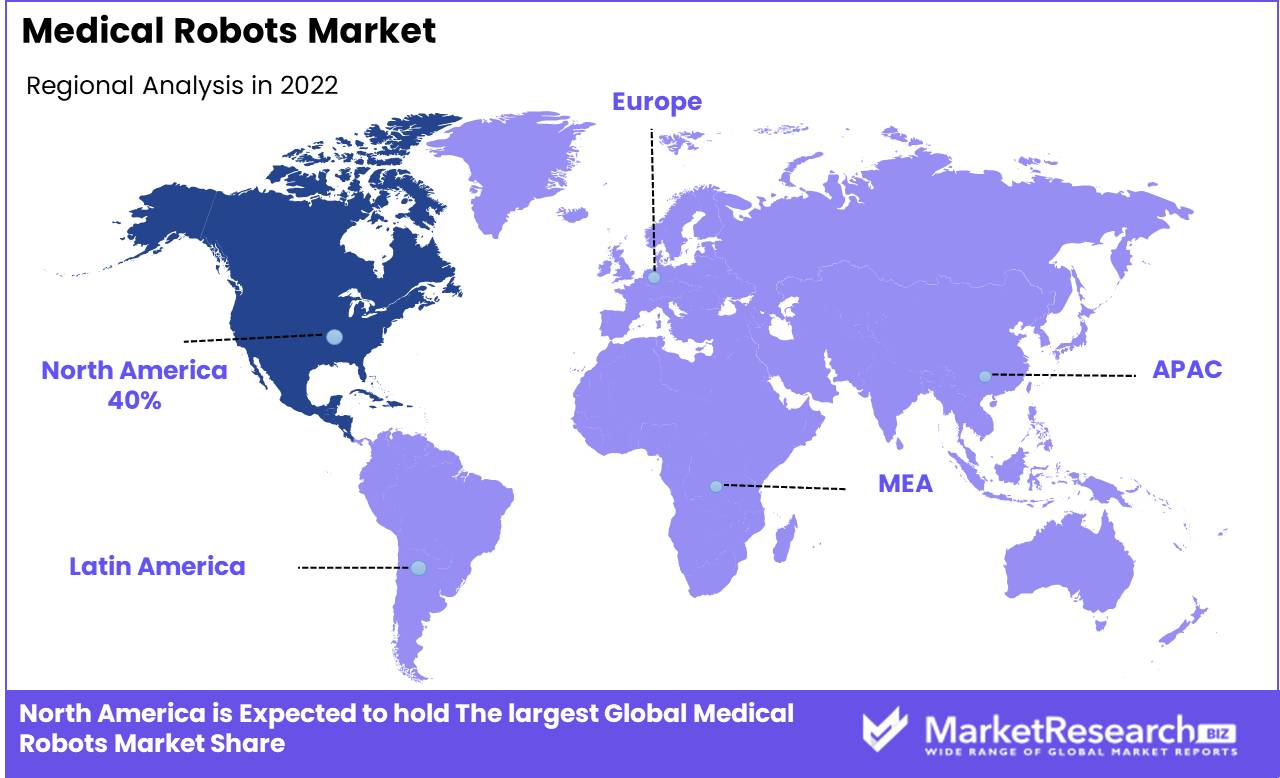

North America dominates the medical robots market with a 40% largest share.

The medical robots market demonstrates significant regional variation in growth and adoption across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. North America dominates the market, capturing a substantial percentage share due to advanced healthcare infrastructure, high adoption rates of robotic systems in hospitals, and significant investments in healthcare technology. Specifically, North America accounts for approximately 40% of the global market share, driven by the presence of key players and increasing demand for minimally invasive surgeries.

Europe follows, with a market share of around 30%, propelled by supportive government policies and a growing aging population necessitating advanced medical interventions. The Asia Pacific region is experiencing rapid growth, with a market share nearing 20%, attributed to rising healthcare expenditure, improving healthcare infrastructure, and increasing awareness and adoption of robotic surgeries in countries like Japan, China, and India.

The Middle East & Africa and Latin America regions collectively hold the remaining market share, with incremental growth expected due to gradual advancements in healthcare facilities and increasing medical tourism. However, these regions face challenges such as limited access to advanced medical technologies and financial constraints, impacting the overall market penetration.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global medical robots market is poised for significant advancements, with key players driving innovation and market expansion. iRobot Corporation, traditionally known for consumer robotics, is expected to make strategic moves into medical applications, leveraging its technological expertise to enhance robotic-assisted surgeries. Medrobotics Corporation and Titan Medical Inc. are anticipated to push boundaries with their flexible robotic systems, designed to provide minimally invasive solutions, thus improving patient outcomes and reducing recovery times.

Renishaw Plc and Health Robotics SLR will likely continue their focus on precision and automation in surgical procedures and pharmaceutical preparation, respectively. OR Productivity plc's innovations in efficiency and cost-effectiveness are expected to resonate well with healthcare providers seeking value-driven solutions.

Intuitive Surgical remains a dominant force, renowned for its da Vinci Surgical System, which continues to set benchmarks in robotic surgery. Mako Surgical Corp. and Mazor Robotics, both under the Stryker umbrella, are expected to advance in orthopedics and spinal surgery, bolstering Stryker’s leadership in these segments.

Varian Medical Systems and Stereotaxis Inc. are predicted to make strides in oncology and cardiology, respectively, enhancing precision and patient safety in these critical areas. Medtronic, Zimmer Biomet, and Smith & Nephew are anticipated to expand their robotic-assisted offerings, integrating advanced technologies to address complex surgical needs and improve surgical outcomes across various specialties.

The collaborative efforts and innovative strategies of these key players are expected to propel the medical robots market toward new heights, ultimately transforming healthcare delivery and patient care on a global scale.

Market Key Players

- iRobot Corporation

- Medrobotics Corporation

- Titan Medical Inc.

- Renishaw Plc

- Health Robotics SLR

- OR Productivity plc

- Intuitive Surgical

- Mako Surgical Corp.

- Varian Medical Systems

- Stereotaxis Inc.

- Mazor Robotics

- Medtronic

- Stryker

- Zimmer Biomet

- Smith & Nephew

Recent Development

- In April 2024, Quantum Surgical, based in Montpellier, France, secured a €30 million loan from the European Investment Bank (EIB). This funding aims to advance the commercialization of its medical robot named Epione, which is designed for the minimally invasive treatment of lung and abdominal cancer.

- In January 2024, Stryker reported a record number of global installations for its Mako surgical robot during the fourth quarter of 2023. The company is set to expand the applications of Mako to spine surgery in the third quarter of 2024 and shoulder surgery by the end of the year

- In October 2023, Moon Surgical began its first U.S. clinical cases with the Maestro robotic surgical assistant in Jacksonville, Florida. By November 2023, the system was successfully used in surgeries in France. The Maestro system integrates into existing clinical workflows, providing surgeons with additional precision and control through its robotic arms.

Report Scope

Report Features Description Market Value (2023) USD 16.5 Billion Forecast Revenue (2033) USD 71.3 Billion CAGR (2024-2032) 16.2% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Equipment, Service, Consumables), By Product (Surgical Robots, Rehabilitation Robots, Noninvasive Radiosurgery Robots, Hospital and Pharmacy Robots, Others), By Application (Neurology, Oncology, Orthopedic Robotic Systems, Laparoscopy, Cardiology, Others), By Setting (Home-Care, In-Patient, Out-Patient), By End User (Hospitals & Clinics, Specialty Centers, Rehabilitation Centers, Others Source) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape iRobot Corporation, Medrobotics Corporation, Titan Medical Inc., Renishaw Plc, Health Robotics SLR, OR Productivity plc, Intuitive Surgical, Mako Surgical Corp., Varian Medical Systems, Stereotaxis Inc., Mazor Robotics, Medtronic, Stryker, Zimmer Biomet, Smith & Nephew Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- iRobot Corporation

- Medrobotics Corporation

- Titan Medical Inc.

- Renishaw Plc

- Health Robotics SLR

- OR Productivity plc

- Intuitive Surgical

- Mako Surgical Corp.

- Varian Medical Systems

- Stereotaxis Inc.

- Mazor Robotics

- Medtronic

- Stryker

- Zimmer Biomet

- Smith & Nephew

Our Clients

View Our Licence Options